Paper Coating Materials Market Outlook:

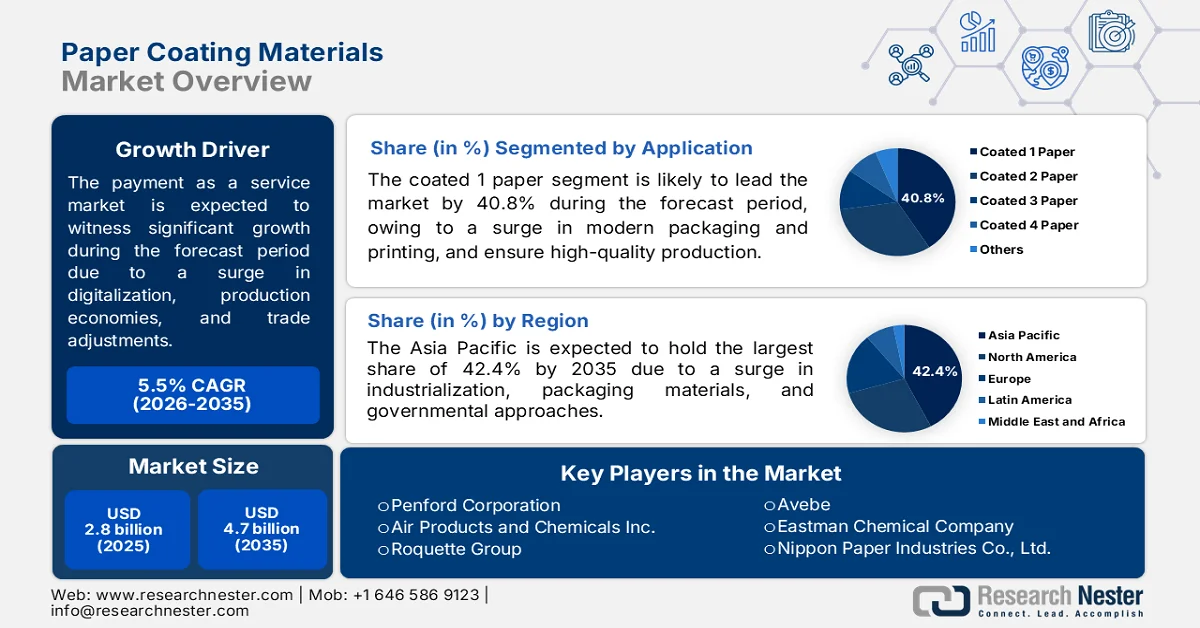

Paper Coating Materials Market size was valued at USD 2.8 billion in 2025 and is projected to exceed USD 4.7 billion by the end of 2035, expanding at over 5.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of paper coating materials is estimated at USD 2.9 billion.

The global paper coating materials market is shaped by different structural factors, such as raw material availability, trade policy adjustments, fluctuating energy prices affecting production economies, the transition towards digitalization in procurement, and demographic trends. According to official statistics published by NLM in November 2023, the worldwide pulping and papermaking industry accomplished an overall output of 417 million tons of paper and cardboard, with China and the U.S. accounting for an estimated 85.8 million tons and 78.2 million tons, respectively. In addition, China, as the major pulp-producing nation, readily consumed 112.9 million tons of pulp, of which 29.6 million tons are imported, and approximately 8.5 million tons are exported. Therefore, based on this, there is a continuous supply of recovered paper pulp to the country as well as other nations, which is positively impacting the market growth.

2024, Recovered Paper Pulp Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Thailand |

647 million |

- |

|

Malaysia |

363 million |

- |

|

China |

201 million |

1.1 billion |

|

Germany |

- |

95.9 million |

|

Saudi Arabia |

- |

95.1 million |

|

Global Trade Valuation |

2.2 billion |

|

|

Global Trade Share |

0.009% |

|

Source: OEC

Furthermore, the tactical industry collaboration for recycling infrastructure development, the adoption of functional and smart coating capabilities, and regionalization of supply chains and nearshoring approaches are a few trends that are responsible for driving the market globally. As stated in an article published by Progress in Organic Coatings in January 2026, the self-healing coatings industry is predicted to reach roughly USD 10 billion by the end of 2028, which is attributed to increased applications across aerospace, construction, and automotive industries. Besides, as per an article published by the America Coatings Association in 2026, the valuation of the global smart coatings industry reached USD 1 billion by the end of 2025, owing to its pre-defined characteristics and display properties, thus positively fueling the market enhancement.

