Payment as a Service Market Outlook:

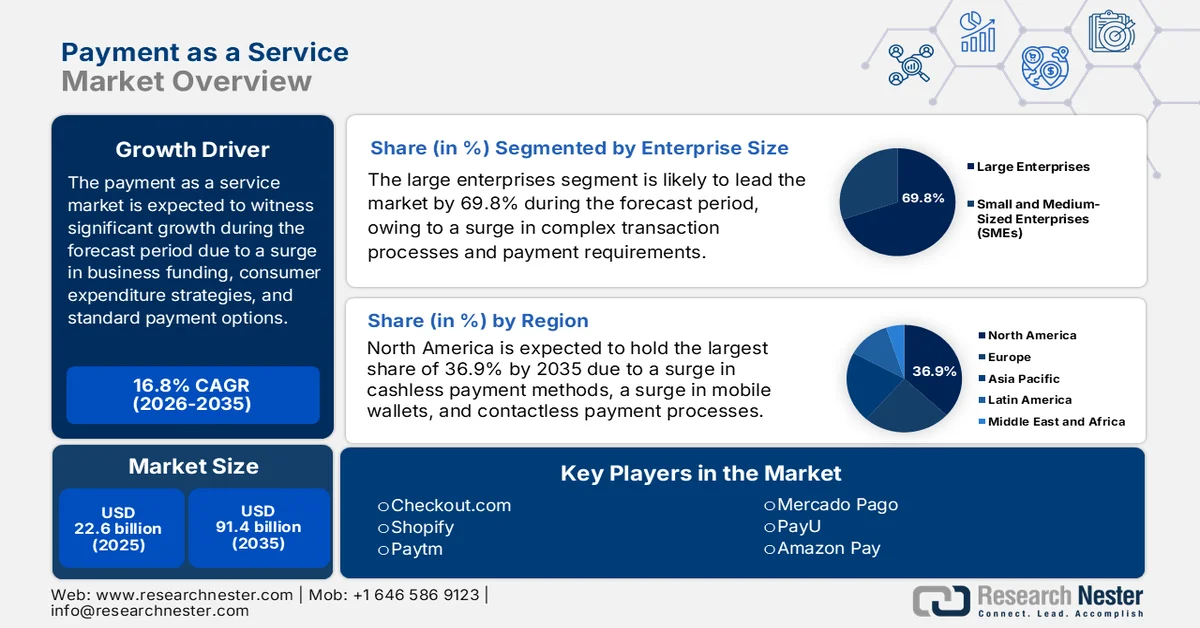

Payment as a Service Market size was valued at over USD 22.6 billion in 2025 and is expected to reach USD 91.4 billion by the end of 2035, growing at a CAGR of 16.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of payment as a service is evaluated at USD 26.4 billion.

The worldwide payment as a service market is positively shaped by different foundational factors, including fluctuations in both business investment and consumer spending patterns in new technologies, business operational efficiencies, suitable payment solutions, cross-border payment flows, and an escalation in developing alternative payment corridors. According to official statistics published by the World Economic Forum in January 2025, the United Nations Tourism reported that international tourism has reached 96% of pre-pandemic levels in the first 7 months of 2024. Likewise, Visa demonstrated that travelers are significantly travelling for long-lasting durations, which is positively driving the market demand. Besides, the worldwide e-commerce sales for B2B businesses are projected to reach USD 36 trillion by the end of 2026, denoting a rise from USD 10 trillion. Therefore, this aspect of long traveling duration and rise in e-commerce sales is deliberately responsible for uplifting the market exposure globally.

Country-Wise Average Length Analysis of a Trip by Travelers (2019 and 2023)

Source: World Economic Forum

Furthermore, the rise of agentic commerce, the tactical shift from cost center to growth lever, and the proliferation of vertical and specialized payment solutions are certain trends that are positively impacting the payment as a service (PaaS) market globally. As per a data report published by the Bank for International Settlements in December 2024, Pix, which is an instant payment system, has been readily implemented in Brazil, and more than 90% of the adult population have received or initiated a Pix transaction between July 2023 and 2024. Likewise, the central bank in Mexico introduced Dinero Móvil in 2023, which has been developed upon the large-scale Interbank Electronic Payments System. Similarly, Costa Rica witnessed a similar success story with SINPE Móvil, with almost 80% of adults utilizing it as of August 2024, thereby making it suitable for driving the market expansion globally.

