Polymer Foam Market Outlook:

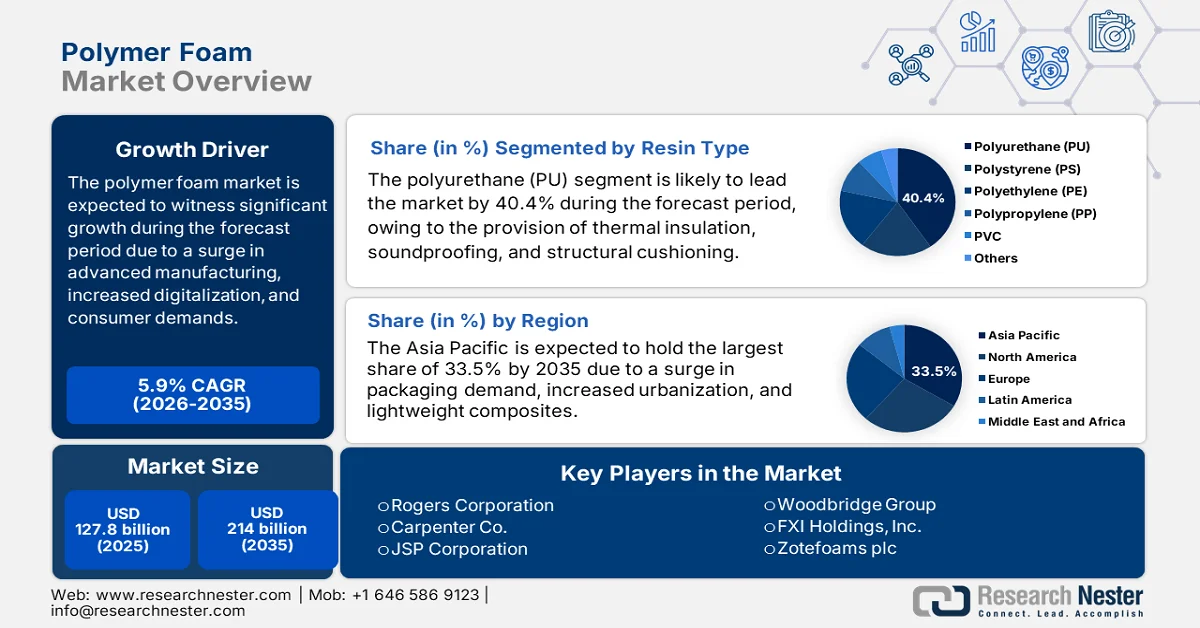

Polymer Foam Market size was over USD 127.8 billion in 2025 and is expected to reach USD 214 billion by the end of 2035, growing at a CAGR of 5.9% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of polymer foam is evaluated at USD 135.3 billion.

The worldwide polymer foam market is rapidly evolving, shaped by conventional demand in automotive and construction, newest technological, consumer-driven, and environmental factors, along with a shift in consumer expectations, advanced manufacturing, and digitalization. According to official statistics published by Heliyon in November 2024, there has been a significant growth in the utilization of lightweight composites, with a yearly increase of an estimated 5%. Besides, in terms of solid surface molding, the filler loading in solid surface products usually ranges between 50% and 65%. Additionally, to enhance the physical characteristics and gain a stabilized result, these products are post-cured at increased temperatures, thereby making them suitable for boosting the market’s growth and expansion across different nations.

Furthermore, the digital manufacturing integration, smart foams for electronics, and circular economy partnerships are certain trends that are also bolstering the polymer foam market globally. As per an article published by NLM in May 2022, the digitalized technological level index of the manufacturing industry in China increased from 0.286 to 0.359. In addition, the effect of digital technology on upscaling the domestic industry is significantly positive at 5% level, along with an influence coefficient of 0.129. Moreover, the domestic digital technology is utilized in a large proportion, with an efficient international digital technology, with coefficients ranging from 0.124 to 0.703. Meanwhile, the capital-intensive industries and technology-intensive industries account for 0.124 and 0.108 coefficients, thereby denoting an optimistic outlook for the market expansion.

