Smart Orthopedic Implants Market Outlook:

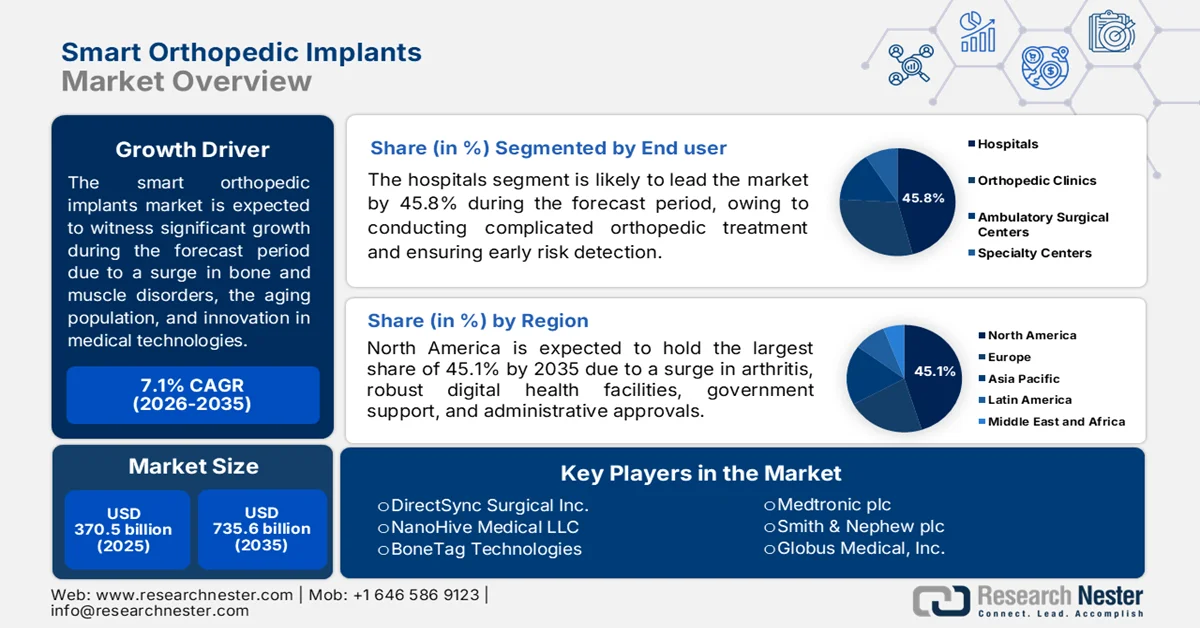

Smart Orthopedic Implants Market size was valued at USD 370.5 billion in 2025 and is expected to reach USD 735.6 billion by the end of 2035, registering around 7.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of smart orthopedic implants is evaluated at USD 396.8 billion.

The global smart orthopedic implants market is rapidly evolving, highly driven by forces such as tissue, bone, and muscle disorders, along with an increase in the elderly population, the increased demand for spinal surgeries and joint replacements, and expansion into technological factors. According to an article published by NLM in July 2024, the percentage of people aged more than 60 years is poised to be almost double, from 12% to 22%, by the end of 2050. This particular demographic transition raised public health risks, including chronic disease management, social support systems, and healthcare infrastructure requiring innovative policy solutions. Besides, chronic conditions account for over 75% of healthcare spending for individuals aged over 65 years, with the global payers’ pricing amounting to more than USD 1.5 trillion, thereby positively impacting the market’s growth and demand.

Furthermore, the expansion of customization and 3D printing, as well as a rise in tactical collaborations and partnerships, and a suitable evolution towards biochemical sensing, are a few trends that are responsible for driving the market globally. For instance, in June 2025, NanoHive Medical, LLC successfully secured an exclusive sub-license of DirectSync Surgical's piezoelectric implantable sensor technology, which is suitable for the spinal fusion field. Likewise, in February 2024, Exactech partnered with Statera Medical and designed the first-ever smart reverse shoulder implant, known as the goldilocks smart implant technology for assisting surgeons to aid patients. Therefore, with such acquisitions and partnerships, there is a huge growth opportunity for the market across different regions.

