Penile Implants Market Outlook:

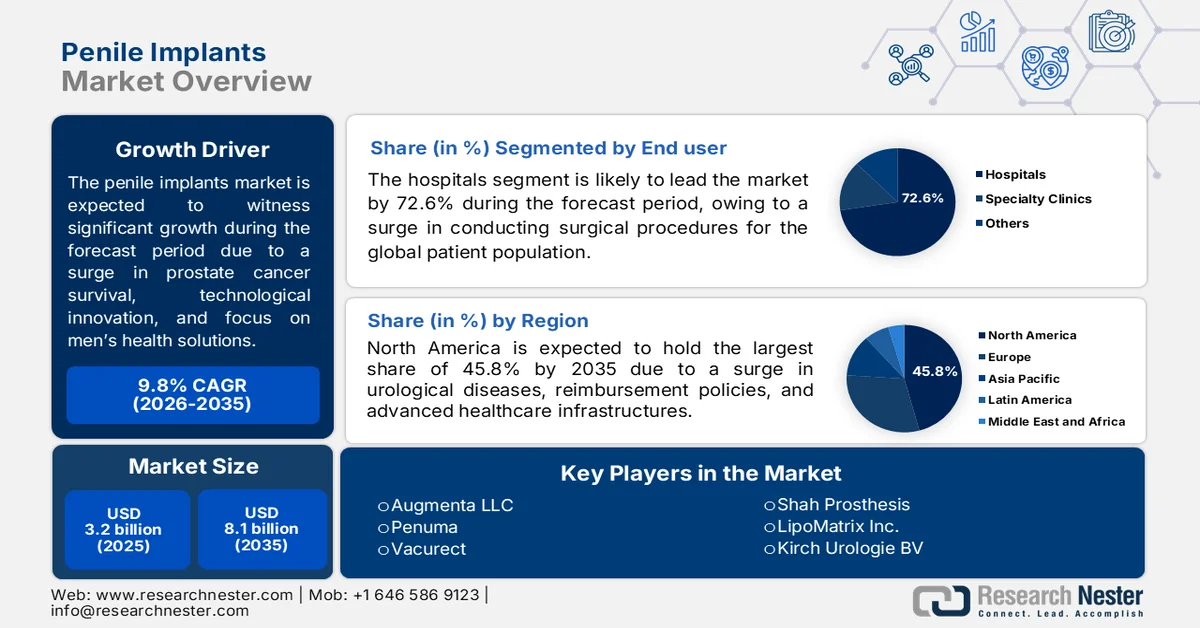

Penile Implants Market size was valued at USD 3.2 billion in 2025 and is projected to reach USD 8.1 billion by the end of 2035, growing at a 9.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of penile implants is evaluated at USD 3.5 billion.

The worldwide penile implants market is positively influenced by factors including expansion of the medical tourism industry, a rising population of prostate cancer survivors, technological convergence between surgical and urological specialties, and a focus on men’s health. According to official statistics published by NLM in March 2026, it has been estimated that there exist 1.5 million new prostate cancer cases, along with 397,000 deaths globally. Additionally, across 2/3rd of nations around the world, this particular cancer is the most frequently diagnosed among the male population. However, with the implementation of standard technologies and treatment solutions, the 5-year relative survival rate surpassed 70% in the majority of regions and countries. For instance, the survival rate was the highest in the U.S. at 98.5%, while it was lowest in Punjab, India, at 30.3%, thereby determining the growth opportunity of the market globally.

Furthermore, the ascendance of ambulatory surgery center-based implantation, the adoption of patient-controlled and digital health features, as well as the center of excellence and specialization accreditation, are a few trends that are responsible for enhancing the penile implants market globally. As stated in an article published by NLM in March 2023, surgical procedures are continuously shifting to non-hospital or outpatient locations, and an expected 4% yearly expansion rate of the ambulatory surgery center (ASC) industry is poised to be witnessed by the end of 2027. In this regard, there was an increase in conducting such surgeries to 144 million as of 2023, and meanwhile, the shift in surgeries to ASCs is owing to the 60% expense of hospital-based outpatient departments (HOPDs), thereby making it suitable for bolstering the market demand.