Key Polymer Foam Market Insights Summary:

Regional Highlights:

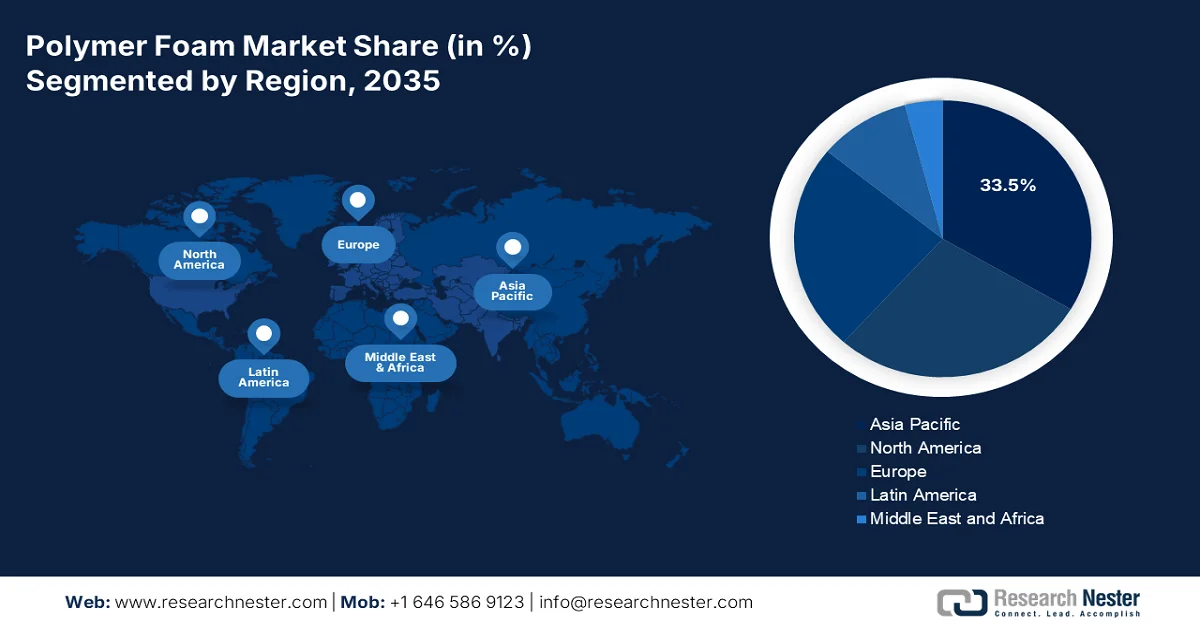

- Asia Pacific polymer foam market is projected to hold a dominant 33.5% share by 2035, fueled by rising packaging demand, automotive lightweighting, and rapid urbanization

- Europe region is anticipated to witness the fastest growth in the forecast period to 2035, stimulated by increasing adoption of sustainable chemical innovations and energy-efficient construction insulation

Segment Insights:

- Polyurethane (PU) segment in the polymer foam market is expected to command a 40.4% share by 2035, driven by its extensive application in soundproofing, cushioning, and thermal insulation across industries

- Rigid foam segment is projected to capture a 52.6% share by 2035, attributed to its superior insulation performance and structural durability in construction and industrial applications

Key Growth Trends:

- Expansion in healthcare

- Increase in renewable energy infrastructure

Major Challenges:

- Raw material price volatility

- Environmental regulations and sustainability pressure

Key Players: BASF SE (Germany), Covestro AG (Germany), Dow Inc. (U.S.), Huntsman Corporation (U.S.), Recticel NV (Belgium), Armacell International S.A. (Luxembourg), Sekisui Chemical Co., Ltd. (Japan), Toray Industries, Inc. (Japan), Ube Industries, Ltd. (Japan), Mitsui Chemicals, Inc. (Japan), Rogers Corporation (U.S.), Carpenter Co. (U.S.), JSP Corporation (Japan), Woodbridge Group (Canada), FXI Holdings, Inc. (U.S.), Zotefoams plc (UK), Vitafoam International Ltd. (UK), Reliance Industries Limited (India), LG Chem Ltd. (South Korea), Chemrez Technologies, Inc. (Malaysia).

