Optical Transport Network Market Outlook:

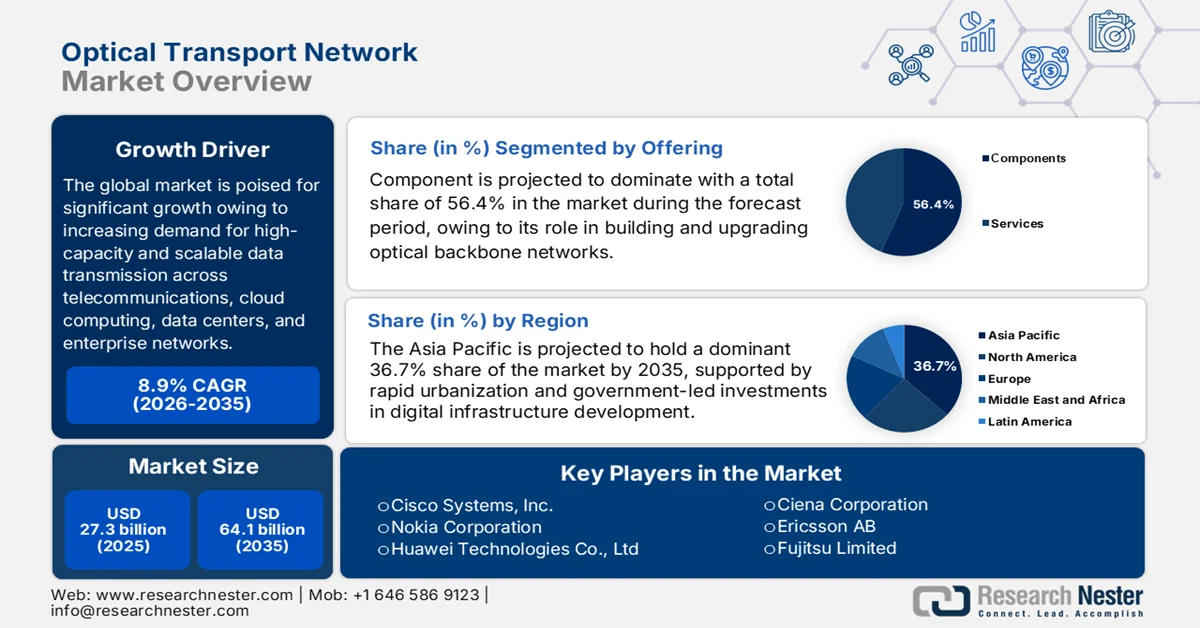

Optical Transport Network Market size was valued at USD 27.3 billion in 2025 and is poised to reach USD 64.1 billion by the end of 2035, expanding at around 8.9% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of optical transport network is evaluated at USD 29.8 billion.

The optical transport network market is poised for solid growth in the upcoming years, owing to increasing demand for high-capacity and scalable data transmission across telecommunications, cloud computing, data centers, and enterprise networks. The expansion of 5G infrastructure, rising internet traffic, and increasing investments in network modernization are deliberately supporting the deployment of advanced OTN solutions. In 2024, the article published by the International Telecommunication Union revealed that global Internet traffic continues to surge, wherein mobile broadband surpassed almost 1 zettabyte in 2023, whereas fixed broadband climbed to 6 ZB. Mobile broadband traffic has grown faster than fixed, averaging 19.6% annually since 2021, when compared to 15.2% for fixed. The report also mentioned that high‑income countries generate far more traffic per subscription than low‑income nations, thus elevating the growth potential of optical transport networks.

Furthermore, technological advancements in wavelength division multiplexing, network automation, and software-defined networking are enhancing the efficiency and flexibility of optical transport systems. In addition, organizations across different nations prioritize network performance and bandwidth optimization, due to which the market is anticipated to maintain a positive growth trajectory across both developed and emerging regions. In June 2024, TDC NET announced the upgradation of its metro and long-haul optical transport network with Ciena’s WaveLogic 5 technology, which enables 800G connectivity to deliver advanced services sustainably and securely. The upgrade leverages Ciena’s 6500 Packet Optical platforms, coherent pluggables, and Navigator Network Control Suite, and it reduces power consumption and provides scalable capacity for future digital service demands.