Key Payment as a Service Market Insights Summary:

Regional Highlights:

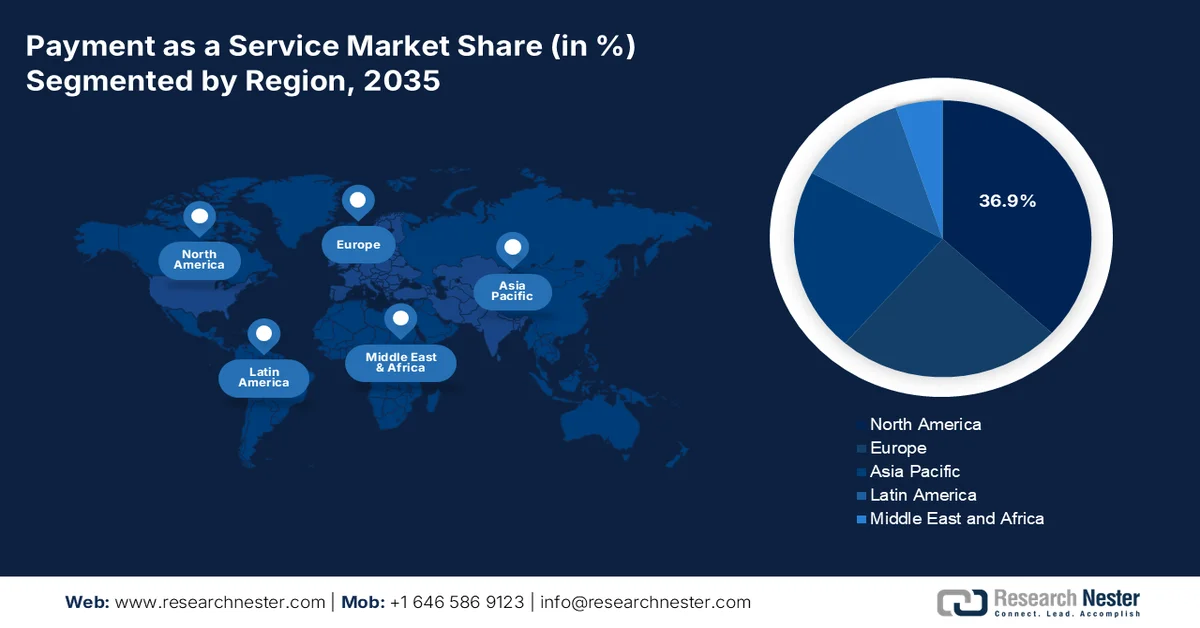

- North America in the payment as a service market is forecasted to capture a leading 36.9% share by 2035, attributed to mature digital infrastructure, high adoption of cashless payments, and strong fintech ecosystem presence

- Asia Pacific is poised to register the fastest growth over the 2026–2035 period, stimulated by rapid digital transformation, expanding e-commerce volumes, and widespread smartphone penetration

Segment Insights:

- The large enterprises sub-segment in the payment as a service market is projected to account for a dominant 69.8% share by 2035, propelled by complex transaction volumes and multifaceted payment requirements

- The platforms and solutions segment is expected to secure the second-largest share over the 2026–2035 period, fueled by the transition toward cloud-based agile systems and rising adoption among tech-savvy younger populations

Key Growth Trends:

- The economic imperative of cloud-based economics

- Escalation in pro-innovation regulation

Major Challenges:

- The intractable problem of legacy technology modernization

- Privacy regulation versus frictionless user experience

Key Players: PayPal, Stripe, Block, Inc., Adyen, Fiserv, FIS, Global Payments, Mastercard, Visa, Worldpay, Checkout.com, Shopify, Paytm, Mercado Pago, PayU, Amazon Pay, Google Pay, Apple Pay, Paysafe, Ingenico.

