Pharmaceutical CDMO 2.0 Market Outlook:

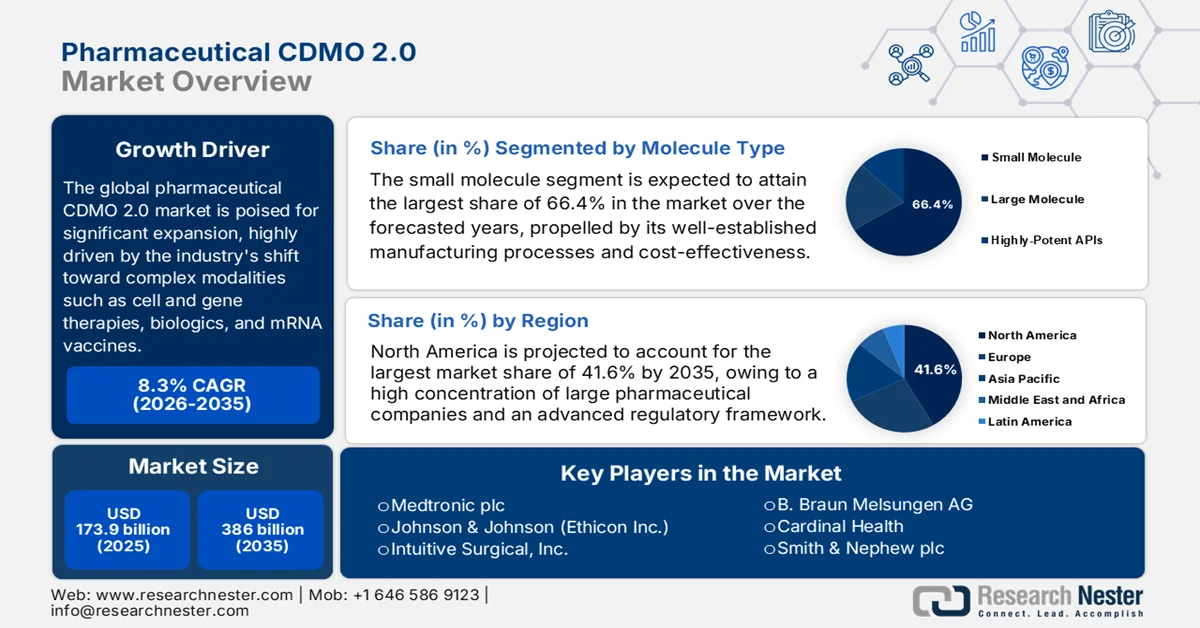

Pharmaceutical CDMO 2.0 Market size was valued at USD 173.9 billion in 2025 and is projected to exceed USD 386 billion by the end of 2035, expanding at over 8.3% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of pharmaceutical CDMO 2.0 is assessed at USD 188.3 billion.

The global pharmaceutical CDMO 2.0 market is poised for extensive growth, effectively driven by the industry's shift toward complex modalities such as cell and gene therapies, biologics, and mRNA vaccines. This outsourcing trend is characterized by a shift from traditional fee-for-service arrangements to strategic, long-term partnerships, where CDMOs function as integrated co-development partners and extensions of pharmaceutical companies throughout the drug development and manufacturing process. According to an article published by the National Institute of Health (NIH) in March 2022, CDMOs have become a central aspect of biopharmaceutical production due to the rising complexity and volume of biologics such as monoclonal antibodies and gene therapies. The article also notes that biologics have expanded remarkably, with their share of top drug sales projected to exceed 50% by the end of 2026, solidifying the need for specialized external manufacturing capabilities, thus positively impacting the market’s growth.

Furthermore, the pharmaceutical CDMO 2.0 market is witnessing stronger strategic collaborations between pharmaceutical innovators and CDMOs, wherein sponsors are looking for long-term partners who are capable of accelerating development timelines, enhancing supply chain resilience, and supporting global commercialization. In addition, the shift toward one-stop-shop service models, expansion of biologics capacity, and growing investments in advanced manufacturing infrastructure are expected to solidify the outlook for the Pharmaceutical CDMO 2.0 industry over the coming years. For instance, in June 2023, Samsung Biologics and Pfizer announced a long-term strategic partnership to manufacture Pfizer’s biosimilars portfolio in oncology, inflammation, and immunology. The company outlined that production will take place at Samsung’s newly completed Plant 4, expanding large-scale manufacturing capacity, thus suitable for bolstering global pharmaceutical CDMO 2.0 market growth.