Global Polymer Foam Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 127.8 billion

- 2026 Market Size: USD 135.3 billion

- Projected Market Size: USD 214 billion by 2035

- Growth Forecasts: 5.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (33.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Vietnam, Indonesia, Mexico

Last updated on : 17 March, 2026

Polymer Foam Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in healthcare: Polymer foams are effectively utilized in hospital bedding, prosthetics, and medical cushioning, which is driven by a rise in healthcare infrastructure investments globally. According to official statistics published by OECD in November 2025, the spending share on healthcare accounts for 9.3% of gross domestic product (GDP), which is above 8.8%. Besides, the per-person expenditure on health amounts to USD 5,000 on average. This usually ranges from USD 12,555 in the U.S. to USD 1,181 in Mexico. Moreover, population ageing is one of the reasons for the increased healthcare demand and provides long-lasting care services, with 18% of the population aged more than 65 years, thus positively impacting the polymer foam market’s growth.

- Increase in renewable energy infrastructure: The polymer foam market is significantly adopted beyond wind turbines, particularly for energy storage systems and solar panel insulation. As per an article published by the IEA Organization in 2026, the worldwide investment in battery energy storage has surpassed USD 20 billion as of 2022. This is predominantly due to grid-scale development, which demonstrated more than 65% of the overall expenditure within the same year. Moreover, this particular investment further hit another record, deliberately exceeding USD 35 billion as of 2023. This growth is effectively based on the current project pipeline targets that have been set by governments. Therefore, with this ongoing investment provision in energy storage systems, the market is gradually expanding.

- Focus on lifestyle and urban furniture demand: The aspect of rapid urbanization is successfully fueling the demand for lifestyle products, mattresses, and ergonomic furniture, which is positively impacting the polymer foam market. As stated in an article published by NLM in January 2023, the suitable association between urbanization and physical activity accounts for 138,206 adults residing across 698 communities across 22 countries. Besides, an estimated 55% of the worldwide population resides in urban locations, which is further projected to increase by 68%, that is, roughly 7 billion people, by the end of 2050. Furthermore, 90% of this increase is expected to occur in Africa and Asia, thereby denoting a huge growth opportunity for the market exposure across different nations.

Challenges

- Raw material price volatility: The polymer foam market is heavily dependent on petrochemical feedstocks such as polyurethane, polystyrene, and polyethylene. Fluctuations in crude oil prices directly impact the cost of these raw materials, creating uncertainty for manufacturers and end users. For instance, geopolitical tensions and supply chain disruptions can cause sudden spikes in oil prices, raising production costs and squeezing profit margins. This volatility makes long-term planning difficult for companies, especially those with global operations. Additionally, the transition toward bio-based alternatives, while promising, is still expensive and not yet widely scalable. As a result, firms face the dual challenge of managing unpredictable petrochemical costs while investing in sustainable alternatives.

- Environmental regulations and sustainability pressure: Governments worldwide are tightening regulations on plastics and chemical waste, directly impacting the production process of the polymer foam market. The EPA’s Green Chemistry Program and the EU’s Circular Economy Action Plan mandate reductions in hazardous waste and encourage recycling initiatives. While these policies promote sustainability, they also increase compliance costs for manufacturers. Foam producers must invest in cleaner technologies, waste management systems, and bio-based alternatives to meet regulatory standards. Besides, the failure to comply can result in fines, reputational damage, and restricted market access. Moreover, consumer demand for eco-friendly products is rising, forcing companies to accelerate innovation in biodegradable and recyclable foams.

