Osteoarthritis Therapeutics Market Outlook:

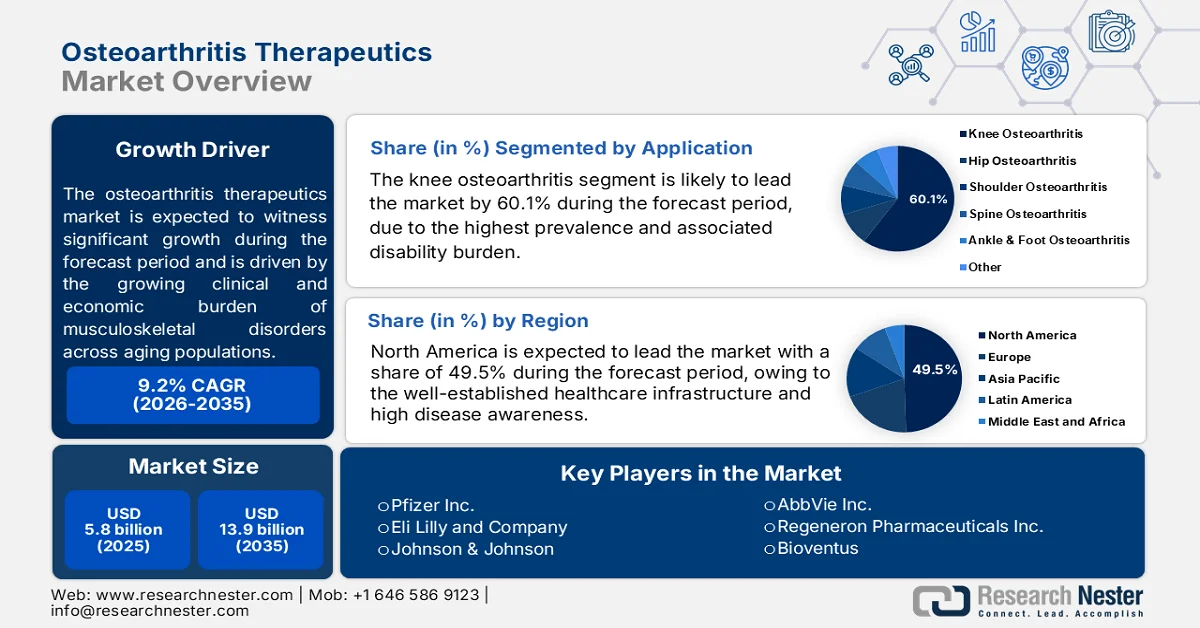

Osteoarthritis Therapeutics Market size was valued at USD 5.8 billion in 2025 and is projected to exceed USD 13.9 billion by the end of 2035, expanding at over 9.2% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of osteoarthritis therapeutics is estimated at USD 6.3 billion.

The osteoarthritis therapeutics market is shaped by the growing clinical and economic burden of musculoskeletal disorders across aging populations. According to the NLM November 2022 data, nearly 32.5 million adults in the U.S. are affected by osteoarthritis, making it one of the most significant drivers of long-term pain management and mobility-related healthcare utilization. Demand for pharmacological therapies, intra-articular treatments, and supportive disease-management interventions continues to rise as healthcare systems seek to reduce disability and maintain patient independence. The U.S. National Institutes of Health continues to fund studies focused on pain pathways, cartilage preservation, regenerative medicine, and biomarkers that could improve treatment outcomes.

Besides, the market expansion is supported by rising disease prevalence and increasing healthcare expenditure directed toward chronic musculoskeletal conditions. The World Health Organization reported in July 2023 that 528 million people worldwide were living with osteoarthritis, representing a substantial increase over previous decades. WHO further noted that about 73% of individuals affected are older than 55 years, highlighting the strong relationship between population aging and therapeutic demand. These demographic and healthcare trends are encouraging manufacturers to expand clinical development programs, explore disease-modifying treatment approaches, and strengthen evidence generation around long-term efficacy and safety. As healthcare providers increasingly focus on reducing disability-related costs and improving patient outcomes, osteoarthritis therapeutics are expected to remain a strategic area of investment across both established and emerging healthcare markets.