Key Penile Implants Market Insights Summary:

Regional Highlights:

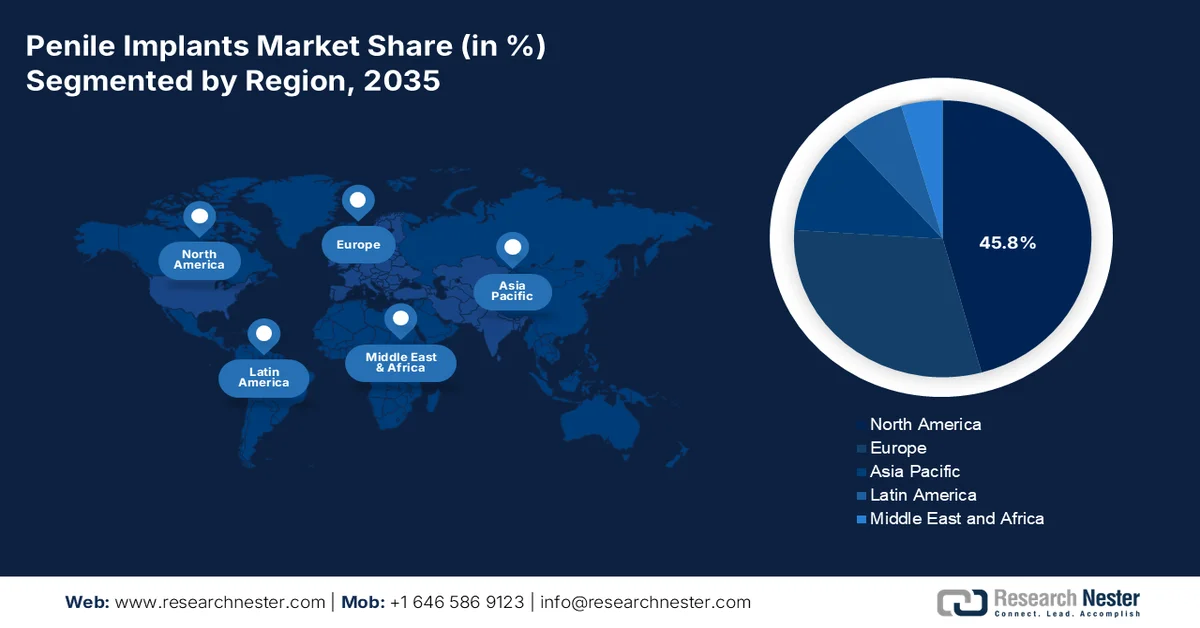

- North America is set to command 45.8% of the penile implants market by 2035, underpinned by increasing erectile dysfunction prevalence, advanced urological facilities, favorable reimbursement policies, and expanding adoption of three-piece implants

- Asia Pacific is poised to register the fastest growth in the market throughout 2026-2035, accelerated by the aging population, rising disposable incomes, expanding awareness campaigns, and substantial government investments in healthcare services

- The penile implants market in the U.S. accounts for 40.2% of the share in North America, which is driven by the increased implantation demand among the elderly population, the provision of standard reimbursement services, and technological innovation

- The penile implants market in Japan accounts for 2.8% of the share in the Asia Pacific, owing to the transition to suitable surgical treatments, advancements in healthcare facilities, and the presence of standard insurance coverage solutions for the patient population

Segment Insights:

- The hospitals segment is projected to account for 72.6% of the penile implants market by 2035, reinforced by the availability of advanced surgical infrastructure, specialized clinical support, and comprehensive post-operative care for complex penile implant procedures

- The inflatable penile implant sub-segment is anticipated to secure a notable share during 2026-2035, stimulated by its critical role in treating severe erectile dysfunction and growing emphasis on infection prevention measures during implantation procedures

Key Growth Trends:

- Rise in cardiovascular disease

- Side-effects of non-surgical treatment alternatives

Major Challenges:

- Limited availability of trained surgical specialists

- Patient psychological barriers and stigma

Key Players: Boston Scientific Corporation (U.S.), Coloplast Corp (Denmark), Rigicon Inc (U.S.), Zephyr Surgical Implants (Switzerland), Promedon S.A. (Argentina/Germany), Silimed (Brazil), Giant Medical (China), Eska Medical (Germany), Augmenta LLC (U.S.), Penuma (U.S.), Vacurect (U.S.), Shah Prosthesis (India), LipoMatrix Inc. (U.S.), Kirch Urologie BV (Netherlands), Milux Holding SA (Luxembourg), Advin Health Care (India), UroMed (U.S.), Bristol Myers Co. (U.S.), Medline Industries (U.S.), Hollister Incorporated (U.S.), Himplant (U.S.), Hanmi Pharmaceutical (South Korea), Phoenix (Canada), Haleon (UK).

