Pharmaceutical Cartridges Market Outlook:

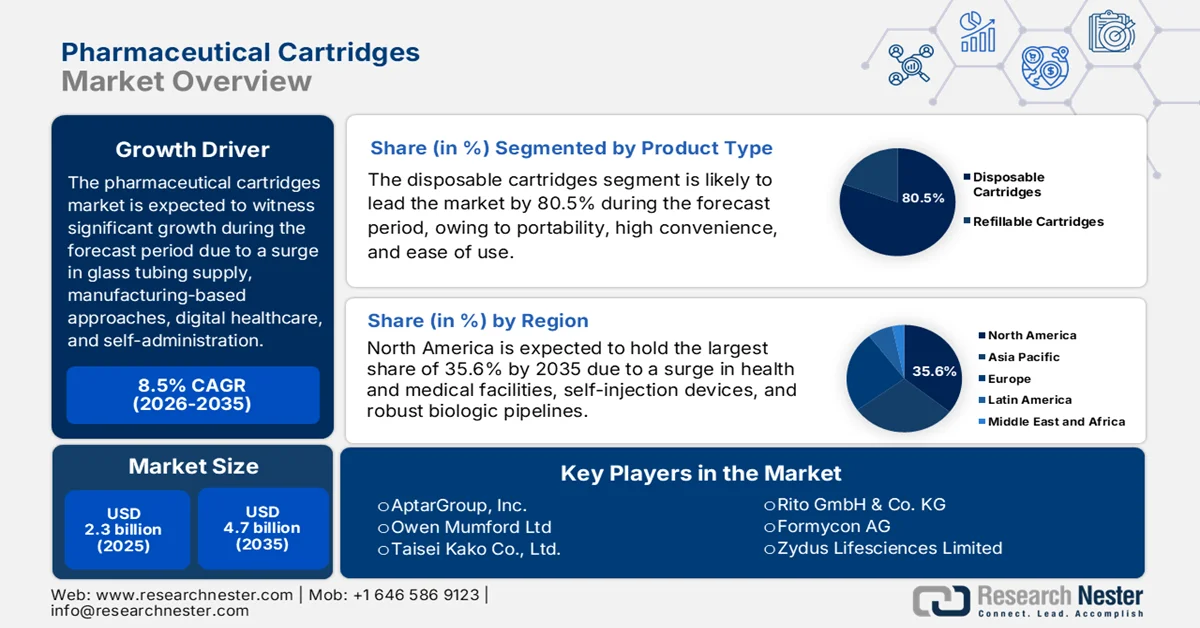

Pharmaceutical Cartridges Market size was worth more than USD 2.3 billion in 2025, which is further expected to reach USD 4.7 billion by the end of 2035, significantly growing at a CAGR of 8.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of pharmaceutical cartridges is assessed at USD 2.5 billion.

The global pharmaceutical cartridges market is significantly reshaped by several external and structural factors, including cross-border sourcing of glass tubing, specialized metal components, and polymer resins, manufacturers escalating nearshoring approaches and supplier diversification, and a sudden transition in healthcare delivery models towards home-driven care and self-administration. According to official statistics published by OEC in April 2026, in terms of sourcing polymer resins, China is regarded as the top exporter, with a valuation worth USD 1 billion, and the U.S. is the top importer with USD 500 million in valuation. Besides, Germany is one of the top exporters of epoxide resins, with USD 872 million in value, followed by China as the importer, amounting to USD 779 million. Simultaneously, the continuous outsourcing of glass tubes for pharmaceutical applications is also responsible for driving the pharmaceutical cartridges market growth.