Key Paper Coating Materials Market Insights Summary:

Regional Highlights:

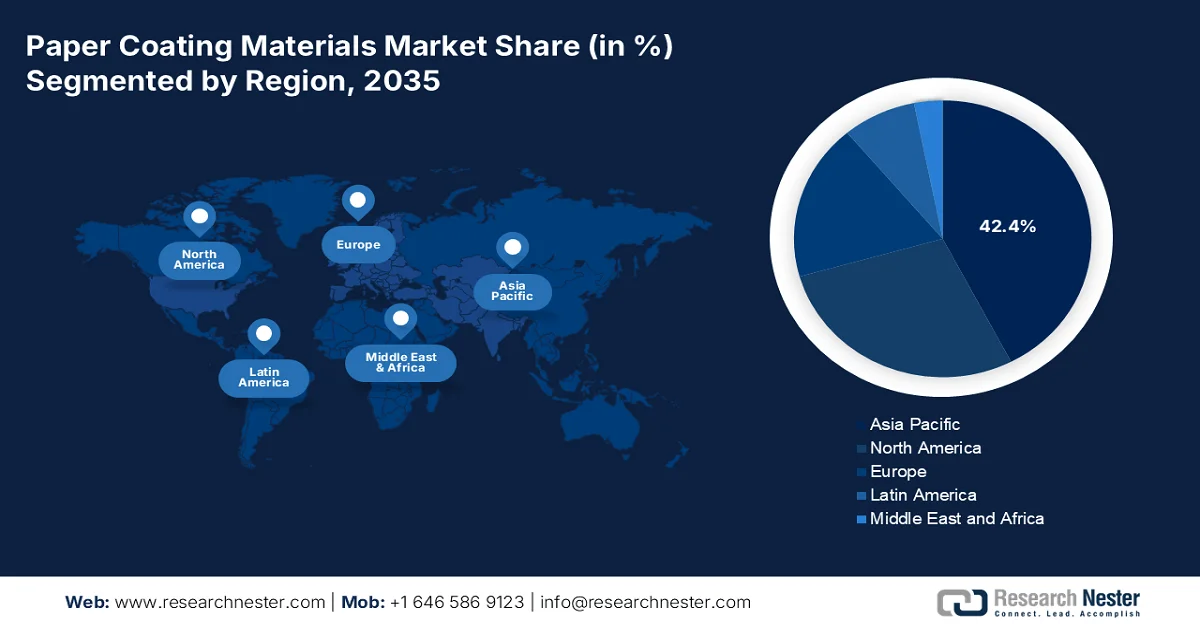

- Asia Pacific paper coating materials market is anticipated to capture a dominant 42.4% share by 2035, fueled by rapid industrialization, expanding e-commerce packaging demand, and the transition toward sustainable paper packaging solutions

- Europe is projected to witness the fastest growth in the market throughout 2026–2035, stimulated by stringent sustainability regulations, rising adoption of PFAS-free barrier coatings, and increasing replacement of single-use plastics with coated paperboard

Segment Insights:

- The coated 1 paper segment is forecast to hold a leading 40.8% share of the paper coating materials market by 2035, supported by its dual-surface functionality and enhanced tensile strength, antimicrobial activity, and biodegradability for advanced packaging and printing applications

- The packaging sub-segment is expected to secure the second-largest share in the market during 2026–2035, accelerated by the growing preference for renewable, recyclable, and biodegradable packaging alternatives to reduce environmental impact

Key Growth Trends:

- Regulatory mandates on plastic reduction

- Expansion in e-commerce for packaging

Major Challenges:

- Technical trade-offs in PFAS-free barrier coatings

- Recycling infrastructure mismatch for multi-layer coated paper

Key Players: BASF SE (Germany), Dow Inc. (U.S.), Omya AG (Switzerland), Imerys S.A. (France), Michelman, Inc. (U.S.), Stora Enso Oyj (Finland), Penford Corporation (U.S.), Air Products and Chemicals Inc. (U.S.), Roquette Group (France), Avebe (Netherlands), Eastman Chemical Company (U.S.), Nippon Paper Industries Co., Ltd. (Japan), Asia Pulp & Paper Co. Limited (Indonesia), Burgo Group SpA (Italy), Mitsubishi Chemical Corporation (Japan), Arkema S.A. (France), Sonoco Products Company (U.S.), Cortec Corporation (U.S.), Sierra Coating Technologies LLC (U.S.), Kuraray Co., Ltd. (Japan), Starbucks EMEA (UK).

Global Paper Coating Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.8 billion

- 2026 Market Size: USD 2.9 billion

- Projected Market Size: USD 4.7 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.4% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Vietnam, Indonesia, Brazil, Thailand, Mexico

Last updated on : 13 May, 2026

Paper Coating Materials Market - Growth Drivers and Challenges

Growth Drivers

- Regulatory mandates on plastic reduction: Government regulations are significantly functional as the ultimate and single-most powerful accelerator of the paper coating materials market adoption. Besides, as stated in an article published by the UNEP Organization in July 2025, almost 2,000 garbage trucks with plastic are dumped into lakes, rivers, and oceans regularly. Additionally, regarding plastic pollution, 19 to 23 million tons of plastic waste leak into aquatic ecosystems, eventually polluting marine life. Therefore, the worldwide regulatory landscape is rapidly shifting away from conventional plastic packaging while simultaneously restricting legacy coating chemistries, creating mandatory replacement demand for compliant paper-based solutions, and thereby driving market growth.

- Expansion in e-commerce for packaging: The structural growth of online retail is readily altering the market requirement patterns that are distinct from the general packaging volume surge. Based on government estimates published by the Census Government in March 2026, the retail e-commerce sales during the fourth quarter of 2025 in the U.S. were worth USD 316.1 billion, demonstrating 1.7% increase from the third quarter. Besides, the overall sales for the fourth quarter were USD 1,900.5 billion, indicating an upsurge of 0.4%. Therefore, this continuous increase in sales has created an outstanding performance, with coated surfaces withstanding expanded logistic chains, maintain print integrity, and resist abrasion during automated sorting, thus denoting an optimistic outlook for the market expansion.

Global B2B E-Commerce Growth Analysis, 2017-2026

|

Year |

Growth (USD Billion) |

|

2017 |

9,837 |

|

2018 |

11,332 |

|

2019 |

13,299 |

|

2020 |

14,874 |

|

2021 |

17,880 |

|

2022 |

21,019 |

|

2023 |

24,453 |

|

2024 |

28,082 |

|

2025 |

32,118 |

|

2026 |

36,163 |

Source: ITA

- Demand for biodegradability and composting certification: Beyond general recyclability claims, a distinct growth driver for the market has emerged around certified compostability and biodegradability. This driver operates in parallel with, but separately from, recycling initiatives, serving applications where recycling infrastructure is unavailable or where food contamination makes recycling impractical. Moreover, brand owners seeking home-compostable claims for food service packaging are driving demand for coating materials that degrade completely under defined conditions without leaving toxic residues. Unlike recyclability, which requires collection infrastructure, composting certifications, such as DIN CERTCO certification, provide independent validation that coated paper products can biodegrade in real-world conditions.

Challenges

- Technical trade-offs in PFAS-free barrier coatings: As regulators aggressively phase out per- and polyfluoroalkyl substances from food-contact paper, the industry faces a non-negotiable reformulation crisis. Besides, conventional PFAS-based coatings provided unmatched grease, oil, and water resistance with minimal coat weight. Their removal forces chemists to replace one molecule with multiple functional layers, often using waxes, starches, or biopolymers. However, these alternatives introduce severe trade-offs. Higher coat weights increase material consumption and drying energy, slowing production line speeds. Moreover, many bio-based barriers lack heat stability, causing blistering during microwave or oven use, thus negatively impacting the market growth.