Global Payment as a Service Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 22.6 billion

- 2026 Market Size: USD 26.4 billion

- Projected Market Size: USD 91.4 billion by 2035

- Growth Forecasts: 16.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.9% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, Indonesia, Vietnam, Philippines, Malaysia

Last updated on : 19 March, 2026

Payment as a Service Market - Growth Drivers and Challenges

Growth Drivers

- The economic imperative of cloud-based economics: The fundamental economic benefit of cloud-based architectures is the ultimate driver for the payment as a service market globally. According to official statistics published by OECD in November 2025, over 90% of overall businesses account for more than half of total business value added and employment. This denotes that their suitable actions tend to significantly escalate progress towards sustainability targets, which is positively impacting the market demand across different regions. Besides, as per an article published by NLM in December 2022, small and medium enterprises (SMEs) readily account for an estimated 62% points of gross domestic product (GDP), along with 66% of job opportunities globally, thereby making it suitable for boosting the market exposure.

- Escalation in pro-innovation regulation: The international regulatory environment is presently acting as a suitable catalyst for technological adoption and modification, which is fueling the market’s exposure. For instance, based on the December 2024 PIB Government estimates, Unified Payments Interface (UPI) has processed an outstanding USD 280 billion across 16.5 billion financial transactions in India as of October 2024, denoting a 45% YoY growth from 11.4 billion transactions in October 2023. Besides, with 632 banks connected to UPI platforms, this increase has highlighted its expansion dominance in the country's payment landscape. As a result, more businesses and individuals embrace the security and convenience of digitalized transactions, thus making it suitable for market growth and expansion.

- Expansion in cross-border commerce: The market’s worldwide expansion is not only about accepting international credit cards, but the necessity to ensure a local-first approach for cross-border commerce. As stated in an article published by NLM in December 2022, 15% of overseas sellers have provided products to consumers through e-commerce channels, demonstrating a 25% increase from previous years. Moreover, by the end of 2022, B2C cross-border online sales significantly accounted for 22% of worldwide e-commerce. Therefore, based on the economic surplus and increased growth, there is a comprehensive consensus that cross-border e-commerce has emerged as one of the most essential pillars of global trade facilities, thus driving the market expansion.

Challenges

- The intractable problem of legacy technology modernization: Financial institutions are trapped by their legacy payment infrastructure, which is simultaneously expensive to maintain and a barrier to innovation. The modernization journey itself is fraught with peril. One of the most significant technical hurdles in the payment as a service (PaaS) market is extracting business requirements and rules from legacy code, a process that is complex, costly, and risks business continuity. While PaaS solutions offer a pathway to modernization, banks must navigate a difficult decision between building in-house, purchasing commercial-off-the-shelf platforms, or leveraging cloud-based PaaS, each with trade-offs in cost, control, time-to-market, and required skill sets. This complexity often leads to paralysis, leaving institutions stuck with inflexible systems that cannot keep pace with market demands.

- Privacy regulation versus frictionless user experience: A fundamental tension in the payment as a service market is emerging between stringent data privacy regulations and the seamless user experience that defines successful PaaS platforms. India's Digital Personal Data Protection Act (DPDPA) of 2023, while essential for safeguarding citizen data, exemplifies this conflict. Its rigid, consent-centric model threatens to introduce significant friction into the UPI ecosystem, which processes over 18 billion transactions monthly. Payment providers, led by NPCI, have sought exemptions, arguing that category-level consent is necessary to maintain the seamlessness that drove digital adoption. This challenge is not unique to India globally, and regulators are grappling with how to balance privacy rights with commercial utility.

Payment as a Service Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

16.8% |

|

Base Year Market Size (2025) |

USD 22.6 billion |

|

Forecast Year Market Size (2035) |

USD 91.4 billion |

|

Regional Scope |

|

Payment as a Service Market Segmentation:

Enterprise Size Segment Analysis

The large enterprises sub-segment, part of the enterprise size, is anticipated to garner the largest share of 69.8% in the payment as a service market by the end of 2035. The sub-segment’s upliftment is highly attributed to its complex transaction volumes and multifaceted payment requirements. These organizations, spanning global retail chains, multinational banks, and Fortune 500 corporations, process millions of transactions annually across diverse geographic markets, each with unique payment preferences and regulatory frameworks. The scale of their operations renders legacy, on-premise payment systems increasingly inadequate, as maintaining separate payment infrastructures for each country or channel becomes prohibitively expensive and operationally cumbersome, thus making it suitable for bolstering the market growth internationally.