Key Smart Orthopedic Implants Market Insights Summary:

Regional Highlights:

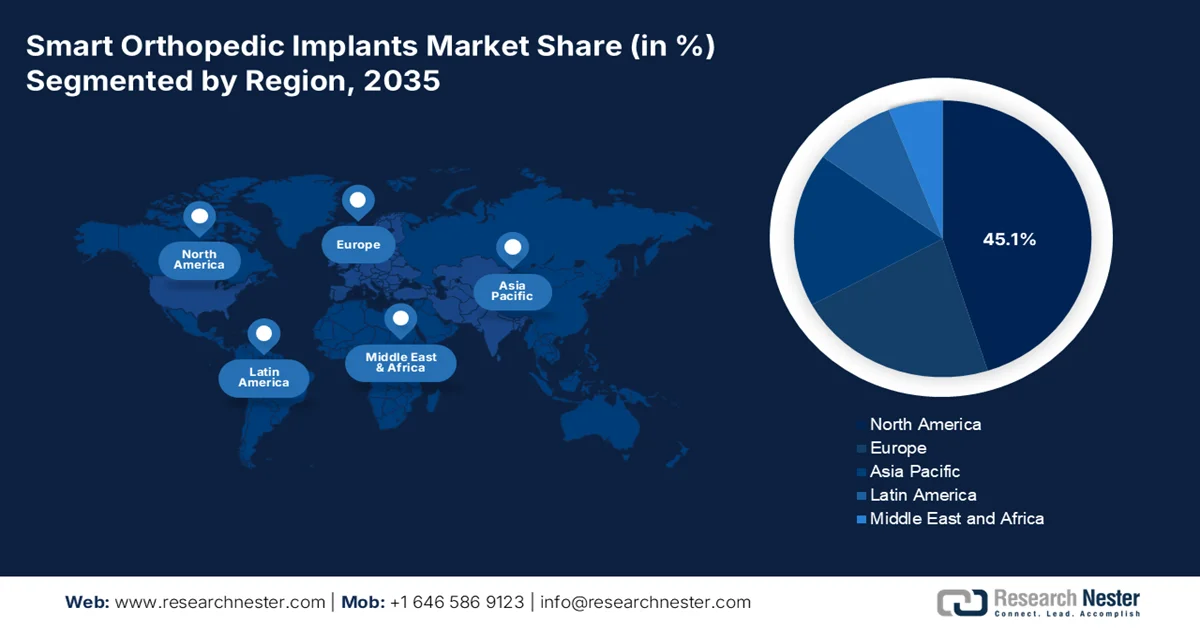

- Smart orthopedic implants market North America is anticipated to capture 45.1% of the market share by 2035, underpinned by rising arthritis prevalence, strong digital health infrastructure, supportive FDA initiatives, the transition toward value-based recovery models, and favorable government policies

- Asia Pacific is projected to register the fastest growth throughout 2026-2035, accelerated by the expanding aging population, increasing prevalence of musculoskeletal disorders, and rising healthcare expenditure

Segment Insights:

- Smart orthopedic implants market the hospitals segment is expected to account for 45.8% market share by 2035, strengthened by the growing adoption of advanced smart implant technologies for complex orthopedic procedures supported by sophisticated hospital infrastructure

- The titanium segment is forecast to secure 39.3% market share by 2035, reinforced by its superior physical properties and expanding use in smart orthopedic implants integrated with biosensors, microelectronics, and therapeutic surface technologies

Key Growth Trends:

- Integration of remote care

- Demand for reduced complications

Major Challenges:

- Stringent and evolving regulatory frameworks

- Data privacy, security, and ethical concerns

Key Players: Zimmer Biomet Holdings, Inc. (U.S.), Stryker Corporation (U.S.), Johnson & Johnson / DePuy Synthes (U.S.), Medtronic plc (Ireland), Smith & Nephew plc (UK), Globus Medical, Inc. (U.S.), Exactech, Inc. (U.S.), Corin Group plc (UK), MicroPort Scientific Corporation (China), OrthoSensor, Inc. (U.S.), SpineGuard S.A. (France), Intelligent Implants GmbH (Germany), Statera Medical Inc. (Canada), DirectSync Surgical Inc. (U.S.), NanoHive Medical LLC (U.S.), BoneTag Technologies (France), Orthofix Medical Inc. (U.S.).

