Medical Implants Market Outlook:

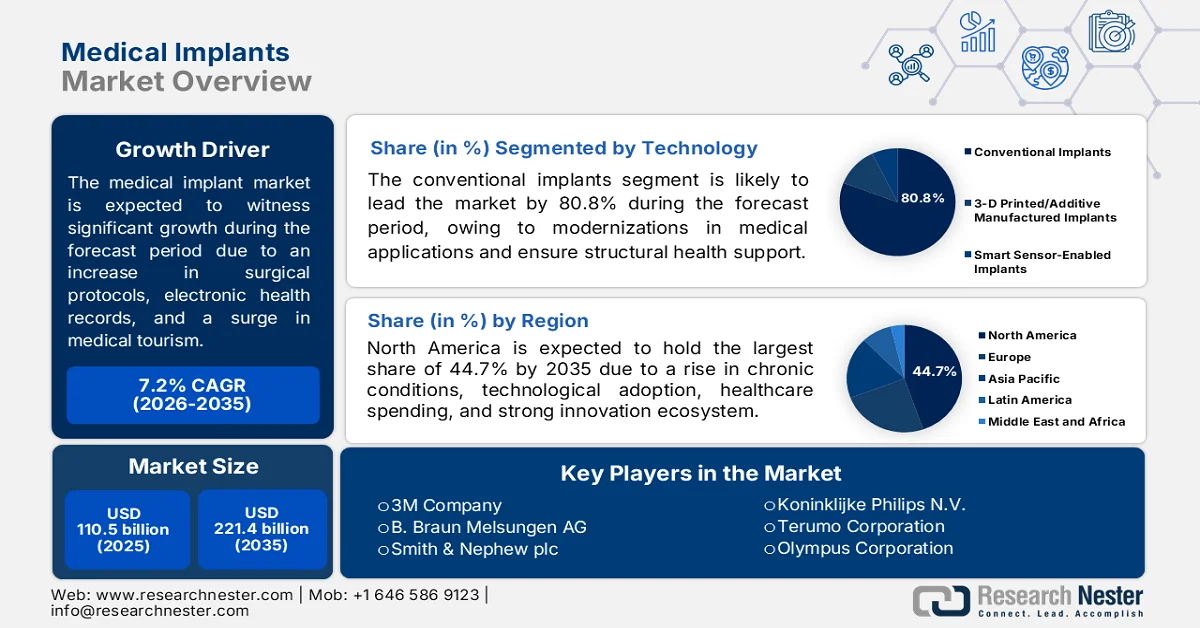

Medical Implants Market size was valued at USD 110.5 billion in 2025 and is projected to cross USD 221.4 billion by the end of 2035, expanding at more than 7.2% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of medical implants is estimated at USD 118.4 billion.

The global medical implants market is significantly reshaping due to an increase in the demand for same-day and outpatient discharge surgical protocols, an expansion in preoperative volumes for diminishing hospital bottlenecks, the standardization of electronic health records, a rise in medical tourism, and a shift from metal-based implants to polymer and bioceramic hybrid devices. According to official statistics published by the JMIR Publications in September 2022, displaying the proof of meaningful utilization of certified electronic health records resulted in USD 27 billion in overall incentive provision to hospitals and physicians. Additionally, of this, USD 406 million was readily allocated to Medicare Advantage Organizations for eligible providers. Besides, the Center for Medicare and Medicaid Services offered payments of USD 63,750 for more than 6 years for Medicaid and USD 44,000 for over 5 years for Medicare, thus enhancing the medical implants market growth.

Furthermore, the decentralized manufacturing through point-of-care 3D printing, implant-based remote therapeutic monitoring, and the adoption of circular models for high-value implants are a few trends that are responsible for bolstering the medical implants market globally. As stated in an article published by NLM in July 2024, the worldwide remote patient monitoring industry is expected to expand rapidly in the upcoming years, accounting for a yearly growth rate of 18.9% by the end of 2028. Besides, based on a meta-analysis, 27 randomized controlled trials on wearable biosensors denoted restricted clinical impacts. Likewise, the impact of digitalized sensor alerting systems for remote monitoring constituted a 9.6% reduction in hospitalization, along with a 3% decrease in all-cause mortality, thereby denoting an optimistic outlook for the medical implants market growth and expansion.