Key Pharmaceutical CDMO 2.0 Market Insights Summary:

Regional Highlights:

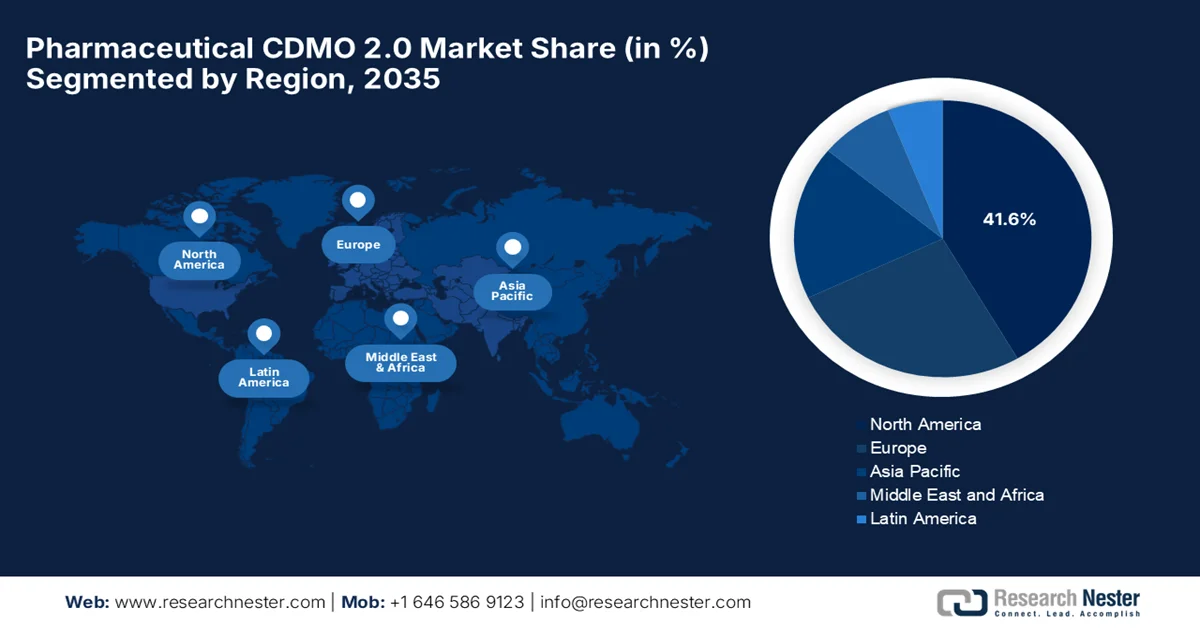

- North America is anticipated to command 41.6% of the pharmaceutical cdmo 2.0 market by 2035, underpinned by the strong presence of pharmaceutical and biotechnology leaders, advanced regulatory frameworks, and extensive outsourcing of complex drug development and manufacturing activities.

- Asia Pacific is projected to witness the fastest expansion throughout 2026–2035, bolstered by the rapid rise of domestic biotechnology startups and an accelerating focus on biosimilars, advanced biologics, and cell and gene therapies.

Segment Insights:

- The small molecule segment is expected to account for 66.4% of the pharmaceutical cdmo 2.0 market by 2035, reinforced by well-established manufacturing processes, cost-effectiveness, and the widespread adoption of oral solid dosage forms.

- API development and manufacturing is poised to capture a noteworthy share of the market during 2026–2035, stimulated by increasing outsourcing of complex small-molecule synthesis and rising demand for generic and specialty drugs requiring scalable outsourced API production.