Glass Tubes, Natural Polymers, and Epoxide Resins Export/Import Comparative Analysis, 2024

|

Countries/Components |

Glass Tubes |

Natural Polymers |

Epoxide Resins |

|||

|

Export (USD) |

Import (USD) |

Export (USD) |

Import (USD) |

Export (USD) |

Import (USD) |

|

|

China |

85.8 million |

55.7 million |

1.0 billion |

- |

- |

779 million |

|

Japan |

73.8 million |

- |

- |

- |

- |

- |

|

Sweden |

- |

- |

583 million |

- |

- |

- |

|

U.S. |

60 million |

43 million |

344 million |

500 million |

771 million |

558 million |

|

South Korea |

- |

- |

- |

263 million |

851 million |

- |

|

Germany |

- |

- |

- |

229 million |

872 million |

449 million |

|

Global Trade Valuation |

353 million |

3.7 billion |

6.6 billion |

|||

|

Global Trade Value |

Less than 0.005% |

0.017% |

0.029% |

|||

|

Product Complexity |

- |

0.63 |

1.68 |

|||

Source: OEC

Furthermore, the large-volume polymer cartridge adoption, dual-chamber cartridge innovation, smart delivery systems and digitalized integration, along with an escalation in ready-to-use format, are a few trends that are bolstering the pharmaceutical cartridges market globally. As stated in an article published by NLM in February 2025, polymer composites as a material are frequently reinforced with glass fibers and carbon fibers, significantly accounting for 50% of the overall structure. In addition, both glass fiber-based polymer and carbon fiber-based polymer are extremely prevalent and further exemplified by an estimated 32 tons of composite materials. Based on these, polymers have gradually emerged as an integral part of various pharmaceutical and engineering applications, thereby making it extremely suitable for fueling the market expansion across different regions.

Key Pharmaceutical Cartridges Market Insights Summary:

Regional Highlights:

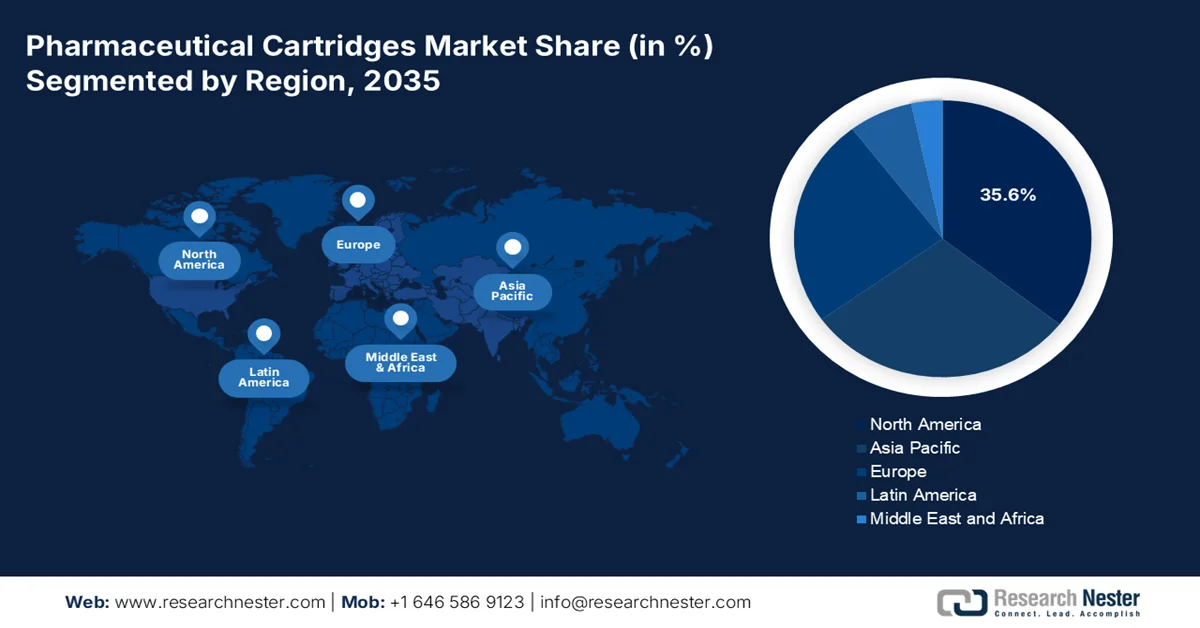

- North America is anticipated to hold a 35.6% share by 2035 in the pharmaceutical cartridges market, attributed to advanced healthcare infrastructure, rising adoption of self-injection devices, and strong R&D investments