Global Smart Orthopedic Implants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 370.5 billion

- 2026 Market Size: USD 396.8 billion

- Projected Market Size: USD 735.6 billion by 2035

- Growth Forecasts: 7.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.1% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Brazil, Saudi Arabia

Last updated on : 1 July, 2026

Smart Orthopedic Implants Market - Growth Drivers and Challenges

Growth Drivers

- Integration of remote care: The healthcare and medical landscape is continuously embracing digitalized health solutions, which have accelerated the smart orthopedic implants market globally. According to an article published by NLM in March 2024, a clinical study was conducted on 186 participants with chronic conditions utilizing telemedicine services. The study demonstrated a reduction in disease-specific markers from 12,000 to 11,000, along with a substantial reduction of symptom severity from 3,500 to 2,500, and overall health improvement status from 7,200 to 8,500. Besides, the savings in healthcare payers’ pricing also lowered from USD 25,000 to USD 12,000, and indirect expenses from USD 10,000 to USD 5,000, thus ensuring patient satisfaction and positively enhancing the market upliftment.

- Demand for reduced complications: This is one of the major drivers for the market, with increased focus on economic and clinical burden of post-surgical risks, such as periprosthetic joint infections and aseptic loosening. As stated in an article published by NLM in September 2025, the median incidence rate of adverse effects of medical treatment (AEMT) accounted for 9.2%, based on which 43% of cases are considered preventable and 7.4% leading to fatal results. Therefore, the aspect of diminishing the incidence of medical-based adverse cases and optimizing the quality of patient care is of great importance to medical health, thus denoting an optimistic outlook for the market’s demand globally.

Challenges

- Stringent and evolving regulatory frameworks: The aspect of navigating the complex and tightening regulatory landscape is a major hurdle for manufacturers of the market. These novel devices, which combine traditional implant materials with sensors, software, and wireless communication, often fall into new or poorly defined regulatory categories. For instance, the European Union's Medical Device Regulation (MDR) has significantly increased clinical data requirements, documentation, and post-market surveillance, leading to delays and the withdrawal of some products from the market. Similarly, in the U.S., gaining Premarket Approval (PMA) for these high-risk Class III devices can be an arduous process costing tens of millions of dollars and taking many years.

- Data privacy, security, and ethical concerns: The market tends to generate vast amounts of sensitive patient health data, raising significant concerns about data privacy and cybersecurity. The transmission of data from inside the patient's body to external healthcare providers or monitoring platforms creates potential vulnerabilities that could be exploited by malicious actors. A study found that patients harbor concerns that data from their smart implants could be shared with unintended recipients, underscoring the fear of privacy violations. There are also complex ethical questions regarding data ownership, algorithmic bias, and patient consent that lack clear regulatory guidelines, thereby limiting the market growth and expansion.

Smart Orthopedic Implants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.1% |

|

Base Year Market Size (2025) |

USD 370.5 billion |

|

Forecast Year Market Size (2035) |

USD 735.6 billion |

|

Regional Scope |

|

Smart Orthopedic Implants Market Segmentation:

End user Segment Analysis

Based on the end user, the hospitals segment is anticipated to account for the highest share of 45.8% in the smart orthopedic implants market by the end of 2035. The segment’s upliftment is highly fueled by its role as the primary destination for complex and high-acuity orthopedic procedures, including total joint replacements, spinal fusions, and multi-trauma surgeries that require advanced smart implant technologies. Additionally, its comprehensive infrastructure, including hybrid operating rooms, intraoperative imaging systems, and intensive care units, enables the integration of sensor-enabled implants that transmit real-time data on load, motion, and temperature. This readily facilitates early detection of complications such as implant loosening or infections, driving adoption among orthopedic surgeons.