Key Growth Trends:

- Growth of cell and gene therapy pipelines

- Digitalization and industry 4.0 adoption

Major Challenges:

- High capital investment requirements

- Increasing regulatory complexity

Key Players: Lonza Group, Catalent, Inc., Thermo Fisher Scientific Inc. (Patheon), Samsung Biologics Co., Ltd., WuXi Biologics, FUJIFILM Diosynth Biotechnologies, Boehringer Ingelheim BioXcellence, Siegfried Holding AG, Recipharm AB, AGC Biologics, Piramal Pharma Solutions, Syngene International Limited, Laurus Labs Limited, Curia Global, Inc., CordenPharma, AmbioPharm, Genetix Biotherapeutics, Eli Lilly and Company, Lone Star Funds, Aenova Group, Fareva, Pfizer CentreOne, IDT Australia Limited, Duopharma Biotech Berhad, Blue Jet Healthcare Limited.

Global Pharmaceutical CDMO 2.0 Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 173.9 billion

- 2026 Market Size: USD 188.3 billion

- Projected Market Size: USD 386 billion by 2035

- Growth Forecasts: 8.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (41.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Singapore, South Korea, Switzerland, Ireland, Australia

Last updated on : 4 June, 2026

Pharmaceutical CDMO 2.0 Market - Growth Drivers and Challenges

Growth Drivers

- Growth of cell and gene therapy pipelines: This factor is stimulating consistent growth in the pharmaceutical CDMO 2.0 market. The cell and gene therapies require specialized manufacturing systems, viral vector production, and strict quality environments. Also, the pharmaceutical companies depend on CDMOs for technical expertise, scalable platforms, and compliance support to manage complex development and commercialization requirements effectively. The American Society of Gene + Cell Therapy in January 2025 revealed that globally, clinical approvals include 33 gene therapies, such as Autolus’ AUCATZYL for relapsed or refractory B-cell precursor acute lymphocytic leukemia. There is a total of 35 RNA therapies, with Ionis Pharmaceuticals’ TRYNGOLZA approved for lipoprotein lipase deficiency. In addition, 72 non-genetically modified cell therapies have been cleared, including StemCyte’s REGENECYTE for transplantation in blood and immune disorders, denoting encouraging opportunities for players in this field.

Global Approved Gene Therapy Market Landscape Q4 2024: Comprehensive List of All Commercially Approved Gene, Cell, CAR-T, RNA, and Genome Editing Therapies Worldwide

|

Product Name |

Generic Name |

Year First Approved |

Diseases |

Locations Approved |

Originator Company |

|

Tecartus |

brexucabtagene autoleucel |

2020 |

Mantle cell lymphoma; acute lymphocytic leukemia |

U.S., Europe, UK, Australia, Canada |

Kite Pharma (Gilead) |

|

Libmeldy |

atidarsagene autotemcel |

2020 |

Metachromatic leukodystrophy |

EU, UK, Switzerland, U.S. |

Orchard Therapeutics |

|

Breyanzi |

lisocabtagene maraleucel |

2021 |

Diffuse large B-cell lymphoma; follicular lymphoma; chronic lymphocytic leukemia; mantle cell lymphoma. |