- Europe is projected to be the fastest-growing region through 2035, fueled by an aging population, increasing chronic disease prevalence, and expanding adoption of biologic therapies requiring advanced drug delivery systems

Segment Insights:

- The disposable cartridges segment is projected to account for an 80.5% share by 2035 in the pharmaceutical cartridges market, propelled by ease of utilization, portability, and high convenience for on-the-go consumers and beginners

- The glass cartridges sub-segment is anticipated to secure the second-highest share by 2035, impelled by its critical role in ensuring drug purity, safety, and stability in pharmaceutical applications

Key Growth Trends:

- Rising prevalence of diabetes

- Expansion of special drugs and biologics

Major Challenges:

- Material integrity and extractable/leachable risks

- Manufacturing scalability and sterility assurance

Key Players: SCHOTT AG, Gerresheimer AG, Becton Dickinson and Company, West Pharmaceutical Services Inc., Nipro Corporation, Stevanato Group S.p.A., SGD Pharma, Vetter Pharma International GmbH, Baxter International Inc., Terumo Corporation, Catalent Inc., Dätwyler Holding Inc., Ypsomed AG, Transcoject GmbH, Pierrel S.p.A., Shandong Medicinal Glass Co., Ltd., AptarGroup Inc., Owen Mumford Ltd, Taisei Kako Co., Ltd., Rito GmbH & Co. KG, Formycon AG, Zydus Lifesciences Limited, TPG.

Global Pharmaceutical Cartridges Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.3 billion

- 2026 Market Size: USD 2.5 billion

- Projected Market Size: USD 4.7 billion by 2035

- Growth Forecasts: 8.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.6% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, Germany, China, Japan, France

- Emerging Countries: India, South Korea, Brazil, Spain, Italy

Last updated on : 22 April, 2026

Pharmaceutical Cartridges Market - Growth Drivers and Challenges

Growth Drivers

- Rising prevalence of diabetes: The worldwide diabetes epidemic is continuing to intensify, with incidence rates surging across different geographies and age groups, which is positively fueling the pharmaceutical cartridges market. According to official statistics published by the World Health Organization (WHO) in November 2024, there has been an increase in people residing with diabetes from 200 million to 830 million as of 2022, with a rise across low- and middle-income nations. Besides, this particular disease has caused kidney failure, leading to more than 2 million deaths. Apart from this, 14% of adults aged over 18 years were affected with the disease, demonstrating an increase by 7% from previous years. Additionally, 59% of adults aged more than 30 years are also impacted, thus enhancing the pharmaceutical cartridges market demand globally.

- Expansion of special drugs and biologics: The pharmaceutical sector’s tactical pivot towards biologics, gene therapies, mRNA-driven treatments, and monoclonal antibodies is considered a suitable driver for the pharmaceutical cartridges market. As stated in an article published by NLM in November 2024, the UK utilizes cost-effectiveness thresholds for different drug pricing that usually range from USD 27,005.4 to USD 67,513.5 per quality-adjusted life year (QALY). Likewise, the payer’s pricing threshold for drugs in the U.S. ranges from USD 50,000 to USD 150,000 per QALY. Therefore, based on the threshold pricing model, the maximum price of a medication is effectively determined, thereby denoting an optimistic outlook for the pharmaceutical cartridges market’s growth and development in different countries.

- Increase in R&D expenditure in the pharmaceutical industry: The presence of companies in the pharmaceutical industry, along with their manufacturing and development partners, is significantly boosting research and development spending. As per an article published by NLM in June 2024, the estimated R&D pricing for the latest drug usually ranges from USD 314 million to USD 4.4 million, significantly depending on modeling assumptions, data, and therapeutic area. Moreover, depending upon the disease or treatment provision, the approximate mean pricing of creating the newest drug amounts to USD 72.5 million for genitourinary and USD 297.2 million for anesthesia and pain. Likewise, in the case of oncology-based treatments, the cost amounts to USD 1,209.2 million, thus proliferating the pharmaceutical cartridges market’s exposure.