Polymer Foam Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.9% |

|

Base Year Market Size (2025) |

USD 127.8 billion |

|

Forecast Year Market Size (2035) |

USD 214 billion |

|

Regional Scope |

|

Polymer Foam Market Segmentation:

Resin Type Segment Analysis

By the end of the stipulated timeline, the polyurethane (PU) segment under the resin type is expected to account for the largest of 40.4% share in the polymer foam market. The segment’s development is effectively propelled by its role for acting as a premier material for soundproofing, structural cushioning, and thermal insulation across different industries, such as construction, automotive, and furniture. As per an article published by the Polyurethanes Organization in 2026, existing projects demonstrate that recovery schemes tend to diminish the volume of polyurethane waste, with over 250,000 tons in Europe being recovered and recycled every year. Besides, domestic refrigerators utilizing polyurethane as an insulator gained energy effectiveness of 37% in the upcoming 10 years, thus boosting the segment’s growth.

Foam Type Segment Analysis

The rigid foam segment, which is part of the foam type, is anticipated to garner the largest share of 52.6% in the polymer foam market by the end of 2035. The segment’s upliftment is highly driven by its superior thermal insulation, structural strength, and durability, making it indispensable in construction, automotive, and industrial applications. In the construction sector, rigid polyurethane and polystyrene foams are widely used for wall insulation, roofing, and flooring, helping reduce energy consumption in residential and commercial buildings. Government initiatives promoting energy-efficient infrastructure, such as the U.S. Department of Energy’s Building Technologies Program, are accelerating adoption. Therefore, with such strategies, there is a huge growth opportunity for the segment in the overall market internationally.

Functionality Segment Analysis

The thermal insulation foams sub-segment in the polymer foam market is projected to hold the second-largest share during the forecast duration. The sub-segment’s growth is highly fueled by its extremely low thermal conductivity that reduces heat transfer through conduction, radiation, and convection. This optimizes energy effectiveness in industrial and construction applications, especially for spray foam, insulation boards, and refrigerated transport. According to official statistics published by NLM in January 2025, the blending of starch in the thermo insulation performance optimized to 0.043 W/mK, along with 20% weight percentage of PBAT, owing to the enhanced extension ratio as well as cell morphology. Therefore, with such improvements, the sub-segment is continuously growing globally.

Our in-depth analysis of the polymer foam market includes the following segments:

|

Segment |

Subsegments |

|

Resin Type |

|

|

Foam Type |

|

|

Functionality |

|

|

Application |

|

|

End use Industry |

|

|

Product Form |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polymer Foam Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the polymer foam market is anticipated to garner the highest share of 33.5% by the end of 2035. The market’s upliftment in the region is highly attributed to the existence of government-based sustainability programs, an increase in packaging demand, automotive lightweighting, and urbanization. According to official statistics published by OECD in July 2025, plastic utilization in Southeast and East Asia has readily increased from 17 million tons to 152 million tons as of 2022. In addition, China presently accounts for almost 70% of the overall regional plastic utilization and 19% for the remaining countries in the region. Moreover, in terms of packaging, the APT average plastics utilization per capita is 67 kg in the region, with 29 kg in Indonesia and more than 100 kg in Korea and Japan. Therefore, the increased use of plastics in the country is suitable for construction purpose thereby uplifting the market growth in the region.

2024 Plastic Building Materials Export and Import in the Asia Pacific

|

Countries |

Export (USD) |

Import (USD) |

|

China |

3.3 billion |

4.4 billion |

|

Vietnam |

279 million |

153 million |

|

South Korea |

101 million |

50.3 million |

|

Philippines |

42.7 million |

97.4 million |

|

Thailand |

42.6 million |

96 million |

|

Malaysia |

87.5 million |

123 million |

|

India |

85.8 million |

94.3 million |

|

Japan |

37.4 million |

152 million |

Source: OEC

The polymer foam market in China is growing significantly, owing to the presence of a huge construction industry, automotive production, packaging demand, stringent sustainability standards, advanced chemical technologies, and an increase in funding opportunities. Based on government estimates published by the ITA in September 2025, the country remains the world’s largest construction industry, which is valued at approximately USD 4.8 trillion as of 2025. Besides, with an urbanization rate accounting for 67% in 2024, the industry’s demand is more stabilized across Tier 1 cities, such as Shanghai and Beijing, significantly driving the focus on sustainable alignment and construction. Moreover, the construction industry in the nation is responsible for more than 50% of domestic carbon dioxide emissions, thereby making it suitable for fueling the market demand.