Global Penile Implants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.2 billion

- 2026 Market Size: USD 3.5 billion

- Projected Market Size: USD 8.1 billion by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, Canada

- Emerging Countries: China, India, South Korea, Australia, Singapore

Last updated on : 2 June, 2026

Penile Implants Market - Growth Drivers and Challenges

Growth Drivers

- Rise in cardiovascular disease: The worldwide epidemic of heart risks readily serves as the fundamental demand and growth of the penile implants market globally. According to official statistics published by NIH in August 2025, a 90% increase in the disease prevalence is expected by 2050, along with 73.4% surge in crude mortality, and 54.7% increase in crude disability-adjusted life years (DALYs). In addition, 35.6 million cardiovascular deaths are also projected by the end of the same year, thus proliferating the market demand globally. Besides, as per the February 2024 AHA Journal, the mean payers’ pricing per hospital discharge is usually highest for peripheral vascular disease, amounting to USD 33,700, and for ventricular fibrillation is USD 32,500, thus enhancing the market expansion.

- Side-effects of non-surgical treatment alternatives: The limitations of present pharmaceutical erectile dysfunction treatments have created a natural patient flow towards the penile implants market. As stated in an article published by NLM in October 2025, a clinical study was conducted on 101 patients, of which 45.5% aged more than 35 years utilized a contraceptive implant. The study demonstrated that common side-effects of the implant including 24.8% of weight gain, 23.8% of headache, and 19.8% of libido. Besides, the majority of women, which is 54.5%, intend to have a contraceptive implant removed in 3 years, owing to menstrual irregularities. Therefore, these particular side effects negatively impact the overall health of women patients, thus making it suitable for standard implantation techniques.

Challenges

- Limited availability of trained surgical specialists: The procedure in the penile implants market requires specialized surgical expertise that remains concentrated in high-volume academic medical centers and a limited number of private urology practices, creating significant geographic and capacity constraints. Unlike many other surgical procedures, successful penile implant outcomes depend heavily on surgeon experience, with high-volume implanters demonstrating substantially lower infection rates, reduced mechanical complications, and superior patient satisfaction compared to low-volume or occasional operators. This learning curve creates a natural barrier to market entry, as new surgeons require dedicated proctoring and significant case experience before achieving independent proficiency.

- Patient psychological barriers and stigma: The aspect of persistent social stigma surrounding erectile dysfunction and surgical treatment options continues to suppress patient willingness to pursue penile implantation, creating a significant demand-side roadblock. Despite medical advancements and proven clinical efficacy, many men harbor misconceptions about penile implants, including fears about unnatural appearance, loss of sensation, partner detection, or irreversible changes to their anatomy. The psychological burden of acknowledging treatment failure from oral medications and progressing to surgical consideration represents a significant emotional hurdle that negatively impacts the penile implants market growth.

Penile Implants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 3.2 billion |

|

Forecast Year Market Size (2035) |

USD 8.1 billion |

|

Regional Scope |

|

Penile Implants Market Segmentation:

End user Segment Analysis

Based on end user, the hospitals segment is anticipated to garner the largest share of 72.6% in the penile implants market by the end of 2035. The segment’s upliftment is primarily attributed to the provision of complex surgical procedures. Besides, the inflatable penile prostheses (IPP) implantation, which is the most widely adopted device type, is an intricate surgery that requires a fully integrated medical environment. Based on this, hospitals possess the advanced operating theaters, specialized anesthetic support, intensive care units, and multi-disciplinary teams essential not only for the surgery itself but also for managing potential post-operative complications. This is particularly critical for complex revision surgeries or for high-risk patients with multiple comorbidities, thereby making it suitable for the market growth and expansion globally.

Type Segment Analysis

During the forecast period, the inflatable penile implant sub-segment, part of the type segment, is projected to grab a suitable share in the penile implants market. The sub-segment’s growth is effectively fueled by its crucial role as a medical device that is surgically placed to aid severe erectile dysfunction. According to official statistics published by NLM in January 2026, fungal infections are reported in more than 10% patients globally, which are not usually covered by contemporary antimicrobial prophylaxis. Besides, the utilization of 0.05% of chlorhexidine gluconate and the overall implementation of antifungal prophylaxis indicate a huge aspect of the implant procedure. Moreover, this procedure also comprises the adoption of disposable tools, including the Furlow, which is suitable for combating infectious complications, thereby boosting the sub-segment’s demand.