Challenges

- Material integrity and extractable/leachable risks: The transition to biologics and high-sensitivity molecules has exposed a fundamental weakness in the pharmaceutical cartridges market globally. Glass, the historical gold standard, is prone to delamination, which is microscopic glass flakes shedding into the drug product, and surface chemical interactions that can denature fragile biologic compounds. This forces manufacturers to implement costly siliconization processes, which introduce their own variability and particulate risks. Conversely, plastic cartridges made from cyclic olefin polymers (COP) or copolymers (COC) offer superior break resistance but struggle with gas permeability and potential leachables from polymer stabilizers.

- Manufacturing scalability and sterility assurance: The aspect of achieving high-volume and defect-free production of pharmaceutical cartridges at a global scale remains an engineering paradox. The shift toward ready-to-use (RTU) formats, with a focus on pre-sterilized, pre-siliconized cartridges nested for direct integration into fill/finish lines, has dramatically raised the bar for manufacturing precision. A single particle, crack, or silicone inconsistency in an RTU nest can contaminate an entire batch of expensive biologic drug, triggering million-dollar write-offs and supply disruptions. Besides, maintaining Class ISO 7 or better cleanroom environments across multiple global sites requires relentless capital reinvestment in automated inspection systems, robotics, and real-time environmental monitoring, which is causing a hindrance in the pharmaceutical cartridges market.

Pharmaceutical Cartridges Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.5% |

|

Base Year Market Size (2025) |

USD 2.3 billion |

|

Forecast Year Market Size (2035) |

USD 4.7 billion |

|

Regional Scope |

|

Pharmaceutical Cartridges Market Segmentation:

Product Type Segment Analysis

The disposable cartridges segment, which is part of the product type, is anticipated to account for the highest share of 80.5% in the pharmaceutical cartridges market by the end of 2035. The segment’s upliftment is primarily attributed to offering ease of utilization, portability, and high convenience for on-the-go consumers and beginners. According to official statistics published by NLM in August 2023, there has been an increase in disposable e-cigarettes, with a surge in volume capacity, accounting for 518% from 1.1 ml to 5.7 ml, along with an average nicotine strength increase by 294% from 1.7% to 5% in September 2022. Besides, as per the October 2024 CDC Government article, in terms of unit sales between February 2020 and June 2024, there has been an increase from 15.7 units to 21.1 million, demonstrating a 34.7% increase, thereby ensuring the segment’s growth globally.

Material Segment Analysis

Based on the material segment, the glass cartridges sub-segment is projected to grab the second-highest share in the pharmaceutical cartridges market during the forecast period. The sub-segment’s growth is highly driven by its importance in pharmaceutical applications for delivering and storing injectable drugs, along with offering inert and superior protection for maintaining drug purity, safety, and stability. As stated in an article published by NLM in January 2026, based on industrial advancements, there has been an increase in recycling rates for glass containers and packaging by 90% across countries, such as Switzerland and Sweden. In addition, there has also been an upsurge in the utilization of 80% of cullet in the furnace feedstocks for the overall global glass industry. Therefore, with all these benefits, glass readily represents the benchmark for recyclability, performance, and safety, thus fueling the pharmaceutical cartridges market exposure.

Distribution Channel Segment Analysis

By the end of the stipulated duration, the direct sales sub-segment, part of the distribution channel segment, is expected to garner the third-highest share in the pharmaceutical cartridges market. The sub-segment’s development is highly propelled by a foundational go-to-market model in the pharmaceutical cartridges industry, characterized by long-term, high-volume supply agreements between cartridge manufacturers and drug companies. This particular channel operates on a business-to-business basis, where specialized suppliers engage directly with pharmaceutical fill/finish facilities, often co-locating technical teams to ensure seamless integration of cartridges into automated filling lines. The strategic advantage of direct sales lies in the ability to customize specifications, including siliconization levels, nozzle geometry, and packaging formats, tailored to each drug molecule’s unique rheological properties.

|

Segment |

Subsegments |

|

Product Type |

|

|

Material |

|

|

Distribution Channel |

|

|

Application |

|

|

End user |

|

|

Capacity/Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Pharmaceutical Cartridges Market - Regional Analysis