Key Osteoarthritis Therapeutics Market Insights Summary:

Regional Highlights:

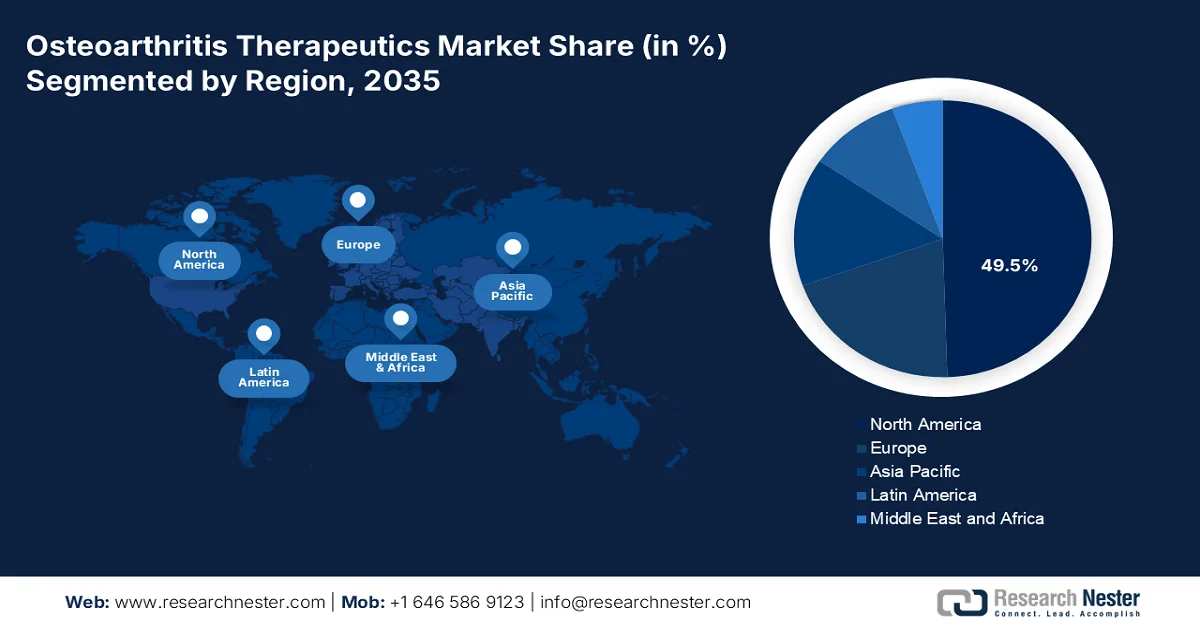

- North America osteoarthritis therapeutics market is anticipated to command 49.5% of the regional revenue share by 2035, underpinned by well-established healthcare infrastructure, high disease awareness, and rapid adoption of innovative biologics and disease-modifying drugs

- Europe is projected to witness robust growth in the market throughout 2026-2035, attributed to established healthcare systems and the increasing prevalence of osteoarthritis driven by the aging population

Segment Insights:

- Knee osteoarthritis is forecast to account for 60.1% of the osteoarthritis therapeutics market by 2035, reinforced by its high prevalence and growing disability burden amid aging populations and rising obesity rates

- Within the market, disease-modifying osteoarthritis drugs (DMOADs) are expected to lead the product type segment by 2035, fueled by their ability to address cartilage degradation, subchondral bone remodeling, and synovial inflammation

Key Growth Trends:

- Rising geriatric population

- Rising prevalence of osteoarthritis

Major Challenges:

- Limited disease-modifying treatment options

- High cost of advanced therapies

Key Players: Pfizer Inc. (U.S.),Eli Lilly and Company (U.S.),Johnson & Johnson (U.S.),AbbVie Inc. (U.S.),Regeneron Pharmaceuticals Inc. (U.S.),Bioventus (U.S.),Flexion Therapeutics (U.S.),Novartis AG (Switzerland),Roche Holding AG (Switzerland),Sanofi S.A. (France),GlaxoSmithKline plc (UK),Merck KGaA (Germany),Takeda Pharmaceutical Company Limited (Japan),Seikagaku Corporation (Japan),Chugai Pharmaceutical Co., Ltd. (Japan),CSL Limited (Australia),Sun Pharmaceutical Industries Ltd. (India),Sobi (Sweden),Cipla (India),Johnson & Johnson MedTech (U.S.).

Global Osteoarthritis Therapeutics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.8 billion

- 2026 Market Size: USD 6.3 billion

- Projected Market Size: USD 13.9 billion by 2035

- Growth Forecasts: 9.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (49.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, Germany, United Kingdom, Japan, France

- Emerging Countries: China, India, South Korea, Brazil, Italy

Last updated on : 11 June, 2026

Osteoarthritis Therapeutics Market - Growth Drivers and Challenges

Growth Drivers

- Rising geriatric population: As per the WHO October 2025 data, nearly 1.4 billion persons are aged 60 and above, which is a rise of 1.1 billion in 2023. In emerging nations, this trend is more swifter and noticeable. The increasing aging population is a primary driver for the osteoarthritis therapeutics market. Osteoarthritis mainly affects elderly people due to the natural wear and tear of joints over time. This demographic shift significantly increases demand for effective therapeutics to manage symptoms and enhance quality of life. Governments and healthcare systems are focusing more on age-related diseases, therefore driving the investments in osteoarthritis treatments.