Key Optical Transport Network Market Insights Summary:

Regional Highlights:

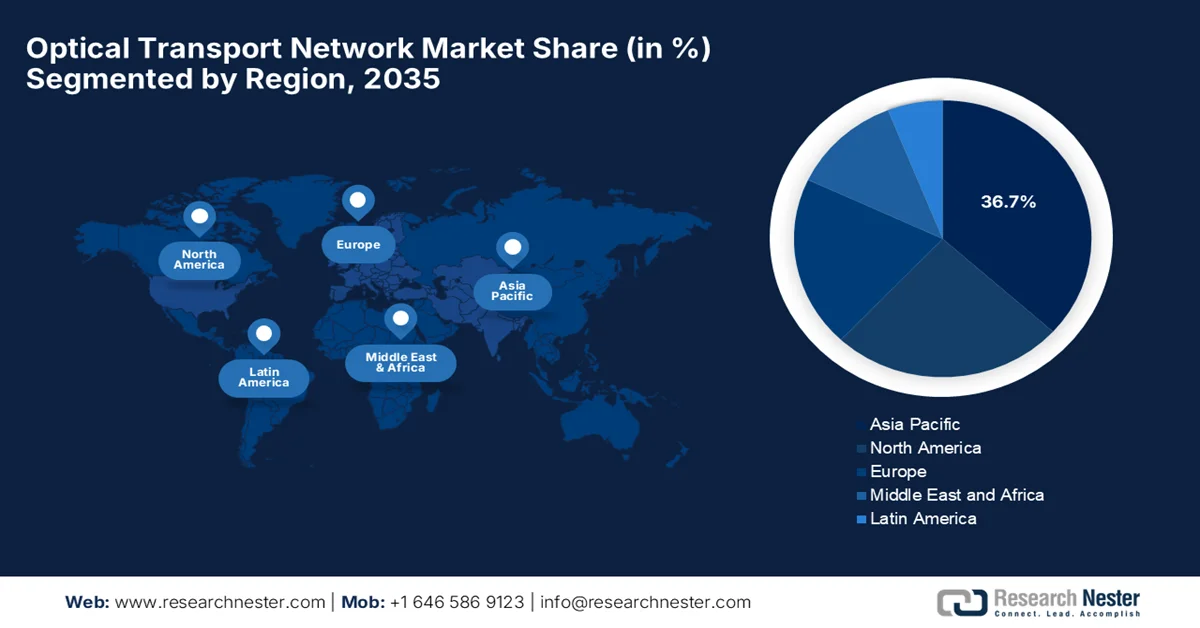

- The Asia Pacific region is projected to command a 36.7% share of the optical transport network market by 2035, bolstered by rapid urbanization, extensive government-backed digital infrastructure initiatives, and widespread 5G commercialization across major economies

- North America is poised to witness considerable growth during 2026-2035, fueled by the rapid expansion of artificial intelligence clusters and the continuous evolution of hyperscale data centers

Segment Insights:

- The component segment in the optical transport network market is expected to capture a 56.4% share by 2035, reinforced by the substantial capital investment required for optical transport hardware and underpinned by the critical role of hardware infrastructure in building and upgrading optical backbone networks

- Wavelengths at 100–400 Gbit/s are anticipated to secure a noteworthy market share during 2026-2035, stimulated by rising demand for high-capacity data center interconnects and the increasing need for AI-driven workloads requiring scalable, energy-efficient connectivity solutions

Key Growth Trends:

- AI and hyperscale data center expansion

- Evolution of ultra-high-speed coherent optics

Major Challenges:

- High capital expenditure and infrastructure upgrade costs

- Network complexity and interoperability issues

Key Players:Cisco Systems, Inc., Nokia Corporation, Huawei Technologies Co., Ltd., Ciena Corporation, Ericsson AB, Fujitsu Limited, NEC Corporation, ZTE Corporation, ADTRAN Holdings, Inc., Ribbon Communications Inc., Juniper Networks, Inc., t3 Broadband, LLC, Aureon, Inc., Nippon Telegraph and Telephone Corporation (NTT), NTT Innovative Devices Corporation (NII), NTT East Corporation.