Component Segment Analysis

The platforms and solutions segment in the payment as a service (PaaS) market is projected to hold the second-highest share during the forecast period. The segment’s growth is highly driven by its importance for transforming rigid legacy financial systems into cloud-based and agile environments. According to official statistics published by Computers in Human Behavior Reports in December 2024, almost 60% of the population is aged under 25 years, denoting a critical factor in the rise of digital payment platforms and solutions, especially in Cambodia, with its existing tech-savvy population. This particular demographic group is extremely receptive to new technologies, leading to a growth opportunity for the market. In addition, this shift provides suitable ground for rapidly incorporating digital payment systems, thus bolstering the sub-segment’s development.

End user Segment Analysis

The retail and e-commerce sub-segment, which is part of the end user segment, is expected to hold the third-highest share in the market by the end of the stipulated timeline. The sub-segment’s development is effectively propelled by the relentless digitization of commerce and evolving consumer expectations for frictionless checkout experiences. Online retailers face the immediate challenge of cart abandonment, with complex or slow payment processes directly correlating with lost revenue, a problem that a PaaS solution directly addresses by offering one-click checkout, digital wallet integration, and localized payment methods. The modern consumer expects to pay via their preferred method, whether that means credit cards in the United States, iDEAL in the Netherlands, or UPI in India, and PaaS platforms provide the unified API infrastructure to offer this diversity without complex integrations for each payment type.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Enterprise Size |

|

|

Component |

|

|

End user |

|

|

Service Type |

|

|

Payment Mode |

|

|

Provider Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Payment as a Service Market - Regional Analysis

North America Market Insights

North America in the payment as a service (PaaS) market is anticipated to garner the largest share of 36.9% by the end of 2035. The market’s upliftment in the region is highly driven by the presence of mature digital infrastructure, increased consumer adoption of cashless payment methods, and the existence of major fintech innovators, along with a surge in mobile wallet usage and contactless payments. According to official statistics published by the Tony Blair Institute for Global Change in March 2022, there has been an increase in the U.S.-based government websites providing online services from 22% to 89%. This also led to doubling the internet penetration in both the U.S. and Canada, from 50% in both nations to 93% in the U.S. and 95% in Canada. Besides, both these nations are federal democracies, hence the digital transformation takes place simultaneously, thus positively attributing the market upliftment in the overall region.

The market in the U.S. is growing significantly, owing to growth in digital commerce, insatiable demand for secure, diverse, and seamless payment processing solutions, the adoption of innovative technologies, AI deployment, and organizational investment for enhancing fraud detection, automating operations, and personalizing customer experiences. As per an article published by NLM in October 2022, 82% of individuals in the country utilize digital payments, denoting an increase from 78% and 72% in the past 5 years. Besides, as per the January 2022 Federal Reserve Board article, about 20% households in the country have increased bank accounts and continue to depend on financial services, including check-cashing services, payday loans, and money orders, thereby making it suitable for boosting the market expansion in the overall nation.

The robust adoption of digital banking, payments by domestic consumers and businesses, strong technology industry presence, clear preference for digitalized financial services, and a significant portion of the population utilizing mobile banking applications are factors for uplifting the payment as a service market in Canada. As stated in an article published by the Government of Canada in May 2024, 20% of adults aged more than 65 years have been without Internet accessibility, but still prefer to adopt online banking in comparison to the young population. Additionally, as of 2022, 76% of Internet users aged between 65 and 74 years have been banked online, while the remaining 24% either adopted conventional banking methods, including automated teller machine (ATM), phone, or branch, or completely avoided banking services. Therefore, there is a huge growth scope for the overall market in the country, with the increased focus on its applications.