- Recycling infrastructure mismatch for multi-layer coated paper: The aspect of sustainability claims drives demand for the market, but the actual recyclability of modern coated substrates lags far behind marketing promises. High-barrier paperboards often combine multiple functional layers, pigments, binders, waxes, and bio-polymers, applied sequentially to mimic plastic performance. While each layer may be theoretically biodegradable, municipal recycling facilities lack the washing and screening technology to separate these composite structures. In practice, heavily coated paper is downgraded from high-value fiber streams to low-grade mixed waste or rejected entirely to landfills or incinerators. Meanwhile, paper mills that accept recycled feedstock refuse bales containing exotic coatings because they clog screens, contaminate pulp, and increase chemical treatment costs.

Paper Coating Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 2.8 billion |

|

Forecast Year Market Size (2035) |

USD 4.7 billion |

|

Regional Scope |

|

Paper Coating Materials Market Segmentation:

Application Segment Analysis

Based on the application, the coated 1 paper segment is anticipated to account for the largest share of 40.8% in the paper coating materials market by the end of 2035. The segment’s upliftment is primarily attributed to its importance in modernized packaging and printing, owing to its ability to combine a printable and high-quality surface on one side with a receptive and natural surface on the other. According to official statistics published by NLM in July 2025, coated paper usually showcases improved tensile strength, robust antimicrobial activity, and outstanding rub resistance of 200 cycles. In addition, there is the reduction of fungi and Staphylococcus aureus by 99.92% and 99.9%, respectively. Moreover, biocompatibility has been confirmed by 100% Caco-2 cell viability, while biodegradability has reached 72.6% within 60 days, all of which positively caters to the segment’s growth.

End use Segment Analysis

The packaging sub-segment, which is part of the end use segment, is projected to garner the second-largest share in the paper coatings market during the forecast duration. The sub-segment’s growth is effectively driven by its necessity for sustainability, providing a renewable, recyclable, and biodegradable alternative to plastic that tends to diminish environmental impact. As stated in an article published by the Packaging Industry Association of India in 2026, the packaging industry in the country was valued at USD 50.5 billion and further reached USD 204.8 billion by the end of 2025, based on a 26.7% growth rate. Besides, packaging is the highest growing industry in the country and is continuously developing by 22% and 25% per year, and is readily emerging as the most preferred center for the industry. Therefore, this denotes a huge growth opportunity for the market in the nation as well as other regions.

Material Type Segment Analysis

During the forecast period, the ground calcium carbonate (GCC) segment, part of the material type, is projected to grab the third-largest share in the market. The segment’s development is highly propelled by the aspect of being cost-effective, eco-friendly, and a vital inorganic mineral filler, which is utilized across different industries to optimize product performance. Additionally, the segment serves as the foundational volume driver within the paper coating materials market, prized primarily for its exceptional brightness and cost efficiency. Moreover, derived directly from natural limestone via mechanical crushing and classification, GCC offers paper manufacturers a reliable mineral filler and coating pigment that enhances print gloss, opacity, and sheet smoothness without requiring complex chemical synthesis.

Our in-depth analysis of the paper coating materials market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

End use |

|

|

Material Type |

|

|

Substrate Type |

|

|

Coating Technology |

|

|

Functionality |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Paper Coating Materials Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the paper coating materials market is anticipated to grab the highest share of 42.4% by the end of 2035. The market’s upliftment in the region is primarily attributed to rapid industrialization, urbanization, the growing demand for packaging materials, particularly in the e-commerce industry, the transition towards sustainable and eco-friendly paper packaging, and governmental strategies. According to official statistics published by the IBEF Organization in March 2025, the paper packaging industry, particularly in India, grew at a 26.7% growth rate by the end of 2025, with the ultimate objective to reduce plastic utilization. Besides, there has been an increase in newsprint and paperboard by nearly 3-times from 532, 700 tons to 1,560,200 tons between 2023 and 2024. Therefore, with this continuous surge in the paper demand, the market is gradually uplifting in the overall region.