Global Optical Transport Network Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 27.3 billion

- 2026 Market Size: USD 29.8 billion

- Projected Market Size: USD 64.1 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (36.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Singapore, Canada, United Kingdom, Australia

Last updated on : 29 June, 2026

Optical Transport Network Market - Growth Drivers and Challenges

Growth Drivers

- AI and hyperscale data center expansion: The global progression of AI and ML workloads across different nations necessitates unprecedented data processing speeds. Therefore, hyperscale data centers are deploying advanced OTN solutions to create high-capacity data center interconnects that handle massive data transfers between clusters efficiently. In February 2023, Nokia entered into a partnership with Liquid Intelligent Technologies to build a multi-terabit Africa optical backbone by connecting subsea landing stations in Kenya, South Africa, and the DRC to create a digital highway. The network possesses a design capacity of up to 12 Tb/s across seven countries, and it will deliver affordable, massive capacity to enterprises, hyperscalers, and mobile operators, thus suitable for bolstering the optical transport network market.

- Evolution of ultra-high-speed coherent optics: The commercialization of next-generation 800G and 1.6T coherent optical pluggables is fueling market growth. These advanced modules allow telecommunications providers to drastically increase their existing fiber capacity and spectral efficiency, thereby delaying expensive new fiber laydowns and meeting soaring enterprise data demands. In February 2023, Ciena introduced WaveLogic 6, which is the industry’s first 1.6Tb/s coherent optic solution, setting a new benchmark in optical transport. The technology possesses WaveLogic 6 extreme and nano, and it delivers unprecedented capacity, efficiency, and sustainability. Therefore, it supports 1.6Tb/s single-carrier wavelengths, 800Gb/s across long-haul links, and energy-efficient pluggables for metro and regional deployments.

Challenges

- High capital expenditure and infrastructure upgrade costs: This factor hampers the growth of the market since it needs huge capital for deployment and modernization. Also, building high-capacity optical transport infrastructure needs considerable expenditures on fiber-optic cables, optical switches, transponders, amplifiers, network management systems, and other associated installation activities. Most of the telecommunication operators, especially in developing regions, face budget constraints that limit their potential to upgrade aging transport networks to advanced OTN architectures. In addition, the migration from older SONET/SDH and packet-based systems to optical transport solutions necessitates extensive planning, network redesign, and workforce training, thus negatively impacting adoption rates in the market.

- Network complexity and interoperability issues: Modern transport networks need to support a combination of services such as 5G backhaul, cloud connectivity, enterprise applications, and data center interconnection. This can be challenging for pioneers in the market. Therefore, integrating equipment from multiple vendors creates interoperability challenges due to differences in hardware architectures, software platforms, and proprietary technologies. In this context, network operators need to ensure compatibility between optical transport equipment, packet networking systems, and management software by maintaining high levels of performance and reliability. In addition, the adoption of disaggregated networking architectures and open optical systems introduces new operational complexities.

Optical Transport Network Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 27.3 billion |

|

Forecast Year Market Size (2035) |

USD 64.1 billion |

|

Regional Scope |

|

Optical Transport Network Market Segmentation:

Offering Segment Analysis

Component in the offering segment is projected to maintain a dominating position with a total share of 56.4% in the optical transport network market during the forecast period. The critical role of hardware infrastructure in building and upgrading optical backbone networks is driving this leadership. In addition, components benefit from the high capital intensity of optical transport hardware, which forms the essential physical layer of all OTN deployments. In September 2024, Coherent announced at ECOC 2024 the demonstration of its 1.6T‑DR8 and 800G‑DR4 transceivers, thereby showcasing advanced multi‑technology solutions for next‑generation data centers. These modules leverage silicon photonics and differential EML innovations, and they deliver high‑capacity, energy‑efficient connectivity over 500 meters, thus denoting a wider segment scope.