APAC Market Insights

The Asia Pacific in the payment as a service (PaaS) market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by the region’s unprecedented digital transformation, a surge in e-commerce volumes, wide-ranging smartphone adoption, and an advanced leapfrog in technologies that tend to bypass conventional banking infrastructure. According to official statistics published by the World Economic Forum in February 2022, Malaysia and the Philippines have emerged as the top two countries in the overall with growth in e-commerce retail, which is gradually increasing by 23% and 25% every year, respectively. Besides, the region presently accounts for almost 60% of the global online retail sales, with an upsurge in the e-commerce industry that doubled by the end of 2025 and significantly reached USD 2 trillion, thus driving the market growth.

E-Commerce Retail Growth Analysis in the Asia Pacific (2022)

|

Countries |

Growth |

|

Philippines |

25.0% |

|

Malaysia |

23.0% |

|

India |

21.0% |

|

Korea |

19.5% |

Source: World Economic Forum

The market in China is gaining increased traction, owing to the rising digital economy, pioneering role in mobile payments, cross-border digital payment services, prioritizing digital payment infrastructure as one of the cornerstones of the domestic digital economy approach, and increased focus on payment advancements. As per an article published by the China and World Organization in October 2025, there has been an increase in travelers utilizing active mobile payment as of 2025, surpassing 10 million. Besides, the country’s mobile payment penetration rate has also risen effectively, reaching 86%, with governmental efforts focusing on combining the comparative strengths of digital payments, card transactions, and cash to develop a composite payment mechanism for worldwide visitors. Therefore, with this increase, there is a huge growth opportunity for the market in the overall country.

The aspects of revolutions in digital payments through the unified payments interface, focus on digital transformation, especially across the chemical industry, for developing specialized B2B payment solutions for cross-border settlements and supply chain financing, and business-based digital payment processes are factors developing the market in India. Based on government estimates published by the PIB Government in January 2025, the forefront of the country’s digital payment revolution is UPI, with a record of 16.7 billion transactions as of December 2024, along with a staggering transaction value amounting to USD 251 billion. This denotes a huge jump from USD 233.2 billion in November 2024. Additionally, UPI effectively processed almost 172 billion in transactions, denoting a 46% surge from 117.6 billion as of 2023, thereby fueling the market demand in the country.

UPI Transaction Analysis in India (2024)

|

Months |

Growth Prevalence (Millions) |

|

January |

12,203 |

|

February |

12,103 |

|

March |

13,440 |

|

April |

13,304 |

|

May |

14,036 |

|

June |

13,885 |

|

July |

14,436 |

|

August |

14,963 |

|

September |

15,042 |

|

October |

16,585 |

|

November |

15,482 |

|

December |

16,730 |

Source: PIB Government

Europe Market Insights

Europe in the payment as a service (PaaS) market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by the existence of the digitalized commerce ecosystem, rise in account-to-account services, the emergence of AI-based commerce with smart AI agents, the regulatory landscape pertaining to digitalized regional frameworks, and the adoption of advanced open banking. According to a data report published by the Manifesto 2030 in 2024, in terms of digitalization, the overall region successfully reached the suitable target of 70% of households and has accessibility to 100 Mbps as of 2025. Primarily, broadband services are significantly integrated into digital, automated, and modernized payment ecosystems, thereby denoting a huge growth opportunity for the market in the region.

The market in Germany is gaining increased exposure, owing to an entrenched industrial base, generation of substantial B2B transaction volumes, robust consumer adoption of contactless and mobile payment methods, and the regulatory environment under Bafin and suitable compliance with PSD2 policy. Besides, based on government estimates published by the ITA in August 2023, the financial technology demand and industry have significantly reached a 64% adoption as of 2023. Additionally, it is further projected to grow steadily due to the 2022 GDP per capita of USD 48,432, USD 21,704 as consumption spending, 97% of the population having accounts at financial institutions, and over 75% of the population are digital payment users since 2023. Therefore, all these have resulted in the availability of aggregate mobile payment services, which are positively impacting the market growth in the country.

The escalating growth originating from policy environment, market dynamics, innovative payment methods, mature fintech ecosystem, the regulatory approach to foster experimentation, and enabling rapid deployment of the newest payment technologies are certain trends fueling the market in the UK. As stated in an article published by the ITA in January 2023, the fintech industry in the country comprises more than 1,600 organizations, with London evolving as the third-biggest fintech facility, with USD 3.6 trillion of regular foreign exchange trades transactions. Besides, high-level investments are readily driving the robust fintech ecosystem, based on reaching USD 11.6 billion in venture capital investment. Therefore, the investment growth for the industry is 217%, which is positively creating an optimistic outlook for the market in the country.