Key Medical Implants Market Insights Summary:

Regional Highlights:

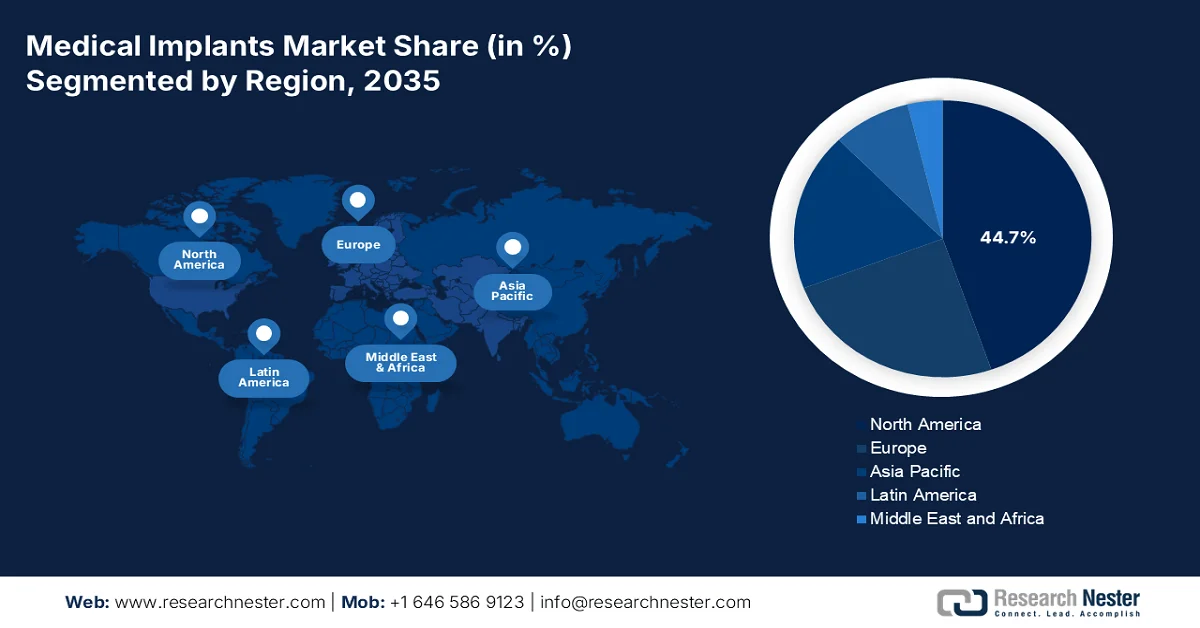

- North America medical implants market is anticipated to command a 44.7% revenue share by 2035, attributed to an aging population, rising chronic disease prevalence, increasing healthcare expenditure, and strong innovation ecosystems supporting advanced implant technologies

- Asia Pacific is projected to witness the fastest expansion in the market throughout 2026–2035, propelled by healthcare accessibility improvements, reimbursement-driven economies, evolving regulatory frameworks, expanding medical infrastructure, and broader insurance coverage

Segment Insights:

- The conventional implants sub-segment is forecast to capture 80.8% of the medical implants market share by 2035, reinforced by its essential role in delivering structural support, restoring physical functionality, and improving patient quality of life

- The metallic biomaterials sub-segment is expected to secure the second-largest share in the market during the forecast period, stimulated by increasing demand for durable load-bearing materials capable of repairing and replacing damaged musculoskeletal tissues

Key Growth Trends:

- Increase in non-communicable diseases programs

- Health insurance penetration in low-income populations

Major Challenges:

- Supply chain fragmentation and raw material dependency

- Stringent and divergent regulatory pathways

Key Players: Johnson & Johnson (U.S.), Medtronic plc (U.S.), Abbott Laboratories (U.S.), Stryker Corporation (U.S.), Boston Scientific Corporation (U.S.), Zimmer Biomet Holdings Inc. (U.S.), Edwards Lifesciences Corporation (U.S.), Becton, Dickinson and Company (U.S.), Intuitive Surgical (U.S.), 3M Company (U.S.), B. Braun Melsungen AG (Germany), Smith & Nephew plc (UK), Koninklijke Philips N.V. (Netherlands), Terumo Corporation (Japan), Olympus Corporation (Japan), Cochlear Limited (Australia), Samsung Medison (South Korea), MicroPort Scientific Corporation (China), Meril Life Sciences Pvt. Ltd. (India), Biotronik SE & Co. KG (Germany).

Global Medical Implants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 110.5 billion

- 2026 Market Size: USD 118.4 billion

- Projected Market Size: USD 221.4 billion by 2035

- Growth Forecasts: 7.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, South Korea, Brazil, Singapore, Saudi Arabia

Last updated on : 27 May, 2026

Medical Implants Market - Growth Drivers and Challenges

Growth Drivers

- Increase in non-communicable diseases programs: The presence of massive government-based screening approaches for these diseases is resulting in unprecedented patient monitoring pipelines that positively cater to the medical implants market demand globally. According to official statistics published by the World Health Organization (WHO) in September 2025, non-communicable diseases negatively impacted almost 43 million people, which is readily equivalent to 75% of non-pandemic-based deaths worldwide. In addition, of the overall deaths, 73% have taken place across low and middle-income nations, with cardiovascular diseases accounting for 19 million deaths. However, to combat the occurrence, the overall payer pricing of healthcare, as per the March 2026 NLM article, particularly in the U.S., is expected to reach USD 6.2 trillion by the end of 2028, significantly catering to 20% of the gross domestic product (GDP), thus positively impacting the medical implants market growth.

- Health insurance penetration in low-income populations: The expansion of catastrophic health insurance coverage, particularly across low and middle-income nations, is increasingly transforming the medical implants market. As stated in an article published by the WHO in December 2025, the aspect of the universal health coverage index has successfully increased from 54 to 71 as of 2023. Additionally, there was a decrease in the population proportion not covered by crucial health services by almost 20% in the same year. However, as of 2022, globally, 2.1 billion people experienced financial challenges, with 1.6 billion people in poverty, which equates to 26% of the overall population and denotes the huge demand for health insurance services, which is proliferating the market expansion.

Challenges

- Supply chain fragmentation and raw material dependency: The medical implants market operates on a globally distributed, just-in-time supply model that has become dangerously brittle. Most high-grade titanium, cobalt-chromium, and specialty ceramics originate from a handful of geopolitical hotspots, while semiconductor supply for active implants remains concentrated in a few Asian fabrication plants. Any disruption, be it a maritime chokepoint closure, export restriction, or logistics breakdown, cascades rapidly across continents, halting production lines and delaying surgeries. Furthermore, the certification process for alternative material sources is notoriously lengthy, often taking years to requalify a new supplier to stringent medical device standards.

- Stringent and divergent regulatory pathways: The aspect of bringing a new medical implants to market requires navigating a labyrinth of regulatory regimes that vary significantly by geography. In this regard, the U.S. demands rigorous premarket approval processes, Europe’s new Medical Device Regulation (MDR) has raised compliance bars substantially, and Asia-based markets often have their own unique clinical evidence requirements. These divergent standards force manufacturers to maintain multiple product variants, conduct separate clinical trials, and manage distinct quality documentation systems. The result is extended time-to-market, often stretching innovation cycles by several years, and dramatically increased development costs, thereby restricting the medical implants market’s growth.

Medical Implants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.2% |

|

Base Year Market Size (2025) |

USD 110.5 billion |

|

Forecast Year Market Size (2035) |

USD 221.4 billion |

|

Regional Scope |

|

Medical Implants Market Segmentation:

Technology Segment Analysis

Based on the technology segment, the conventional implants sub-segment is anticipated to account for the largest share of 80.8% in the medical implants market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its foundational role in modernized medicine, which is suitable for providing structural support, restoring physical function, and significantly enhancing the quality of life for patients. According to official statistics published by NLM in October 2025, more than 7.5 million orthopaedic devices are readily implanted annually, and the worldwide orthopaedic implant industry is expected to reach USD 79.5 billion by the end of 2030. Besides, as per the May 2026 OEC data report, the global shipment valuation of orthopedic appliances was worth USD 81.6 billion as of 2024, along with 0.3% trade share and 5.9% as export growth, thereby enhancing their clinical applications across different regions.