North America Market Insights

North America in the pharmaceutical cartridges market is anticipated to grab the largest share of 35.6% by the end of 2035. The market’s upliftment in the region is primarily attributed to the presence of advanced healthcare infrastructure, the increased adoption of self-injection devices, a strong biologics pipeline, and generous R&D investments from pharmaceutical leaders. According to official statistics published by the CMS Government in January 2026, the national health expenditure, particularly in the U.S., surged by 7.2% to USD 5.3 trillion as of 2024, which is USD 15,474 per person, and further accounted for 18% of gross domestic product (GDP). Besides, the Medicare expenditure increased by 7.8% to USD 1,118 billion, which is 21% of the overall national health expenditure (NHE) in the same year. Therefore, with growth in other healthcare segments, the pharmaceutical cartridges market is gradually expanding in the region.

Expenditure Growth in Healthcare and Medical Segments in North America, 2024

|

Components |

Growth % |

Growth Amount |

% of NHE |

|

Medicaid |

6.6% |

USD 931.7 billion |

18% |

|

Private Health Insurance |

88.% |

USD 1,644.6 billion |

31% |

|

Out of Pocket |

5.9% |

USD 556.6 billion |

11% |

|

Other Third-Party Payers and Programs and Public Health Activity (decline) |

7.0% |

USD 590.5 billion |

11% |

|

Hospital Spending |

8.9% |

USD 1,634.7 billion |

10.6% |

|

Physician and Clinical Services |

8.1% |

USD 1,109.7 billion |

7.4% |

|

Prescription Drugs |

7.9% |

USD 467.0 billion |

10.8% |

Source: CMS Government

The pharmaceutical cartridges market in the U.S. is growing significantly, owing to biosimilar adoption, optimization in Medicare Part D, federal initiatives through disease management programs, and strict container closure guidance. As stated in an article published by the U.S. Food and Drug Administration (FDA) in October 2025, expensive biologic medications effectively make up almost 5% of prescriptions in the country and readily cater to 51% of overall drug expenditure in 2024. Besides, FDA-approved biosimilars are safe and effective, with a pharmaceutical cartridges market share accounting for 20%. Moreover, at present, the FDA has accepted 76 biosimilars, in comparison to a small fraction of approved biologics. On the whole, there exist more than 30,000 accepted generics, which exceeds branded drugs, thereby creating a positive impact on the market growth in the nation.

The existence of therapeutic cartridge manufacturing capacity, an expansion in domestic vaccine production, the strong drug delivery facility, coverage extension for biologic therapies, a regulatory framework, an escalation in high-value biologic therapies, and federal-provincial partnerships are certain factors that are fueling the pharmaceutical cartridges market in Canada. As per an article published by the PMGC in March 2024, Sanofi developed the latest state-of-the-art Vaccine Manufacturing Facility in Ontario, which is generously backed by a federal investment of USD 20 million. In addition, this particular facility is considered to emerge as one of the most innovative vaccine manufacturing infrastructures globally. This facility produces diphtheria, tetanus, and cough vaccines for the population as well as for 60 foreign economies, and it has also created more than 200 employment opportunities and further maintains over 1,000 other jobs in Ontario, thus driving the market expansion.

Europe Market Insights

Europe in the pharmaceutical cartridges market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by the aging population, a rise in chronic disorders, an increase in integrating biologic therapies that demand innovative drug delivery systems, an expansion in patient accessibility to cartridge-driven biologic treatments, and substantial funding allocation. According to official statistics published by OECD in November 2024, over 1/3rd of adults in the region, which is 35%, reported residing with a long-term health or illness problem as of 2023. Additionally, 37% of the female population in the region suffers from severe chronic conditions as of the same year, in comparison to 33% of the male population. Simultaneously, 60% of aged people over 65 years of age have chronic illnesses, and this percentage usually ranges from 1 in 2 in Finland, as well as 1 in 6 in Italy, thus enhancing the pharmaceutical cartridges market development.