U.S., Japan, Europe, Switzerland, UK, Canada |

Celgene (Bristol Myers Squibb) |

|

Abecma |

idecabtagene vicleucel |

2021 |

Multiple myeloma |

U.S., Canada, Europe, UK, Japan, Israel, Switzerland |

bluebird bio |

|

Delytact |

teserpaturev |

2021 |

Malignant glioma |

Japan |

Daiichi Sankyo |

|

Relma-cel |

relmacabtagene autoleucel |

2021 |

Diffuse large B-cell lymphoma; follicular lymphoma; mantle cell lymphoma |

China |

JW Therapeutics |

|

Skysona |

elivaldogene autotemcel |

2021 |

Early cerebral adrenoleukodystrophy (CALD) |

U.S. |

bluebird bio |

|

Carvykti |

ciltacabtagene autoleucel |

2022 |

Multiple myeloma |

U.S., Europe, UK, Japan, Brazil, Australia, Canada, China |

Legend Biotech |

|

Upstaza |

eladocagene exuparvovec |

2022 |

AADC deficiency |

Europe, UK, Israel, U.S. |

PTC Therapeutics |

|

Roctavian |

valoctocogene roxaparvovec |

2022 |

Hemophilia A |

Europe, U.S. |

BioMarin |

|

Hemgenix |

etranacogene dezaparvovec |

2022 |

Hemophilia B |

U.S., Europe, UK, Canada, Switzerland |

uniQure |

|

Adstiladrin |

nadofaragene firadenovec |

2022 |

Bladder cancer |

U.S. |

Merck & Co. |

|

Elevidys |

delandistrogene moxeparvovec |

2023 |

Duchenne muscular dystrophy |

U.S. |

Sarepta Therapeutics |

|

Vyjuvek |

beremagene geperpavec |

2023 |

Dystrophic epidermolysis bullosa |

U.S. |

Krystal Biotech |

|

Fucaso |

equecabtagene autoleucel |

2023 |

Multiple myeloma |

China |

Nanjing IASO Biotechnology |

|

Casgevy |

exagamglogene autotemcel |

2023 |

Sickle cell anemia; thalassemia |

U.S., UK, Bahrain, Saudi Arabia, Europe, Canada, Switzerland |

CRISPR Therapeutics |

|

inaticabtagene autoleucel |

inaticabtagene autoleucel |

2023 |

Acute lymphocytic leukemia |

China |

Juventas Cell Therapy |

|

Lyfgenia |

lovotibeglogene autotemcel |

2023 |

Sickle cell anemia |

U.S. |

bluebird bio |

|

zevorcabtagene autoleucel |

zevorcabtagene autoleucel |

2024 |

Relapsed or refractory multiple myeloma |

China |

CARsgen Therapeutics |

|

Beqvez |

fidanacogene elaparvovec |

2024 |

Hemophilia B |

Canada, U.S., Europe |

Pfizer |

|

Tecelra |

afamitresgene autoleucel |

2024 |

Synovial sarcoma |

U.S. |

Adaptimmune |

|

Aucatzyl |

obecabtagene autoleucel |

2024 |

Acute lymphocytic leukemia |

U.S. |

Autolus |

Source: ASGCT

- Digitalization and industry 4.0 adoption: The continued adoption of digital technologies and industry 4.0 solutions is effectively transforming pharmaceutical CDMO 2.0 operations. AI-based analytics, automation, and continuous manufacturing enhance efficiency, yield, and quality control, thereby prompting a profitable business environment for the pharmaceutical CDMO 2.0 market. These advancements improve supply chain visibility and reduce production failures, thereby strengthening operational excellence across global CDMO networks. For instance, in September 2024, Merck and Siemens signed a strategic MoU in order to advance digital transformation and smart manufacturing across Merck’s three business sectors. Siemens was named a preferred global supplier, with its Xcelerator platform driving modular, flexible, and sustainable production, thus denoting a positive pharmaceutical CDMO 2.0 market outlook.

Key Pharmaceutical CDMO 2.0 Market Opportunities Driven by Strategic Investments, Acquisitions, and Capacity Expansions 2022 - 2025

|

Company |

Year |

Key Development |

Pharmaceutical CDMO 2.0 Market Opportunity |

|

Samsung Biologics |

2025 |

Acquisition of Human Genome Sciences from GSK, adding a U.S.-based biologics manufacturing site with 60,000 L capacity. |

Strengthens global CDMO networks, supply chain resilience, and multi-site commercial manufacturing capabilities. |

|

AbbVie |

2024 |

USD223 million investment to expand biologics manufacturing capacity in Singapore. |

Enhances large-scale biologics production, advanced manufacturing capacity, and Asia-Pacific biopharma innovation. |

|

Lonza |

2022 |

Expansion of HPAPI multipurpose suite in Visp for ADC payload-linker development and manufacturing. |

Supports growth in antibody-drug conjugates, targeted oncology therapies, and integrated end-to-end CDMO services. |

Source: Company Official Press Releases

Challenges

- High capital investment requirements: One of the main challenges in the pharmaceutical CDMO 2.0 market is the extensive capital investments that are required to establish and maintain these advanced manufacturing capabilities. Modern CDMOs are expected to provide services for biologics, antibody-drug conjugates, cell and gene therapies, peptides, and highly potent active pharmaceutical ingredients, all of which necessitate specialized facilities, equipment, and stringent containment systems. Therefore, building and validating these facilities can require huge costs and time before generating meaningful returns. In addition, companies need to make investments in automation, digital manufacturing technologies, and quality systems in order to remain competitive. Apart from this, smaller CDMOs in this field struggle to achieve sufficient funding for expansion, whereas larger players face pressure to achieve high facility utilization rates to justify ongoing investments.