Material Segment Analysis

The silicone-based implants sub-segment, which is part of the materials segment, is expected to capture a considerable share in the penile implants market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by its importance in modernized reconstructive and medical surgery due to its longevity, flexibility, and biocompatibility, along with precisely mimicking human tissue. As stated in an article published by NLM in November 2025, silicone implants comprise smooth shell surfaces, with minimal roughness of less than 10 μm, along with 10 to 100 μm of micro-texture, and more than 50 μm of macrotexture. Meanwhile, the continuous supply of silicone in its primary form, which is suitable for producing implants, is also responsible for boosting the sub-segment globally.

2024 Silicon Primary Forms Global Export and Import Analysis

|

Countries/Component |

Export (USD) |

Import (USD) |

|

Germany |

1.7 billion |

- |

|

U.S. |

1.3 billion |

704.0 million |

|

China |

1.5 billion |

829.0 million |

|

South Korea |

- |

514.0 million |

|

Global Trade Valuation |

8.5 billion |

|

|

Global Trade Share |

0.03% |

|

|

Product Complexity |

1.4 |

|

|

Export Growth |

0.6% |

|

Source: OEC

Our in-depth analysis of the penile implants market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Type |

|

|

Material |

|

|

Indication |

|

|

Patient Type |

|

|

Deployment Method |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Penile Implants Market - Regional Analysis

North America Market Insights

North America in the penile implants market is anticipated to garner the highest share of 45.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to an increase in erectile dysfunction prevalence, innovative urological facilities, suitable reimbursement policies, supportive insurance coverage, and a rise in the adoption of three-piece implants for reduced stigma, enhanced ambulatory surgical centers, and natural functionality. According to official statistics published by the American Urological Association Journal in March 2025, 1 in 5 people residing in the region’s non-urban areas, with a similar number of urologists practicing, and despite this, 63% of regional countries have a lack of urologists. Besides, based on a clinical study conducted on a patient pool of 552 urologists, stressors for non-metropolitan urologists included 59.3% of workforce issues and call concerns, and 40.7% of lack of resources, thus denoting a suitable growth opportunity for the market.

The penile implants market in the U.S. is growing significantly, owing to an increase in the aging baby boomer population, a rise in diabetes prevalence, the presence of Medicare and private insurer reimbursement expansion, and suitable technological advancements. Based on government estimates published by the CDC in January 2026, the approximate number of people diagnosed with diabetes in the country accounts for 40.1 million, with the inclusion of undiagnosed incidences. In addition, the estimated percentage of the domestic population with diabetes constitutes 12%. Moreover, 29.1 million caters to an approximate number of people with diagnosed diabetes in the country, effectively including 28.8 million adults aged more than 18 years. Meanwhile, 27.6% roughly constitutes 18-year-old adults with undiagnosed diabetes, thus enhancing the market demand.

The support by provincial health system adoption, an expansion in public reimbursement, the concentration of specialized urological facilities, the alignment with U.S. clinical guidelines, and an increase in the focus on surgeon education are certain factors that are boosting the penile implants market in Canada. As per an article published by NLM in April 2025, the Canadian Urological Association (CUA) conducted a census-based study on a patient pool of 342, both active and senior members, to analyze practice patterns and membership demographics as of 2024. The study demonstrated that the primary language utilization in clinical practice was English for 74% of members and French for 19%. In addition, 91% of members completed medical school in the country in 2022 and 90% in 2024, thereby denoting an optimistic outlook for the market growth and expansion.

CUA Survey Analysis Parameters for Urologists Availability in Canada, 2024

|

Parameters |

Attributes |

|

Employment Status |

|

|

Full Time |

90% |

|

Part Time |

8% |

|

Unemployed |

2% |

|

Main Practice Setting |

|

|

Academic |

40% |

|

Community |

40% |

|

Hybrid |

20% |

|

Gender |

|

|

Male |

82% |

|

Female |

17% |

|

Age |

|

|

Less Than 35 years |

6% |

|

35 to 44 years |

41% |

|

45 to 54 years |

26% |

|

More Than 55 years |

27% |

Source: NLM

APAC Market Insights

The Asia Pacific in the penile implants market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the aging population, a rise in disposable incomes, an increase in public awareness campaigns, and generous government investments in healthcare services. According to official statistics published by NLM in February 2023, an estimated 4% to 7% of the overall gross domestic product (GDP) has been generously invested in the regional healthcare industry. Besides, as per the December 2025 OECD article, the out-of-pocket spending, particularly in Southeast Asia, constituted to 31% of overall healthcare expenditure. Additionally, this is significantly more than the expenditure in other countries as of 2022, thereby making it suitable for enhancing the penile implants market in the overall region.