Implantable Electronic Devices Clinical Applications, 2025

|

Device Name |

Size/Dimensions |

Metrics |

|

Cardiac Devices |

|

|

|

Micra Leadless Pacemaker |

Right ventricle, 25.9x6.7 mm, 2.0 g ECG, R-wave, Titanium, Nitinol |

Battery- 12 to 17 years Capture threshold- More than 1.2 V@0.24 ms, R-wave: 10.7 ± 5.0 mV |

|

S-ICD (Boston Scientific) |

Subcutaneous 83 × 69 × 12.7 mm Surface ECG Titanium |

Shock success: >98%; Battery: 7.5 years; Detection: 170–250 bpm |

|

Neural Interfaces |

|

|

|

DBS Electrodes (Medtronic) |

Subthalamic nucleus 1.27 mm diameter, 4 contacts LFP, Beta oscillations Platinum-Iridium |

Frequency: 60–185 Hz, Voltage: 0–10.5 V, Pulse width: 60–450 μs |

|

Neuralink N1 |

Cerebral cortex 23 × 8 mm chip, 1024 channels Spike activity Flexible polymer threads |

Threads: 64 per chip, Bandwidth: 20 kHz, Wireless: 10 Mbps |

|

Metabolic Sensors |

|

|

|

Abbott Libre 3 |

Subcutaneous arm 21 mm diameter × 2.9 mm Glucose Enzymatic sensor |

MARD: 8.9%, Lag: 1.8 ± 4.8 min, Duration: 14 days |

|

Eversense 365 |

Subcutaneous upper arm 18.3 × 3.5 mm Glucose (fluorescence) Fluoropolymer, Hydrogel |

MARD: 8.8%, Duration: 365 days, Calibration: 1/week |

|

GI/Biliary Devices |

|

|

|

Magnetoelastic Sensor |

Biliary stent surface 28 μm thickness Viscosity/Mass Metglas, PDMS, Ferrite |

SNR: 106, Detection: 17 cm distance, Sensitivity: 0.1% mass change |

|

Wireless pH Sensor |

Esophagus/Stomach 26 × 13 mm capsule pH, Temperature Silicon nanowire |

pH range: 0–14, Accuracy: ±0.1 pH, Battery: 48–96 h |

Source: NLM

Material Segment Analysis

The metallic biomaterials sub-segment, part of the material segment, is projected to garner the second-largest share in the medical implants market during the forecast period. The sub-segment’s growth is effectively fueled by the provision of necessary structural integrity, load-bearing capacity, and durability for repairing or replacing damaged musculoskeletal tissues. As stated in an article published by NLM in February 2022, both the Asia Pacific and North America are considered the fastest-growing and most significant biomaterials economies, respectively, along with a 13.6% yearly growth rate. Besides, implants are readily fabricated and designed based on the potential of biomaterials, and in this relation, Ti-6Al-4 V alloy, 316L stainless-steel (SS), Co-Cr–Mo, and nickel-titanium shape memory alloy (NiTi-SMA) metallic implant biomaterials are frequently utilized, thereby boosting the sub-segment’s expansion.

End user Segment Analysis

By the end of the stipulated timeline, the hospitals sub-segment, which is part of the end user segment, is expected to grab the third-largest share in the medical implants market. The sub-segment’s development is highly propelled by serving as the primary setting for complex implant procedures. These institutions offer the critical infrastructure required for successful surgical outcomes, including advanced operating theaters equipped with hybrid imaging capabilities, laminar airflow systems to minimize infection risk, and robotic-assisted surgical platforms. The multidisciplinary nature of hospitals for integrating anesthesiologists, specialty surgeons, radiologists, rehabilitation teams, and infection control specialists creates a comprehensive care ecosystem that ambulatory centers cannot fully replicate for high-acuity cases.