- Increasing regulatory complexity: Pharmaceutical CDMO 2.0 providers work under a highly regulated environment in which compliance requirements have become more stringent in most markets. The CDMOs need to comply with good manufacturing practice standards, data integrity requirements, environmental regulations, and product-specific guidelines for complex therapies. Apart from this, regulatory processes are complex for biologics, cell therapies, gene therapies, and sterile manufacturing operations. Any type of inspection observations, warning letters, or quality failures can damage client relationships and disrupt business operations. Furthermore, serving multinational pharmaceutical customers requires compliance with multiple regulatory agencies, which simultaneously increases administrative burden and operational complexity, thereby negatively impacting the growth of the pharmaceutical CDMO 2.0 market.

Pharmaceutical CDMO 2.0 Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.3% |

|

Base Year Market Size (2025) |

USD 173.9 billion |

|

Forecast Year Market Size (2035) |

USD 386 billion |

|

Regional Scope |

|

Pharmaceutical CDMO 2.0 Market Segmentation:

Molecule Type Segment Analysis

On the basis of molecule type, small molecule is expected to attain the largest share of 66.4% in the pharmaceutical CDMO 2.0 market over the forecasted years. The segment’s dominance is majorly propelled by its well-established manufacturing processes, cost-effectiveness, and widespread use in oral solid dosage forms, which continue to represent the backbone of global pharmaceutical production. For instance, in May 2023, Cingulate Inc. announced the successful transfer of its small-molecule ADHD drug candidate CTx-1301, i.e., dexmethylphenidate manufacturing process, to Societal CDMO for clinical and commercial production, confirming readiness for Phase 3 supply. This collaboration specifically involved scaling up production of a tablet-based oral solid dosage formulation by using established CDMO infrastructure. Such instances highlight the prominence of small-molecule therapies that continue to rely on cost-efficient, scalable manufacturing processes and well-established oral dosage technologies.

Service Segment Analysis

The API development and manufacturing in the service category of the pharmaceutical CDMO 2.0 market is anticipated to grow with a noteworthy share during the discussed timeframe. The increasing outsourcing of complex small-molecule synthesis, where established chemical processes allow for scalable and cost-efficient production, is the main factor behind the segment’s leadership. Growth is also supported by rising demand for generic and specialty drugs, which rely heavily on outsourced API production to optimize cost, speed, and regulatory compliance. In January 2023, Sai Life Sciences inaugurated a new HPAPI manufacturing facility at its Bidar campus, which is designed to handle high-potent molecules with containment below 1 μg/m³. The 16,000 sq. ft. block includes advanced isolators, reactors, powder processing, QC testing, and deactivation facilities to support commercial-scale production, thus denoting a wider segment scope.

End user Segment Analysis

Large pharma in the end user segment is projected to grow with a considerable revenue share in the pharmaceutical CDMO 2.0 market by the conclusion of 2035. The segment’s growth is largely attributable to their dependence on outsourcing for both clinical and commercial manufacturing, cost optimization, and capacity flexibility, rather than maintaining fully in-house production networks. This shift is majorly driven by the need to reduce fixed capital expenditure, accelerate time-to-market for new drug launches, and access specialized CDMO capabilities for complex small molecules and biologics. In addition, big pharma uses CDMOs to manage end-to-end supply chains, regulatory compliance, and scalable manufacturing capacity. In March 2024, Roche entered into a definitive agreement with Lonza to sell its Genentech manufacturing facility in Vacaville, California, for USD 1.2 billion. In this context, around 750 Genentech employees will be offered employment by Lonza, whereas Roche’s products from the site will continue to be supplied during a transition period.