Global Optical Fiber Cable Shipment Trends: Top Importing Countries in 2024

|

Importing Economy |

Trade Value (USD Thousand) |

Quantity (Kg) |

|

U.S. |

2,536,908.16 |

- |

|

Europe |

877,206.01 |

40,266,200 |

|

Mexico |

462,386.12 |

38,719,400 |

|

UK |

447,989.87 |

21,535,000 |

|

Germany |

384,229.94 |

16,587,100 |

|

France |

327,780.54 |

24,774,800 |

|

Netherlands |

279,320.73 |

6,586,760 |

|

Canada |

277,581.85 |

- |

|

Hong Kong, China |

231,959.79 |

- |

|

China |

182,097.08 |

3,473,240 |

|

Brazil |

170,360.77 |

50,893,100 |

|

Australia |

161,653.42 |

- |

Source: WITS

Data Rate Segment Analysis

Wavelengths at 100-400 Gbit/s are anticipated to hold a noteworthy share in the market during the discussed timeframe. The segment’s growth is majorly propelled by rising demand for high-capacity data center interconnects and the increasing need for AI-driven workloads that require scalable, energy-efficient connectivity solutions. In September 2024, Lightpath, in collaboration with Ciena, announced the deployment of the industry’s first 400G protected optical circuit, which is powered by WaveLogic 5 Nano coherent optics, achieving 80% lower power consumption. It is designed for a hyperscale customer, and the solution spans 200 miles with diverse routes and stringent failover times under 50ms, ensuring mission‑critical reliability, thus denoting a lucrative opportunity for the segment to grow.

Technology Segment Analysis

On the basis of technology, DWDM is expected to lead with a significant share in the market over the forecasted years. The segment’s growth is largely driven by the continuous scaling of backbone capacity to support hyperscale data centers. In addition, the rising demand for efficient network utilization and the growing need to support latency-sensitive applications such as AI and video streaming are accelerating DWDM adoption across metro, long-haul, and submarine networks. In May 2023, MOX Networks entered into a partnership with Ciena to deploy WaveLogic 5 Extreme coherent optics across its next‑generation dark fiber routes, enabling up to 400G wavelength services. The upgrade leverages Ciena’s 6500 flexible grid ROADM optical layer to deliver multi‑terabit capacity, supporting both 100G and 400G connectivity across key U.S. routes, including Hillsboro‑Portland‑Seattle and Columbus‑Ashburn‑Atlanta.

Our in-depth analysis of the optical transport network includes the following segments:

|

Segment |

Subsegments |

|

Offering |

|

|

Data Rate |

|

|

Technology |

|

|

Application |

|

|

End use Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Optical Transport Network Market - Regional Analysis

APAC Market Insights

The Asia Pacific optical transport network market is forecasted to lead with a dominating share of 36.7% during the forecast period. The region benefits from rapid urbanization, massive government-backed digital infrastructure initiatives, and widespread 5G commercialization across major economies. The regional market also benefits from the construction of hyperscale data centers and extensive submarine cable networks, which are designed to bridge international data hubs. For instance, in May 2024, Fujitsu introduced the 1FINITY T250 optical transmission solution, which is designed to advance the IOWN initiative by enabling highly reliable, low‑latency All‑Photonics Networks. It is equipped with latency adjustment and hitless path switching, and it enhances resilience against failures and disasters while supporting new services in telemedicine, remote robotics, and infrastructure monitoring.

The state-directed digital transformation initiatives and nationwide 5G-advanced rollouts are responsibly uplifting China optical transport network market. The country’s market benefits from a highly integrated domestic ecosystem, in which major homegrown telecommunications giants and equipment manufacturers work in unison to deploy next-generation ultra-high-speed coherent networks. Based on the government data published in January 2025, China’s Ministry of Industry and Information Technology announced its plans to launch 10‑gigabit optical network pilot projects in select cities and regions. It also mentions that these pilots will focus on key venues such as residential communities, factories, and industrial parks, driving the evolution of next‑generation networks toward ultra‑high speed, large capacity, and intelligence. Furthermore, the initiative aimed to build a mature industrial chain and ecosystem for 10G optical networks, thus supporting huge applications and new industrialization.