2024 Paper and Paperboard Export/Import Analysis in Asia

|

Countries |

Export (USD) |

Import (USD) |

|

China |

1.9 billion |

- |

|

Vietnam |

107.0 million |

20.7 million |

|

Malaysia |

64.1 million |

28.9 million |

|

India |

63.4 million |

6.8 million |

|

South Korea |

46.3 million |

29.8 million |

|

Indonesia |

41.4 million |

7.4 million |

|

Japan |

- |

149.0 million |

|

Thailand |

30.4 million |

17.8 million |

Source: OEC

The paper coating materials market in China is growing significantly, owing to the largest producer and consumer of coated printing and writing papers, the government’s strong promotion of paper packaging in place of plastics, the existence of global manufacturers, the sustained industrial demand, and technological advancements. As stated in an article published by Resources, Conservation and Recycling in November 2023, the demand for paper in the country is predicted to increase to 186 million tons in the upcoming 30 years, effectively leading to a significant surge in both the need for fibers, accounting for 173 million tons, as well as waste paper generation of 138 million tons. Moreover, the country has readily emerged as the largest paper producer globally, catering to 30% of the worldwide production due to social development and rapid economic upliftment, thus proliferating the market growth.

The aspects of an upsurge in paperboard production, coating materials, an increase in the demand for packaging materials and food-based applications, the requirement for coated paper with barrier properties, along with the value chain dynamics are a few factors that are driving the paper coating materials market in Japan. Besides, the domestic market was valued at USD 246.3 million as of 2025, which is further projected to increase to USD 261.5 million by the end of 2026, followed by USD 358.4 million by 2035, based on a 4.4% growth rate. Moreover, as stated in an article published by the Japan Paper Association in 2024, the paper and paperboard production in the country was 21,604,000 tons as of 2024, which has positioned it as the third-largest producer after China and the U.S. This particular growth is possible with the continuous demand for paper-based products in previous years, thus positively driving the market growth.

Paperboard Production Analysis in Japan, 2005-2024

|

Segments (1,000 metric tons) |

2005 |

2010 |

2015 |

2019 |

2020 |

2021 |

2022 |

2023 |

2024 |

|

Newsprint |

3,720 |

3,349 |

2,985 |

2,422 |

2,061 |

1,978 |

1,854 |

1,666 |

1,524 |

|

Printing & Communication |

11,503 |

9,547 |

8.384 |

7,512 |

5,877 |

6,314 |

5,997 |

5,552 |

5,275 |

|

Packaging & Wrapping |

975 |

904 |

891 |

899 |

759 |

831 |

842 |

764 |

754 |

|

Sanitary Tissue |

1,764 |

1,792 |

1,766 |

1,831 |

1,836 |

1,797 |

1,872 |

1,823 |

1,869 |

|

Other Paper |

939 |

794 |

804 |

838 |

685 |

760 |

708 |

624 |

662 |

|

Total Paper |

18,901 |

16,387 |

14,830 |

13,502 |

11,218 |

11,681 |

11,273 |

10,430 |

10,084 |

|

Containerboard |

9,311 |

8,647 |

9,187 |

9,658 |

9,702 |

10,131 |

10,201 |

9,511 |

9,468 |

|

Other Paperboard |

850 |

656 |

642 |

642 |

578 |

625 |

624 |

567 |

568 |

|

Total Paperboard |

12,051 |

10,977 |

11,398 |

11,899 |

11,658 |

12,258 |

12,388 |

11,569 |

11,520 |

|

Total Paper and Paperboard |

30,952 |

27,363 |

26,228 |

25,401 |

22,876 |

23,939 |

23,661 |

21,999 |

21,604 |

Source: Japan Paper Association

Europe Market Insights

Europe in the paper coating materials market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by regulatory frameworks, stringent sustainability targets, along with resilience and digitalization, an escalation in the substitution of single-use plastics with coated paperboard, and an increase in the need for PFAS-free barrier coatings. According to official statistics published by the Europe Commission in April 2024, there has been an increase in employment for manufacturing paper and paper-based products by 10.9%, indicating 62,500 people in the industry. Besides, as of 2022, 637,000 people were operational in this particular industry, of which 622,700 were employees, demonstrating an 11.3% increase. Moreover, the manufacturing sector for paper and paper-based products in the region readily makes up 19.9% of the overall industry, thus bolstering the market development.