Our in-depth analysis of the pharmaceutical CDMO 2.0 market includes the following segments:

|

Segment |

Subsegments |

|

Molecule Type |

|

|

Service |

|

|

End user |

|

|

Development Phase |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Pharmaceutical CDMO 2.0 Market - Regional Analysis

North America Market Insights

The North America pharmaceutical CDMO 2.0 market is forecasted to emerge with a dominating share of 41.6% during the stipulated timeframe. The region’s dominance is highly fueled by the dense concentration of large pharmaceutical and biotechnology companies, an advanced regulatory framework, and strong adoption of outsourcing for complex drug development and manufacturing, which encourages both innovation and large-scale CDMO partnerships. In April 2026, PCI Pharma Services announced a sweeping expansion of its U.S. sterile fill-finish and drug-device delivery capabilities, which is backed by a generous investment of USD 1 billion. Central to this plan is a USD 100 million project at its San Diego campus, adding a high-speed isolator filling line for prefilled syringes and cartridges, set to double capacity by 2028, hence positively benefiting the region’s market.

A massive pipeline of complex modalities, especially cell and gene therapies, advanced biologics, and antibody-drug conjugates that demand highly specialized technical capabilities and flexible, single-use facility designs, is propelling the growth of the U.S. pharmaceutical CDMO 2.0 market. In addition, domestic drug developers prioritize strategic, end-to-end outsourcing partnerships when compared to traditional, transactional manufacturing models. In October 2025, the article published by the Parenteral Drug Association revealed that the U.S. FDA has introduced a pilot program to fast-track reviews of generic drug applications from companies manufacturing and testing in the U.S., aiming to strengthen domestic production. The report outlined that only 9% of active pharmaceutical ingredients are produced domestically, and there is a heavy reliance on China and India, whereas the initiative looks to reduce supply chain vulnerabilities, thereby providing encouraging opportunities for pharmaceutical CDMOs.

The Canada pharmaceutical CDMO 2.0 market is growing significantly as the country makes a shift toward robust domestic biomanufacturing capabilities and strategic, long-term drug development partnerships. Market growth is also being fueled by the federal Biomanufacturing and Life Sciences Strategy, which incentivizes the onshoring of critical medical supplies to establish health emergency preparedness and reduce heavy reliance on foreign supply chains. The article published by Drug Discovery Today in October 2025 states that the commercialization of cell and gene therapies in Canada is constrained by limited domestic manufacturing capacity and reliance on external GMP infrastructure. Besides, Health Canada-approved therapies such as Kymriah and Casgevy depend on complex, highly specialized manufacturing processes typically supported by CDMOs. This reflects Canada’s dependence on imported advanced therapies and external production ecosystems.

APAC Market Insights

In the Asia Pacific, the pharmaceutical CDMO 2.0 market is expected to register the fastest growth from 2026 to 2035. The region has been transitioning from a low-cost, transactional manufacturing hub into a highly sophisticated global center for co-development and innovation. Market momentum is heavily propelled by an unprecedented surge in domestic biotechnology startups and a strategic shift toward complex modalities, which include biosimilars, advanced biologics, and cell and gene therapies. For instance, in March 2024, Novartis announced a total of USD 256 million expansion of its biopharmaceutical manufacturing facility in Singapore in order to address rising demand for biologics in the regional market. The expansion will deploy digital and automation technologies to improve productivity and focus on the manufacturing of therapeutic antibody drugs for global supply, thus making it suitable for standard pharmaceutical CDMO 2.0 market growth.

The rapidly aging demographic, which fuels intense demand for specialized therapeutics such as oncology treatments, biosimilars, and regenerative cell and gene therapies are certain driver boosting the Japan pharmaceutical CDMO 2.0 market. To accelerate innovation, domestic pharmaceutical stalwarts and emerging biotech spinouts are engaging CDMOs much earlier in the drug development cycle, particularly for technically demanding peptide and antibody-drug conjugate pipelines. In July 2025, JCR Pharmaceuticals announced that it had been selected for Japan’s regenerative medicine CDMO subsidy program to support facility upgrades and workforce training to expand biomanufacturing capacity. In addition, the company is advancing its JUST-AAV gene therapy platform for targeted delivery across the blood-brain barrier, thus positively impacting the market’s growth.