Key Payment as a Service Market Players:

- PayPal (U.S.)

- Stripe (U.S.)

- Block, Inc. (formerly Square) (U.S.)

- Adyen (Netherlands)

- Fiserv (U.S.)

- FIS (U.S.)

- Global Payments (U.S.)

- Mastercard (U.S.)

- Visa (U.S.)

- Worldpay (UK)

- Checkout.com (UK)

- Shopify (Canada)

- Paytm (India)

- Mercado Pago (Brazil)

- PayU (Netherlands)

- Amazon Pay (U.S.)

- Google Pay (U.S.)

- Apple Pay (U.S.)

- Paysafe (UK)

- Ingenico (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- PayPal remains a dominant force in the PaaS market by leveraging its extensive two-sided network connecting consumers and merchants globally. The company continues to expand its service offerings beyond basic processing to include comprehensive checkout solutions, payouts, and buy now, pay later options, solidifying its position as a versatile payment partner for businesses of all sizes.

- Stripe has established itself as the foundational technology layer for countless internet-based businesses, providing a suite of modular, API-first payment tools. Its strategy focuses on economic infrastructure for the digital economy, enabling platforms and marketplaces to seamlessly integrate payments, manage revenue, and launch new business models with ease.

- Block, Inc. serves the PaaS market by offering integrated ecosystems that combine payment processing with sophisticated software solutions for sellers and individuals. Through its Square and Cash App ecosystems, the company democratizes access to financial tools, enabling small and micro-merchants to accept payments and manage their operations alongside providing peer-to-peer payment capabilities.

- Adyen distinguishes itself in the PaaS landscape with its single, unified platform that provides end-to-end payment capabilities directly, bypassing the need for third-party integrations. This unified commerce approach is particularly attractive to large enterprises and retailers seeking a consistent payment experience across online, mobile, and in-store channels globally.

- Fiserv empowers financial institutions and businesses with a comprehensive suite of PaaS solutions. Its strategy emphasizes modernization and scale, enabling clients to move core payment operations to the cloud, enhance fraud management capabilities, and deliver seamless digital experiences to their customers through its Carat ecosystem.

Here is a list of key players operating in the global market:

The payment as a service market is characterized by intense competition and strategic consolidation, with major players aggressively pursuing growth through mergers, acquisitions, and technological innovation. The market landscape is dominated by established U.S.-based financial technology giants such as PayPal, Fiserv, and FIS, which maintain significant market share through comprehensive service portfolios and global reach. Key strategic initiatives include the integration of artificial intelligence for enhanced fraud detection and personalized payment experiences, with companies, including Corpay, leveraging AI to drive double-digit revenue growth in enterprise payments. Besides, in January 2024, Treasury Intelligence Solutions (TIS) and Treasury Strategies partnered with each other to ensure the worldwide bank fee analysis platform integration with the TIS cloud platform for payments, liquidity, and cashflow, thus positively impacting the payment as a service industry globally.

Corporate Landscape of the Payment as a Service (PaaS) Market:

Recent Developments

- In June 2025, Samsung Electronics declared that Samsung Wallet is projected to support digitalized notable compatibility, particularly for Mercedes-Benz vehicles. Additionally, with this latest integration, Galaxy consumers are able to experience a seamless and suitable way for locking, unlocking, and starting their Mercedes-Benz vehicle from their smartphone.

- In March 2025, AI Ansari Digital Pay successfully secured finalized acceptances from the Central Bank of the UAE for both the retail payment services and card schemes (RPSCS) as well as stored value facility (SVF) licenses, marking a suitable step toward the official unveiling of its state-of-the-art digital wallet.

- In August 2024, Mastercard introduced the latest Payment Passkey Service to ensure online shopping is easier and more secure. This launch first debuted in India as a pilot with a few of the country’s largest payment players, such as PayU, Razorpay, and Juspay, along with online merchants such as BigBasket and notable banks, including Axis Bank.

- Report ID: 8451

- Published Date: Mar 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.