Our in-depth analysis of the medical implants market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

Material |

|

|

End user |

|

|

Product |

|

|

Application |

|

|

Functionality |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Medical Implants Market - Regional Analysis

North America Market Insights

North America in the medical implants market is anticipated to register the highest share of 44.7% by the end of 2035. The market’s uplift in the region is primarily attributed to an aging population and rising rates of chronic illnesses, technological integration for advanced materials and smart implants, a surge in healthcare expenditure, and a robust innovation ecosystem. According to official statistics published by The Lancet Regional Health – Americas in February 2026, a clinical study was conducted on a patient pool of 5,624 to evaluate the impact of chronic diseases by the U.S. Department of Health and Human Services (HHS). The study demonstrated that hypertension was one of the most prevalent chronic conditions, affecting 68.9 million adults, which was followed by 64.7 million adults suffering from cholesterol, 54 million from arthritis, and 52.1 million adults with chronic pain, thereby denoting a huge demand for the medical implants market to expand in the overall region.

The medical implants market is growing significantly in the U.S., owing to the aging demographic, an upsurge in the demand for cardiovascular and orthopedic implants, a high prevalence of lifestyle-based rare diseases, such as heart failure, obesity, and diabetes, along with the presence of outstanding healthcare spending and infrastructure. As stated in an article published by the CDC Government in October 2024, heart disease is one of the leading causes of death, with 1 person dying every 34 seconds in the country. In addition, 919,032 people died from cardiovascular disorders as of 2023, which is equivalent to 1 in every 3 deaths. Besides, the expense of healthcare medications and services for this disease amounts to over USD 168 billion as of 2022, thus bolstering the market demand. Moreover, an increase in the country’s national health expenditure is also fueling the medical implants market.

Monthly National Health Expenditure Analysis in the U.S., 2018a-2024

|

Components |

2018a |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

|

NHE (USD billion) |

3,637.7 |

3,805.1 |

4,204.3 |

4,376.9 |

4,586.6 |

4,925.3 |

5,278.6 |

|

GDP (USD billion) |

20,656.5 |

21,540.0 |

21,375.3 |

23,725.6 |

26,054.6 |

27,811.5 |

29,298.0 |

|

NHE as GDP % |

17.6 |

17.7 |

19.7 |

18.4 |

17.6 |

17.7 |

18.0 |

|

Population (million) |

329.4 |

331.3 |

332.7 |

333.2 |

335.1 |

337.8 |

341.1 |

|

NHE per capita |

USD 11,042 |

USD 11,487 |

12,637 |

13,137 |

13,689 |

14,580 |

15,474 |

|

GDP per capita |

USD 62,703 |

65,024 |

64,246 |

71,208 |

77,761 |

82,330 |

85,888 |

|

Chain-Weighted NHE Deflator |

102.3 |

103.3 |

106.3 |

108.0 |

111.4 |

114.7 |

117.5 |

|

GDP price index |

102.3 |

104.0 |

105.4 |

110.2 |

118.0 |

122.4 |

125.4 |

|

Real NHE Spending (USD billion) |

3,556 |

3,683 |

3,954 |

4,053 |

4,117 |

4,294 |

4,492 |

|

Real GDP Spending (USD billion) |

20,194 |

20,176 |

20,285 |

21,532 |

22,076 |

22,724 |

23,358 |

Source: Health Affairs Organization

The high burden of neurological diseases, the increased demand for innovative biomaterials, such as stainless steel and titanium for dental and orthopedic fixtures, consistent provincial healthcare investment, and a focus on supply chain integration into regional distribution networks are certain factors that are bolstering the medical implants market in Canada. As per an article published by Brain Injury Canada in 2024, more than 10 million people in the country are residing with neurological conditions, ranging from injuries, disorders, and illnesses, increasingly impacting regular life. In addition, 1 in 3 individuals is expected to have a neurological condition at some point in their lifetime. Moreover, both mental health and neurological disorders are estimated to amount to the domestic economy of USD 61 billion yearly, which is more than cardiovascular and cancer diseases, thereby driving the medical implants market growth.