The aspects of rapid urbanization, infrastructure expansion, government-backed chemical advancement, sustainable chemical technologies, generous investments, and robust industrial alignment are factors that are responsible for uplifting the polymer foam market in India. Based on government estimates published by the ITA in January 2024, the diversified chemicals industry in the country covers more than 80,000 commercial products. Besides, the chemical industry is significantly valued at USD 220 billion and is further predicted to grow by 9% to 12% per year to reach USD 300 billion by the end of 2026. Moreover, the specialty chemical industry is anticipated to significantly contribute to total industry growth and is projected to reach USD 40 billion by the end of 2026, thus proliferating the market growth and expansion in the overall country.

Europe Market Insights

Europe in the polymer foam market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by sustainable chemical innovations, construction insulation, packaging, automotive lightweight materials, along with polyurethane foams dominating, owing to thermal efficiency. According to official statistics published by Energy and Buildings in September 2023, traditional and historic buildings constitute an estimated 25% of the regional building stock. These particular buildings tend to significantly hold cultural and architectural value, and further account for almost 40% of overall energy consumption and 36% of carbon dioxide emissions from the regional building stock. Therefore, with such development in building stock, there is a huge growth opportunity for the market in the overall region.

The polymer foam market in Germany is gaining increased traction, owing to government-based sustainability programs, a strong chemical industry, prioritizing funding opportunities for sustainable materials, and green chemical approaches. As per an article published by Green Carbon in March 2024, 373 million tons of plastic have been produced from fossil raw materials as per calculations by the German Nova Institute. Besides, the Plastics Europe industry association estimated the production of plastics to account for 391 million tons, and meanwhile, the OECD Global Plastics Outlook of the Organization of Economic Cooperation and Development predicted roughly 600 million tons of plastics to be produced by the end of 2060. Moreover, roughly 60% of all polymers, such as packaging materials, shopping bags, and mulch films are produced for single utilization, thus fueling the market development in the country.

The aspects of strong government support for circular economy initiatives, sustainable chemical production, generous industrial budget, and an increased focus on advanced materials research are factors bolstering the polymer foam market in France. As stated in an article published by the CEFIC Organization in 2024, the chemical industry in the country accounts for a turnover worth USD 126 billion as of 2023, which is generated by over 4,000 organizations. In addition, the country is regarded as the second-largest chemical producer in the whole of Europe, with USD 2.3 billion as an investment for thorough research and development. Moreover, there are a total of 177,000 direct employees in companies from this particular industry, along with USD 9.3 billion in capital expenditure, thus denoting a huge growth opportunity for the polymer foam market in the overall country.

North America Market Insights

North America in the polymer foam market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by a robust demand in packaging, automotive light weighting, construction insulation, along with the government’s sustainable building materials and energy efficiency. According to official statistics published by National Academies of Sciences, Engineering, and Medicine in 2022, an estimated 1/5th, which 19%, of the international plastic production occurred in the region. Besides, the America Chemistry Council’s (ACC) methodology is indicated to readily cover 95% to 100% of overall production in both the U.S. and Canada. Moreover, there has been the production of 41.1 million metric tons of plastic resins in the overall region, which is positively impacting the market growth.

The polymer foam market in the U.S. is gaining increased exposure, owing to lightweight automotive materials, energy-efficient construction, sustainability regulations, and an increase in packaging demand. As per an article published by the EPA Government in October 2025, packaging and containers significantly make up a massive portion of municipal solid waste, amounting to 82.2 million tons of generation. Moreover, the recycling rate of generated packaging and containers has been 53.9%. In addition, the combustion accounts for 7.4 million tons, which is 21.5% of the overall combustion with energy recovery, as well as landfills receiving 30.5 million tons, which is 20.9% of the total landfilling. Therefore, based on these recycling strategies, there is a huge growth opportunity for the market in the country.