The penile implants market in China is gaining increased traction, owing to the massive aging population, a rise in healthcare expenditure, an increase in urbanization, the growing awareness of erectile dysfunction, and lifestyle risks related to cardiovascular diseases and diabetes. As stated in an article published by NLM in November 2025, the 2024 Annual Report on Cardiovascular Health and Diseases in China indicated that the sudden cardiac death was 620.3 per 100,000 population, along with 87.6 for acute myocardial infarction (AMI). Likewise, the stroke incidence accounted for 491.0 per 100,000 population, while adult coronary heart disease was 758 per 100,000 population. Moreover, the crude mortality rate of cardiovascular disease was 364.1 per 100,000 population across rural locations and 305.3 in urban areas, thereby positively fueling the market development.

The aspects of the male aging population, a rise in chronic conditions, the increased demand among prostate cancer survivors, the gradual shift towards surgical treatments, the high-quality healthcare infrastructure, and generous insurance coverage are a few trends that are responsible for driving the penile implants market in Japan. The Japan penile implant industry was worth USD 327.3 million as of 2025, which is further projected to be valued at USD 357 million by 2026 and eventually reach USD 781.9 million, along with a 9.1% growth rate by 2035. As per an article published by the World Economic Forum in April 2026, the national 5-year survival rate for prostate cancer reached 92.5% in the country for adults aged more than 15 years. Moreover, according to the Japan Cancer Society, cancer caused an estimated 380,000 deaths as of 2025, which represented 23.9% of overall deaths. Therefore, to overcome this, local and national governments have ensured early detection, support expansion, and treatment innovation, thus bolstering the market demand in the country.

Europe Market Insights

Europe in the penile implants market is projected to witness considerable expansion by the end of the stipulated timeline. The market’s growth in the region is effectively driven by the presence of the elderly population, well-established health and medical systems, the incorporation of advanced medical devices, supportive regulatory frameworks, and the increased prevalence of erectile dysfunction related to post-prostatectomy recovery. According to official statistics published by NLM in February 2023, the presence of regional healthcare companies readily attends to over 500 million in health services, deliberately enhancing the general life quality and the availability of medical products. In addition, the healthcare spending in the region accounts for a significant portion of the GDP, ranging from 5.5% in Latvia to 11.4% in Switzerland, as well as 11.1% in France and 11.7% in Germany, thereby bolstering the market growth.

Healthcare Expenditure Analysis in Europe, 2023

|

Countries |

USD Million |

USD Per Inhabitant |

PPS Per Inhabitant |

GDP % |

|

Europe |

2.0 |

4,461.4 |

3,835 |

10.0 |

|

Belgium |

74,934.3 |

6,361.2 |

4,569 |

10.8 |

|

Bulgaria |

8,724.8 |

1,352.9 |

2,084 |

7.9 |

|

Czechia |

31,111,1 |

2,863.9 |

2,925 |

8.4 |

|

Denmark |

41,654.8 |

7,004.2 |

4,173 |

9.5 |

|

Germany |

571,832.7 |

6,865.7 |

5,413 |

11.7 |

|

Estonia |

3,318.8 |

2,421.9 |

2,145 |

7.5 |

Source: European Commission

The penile implants market is gaining increased exposure in Germany, owing to the provision of procedural support and surgeon training services, the existence of strict quality standards, the demand for surgical rehabilitation, a suitable reimbursement framework, and the presence of specialized implanting urologists. As stated in an article published by the ITA in August 2025, the surgical equipment industry in the country is steadily growing, with a predicted yearly growth rate of 0.8% by the end of 2030. Besides, based on the February 2026 UNDP Organization article, the Government of Germany’s strategy, which is the USD 34.8 million (EUR 30 million), has been provided for effectively contributing towards the 36-month project for restoring operational readiness of 5 hospitals, including Deir-ez-Zor, Dara’a, Idleb, Homs, and Hama, thereby proliferating the market upliftment.