APAC Market Insights

The Asia Pacific in the medical implants market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by fundamental transformation, reimbursement-based economies, an expansion in healthcare accessibility, regulatory frameworks, medical facilities, and expanded insurance coverage. According to official statistics published by NLM in November 2025, health service coverage is predicted to increase from 53.5% to 81.5% by the end of 2030, especially in South Asia. Simultaneously, the catastrophic health expenditure is projected to increase from 7.2% to 18.6% by the end of the same year. Besides, 4.5 billion people in the region lacked access to crucial health and medical services, while more than 1 billion experienced catastrophic health spending, and 344 million lived in poverty, thereby positively fueling the market development.

The medical implants market is gaining increased traction in China, owing to urban development, growth in the middle-class, an increase in the demand for dental and cosmetic restoration treatments, strengthened government programs, and the presence of major innovation and production bases. As stated in an article published by the ITA in August 2025, the country’s healthcare industry is considered the world’s second-largest facility, with an approximate valuation that surpassed USD 1 trillion as of 2024, and is further predicted to amount to more than USD 1.5 trillion by the end of 2029. Based on this growth, the country constituted over 40,000 hospital centers, which provided more than 8 million beds. Of these, public infrastructures provided 70.2% of hospital bed accommodations and successfully gained 83.4% of patient visits, thereby driving the market development in the nation.

The aspects of an increase in the elderly population, the rising prevalence of chronic diseases, the adoption of innovative implant technology, suitable supply chain dynamics, and organizational contributions are a few trends that are responsible for driving the medical implants market in Japan. Besides, the Japan medical implants market was worth USD 8.8 billion as of 2025, which is anticipated to be valued at USD 9.2 billion by the end of 2026, and eventually reach 14.4 billion by 2035, along with a 5.1% growth rate. Furthermore, as per an article published by the World Economic Forum in September 2023, more than 1 in 10 people in the country are currently aged over 80 years. In addition, nearly 1/3rd of the domestic population is aged more than 65 years, which is estimated to be 36.2 million, thereby denoting a huge growth and expansion opportunity for the market in the country.

Europe Market Insights

Europe in the medical implants market is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively driven by the demographic profile, an increase in the prevalence of arthritis, the presence of innovative healthcare facilities, a robust reimbursement framework, and leadership in orthopedic biomaterials innovation. According to official statistics published by NLM in January 2026, a clinical study was conducted on 6,767,340 individuals suffering from hip osteoarthritis (OA) and 6,805,777 from knee OA. The pooled prevalence of knee OA and hip OA in the region was roughly 10% and 6%, respectively. Besides, the study also demonstrated that the hip OA prevalence in the region ranged from 2% in the East part, followed by 7% in the South, while the knee OA prevalence ranged from 7% in the North to 19% in the East, thereby denoting a huge market growth and demand.

The medical implants market is gaining increased exposure in Germany, owing to strong healthcare infrastructure, leadership in orthopedic biomaterials, the existence of a statutory health insurance system, comprehensive coverage of implant procedures, sustained innovation, and the launch of manufacturing products. As stated in a data report published by the OECD in 2025, the health and medical spending per capita in the country is the highest, in comparison to other regional countries, which significantly reached USD 6,296.4 as of 2023. Additionally, the public funding readily accounted for 86% of overall health spending, while out-of-pocket expenses constituted the majority of private spending, which was 11%. This particular spending is well above the regional average of 16%, thereby denoting an optimistic outlook for the market expansion in the country.