The pharmaceutical CDMO 2.0 market in China is undergoing a profound structural evolution, making a shift from a massive, cost-efficient manufacturing base into a highly sophisticated, high-quality development ecosystem focused on global innovation and technological integration. Market momentum is heavily propelled by the domestic landscape, which is consolidating around deeply integrated, full-service partners that leverage massive scientific talent and closed-loop ecosystems to seamlessly navigate regulatory reviews. In February 2025, the NMPA issued the interim provisions on the management of designated domestic responsible persons, which were effective July 1, 2025. These rules primarily aim to strengthen oversight of overseas MAHs under China’s Drug Administration Law and Vaccine Administration Law. To support implementation, relevant modules in the National Pharmaceutical Business Application System were launched on November 14, 2024.

Europe Market Insights

Europe pharmaceutical CDMO 2.0 market is projected for exponential growth in the next decade as a predominant hub for complex therapeutic modalities and high-quality, sustainable drug development. To navigate Europe's regulatory landscapes, biopharma companies are making a shift from traditional transactional manufacturing, instead choosing deeply integrated, long-term co-development partnerships with CDMOs. This shift is further accelerated by European Union initiatives, which are aimed at strengthening health emergency preparedness and establishing localized, secure supply chains to protect against geopolitical disruptions. The Health Emergency Preparedness and Response Authority (HERA), together with the Belgian Presidency of the Council of the EU, announced the launch of the Critical Medicines Alliance in April 2024, in order to address shortages of essential medicines. This initiative unites the region’s Member States, industry, healthcare organizations, and civil society to strengthen supply security and reduce dependencies in the pharmaceutical chain. The alliance consists of more than 250 members and is highly focused on diversification, production capacity, and investment projects.

An industry-wide shift toward innovative modalities, especially messenger RNA technologies, advanced biologics, and regenerative cell and gene therapies, which require sophisticated bioprocessing capabilities, is the main factor driving the pharmaceutical CDMO 2.0 market in Germany. Domestic CDMOs are making heavy investments in terms of Industry 4.0 technologies, which include automated high-throughput screening, digital twin process simulation, and flexible, modular single-use facility architectures. For instance, in October 2024, Rentschler Biopharma announced its largest single investment at its Laupheim headquarters with the construction of a new buffer media station. This is a four-story facility that covers 3,400 square meters and will modernize production processes, enhance automation, and support sustainability goals, with completion expected by 2027 and full operation by 2028.

In the UK, the pharmaceutical CDMO 2.0 market is being driven by the exceptional academic research base and thriving biotechnology clusters. Growth in this market is accelerated by the government's Life Sciences Vision, which aims to solidify the country’s position as a global superpower by investing in advanced manufacturing infrastructure and streamlining domestic clinical trial pipelines. Consequently, the country’s market landscape is consolidating around end-to-end, agile partners that can fluidly bridge the gap between early-stage clinical trial supplies and large-scale, regulatory-compliant commercial formulation. In February 2026, FUJIFILM Biotechnologies unveiled a USD 505 million expansion at its Teesside site, thereby establishing the UK’s largest single-use biopharmaceutical CDMO facility with bioreactors up to 5,000 L and a total capacity of 19,000 L. Along with this, the new Bioprocess Innovation Centre UK doubles lab space and creates a global hub for biomanufacturing innovation and process development.

Key Pharmaceutical CDMO 2.0 Market Players:

- Lonza Group (Switzerland)

- Catalent, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (Patheon) (U.S.)

- Samsung Biologics Co., Ltd. (South Korea)

- WuXi Biologics (China)

- FUJIFILM Diosynth Biotechnologies (Japan)

- Boehringer Ingelheim BioXcellence (Germany)

- Siegfried Holding AG (Switzerland)

- Recipharm AB (Sweden)

- AGC Biologics (Japan)

- Piramal Pharma Solutions (India)

- Syngene International Limited (India)

- Laurus Labs Limited (India)

- Curia Global, Inc. (U.S.)