Material Segment Analysis

The titanium segment under material is projected to grab the second-highest share of 39.3% in the market during the forecast period. The segment’s growth is effectively driven by its role as a crucial foundational material due to outstanding physical properties, embedded with therapeutic surface technologies, biosensors, and microelectronics. According to a data report published by the USGS Publications Warehouse in August 2025, there was an increase in the U.S. production of titanium concentrates to 300,000 metric tons as of 2022 from 200,000 metric tons in the previous year. Additionally, the country was estimated as the 81% net importer of titanium concentrates and 95% importer of titanium sponge. Likewise, as per the 2022 World Integrated Trade Solution (WITS), India also imported titanium ores and concentrates across various countries, with a shipment of 40,248,600 kg and amounting to USD 17,601.1 thousand, thus proliferating the segment’s growth and expansion globally.

Global Titanium Shipment Imports from India, 2022

|

Countries |

Production (Kg) |

Trade Valuation (USD 1,000) |

|

Japan |

77,753,000 |

59,870.5 |

|

Other Asia |

30,718,800 |

48,572.8 |

|

China |

41,170,200 |

22,061.2 |

|

Europe |

40,248,600 |

17,601.1 |

|

Germany |

30,610,000 |

1,372.0 |

|

Malaysia |

4,186,000 |

6,652.0 |

|

Netherlands |

339,860 |

169.2 |

|

Uganda |

52,000 |

91.0 |

|

Nigeria |

5,130 |

19.3 |

|

South Africa |

33 |

2.3 |

Source: WITS

Product Type Segment Analysis

By the end of the stipulated timeline, the knee reconstruction sub-segment, part of the product type segment, is expected to capture the third-largest share, at 35.2%, in the market. The sub-segment’s development is driven by the need for a vital surgery to replace damaged cartilage and bone with artificial parts to overcome chronic pain and restore movement. As stated in an article published by NLM in November 2025, there was a surge in total hip arthroplasties (THA) and total knee arthroplasties (TKA) by 73% and 105% in Australia, with a similar concentration in the U.S. and Europe. Besides, TKA rates in the U.S. are expected to increase by 673% and THA by 174% by the end of 2030. Meanwhile, revised TKA incidences are predicted to increase by 90% by the end of 2050, thereby making it suitable for boosting the sub-segment’s demand.

Our in-depth analysis of the smart orthopedic implants includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Material |

|

|

Product Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Smart Orthopedic Implants Market - Regional Analysis

North America Market Insights

The North America smart orthopedic implants market is anticipated to account for the highest share of 45.1% by the end of 2035. The market’s upliftment in the region is primarily attributed to an increase in arthritis prevalence, the existence of a strong digital health facility, support provision from the FDA, a shift to recovery models, and suitable government approaches. According to an article published by NLM in September 2024, it has been estimated that 53.2 million adults, particularly in the U.S., which is equivalent to 21.2% of the population, are diagnosed with fibromyalgia, lupus, gout, rheumatoid arthritis, and arthritis. Besides, arthritis is one of the most significant public health burdens, affecting roughly 21% of adults in the U.S. Moreover, the government’s Healthy People 2030 approach aims to diminish the population with arthritis from 55.3% to 52.1%, thus positively driving the market in the region.

The U.S. smart orthopedic implants market is growing significantly, owing to the development of fund sensor-integrated implants, innovations in tracking high-implant, an expansion in reimbursements, fueling the demand for joint replacement, and the transition to value-based care. As stated in an article published by the Arthroplasty Organization in April 2024, the American Joint Replacement Registry (AJRR) demonstrated a 2.5% rate for cementless total hip and 2.1% for cemented total knees. In addition, the AJRR also indicated a 23% surge in patient-reported outcome measures (PROMS) as of 2023, and continues to support both Medicaid and Medicare services. Moreover, ambulatory surgery centers (ASCs) noted an 84% increase in arthroplasty procedures, thereby denoting an optimistic outlook for the market’s growth in the country.

The existence of a publicly funded healthcare system, the smart implant adoption, provincial health systems, the provision of generous investments, along with collaboration with industrial stakeholders for establishing standards for data transmission are certain factors for boosting the market in Canada. As per an article published by the Commonwealth Fund in May 2026, the country accounts for 11.2% of healthcare expenditure in the form of gross domestic product (GDP). This is followed by 81.6 years of life expectancy at birth, as well as 100% of public insurance coverage. Besides, at the federal level, the government offers suitable coverage for prescription drugs for nearly 1 million people to ensure drug benefit strategies, particularly to patients aged more than 65 years with cancer, thus positively driving the market’s growth and demand in the overall nation.