Health Spending Per Capita Analysis in Germany, 2023

|

Components |

Germany |

Europe |

|

Compulsory or Government Schemes |

86% |

80% |

|

Private Sources |

14% |

20% |

|

Overall Health Spending |

USD 6,296.4 |

USD 4,456.2 |

Source: OECD

The tactical focus on innovative treatment options, emphasis on advanced therapies, a rise in medical expenditure, suitable government strategies, an expansion in robotic-driven surgery programs, the establishment of cardiac and orthopedic centers, and an alignment with global standards are certain trends that are proliferating the medical implants market in the UK. As per an article published by the British Heart Foundation in May 2024, there was an upsurge in cardiac waiting lists to 414,596 in March 2024, particularly in England, demonstrating a rise of 6,048 from February. In addition, the cardiac care waiting list is 78% large than in previous years, denoting an increase of 182,000 people. Moreover, 41% of people are on the waiting list for more than 18 weeks, which at present accounts for 168,403 patients, thus ensuring a massive demand for heath facilities in the country.

Key Medical Implants Market Players:

- Johnson & Johnson (U.S.)

- Medtronic plc (U.S.)

- Abbott Laboratories (U.S.)

- Stryker Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- Zimmer Biomet Holdings Inc. (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Becton, Dickinson and Company (U.S.)

- Intuitive Surgical (U.S.)

- 3M Company (U.S.)

- B. Braun Melsungen AG (Germany)

- Smith & Nephew plc (UK)

- Koninklijke Philips N.V. (Netherlands)

- Terumo Corporation (Japan)

- Olympus Corporation (Japan)

- Cochlear Limited (Australia)

- Samsung Medison (South Korea)

- MicroPort Scientific Corporation (China)

- Meril Life Sciences Pvt. Ltd. (India)

- Biotronik SE & Co. KG (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Johnson & Johnson maintains a diversified portfolio across orthopedics and cardiovascular implants through its DePuy Synthes and Biosense Webster divisions. The company prioritizes innovation in robotic-assisted joint replacement and digital surgical ecosystems to strengthen its competitive foothold.

- Medtronic plc leads across multiple implant categories, including cardiac rhythm management, spine, and neurostimulation, leveraging its extensive global distribution network. The company focuses on integrating artificial intelligence and smart sensor technologies into its implantable devices.

- Abbott Laboratories is a prominent player in cardiovascular and neuromodulation implants, known for its durable pacemakers and deep-brain stimulation systems. The company emphasizes minimally invasive device designs and remote patient monitoring capabilities.

- Stryker Corporation commands a strong position in orthopedic implants and surgical technologies, with particular strength in joint replacement and trauma fixation devices. The company continues to advance robotic-assisted surgery platforms and 3D-printed patient-specific implants.

- Boston Scientific Corporation holds a significant share in cardiovascular implants, especially in pacemakers, stents, and structural heart devices. The company strategically expands into neuromodulation and urology implants through targeted acquisitions and product line extensions.

Here is a list of key players operating in the global medical implants market:

The medical implants market remains highly consolidated, with U.S.-headquartered multinationals holding the dominant share, followed by strong regional leaders from Europe and the Asia Pacific. Notable players are pursuing strategic initiatives focused on three key areas, such as technological differentiation through smart implants and 3D-printed patient-specific devices, geographic expansion into high-growth Asia Pacific markets, and vertical integration to secure supply chains amid tariff-driven raw material cost pressures. Recent merger and acquisition activity, such as Boston Scientific’s acquisition of Axonics, highlights a strategic pivot toward high-margin neurostimulation and urology segments. Besides, in February 2025, Stryker completely acquired Inari Medical, Inc. to ensure an established peripheral vascular position for the company in the continuously growing venous thromboembolism segment, thus driving the medical implants industry.

Corporate Landscape of the Market:

Recent Developments

- In February 2026, Medtronic plc acquired CathWorks, with the intention of transforming coronary artery disease treatment and diagnosis, along with leveraging the power of AI and data for delivering advanced solutions.

- In October 2025, Boston Scientific Corporation entered into a definitive agreement for acquiring Nalu Medical, Inc., generously constituting an upfront cash payment of an estimated USD 533 million for the remaining equity and commercializing minimally invasive solutions.

- In October 2024, Johnson & Johnson acquired V-Wave Ltd., and deliberately expanded its position in cardiovascular disorders and ensured the provision of a huge opportunity for tackling heart risks.

- Report ID: 8586

- Published Date: May 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.