- CordenPharma (Germany)

- AmbioPharm (U.S.)

- Genetix Biotherapeutics (U.S.)

- Eli Lilly and Company (U.S.)

- Lone Star Funds (U.S.)

- Aenova Group (Germany)

- Fareva (France)

- Pfizer CentreOne (U.S.)

- IDT Australia Limited (Australia)

- Duopharma Biotech Berhad (Malaysia)

- Blue Jet Healthcare Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- SWOT Analysis

- Lonza Group is considered to be a dominant force in the pharmaceutical CDMO 2.0 market, which is offering integrated services across biologics, small molecules, cell and gene therapies, and commercial manufacturing. Besides, the company has proactively built a strong competitive position through continuous investment in large-scale biologics facilities, advanced manufacturing technologies, and end-to-end development capabilities.

- Thermo Fisher Scientific Inc., through its Patheon business, is among the largest integrated CDMOs globally. The company provides services spanning drug development, clinical trial manufacturing, commercial production, packaging, and supply chain management.

- Samsung Biologics Co., Ltd. is a prominent player in biologics manufacturing and is recognized for operating one of the world's largest biologics production capacities. The company is highly focused on monoclonal antibodies, biosimilars, antibody-drug conjugates, and next-generation biologics.

- Catalent, Inc. has registered itself as a leading CDMO that specializes in drug delivery technologies, biologics manufacturing, gene therapies, and oral dosage forms. The company has deliberately differentiated itself through proprietary formulation technologies and specialized expertise in terms of complex therapeutics.

- FUJIFILM Diosynth Biotechnologies has become a major player in the CDMO sector, propelled by remarkable investments in biologics, vaccine manufacturing, cell therapies, and microbial production technologies. The firm’s strategic focus is structured around advanced biopharmaceutical manufacturing, process innovation, and flexible production platforms that support both clinical and commercial-scale manufacturing.

Here is a list of key players operating in the global pharmaceutical CDMO 2.0 market:

The pharmaceutical CDMO 2.0 market is extremely competitive, which hosts global biologics specialists, integrated development-and-manufacturing providers, and emerging regional players. Leading players in this sector are expanding biologics, antibody-drug conjugates, cell and gene therapy, peptide, and high-potency API capabilities with a prime goal to address the heightening demand for complex therapeutics. Strategic initiatives adopted by the pioneers are capacity expansion through new manufacturing facilities, acquisitions in order to strengthen geographic reach, and the establishment of long-term partnerships with biotechnology firms. In January 2026, Asimov and AGC Biologics entered into a partnership to offer a cost-effective viral vector manufacturing approach using Asimov’s LV edge packaging system at AGC’s Milan Cell & Gene Center of Excellence. In addition, this single-plasmid transfection system simplifies production, reduces GMP plasmid costs, and minimizes supply chain risks when compared to traditional four-plasmid methods.

Corporate Landscape of the Pharmaceutical CDMO 2.0 Market:

Recent Developments

- In May 2026, CordenPharma announced the acquisition of AmbioPharm to expand its global peptide API capacity with facilities in South Carolina and Shanghai. The deal strengthens U.S. peptide manufacturing capabilities, adds advanced synthesis approaches such as SPPS, LPPS, and hybrid methods.

- In March 2026, Lonza and Genetix Biotherapeutics extended their manufacturing partnership to expand production of ZYNTEGLO at Lonza’s Houston facility for a reliable supply for growing patient demand.

- In March 2026, Samsung Biologics and Lilly announced it will establish a new Gateway Labs Korea site at Bio Campus II, providing infrastructure for up to 30 biotech startups. The collaboration strengthens Samsung Biologics’ role as a connector between early-stage innovation and global development, while expanding Lilly’s Catalyze360 network.

- In March 2026, Lonza signed an agreement to divest its Capsules & Health Ingredients business to Lone Star Funds for USD 3 billion, with upfront proceeds of USD 2.2 billion and a retained 40% stake. The transaction marks the final step in Lonza’s transformation into a pure-play CDMO, focused on high-growth pharmaceutical modalities.

- Report ID: 8607

- Published Date: Jun 04, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.