The paper coating materials market in Germany is gaining increased traction, owing to the presence of massive consumers of coated printing and writing paper, the increased production capacity, substantial domestic consumption, government support through BMWK programs for ensuring industrial decarbonization, and an advanced recycling facility. As stated in an article published by the ITA in December 2025, the book industry in the country surpassed its sales by USD 11.3 billion as of 2024, indicating a minute increase from 2023. In addition, the industry generated an overall revenue of USD 7.7 billion from print book sales, as well as another revenue worth USD 260 million from e-book sales and USD 350 million from audiobook sales. Therefore, with this continuous increase in different segments of the industry, the market is eventually gaining increased exposure.

The presence of a strategic logistics and distribution facility for packaging materials, significant investments from international packaging converters, alignment with regional regulatory policies, concentrated chocolate and food processing sectors, and the combination of logistic benefits and industrial specialization are certain factors responsible for driving the market in Belgium. As per a data report published by Beyond Chocolate in 2025, the country is considered the largest manufacturing nation of chocolate products, producing 700,000 tons, of which 649,131 are exported to other countries. Meanwhile, Beyond Chocolate partners focused on certified sustainability for producing cocoa and making it suitable for producers to earn a suitable income. Therefore, with the increased production and regulatory engagements, there is a huge demand for the market in the country.

North America Market Insights

North America in the paper coating materials market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by a shift from legacy graphic paper applications to high-performance coated paperboard, an increase in packaging demand, regulatory tailwinds, and a surge in the need for compostable and repulpable coatings that are aligned with expanded producer responsibility. According to official statistics published by the EPA Government in October 2025, both packaging and containers readily make up the majority portion of municipal solid waste, significantly amounting to 82.2 million tons of generation, especially in the U.S. Besides, the recycling rate of generated containers and packaging was 53.9%, thereby creating a huge growth opportunity and demand for paper containers in the overall region.

2024 Paper Containers Export and Import Analysis in North America

|

Countries |

Export (USD) |

Import (USD) |

|

U.S. |

2.2 billion |

3.6 billion |

|

Canada |

994.0 million |

1.2 billion |

|

Mexico |

566 million |

1.3 billion |

|

Guatemala |

193.0 million |

70.7 million |

|

El Salvador |

111.0 million |

26.6 million |

|

Honduras |

67.3 million |

57.4 million |

|

Costa Rica |

63.6 million |

105.0 million |

|

Dominican Republic |

60.1 million |

79.5 million |

Source: OEC

The paper coating materials market in the U.S. is gaining increased exposure, owing to the regulatory phase-out of PFAS and single-use plastics, e-commerce growth and unboxing aesthetics, sustainable packaging mandates, brand commitments, digital printing technology, along with supply chain reconfiguration and tariff adjustments. As stated in an article published by the Printing and Imaging Association of Georgia in October 2022, the domestic printing industry effectively comprises 29,118 establishments, which have incorporated digital technologies that are proliferating the market growth. Based on this, there has been a growth in the number of domestic screen-printing establishments by 25%, which is 4,454 to 5,563. This particular growth demonstrated the digital print technology adoption, which is responsible for fueling the market in the country.

The increased demand for food packaging materials, an expansion in producer responsibility programs across all provinces, growth in the e-commerce sector, along with packaging aesthetics, innovation in bio-based and sustainable binders, and an increased focus on domestic production and import substitution are a few factors that are enhancing the paper coating materials market in Canada. As per an article published by the United Nations Organization in 2022, the country’s 2022 Budget proposed to offer USD 183.1 million for more than 5 years between 2022 and 2023. The purpose of this fund was to diminish plastic waste and enhance plastic circularity by creating and implementing regulatory measures and conducting scientific research to ensure policy-making, thereby denoting a huge growth opportunity and development in the overall country.