The tactical shift towards ambulatory surgery centers, targeted public health investment, an increase in the demand for clinically safe and effective devices, import volatility, the diversification of supply sources, and the focus on pharmacological solutions for patients are certain trends that are bolstering the penile implants market in France. Based on a data report published by OECD in December 2025, the health expenditure in the country accounted for 11.5% of the GDP as of 2023, which is the second-highest share after Germany. Besides, medical devices and retail pharmaceuticals constitute a considerable share of domestic expenditure, catering to 19% of health spending, while long-lasting care accounts for 16%. Moreover, as per the April 2026 OEC article, medical device exports in the country amounted to USD 3.9 billion, while imports were worth USD 6.2 billion as of 2024, thus enhancing the market demand.

Key Penile Implants Market Players:

- Boston Scientific Corporation (U.S.)

- Coloplast Corp (Denmark)

- Rigicon Inc (U.S.)

- Zephyr Surgical Implants (Switzerland)

- Promedon S.A. (Argentina/Germany)

- Silimed (Brazil)

- Giant Medical (China)

- Eska Medical (Germany)

- Augmenta LLC (U.S.)

- Penuma (U.S.)

- Vacurect (U.S.)

- Shah Prosthesis (India)

- LipoMatrix Inc. (U.S.)

- Kirch Urologie BV (Netherlands)

- Milux Holding SA (Luxembourg)

- Advin Health Care (India)

- UroMed (U.S.)

- Bristol Myers Co. (U.S.)

- Medline Industries (U.S.)

- Hollister Incorporated (U.S.)

- Himplant (U.S.)

- Hanmi Pharmaceutical (South Korea)

- Phoenix (Canada)

- Haleon (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Boston Scientific Corporation maintains a commanding presence through its AMS series of inflatable implants, which are widely regarded as the clinical gold standard for erectile dysfunction treatment. The company invests heavily in surgeon training programs and patient education resources to sustain its premium market positioning.

- Coloplast Corporation competes directly with Boston Scientific through its Titan line of inflatable penile prostheses, emphasizing durability and high patient satisfaction rates. The company leverages its strong Europe-based heritage and global distribution network to maintain competitive parity in key markets.

- Rigicon Inc. has emerged as a challenger brand in the penile implant space, offering innovative inflatable devices designed with user-friendly features such as a simplified pump mechanism. The company focuses on differentiating itself through nimble product development cycles and responsive customer support.

- Zephyr Surgical Implants serves the market with a specialized focus on malleable and semi-rigid penile implants, catering to price-sensitive segments and specific clinical indications. The Swiss manufacturer benefits from the reputation of Swiss precision engineering and adherence to stringent European medical device regulations.

- Promedon S.A. maintains a dual footprint in Latin America and Europe, offering both inflatable and malleable penile implant solutions at competitive price points. The company strategically targets emerging markets and cost-conscious healthcare systems where premium devices face affordability constraints.

Here is a list of key players operating in the global penile implants market:

The global penile implants market remains highly concentrated, with North America and Europe-based manufacturers holding dominant positions. Key players are pursuing aggressive innovation strategies, as evidenced by Boston Scientific's 2023 FDA approval of the Tenacio pump with automated deflation technology. Strategic initiatives focus on expanding product portfolios with inflatable and malleable implants, improving usability features, and strengthening distribution networks. Besides, in June 2024, Himplant proclaimed that the U.S. Food and Drug Administration (FDA) approved its penile enhancement implant. This particular implant preserves penile health in crucial trauma cases, thereby making it suitable for bolstering the penile implants industry’s growth globally.

Corporate Landscape of the Penile Implants Market:

Recent Developments

- In April 2025, Hanmi Pharmaceutical launched Aditams, which is a urological product, by partnering with Laboratories Silanes, with its commercialization in Latin America, and increased exports to Mexico.

- In March 2025, Phoenix signed a USD 36.2 million (CAD 50 million) Series A funding round, which was led by Valspring Capital, along with renewed investment from Y Combinator and suitable support from CIBC Innovation Banking for uplifting the healthcare system.

- In September 2024, Haleon unveiled Eroxon®, which is the first-ever and only FDA-cleared OTC gel, which is extremely suitable for aiding erectile dysfunction, and readily available in the U.S. without the need for prescriptions.

- Report ID: 8596

- Published Date: Jun 02, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.