- Rising prevalence of osteoarthritis: The CDC February 2024 data depict that the prevalence of diagnosed arthritis in women was arthritis 21.5% in, with the age-adjusted prevalence among individuals aged 18 and older being 18.9%. The increasing prevalence of osteoarthritis is driven by factors, including sedentary lifestyle habits, joint injuries, and obesity. Increased weight on joints, mainly on weight-bearing joints like knees and hips, leads to cartilage deterioration. Activity in sports also leads to an increased occurrence of injuries, both in the workplace and in sports, leading to an incidence of osteoarthritis.

Challenges

- Limited disease-modifying treatment options: Although research is ongoing, there aren't many real disease-modifying osteoarthritis medications (DMOAD). The majority of existing therapies are intended to alleviate symptoms rather than alter the progression of joint deterioration. As a result, both patients and doctors have limited long-term treatment efficacy; disease management frequently outperforms patient results in terms of finding a cure.

- High cost of advanced therapies: New treatment modalities, such biologics, regenerative medicine, and minimally invasive procedures, can be costly, making access difficult for patients from low- and middle-class backgrounds. There are still obstacles to cost for both individuals and the healthcare system, which can make it challenging to spread innovative treatments.

Osteoarthritis Therapeutics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.2% |

|

Base Year Market Size (2025) |

USD 5.8 billion |

|

Forecast Year Market Size (2035) |

USD 13.9 billion |

|

Regional Scope |

|

Osteoarthritis Therapeutics Market Segmentation:

Application Segment Analysis

Under the application segment, the knee osteoarthritis is projected to dominant in the osteoarthritis therapeutics market and is poised to hold the share value of 60.1% by the end of 2035. The segment is driven by its highest prevalence and associated disability burden. According to the NYU Langone Health August 2025 data, 1 in 7 people reported some of osteoarthritis, a figure that continued to rise due to aging populations and increasing obesity rates. This high disease burden accelerates demand for both symptom-modifying drugs and disease-modifying osteoarthritis drugs specifically targeting the knee joint. Knee OA’s larger patient pool compared to hip or hand OA ensures its leading revenue share throughout the forecast period.

Product Type Segment Analysis

Within the osteoarthritis therapeutics market, the product type segment is broadly categorized into symptom-modifying drugs and disease-modifying osteoarthritis drugs. By 2035, DMOADs are expected to emerge as the leading sub-segment, fundamentally transforming the treatment landscape. Unlike conventional therapies that only alleviate pain and inflammation, DMOADs target underlying pathological processes including cartilage degradation, subchondral bone remodeling, and synovial inflammation. This paradigm shift toward structure modification and disease reversal, rather than mere symptom suppression, drives their dominance. With an aging global population and increasing preference for curative approaches, DMOADs are poised to capture the largest revenue share among all product types in the forecast year.

End user Segment Analysis

Orthopedic clinics is dominating the end-user segment by 2035, driven by rising outpatient and rehabilitation visits for OA pain management. According to the JHEOR March 2022 study, patients with moderate-to-severe (MTS) OA pain, mean outpatient visits increased substantially from 22.8 (SD 22.4) at baseline to 32.9 (26.6) at 12 months and 60.7 (47.8) at 24 months. Rehabilitation and physical therapy visits alone rose from 1.5 (5.3) to 6.2 (12.8) over the same period (all P<0.0001). These increases reflect growing dependence on specialist-led, non-surgical interventions such as intra-articular injections and structured PT, services predominantly delivered at orthopedic clinics. Consequently, orthopedic clinics capture the largest revenue share among end users by 2035.

Our in-depth analysis of the osteoarthritis therapeutics includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

|

Drug Class |

|

|

Route of Administration |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Osteoarthritis Therapeutics Market - Regional Analysis

North America Market Insights

North America is dominating the osteoarthritis therapeutics market and is expected to hold the regional revenue share of 49.5% by the end of 2035. The region is driven by a well-established healthcare infrastructure, high disease awareness, and rapid adoption of innovative biologics and disease-modifying drugs. The region benefits from strong regulatory pathways that accelerate approvals of novel intra-articular injectables and DMOADs. Additionally, digital health integration, including telehealth consultations and virtual physical therapy programs, is reshaping care delivery. With a strong emphasis on value-based reimbursement models favoring non-surgical management, North America continues to lead global market growth throughout the forecast period.