Key Paper Coating Materials Market Players:

- BASF SE (Germany)

- Dow Inc. (U.S.)

- Omya AG (Switzerland)

- Imerys S.A. (France)

- Michelman, Inc. (U.S.)

- Stora Enso Oyj (Finland)

- Penford Corporation (U.S.)

- Air Products and Chemicals Inc. (U.S.)

- Roquette Group (France)

- Avebe (Netherlands)

- Eastman Chemical Company (U.S.)

- Nippon Paper Industries Co., Ltd. (Japan)

- Asia Pulp & Paper Co. Limited (Indonesia)

- Burgo Group SpA (Italy)

- Mitsubishi Chemical Corporation (Japan)

- Arkema S.A. (France)

- Sonoco Products Company (U.S.)

- Cortec Corporation (U.S.)

- Sierra Coating Technologies LLC (U.S.)

- Kuraray Co., Ltd. (Japan)

- Starbucks EMEA (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- BASF SE is a dominant force in the paper coating chemicals market, supplying high-performance styrene-butadiene (SB) latex binders and dispersions that enhance printability and water resistance. The company is actively shifting its product portfolio toward bio-based and recyclable coating formulations to meet tightening global regulations on single-use plastics.

- Dow Inc. leverages its extensive acrylic and vinyl acetate ethylene (VAE) emulsion technologies to provide paper coating solutions that deliver superior gloss, barrier properties, and binding strength for lightweight packaging papers. The manufacturer is investing heavily in waterborne barrier coatings designed to replace conventional PFAS-based treatments in food-contact paperboard applications.

- Omya AG is a premier global supplier of GCC pigments, providing consistent, high-brightness mineral slurries that optimize coating coverage and sheet smoothness for premium printing and packaging grades. The company differentiates itself through vertically integrated mine-to-mill operations and customized particle size engineering tailored to individual paper machine requirements.

- Imerys S.A. is a leading producer of functional mineral additives, including kaolin, talc, and calcium carbonates, which serve as cost-effective fillers and coating pigments to improve opacity, ink reception, and surface uniformity. The company pursues continuous innovation in calcined clays and platy kaolins specifically engineered for high-barrier packaging papers and sustainable molded fiber products.

- Michelman, Inc. specializes in advanced water-based barrier and functional coatings designed for paper and paperboard applications, including grease, oil, moisture, and oxygen resistance layers. The company is recognized for its rapid development of PFAS-free and compostable coating systems that enable food service packaging to meet stringent global biodegradability and recyclability standards.

Here is a list of key players operating in the global market:

The paper coating materials market is characterized by a fragmented yet consolidating competitive landscape, dominated by multinational chemical giants and specialized mineral processors. Key players such as BASF, Dow, and Omya hold significant shares through integrated supply chains spanning raw material extraction to advanced formulation. Meanwhile, a major strategic shift is underway toward sustainable, PFAS-free, and bio-based barrier solutions in response to global plastic regulations. Leading manufacturers are aggressively pursuing mergers and acquisitions, notably Henkel's acquisition of Stahl, alongside capacity expansions for waterborne coatings. Besides, in May 2025, Starbucks EMEA partnered with Transcend Packaging, Qwarzo® and Metsä Board and introduced the latest home compostable hot cup and lid that are extremely recyclable, thus catering to the paper coating materials industry growth.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, BASF and UPM Specialty Materials (UPM) collaborated to assist brand owners, formulators, and converters in escalating the transition to recyclable and fiber-specific packaging solutions.

- In December 2025, Siegwerk introduced sustainable coating solutions under the rethINK packaging strategy that is focused on driving the transformation towards a circular economy by creating eco-friendly solutions that ensure suitable packaging circularity.

- In May 2025, Dow unveiled the BLUEWAVE™ technology facility in France for effectively supporting a comprehensive variety of paper packaging products that are to be designed for less resource-intensive and more recyclable through advanced barrier coating applications.

- Report ID: 8559

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Paper Coating Materials Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.