The insulation in sustainable buildings, e-commerce packaging growth, automotive applications, and bio-based innovation are certain factors that are bolstering the polymer foam market in Canada. As stated in an article published by the Government of Canada in January 2026, the domestic Net-Zero Emissions Accountability Act enshrined in legislation for the government’s projected commitment to diminish greenhouse gas emissions by 40% to 45% by the end of 2030 and gain net-zero emissions by the end of 2050. Besides, buildings account for 18% of the country’s emissions, including electricity-based emissions. Additionally, all buildings’ operating emissions account for more than 96%, originating from space and water heating by utilizing fossil fuels, including boilers and natural gas furnaces, thereby making it suitable for fueling the market in the country.

Key Polymer Foam Market Players:

- BASF SE (Germany)

- Covestro AG (Germany)

- Dow Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Recticel NV (Belgium)

- Armacell International S.A. (Luxembourg)

- Sekisui Chemical Co., Ltd. (Japan)

- Toray Industries, Inc. (Japan)

- Ube Industries, Ltd. (Japan)

- Mitsui Chemicals, Inc. (Japan)

- Rogers Corporation (U.S.)

- Carpenter Co. (U.S.)

- JSP Corporation (Japan)

- Woodbridge Group (Canada)

- FXI Holdings, Inc. (U.S.)

- Zotefoams plc (UK)

- Vitafoam International Ltd. (UK)

- Reliance Industries Limited (India)

- LG Chem Ltd. (South Korea)

- Chemrez Technologies, Inc. (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF SE is one of the largest chemical producers globally, with a strong presence in polymer foams, particularly polyurethane and polystyrene, used in construction and automotive applications. The company emphasizes sustainability, investing in circular economy solutions and bio-based foam innovations to reduce environmental impact.

- Covestro AG specializes in high-performance polymers and is a leading supplier of polyurethane foams for insulation and automotive lightweighting. The company has committed to becoming fully circular, focusing on climate-neutral production and resource-conserving technologies.

- Dow Inc. is a major player in polymer foams, producing polyurethane, polystyrene, and polyethylene foams for packaging, construction, and automotive industries. The company leverages advanced R&D to develop sustainable foam solutions, aligning with global energy efficiency and recycling initiatives.

- Huntsman Corporation is a global leader in MDI-based polyurethanes, offering both rigid and flexible foams for diverse applications, including construction, automotive, and furniture. With production facilities across the U.S., Europe, and Asia, Huntsman emphasizes tailored solutions and innovation in polyurethane chemistry.

- Recticel NV specializes in polyurethane-based flexible foams, serving industries such as transportation, healthcare, and construction. The company focuses on sustainable growth, leveraging emerging markets and compliance with low-VOC regulations to strengthen its competitive position.

Here is a list of key players operating in the global polymer foam market:

The international polymer foam market is highly competitive, dominated by multinational corporations such as BASF, Covestro, and Dow, alongside regional leaders in the Asia Pacific, such as Sekisui Chemical and LG Chem. Strategic initiatives include sustainability-driven R&D, partnerships for bio-based foams, and capacity expansions in emerging markets. For instance, BASF has invested heavily in circular economy solutions, while Covestro focuses on low-carbon polyurethane foams. Moreover, Asia-based players are leveraging cost advantages and government-backed innovation programs to expand market share. Besides, in July 2025, Jennmar successfully acquired Weber Mining and Tunnelling SAS, along with its subsidiaries. Weber’s proprietary foam and resin product portfolio has been evolving to meet the demands of the mining sector, thus making it suitable for uplifting the polymer foam industry.

Corporate Landscape of the Polymer Foam Market:

Recent Developments

- In December 2025, BASF introduced a modernized amine catalyst, known as Lupragen N 208, to its portfolio of Lupragen amine catalysts for the production of polyurethane (PU) foams that are readily integrated into the PU polymer network during foam production.

- In September 2025, Asahi Kasei unveiled its newest advancement in PFAS-free polyamide (PA) and recycling technology of continuous carbon fibers for automotive applications, for optimizing lightweight and connectivity.

- In May 2025, Borealis invested more than USD 115 million in the latest High Melt Strength polypropylene (HMS PP) line at its Burghausen, Germany, facility through sustainable solutions that are focused in transforming the polymer industry.

- Report ID: 8443

- Published Date: Mar 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.