The rising burden of arthritis-related conditions and healthcare spending is shaping the osteoarthritis therapeutics market in the U.S. According to the NLM October 2023 data, 53.2 million U.S. adults, or 21.2% of the adult population, were living with doctor-diagnosed arthritis in 2022, creating sustained demand for long-term pain management and musculoskeletal care services. In parallel, the CHCF January 2026 data reported that U.S. national health expenditures increased by 7.5% in 2023 to USD 4.9 trillion, reflecting greater healthcare utilization and investment across chronic disease treatment categories. These factors are supporting increased adoption of therapeutic interventions, clinical research activities, and treatment access across the United States.

The expanding non-pharmacological treatment options for chronic joint pain is driving the osteoarthritis therapeutics market in Canada. The Clinical Trials August 2024 data depict that investing green light therapy (GLT) in 44 patients with knee osteoarthritis, assessing whether daily exposure to green LED light over 20 weeks can reduce pain by altering brain pain-processing pathways. This research reflects increasing interest in alternatives to long-term NSAID and corticosteroid use. In parallel, the Canadian Institute for Health Information (CIHI) reported that total health spending is supporting investment in chronic disease management and musculoskeletal care. Together, these developments are strengthening Canada’s osteoarthritis treatment and innovation landscape.

Europe Market Insights

Europe is anticipated to experience a strong growth in the global osteoarthritis therapeutics market due to the established healthcare systems and the increasing prevalence of osteoarthritis due to the aging population. Countries such as the UK, Germany, and France currently have advanced diagnostic and therapeutic facilities that allow for early intervention and continued osteoarthritis treatment. Moreover, the government support and healthcare policies, along with reimbursement, enable the use of advanced therapies such as disease-modifying drugs and regenerative therapies to be more acceptable. Europe shows a strong medical device and pharmaceutical sector with substantial scientific R&D into osteoarthritis and public health awareness and promotion.

The rising economic burden of osteoarthritis and increasing healthcare utilization among aging populations is driving the osteoarthritis therapeutics market in Germany. According to NLM November 2025 data, osteoarthritis-related direct healthcare costs increased from €8.6 billion to €12.1 billion, representing a 41% increase over five years. The strongest growth was observed among adults aged over 85 years, where costs nearly doubled (+99%), reflecting increasing demand for long-term disease management and supportive care. Inpatient and semi-inpatient expenditures reached €6.6 billion in 2020, driven by higher nursing care requirements. These trends are encouraging continued investment in therapies that improve pain management and functional outcomes.

The rising burden of musculoskeletal (MSK) conditions and growing demand for chronic pain management is driving the osteoarthritis therapeutics market in the UK. According to the Government of UK March 2022 data, 30.1% of England’s population, equivalent to approximately 15.9 million people, were living with an MSK condition in 2017, highlighting a large potential patient pool for osteoarthritis-related therapies. In addition, around 20% of people in the UK consult a doctor each year for an MSK problem, reflecting significant healthcare utilization associated with joint and mobility disorders. With population aging and increasing prevalence of chronic musculoskeletal conditions, demand for effective osteoarthritis treatments and supportive care services continues to expand.

APAC Market Insights

Asia Pacific is expected to emerge rapidly in the global osteoarthritis therapeutics market during the forecast period. The region is driven by lifestyle changes, including urban living, sedentary habits, and rising obesity rates. Countries such as China, India, and Japan are seeing a notable increase in joint-associated issues as life expectancy rises, and healthcare becomes more accessible. Moreover, the development of healthcare infrastructure, government efforts to enhance musculoskeletal health, and higher disposable incomes are all fueling the uptake of the region’s advanced osteoarthritis treatments.

The rapidly aging population and increasing prevalence of chronic health conditions is driving the osteoarthritis therapeutics market in India. According to the NLM October 2025 study the Longitudinal Ageing Study in India (LASI), more than 75 million people in India aged 60 years and above were living with at least one chronic disease, while 27% of older adults experienced multimorbidity, increasing the need for comprehensive long-term healthcare management. The coexistence of conditions such as hypertension, obesity, diabetes, and cardiovascular disease can complicate osteoarthritis treatment and increase healthcare utilization. As the elderly population continues to grow, demand for effective pain management therapies, rehabilitation services, and integrated musculoskeletal care is expected to strengthen across India.