The domestic digital economy is driving extensive growth in the optical transport network market in India. The market is being propelled by a strong surge in data consumption from mobile streaming, digital payments, and e-commerce, along with a significant influx of global investment into hyper-scale data centers. In this context, Press Information Bureau (PIB) in December 2025, the Department of Telecommunications achieved major scale expansion wherein 5 G was deployed in 99.9% of districts covering about 85% of the population, and more than 5.08 lakh 5G BTS were installed nationwide. The report also mentioned that internet connections crossed 1 billion, broadband connections reached about 995.6 million, and the length of the optical fiber network expanded to around 4.2 million route km, thus reflecting the strong expansion of India’s digital infrastructure.

North America Market Insights

The North America market is expected to grow at a considerable rate from 2026 to 2035. The region benefits from the rapid expansion of artificial intelligence clusters and the continuous evolution of hyperscale data centers. The region is considered to be a primary hub for global technology giants, which fuels an insatiable demand for ultra-high-speed data center interconnects and advanced pluggable optics. For instance, in February 2024, Astound Business Solutions announced the launch of a nationwide 400G Wavelength service, which is powered by Ciena’s WaveLogic 5 Extreme and Nano optics, to deliver massive capacity for carriers, enterprises, and public sector organizations. It covers about 41,000 route miles and connects over 100 data centers, and the service provides low‑latency, point‑to‑point bandwidth for hyperscaler and cloud applications, thus elevating the growth potential of optical transport networks.

A strong industry push toward disaggregated, open optical networking architectures that prevent vendor lock-in and enhance software-defined control is driving the U.S. optical transport network market. The need to connect sprawling data center campuses, domestic service providers, and enterprises is proactively deploying ultra-high-speed coherent pluggable optics, leading the global transition toward highly scalable and long-haul transport infrastructure. In March 2026, Adtran showcased its latest open optical networking innovations at OFC 2026. It also mentioned some of the key demonstrations, which include LiteWave800™, which is an ultra‑low‑power 800G pluggable transceiver setting a new 1pJ/bit efficiency benchmark, REAL AI for explainable automation in operations, and quantum‑safe networking with the FSP 3000 S‑Flex™.

In Canada, the optical transport network market has gained immense exposure owing to the unique challenge of connecting vast geographic distances and a growing concentration of hyperscale data centers in major metropolitan hubs. This market is also catalyzed by remarkable investments in middle-mile fiber infrastructure to bridge rural connectivity gaps, along with a strong technical shift toward automated solutions that optimize network efficiency across long-haul backbones. Based on the government data published in July 2023, Canada and the Northwest Territories have announced a joint investment of USD 19.7 million to build the nation’s most northerly fiber optic link between Inuvik and Tuktoyaktuk. This project is supported by the Inuvialuit Regional Corporation and will strengthen healthcare, education, local economies, and Arctic science, thus elevating the growth potential of optical transport networks.

Europe Market Insights

Europe market has acquired a central position in the global landscape. The region’s market is largely driven by strict data sovereignty laws and cross-border digital integration. The region also benefits from a strong emphasis on energy-efficient optical technologies and sustainability, wherein operators seek to reduce the carbon footprint of expanding data center hubs. In June 2026, the European Commission stated that 96.8% of households now possess basic 5G coverage, and more companies are adopting cloud, AI, and data solutions. It also mentioned that digital skills have improved, with more than 60% of residents having basic competencies. The Commission recommends that Member States update national roadmaps, mobilize investments, and thus, this heightens demand in the optical transport network industry.

The strong demand for scalable and efficient data transmission across telecom operators, cloud service providers, and large enterprises is reshaping the growth dynamics of the optical transport network market in Germany. Adoption of advanced Optical Transport Network solutions is being driven by the ongoing modernization of carrier networks and the expansion of data-heavy applications such as industrial automation and digital services. In March 2026, Fraunhofer HHI and Fujitsu’s 1Finity together announced the launch of a long‑term cooperation under the SHINKA project to advance open and disaggregated optical networking. The partnership is highly focused on developing federated digital twins and multi‑vendor testbeds to validate automation, interoperability, and AI‑assisted operations for next‑generation networks. In addition, the initiative also strengthens contributions to global standardization, thereby driving scalable, automated, and interoperable optical networks for the AI era.