Long-Term Health/Illness Problem by Gender in Europe, 2023

|

Countries |

Male |

Female |

Total |

|

Italy |

14% |

18% |

16% |

|

Romania |

17% |

25% |

21% |

|

Bulgaria |

20% |

25% |

23% |

|

Luxembourg |

21% |

24% |

23% |

|

Greece |

22% |

27% |

25% |

|

Belgium |

25% |

29% |

27% |

|

Ireland |

29% |

29% |

29% |

|

Malta |

28% |

32% |

30% |

|

Croatia |

29% |

33% |

31% |

|

Slovak Rep |

30% |

37% |

33% |

Source: OECD

The pharmaceutical cartridges market in Germany is gaining increased traction, owing to advanced drug delivery systems, the largest pharmaceutical manufacturing facilities, suitable reimbursement policies, statutory health insurance funds, an increase in biosimilar biologics, a strong export-based pharmaceutical industry, and the digital health integration trend. As stated in an article published by Eurostat in April 2025, the country is regarded as the largest exporter of pharmaceutical medicinal products, amounting to USD 79.8 billion, along with being the largest extra-regional importer, with products worth USD 27 billion. Based on this, the overall regional exports of such products upsurged by 13.5% as of 2024, in comparison to 2023, and successfully reached 368.7 billion. Likewise, regional imports recorded an increase by 0.5%, significantly amounting to USD 140.8 billion, thus denoting a huge pharmaceutical cartridges market growth opportunity.

The wide-ranging public health coverage for rare disease treatments, government-based strategies for strengthening domestic biomanufacturing capacity, reimbursement pathways, significant fund allocations, home healthcare programs, the existence of the centralized procurement model, and eco-design trends are a few factors that are responsible for enhancing the market in France. As per an article published by the U.S. Department of State in 2024, the country’s government is focused on international investors and has readily concluded 1,815 transactions as of 2023, leading to 59,254 employment opportunities that have been both developed and maintained. Besides, the U.S. has been the ultimate foreign investor in the country with investments for 305 latest projects that created and sustained 17,000 jobs, thereby denoting an optimistic outlook for the market development.

APAC Market Insights

The Asia Pacific in the pharmaceutical cartridges market is projected to experience considerable growth by the end of the stipulated timeline. The market’s growth in the region is effectively driven by the rapid increase of biologic drug manufacturing, a combination of large-scale public healthcare approaches, particularly in India and China, technology-driven economies, and a sudden transition to self-administered biosimilars and insulin. According to official statistics published by NLM in June 2022, a cross-sectional clinical study was conducted across 14 regional countries for 440 mAb and FcP biological products. The study results demonstrated 12.9% of lymphocyte or adhesion molecules, along with 22% growth in tumor cells, 26.1% check point inhibitors, and 4% of other targets. Based on these, bio-originators catered to 64.3%, which is 283 units of 440, of the overall products, thereby positively uplifting the market expansion in the overall region.

The pharmaceutical cartridges market in China is gaining increased exposure, owing to the presence of an increased diabetic population, robust healthcare infrastructure modernization, escalated approvals for biosimilars and prefilled cartridge systems, expansion in treatment accessibility, government spending, and a rise in diagnosed patients. As stated in an article published by NLM in July 2024, a questionnaire-based study was conducted on 111,943 participants aged between 18 and 79 years. Based on the study, it was demonstrated that there was an increase in the overall diabetes prevalence in Beijing from 9.6% to 13.9% as of 2022. In addition, undiagnosed diabetes upsurged from 3.5% to 7.2%, and meanwhile, the yearly awareness and treatment accounted for 1.3% and 1.4%, thereby significantly fueling the market exposure.

The aspects of increasingly focusing on non-communicable diseases, a surge in patient numbers readily demanding insulin and other injectable biologics, suitable support provision by extended diagnostic coverage, and export of pharmaceuticals are certain trends that are responsible for uplifting the pharmaceutical cartridges market in India. As per an article published by NLM in May 2024, the expense of insulin is usually not transparent, and in the case of biosimilar insulins, which effectively serve as generic alternatives, they constitute the potential to be more than 25% more affordable, in comparison to the original product. Besides, as per the June 2024 Journal of the Association of Physicians of India article, Type 1 diabetes is continuously growing in the country at 6.7% every year, in comparison to 4.4% for Type 2 diabetes, thereby proliferating the market demand.