APAC Market Insights

The Asia Pacific market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the aging population, a rise in the prevalence of musculoskeletal disorders, and an increase in healthcare spending. According to an article published by NLM in June 2025, there was an increase in osteoarthritis and gout, especially in China by 150.4% and 160.5%, which is followed by 65.3% of gout in Japan, as well as rheumatoid arthritis and gout in South Korea by 164.4% and 165%. Besides, Japan comprises the most aging population, with an aging rate of 29.1%, followed by 19.2% in South Korea and 13.5% in China. Moreover, musculoskeletal disorders are ranked as the second-most contributing factor to disabilities, thus fueling the market’s development in the region.

The China smart orthopedic implants market is gaining increased traction, owing to regulatory pathways for enabling advanced medical devices, escalating the market entry for smart implants, government expenditure, and a rise in disposable incomes, along with expanded healthcare coverage. As stated in a data report published by the ITA in September 2025, the medical device sector in the country is projected to grow at an 8.9% growth rate by the end of 2029, with the industry size amounting to USD 55.2 billion. In this regard, medical device imports accounted for 12% of the domestic economy, and meanwhile, suppliers in the U.S. catered to 25.5% of the national medical device imports, valued at USD 5.4 billion as of 2023. Therefore, the medical device industry is an essential sector for high-end and high-tech medical devices, thereby bolstering the market’s development in the country.

The aspects of innovation in medical technology, the presence of a strong healthcare system, the adoption of digital health solutions, the elderly population, and an increase in joint disorder prevalence leading to the demand for hip and smart knee implants, are a few factors that are positively fueling the smart orthopedic implants market in Japan. As per the 2026 GNIUS article, the healthcare expenditure accounts for 11.4% of the country’s GDP as of 2022, with 47 prefectures comprising a standard insurance scheme based on the residence place, and employment-specific plans for more than 1,400 people. Besides, in terms of the healthcare system, insurance services for specialist and hospital care are provided by private and public hospitals and reimbursed by insurers, with patients spending roughly 30% out-of-pocket, thus positively enhancing the market development.

Europe Market Insights

Europe market is projected to witness a considerable share by the end of the stipulated timeline. The market’s growth in the region is effectively driven by innovative healthcare infrastructure, a rise in the prevalence of orthopedic conditions, robust emphasis on advanced medical solutions, generous investment in research and development, and the enhancement of digital health technologies. According to a report published by OECD in November 2024, almost 1 million hip replacements were significantly performed in the region, along with 680,000 knee replacements. In addition, 202 hip replacements per 100,000 population, along with 134 knee replacements per 100,000 population, were also performed. Besides, Denmark, Austria, and Germany accounted for the highest rate of such replacements, and with Belgium, these nations constituted hip replacement rates almost 40% higher than the regional average.

The Germany market is gaining increased exposure, owing to the existence of a strong medical technology ecosystem, suitable government support, standard implant performance, innovative manufacturing capabilities, and health funding initiatives. As stated in a data report published by the Germany Trade and Invest (GTAI) in 2025, the overall healthcare expenditure of the country amounts to USD 612.8 billion as of 2024, while the medical technology industry was worth USD 39.8 billion as of 2025. Additionally, the total medtech production valuation in the country was worth USD 52.4 billion in 2024, significantly comprising 265,000 employees in the medical technology industry. Besides, the country also comprises an estimated 1,500 medtech manufacturers with over 20 employees as of 2025, thus enhancing the market upliftment.