The substantial disease burden and increasing need for long-term musculoskeletal care is driving the osteoarthritis therapeutics market in China. According to the NLM January 2024 study, China recorded an age-standardized osteoarthritis incidence rate of 509.84 per 100,000 population, exceeding the Asian average of 463.34 per 100,000, indicating a comparatively higher disease burden. The study also reported an age-standardized osteoarthritis DALY rate of 224.78 per 100,000 population, highlighting the significant impact of the disease on health and productivity. These trends are driving demand for pain management therapies, rehabilitation services, and advanced treatment approaches across China’s healthcare system.

Key Osteoarthritis Therapeutics Market Players:

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Johnson & Johnson (U.S.)

- AbbVie Inc. (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Bioventus (U.S.)

- Flexion Therapeutics (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Sanofi S.A. (France)

- GlaxoSmithKline plc (UK)

- Merck KGaA (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Seikagaku Corporation (Japan)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- CSL Limited (Australia)

- Sun Pharmaceutical Industries Ltd. (India)

- Sobi (Sweden)

- Cipla (India)

- Johnson & Johnson MedTech (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Pfizer Inc. is leading in the osteoarthritis therapeutics market and maintains a strong legacy through its portfolio of analgesics and non-steroidal anti-inflammatory drugs, including celecoxib. However, the company’s current strategic initiative focuses on transitioning beyond symptomatic relief toward novel disease-modifying osteoarthritis drugs. In 2025, the company has made a total revenue of USD 62,579 million.

- Eli Lilly and Company has strategically positioned itself within the osteoarthritis therapeutics market by focusing on non-opioid pain management solutions, particularly tanezumab (a nerve growth factor inhibitor), although regulatory challenges prompted strategic pivots. Currently, Eli Lilly emphasizes the development of novel biologics and monoclonal antibodies targeting neurogenic inflammation associated with osteoarthritis pain.

- Johnson & Johnson, through its subsidiary DePuy Synthes, has a dual focus in the osteoarthritis therapeutics market: advanced surgical interventions and non-surgical biologic therapies. Recognizing the shift toward early disease management, the company strategically expanded into intra-articular injectables, including corticosteroids and hyaluronic acid formulations. In 2024 the company has witnessed the operational sales growth of 7%.

- AbbVie Inc. has established a prominent footprint in the osteoarthritis therapeutics market primarily through its blockbuster immunology asset, Humira (adalimumab), which is also prescribed off-label for inflammatory osteoarthritis phenotypes. Recognizing patent expirations, AbbVie’s strategic initiative shifted toward next-generation biologics and small molecule DMOADs.

- Regeneron Pharmaceuticals Inc. has entered the osteoarthritis therapeutics market with a focus on monoclonal antibodies and genetically targeted therapies. The company’s flagship initiative involves fasinumab, a nerve growth factor (NGF) inhibitor designed to provide potent, long-lasting pain relief for moderate-to-severe knee and hip osteoarthritis.

Here is a list of key players operating in the global osteoarthritis therapeutics market:

The global osteoarthritis therapeutics market is moderately consolidated, with leading pharmaceutical and biotechnology firms aggressively pursuing disease-modifying osteoarthritis drugs (DMOADs) and next-generation intra-articular injectables. Key players are adopting strategic initiatives including mergers and acquisitions, licensing agreements, and extensive late-stage clinical trials for biologic candidates. For example, in December 2025, Sobi® announced the acquisition of Arthrosi Therapeutics, Inc. Companies are also expanding into emerging Asia markets through local partnerships and manufacturing agreements. Several Europe and U.S. firms dominate the DMOAD pipeline, while Japanese and South Korea entities lead in hyaluronic acid and cell-based therapies.

Corporate Landscape of the Market:

Recent Developments

- In December 2025, Cipla Limited announced the launch of Ciplostem, an innovative allogeneic mesenchymal stromal cell therapy for Knee Osteoarthritis (Knee OA), approved by the Drug Controller General of India (DCGI).

- In July 2025, Johnson & Johnson MedTech announced a strategic co-promotion agreement with Pacira BioSciences, Inc. The agreement expands the Company’s Early Intervention portfolio with ZILRETTA® which is an extended-release injectable for treatment of pain related to osteoarthritis (OA) of the knee.

- In September 2024, Sun Pharma and Moebius Medical were granted fast-track designation by the USFDA for their non-opioid treatment MM-II, which is intended to alleviate knee pain caused by osteoarthritis. This designation permits a quicker review process and possibly a quicker approval process. The businesses want to apply for a CE Mark in the EU and start Phase 3 clinical studies.

- Report ID: 195

- Published Date: Jun 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.