Key Pharmaceutical Cartridges Market Players:

- SCHOTT AG (Germany)

- Gerresheimer AG (Germany)

- Becton Dickinson and Company (U.S.)

- West Pharmaceutical Services, Inc. (U.S.)

- Nipro Corporation (Japan)

- Stevanato Group S.p.A. (Italy)

- SGD Pharma (France)

- Vetter Pharma International GmbH (Germany)

- Baxter International Inc. (U.S.)

- Terumo Corporation (Japan)

- Catalent Inc. (U.S.)

- Dätwyler Holding Inc. (Switzerland)

- Ypsomed AG (Switzerland)

- Transcoject GmbH (Germany)

- Pierrel S.p.A. (Italy)

- Shandong Medicinal Glass Co., Ltd. (China)

- AptarGroup, Inc. (U.S.)

- Owen Mumford Ltd (UK)

- Taisei Kako Co., Ltd. (Japan)

- Rito GmbH & Co. KG (Germany)

- Formycon AG (Germany)

- Zydus Lifesciences Limited (India)

- TPG (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- SCHOTT AG is recognized as a global innovation leader in pharmaceutical glass and polymer cartridges, particularly known for advancing ready-to-use system integration. The company focuses heavily on developing specialized surface coatings and high-barrier materials that enhance drug stability for sensitive biologic formulations.

- Gerresheimer AG operates as a comprehensive systems partner, combining precision glass cartridge manufacturing with proprietary plastic injection molding capabilities for complete pen injector assemblies. The company differentiates itself through its dual expertise in both standard tubular glass and high-performance polymer cartridges tailored for next-generation autoinjector platforms.

- Becton Dickinson and Company leverages its dominant position in injection devices to drive demand for compatible cartridge formats, effectively linking hardware and consumable sales. The company focuses on engineering cartridges that integrate seamlessly with its extensive portfolio of pen injectors and safety syringes for chronic disease management.

- West Pharmaceutical Services, Inc. brings deep expertise in elastomeric components and container closure integrity systems, positioning its cartridges as part of broader drug delivery ecosystems. The company emphasizes holistic solutions that pair cartridges with advanced injection molding and analytical testing services to reduce fill-finish risks for biopharmaceutical customers.

- Nipro Corporation maintains a strong presence in Asia-Pacific markets through its vertically integrated glass manufacturing, producing cartridges for both insulin delivery and dental anesthesia applications. The company focuses on scaling high-volume production capabilities while maintaining rigorous quality standards to serve large pharmaceutical tenders across emerging economies.

Here is a list of key players operating in the global pharmaceutical cartridges market:

The pharmaceutical cartridges market is characterized by a consolidated competitive landscape dominated by established Europe and North America-based players with decades of glass-forming and aseptic filling expertise. Based on this, notable strategic initiatives include capacity expansion for large-volume ready-to-use cartridges, investments in polymer technology to address biologic drug stability requirements, and vertical integration through acquisitions of fill-finish service providers. For instance, in June 2025, SCHOTT Pharma invested over USD 117.6 million in its present facility in Hungary for effectively expanding its capacity, especially for sterile ready-to-use (RTU) cartridges. In addition, the organization also added a manufacturing capacity for high-value solutions, thereby making it extremely suitable for bolstering the pharmaceutical cartridges industry globally.

Corporate Landscape of the Market:

Recent Developments

- In December 2025, Formycon AG and Zydus Lifesciences Limited entered into a tactical partnership for the outstanding licensing and supply of checkpoint inhibitor FYB206, which is considered a biosimilar of Keytruda®1, particularly in the U.S. and Canada.

- In May 2025, TPG significantly entered into a binding agreement with the Serum Institute of India and SCHOTT Pharma to acquire a 35% stake in the joint venture, SCHOTT Poonawalla. Besides, TPG, along with Novo Holdings, funded the investment to ensure growth equity in its own platforms.

- In May 2025, Nipro commenced the high-quality glass cartridge production, particularly for pen and dental applications, at its very own India-based manufacturing facility, with the intention of supporting the growing industrial demand for glass cartridges in the overall Asia.

- Report ID: 8524

- Published Date: Apr 22, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.