Medical Device Manufacturers in Germany, 2024

|

Number of Employees |

Organizations |

Total Employee |

|

250+ |

106 |

90,742 |

|

100 to 249 |

165 |

25,333 |

|

50 to 99 |

258 |

17,853 |

|

20 to 49 |

951 |

27,571 |

|

0 to 19 |

10,000 |

104,000 |

|

|

|

Total- 265,000 |

Source: GTAI

The regulatory support, NHS modernization, the administrative approval of robotic surgery systems, the health system’s standard commitment to innovative orthopedic technologies, and advancements in replacement procedures are a few trends that are responsible for fueling the smart orthopedic implants market in the UK. As per an article published by the NCBI in March 2026, a survey-based study was conducted on 153 NHS trusts, of which 97% responded regarding the adoption of robotic-assisted surgical systems (RASS). Of this, 67% utilized these systems as of 2024, in comparison to only 20% in the past 10 years. Besides, by the end of 2024, 212 RASS were significantly operational in the country. Moreover, there was a surge in robotic procedure volumes from 3,622 to 36,209 in the same year, thus positively impacting the market growth and expansion.

Key Smart Orthopedic Implants Market Players:

- Zimmer Biomet Holdings, Inc. (U.S.)

- Stryker Corporation (U.S.)

- Johnson & Johnson / DePuy Synthes (U.S.)

- Medtronic plc (Ireland)

- Smith & Nephew plc (UK)

- Globus Medical, Inc. (U.S.)

- Exactech, Inc. (U.S.)

- Corin Group plc (UK)

- MicroPort Scientific Corporation (China)

- OrthoSensor, Inc. (U.S.)

- SpineGuard S.A. (France)

- Intelligent Implants GmbH (Germany)

- Statera Medical Inc. (Canada)

- DirectSync Surgical Inc. (U.S.)

- NanoHive Medical LLC (U.S.)

- BoneTag Technologies (France)

- Orthofix Medical Inc. (U.S.)

- Acumed (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Zimmer Biomet Holdings, Inc. leads in smart knee technology with its Persona IQ sensor-enabled implant, which provides objective patient activity data post-surgery. The company leverages its broad portfolio and global distribution network to maintain a strong presence across all major orthopedic segments, including hips, spine, and extremities.

- Stryker Corporation combines smart orthopedic implants with its Mako robotic-assisted surgical platform, creating a comprehensive digital solution for joint replacement. The company's focus on innovation and minimally invasive techniques has solidified its leadership across the knee, hip, and trauma markets.

- Johnson & Johnson/DePuy Synthes offers one of the industry's most extensive orthopedic portfolios, covering joint reconstruction, trauma, spine, and sports medicine. The company invests heavily in digital surgery platforms and data-driven solutions, aiming to integrate smart technologies across its product lines.

- Medtronic plc focuses on advanced surgical navigation, robotic-assisted procedures, and implantable devices for spinal conditions. The company's expertise in neuromodulation and data integration positions it uniquely in the smart implant space for spine applications.

- Smith & Nephew plc emphasizes innovation in robotics-assisted surgery through its CORI Surgical System and advanced implant materials. The company continues to expand its digital health capabilities, focusing on knee and hip reconstruction technologies.

Here is a list of key players operating in the global market:

The smart orthopedic implants market is moderately consolidated, dominated by large-cap medical technology multinationals headquartered in the U.S. and Western Europe that command significant global market share through diversified product portfolios spanning smart knee, hip, spine, and shoulder systems. Competitive differentiation centers on proprietary sensor integration, robotic-assisted surgical platforms, and real-time data analytics ecosystems that enable remote patient monitoring and predictive complication detection. Moreover, mid-tier players compete through specialization in specific anatomies or technologies, while emerging entrants focus on niche sensor innovations. Besides, in March 2025, Johnson & Johnson MedTech unveiled the newest orthopedic solutions and technologies at the American Academy of Orthopaedic Surgeons (AAOS) 2025 Annual Meeting in California. This included the introduction of VELYS™ robotic-assisted solution, the expansion of VOLT™ trauma system, and others, thus positively impacting the smart orthopedic implants industry.

Corporate Landscape of the Market:

Recent Developments

- In February 2026, Stryker launched the limited release of the Mako Robotic Power System (RPS), which is suitable for total knee replacement and considered an intuitive handheld robotic system for combining power tools and proven robotics.

- In November 2025, Acumed successfully acquired assets from TECHFIT Digital Surgery, which is a partner in its Craniomaxillofacial (CMF) patient-specific solutions portfolio, representing a crucial step in the growth strategy.

- Report ID: 8652

- Published Date: Jul 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Smart Orthopedic Implants Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.