The UK optical transport network market is projected for exponential growth, driven primarily by dense interconnect traffic flows between data center clusters, sustained upgrades to metro fiber rings. The market’s upliftment is also fueled by the growing role of coastal landing stations that funnel international capacity into domestic backbone routes. For instance, in January 2025, Openreach selected Nokia to build its One Network Platform, which is an open‑access fiber network that will expand coverage from 17 million to 25 million UK premises by the end of 2026. The platform is powered by Nokia’s Altiplano and NSP domain controllers, and it will automate fiber services across GPON, XGS PON, and Ethernet, reducing OSS complexity by 85% and hence such instances denote a lucrative opportunity for the country’s market to grow.

Key Optical Transport Network Market Players:

- Cisco Systems, Inc. (U.S.)

- Nokia Corporation (Finland)

- Huawei Technologies Co., Ltd. (China)

- Ciena Corporation (U.S.)

- Ericsson AB (Sweden)

- Fujitsu Limited (Japan)

- NEC Corporation (Japan)

- ZTE Corporation (China)

- ADTRAN Holdings, Inc. (U.S.)

- Ribbon Communications Inc. (U.S.)

- Juniper Networks, Inc. (U.S.)

- t3 Broadband, LLC (U.S.)

- Aureon, Inc. (U.S.)

- Nippon Telegraph and Telephone Corporation (NTT) (Japan)

- NTT Innovative Devices Corporation (NII) (Japan)

- NTT East Corporation (NTT EAST) (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Cisco Systems, Inc. is a major participant in the market, which is leveraging its optical networking portfolio to support metro, long-haul, subsea, and data center interconnect applications. The company has strong prominence in offering solutions, i.e., the NCS 1014 transponder platform, open line systems, coherent optics, and optical network automation software.

- Nokia Corporation is one of the leading global suppliers of optical transport equipment, which is serving telecom operators, cloud providers, enterprises, and data center operators. The firm’s Optical Networks division provides coherent optical engines, intelligent pluggables, open optical line systems, and AI-based network automation.

- Huawei Technologies Co., Ltd. is well recognized as one of the largest suppliers of optical transport solutions globally. In addition, the company provides end-to-end optical networking products, including DWDM systems, OTN switching platforms, optical cross-connect solutions, and intelligent network management software.

- Ciena Corporation is a central player in this sector and specializes in optical networking and is frequently regarded as a global leader in high-speed connectivity. The company's portfolio is highly focused on cloud and AI networking, thereby enabling high-capacity and low-latency data transport for hyperscalers, telecommunications providers, and data center operators.

- Ericsson AB participates in the optical transport ecosystem with the assistance of its transport, mobile backhaul, and integrated network infrastructure services. The firm is highly focused on supporting 5G transport networks, packet-optical integration, and high-capacity mobile backhaul solutions for communications service providers.

Here is a list of key players operating in the global market:

The global optical transport network market is extremely competitive, which hosts well-established telecommunications equipment manufacturers and optical networking specialists. The pioneering companies, i.e., Cisco, Nokia, Huawei, Ciena, and Ericsson, intensely compete through continuous innovation in coherent optics, DWDM systems, and high-capacity 400G/800G transport solutions. Mergers & acquisitions, investments in terms of AI-based network automation, and partnerships with telecom operators and cloud service providers are certain strategies opted for by the leading market players. In September 2025, NGN entered into a partnership with Ribbon Communications to modernize its optical network infrastructure across North Georgia by deploying the Apollo 800G solution to deliver scalable broadband capacity. This strategic collaboration enhances connectivity for healthcare, education, businesses, and underserved communities, thereby supporting 100G, 400G, and 800G services.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, Nokia, t3 Broadband, and Aureon entered into a partnership to deploy an ultra-high-capacity optical transport network, which delivers up to 100 Tb/s of AI-ready connectivity with scalability to 400 Tb/s. This new route links a North Dakota data center to the Chicago metro area.

- In December 2025, NII, NTT, and NTT EAST achieved the world’s first demonstration of automated optical transport layer control, which enables rapid wavelength-path switching and addition based on real-time network conditions. This allows traffic rerouting within 10 minutes during severe disasters.

- Report ID: 8639

- Published Date: Jun 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.