Optical Film Market Outlook:

Optical Film Market size was valued at USD 33.1 billion in 2025 and is projected to reach USD 63.4 billion by the end of 2035, rising at a 7.5% CAGR during the forecast period, 2026-2035. In 2026, the industry size of optical film is evaluated at USD 35.5 billion.

The worldwide optical film market is continuously expanding based on factors, including raw material supply stability for polyvinyl alcohol (PVA), the presence of intellectual property licensing frameworks, and trade dynamics for display-grade optical substrates. According to official statistics published by NLM in September 2024, a freeze/thaw (F/T) procedure is typically responsible for freezing a subsequent PVA solution at concentrations usually ranging from -10 degrees Celsius to -40 degrees Celsius, for almost 12 hours to 24 hours. This is followed by thawing it at a room temperature of 25 degrees Celsius for 1 to 3 hours. Therefore, these cross-linked PVA hydrogels are increasingly preferred for different applications, based on which there is a continuous supply across different countries, which is positively impacting the optical film market growth and development.

2024 PVA Export and Import Global Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

404 million |

- |

|

U.S. |

217 million |

- |

|

Japan |

210 million |

- |

|

Netherlands |

- |

177 million |

|

Belgium |

- |

161 million |

|

Germany |

- |

145 million |

|

Global Trade Valuation |

1.5 billion |

|

|

Global Trade Share |

0.006% |

|

|

Product Complexity |

1.7 |

|

|

Export Growth |

1.8% |

|

Source: OEC

Furthermore, the migration towards rollable film architectures, the integration of energy-harvesting layers within optical stacks, and the adoption of self-healing surface coatings are certain trends that are responsible for driving the optical film market globally. As stated in an article published by NLM in November 2025, self-healing surface coatings constitute a healing efficiency of 100%, thus indicating a complete recovery of the measured property. Additionally, in terms of operating conditions, these particular coatings comprise a material that demands 120 degrees Celsius for healing. Besides, PANI-based hallosyte nanotubes (HNTs) successfully achieved an estimated 14.5 wt.% loading and comprise an enhanced barrier performance by 2 to 4 orders of magnitude within 3.5 wt.%, thereby denoting a huge growth opportunity for the market globally.

Key Optical Film Market Insights Summary:

Regional Highlights:

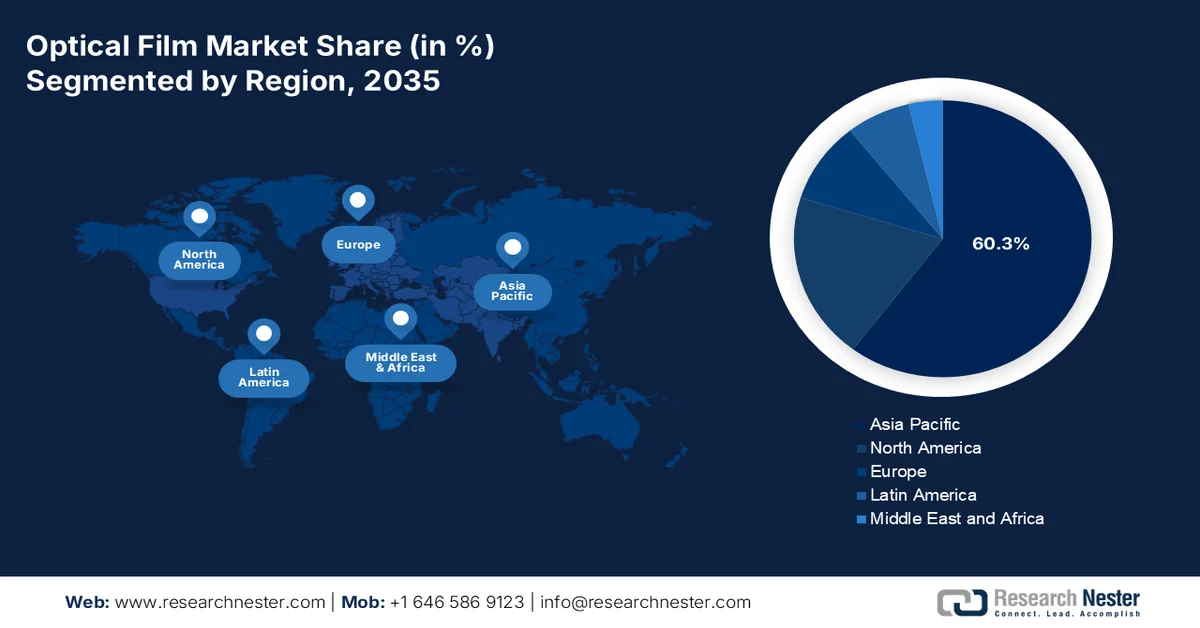

- Asia Pacific is anticipated to dominate the optical film market with a 60.3% share by 2035, impelled by strong display panel manufacturing and rising consumer electronics demand across emerging economies

- Europe is expected to witness the fastest growth during 2026–2035, spurred by increasing adoption of premium electronics, automotive displays, and digital cockpit technologies

Segment Insights:

- The consumer electronics segment is projected to account for a dominant 65.6% share of the optical film market by 2035, propelled by its expanding role in enhancing communication, entertainment, and productivity alongside rising global electronics trade

- The polarizing film sub-segment is expected to secure the second-largest share over the forecast period 2026–2035, fueled by its critical function in improving contrast, minimizing glare, and regulating light across advanced optical applications

Key Growth Trends:

- Expansion of automotive head-up display adoption

- Proliferation of transparent OLED advertising displays

Major Challenges:

- Intense margin pressure from downstream consolidation

- Raw material constraints and supply chain fragility

Key Players: 3M Company, Nitto Denko Corporation, Sumitomo Chemical Co. Ltd., Toray Industries Inc., LG Chem Ltd., Samsung SDI Co. Ltd., Saint-Gobain S.A., Mitsubishi Polyester Film Inc., Teijin Limited, Zeon Corporation, Kolon Industries Inc., Hyosung Chemical Co. Ltd., SKC Co. Ltd., Toyobo Co. Ltd., Fujifilm Corporation, Shinhwa Intertek Corporation, BenQ Materials Corporation, Sanritz Automation Co. Ltd., MNTech Co. Ltd., Eternal Materials Co. Ltd., Kuraray Co. Ltd., Vishay Intertechnology Inc., Samsung Display.

Global Optical Film Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 33.1 billion

- 2026 Market Size: USD 35.5 billion

- Projected Market Size: USD 63.4 billion by 2035

- Growth Forecasts: 7.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (60.3% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Vietnam, Thailand, Indonesia, Brazil

Last updated on : 1 May, 2026

Optical Film Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of automotive head-up display adoption: The automotive industry is increasingly adopting windshield-projected head-up displays as suitable features in mid-range vehicles that move beyond previous luxury-only availability. According to official statistics published by NLM in March 2024, an estimated 1.3 million people succumb yearly, owing to road traffic accidents, and 94% of these incidents are readily contributed to by human error. Besides, the road environment is unpredictable, and it is very easy to cause traffic accidents. Therefore, to combat these, a heads-up display is considered to be an interaction-specific in-vehicle display technology for projecting driving information onto the physical scene and ensuring driving safety, which in turn, is fueling the optical film market growth.

- Proliferation of transparent OLED advertising displays: Both public and retail space applications are implementing transparent OLED displays that readily appear as clear glass at the power off time and become vibrant signage during illumination. As stated in a data report published by Invest Korea Organization in November 2023, OLEDs are predicted to lead the industrial growth by an average yearly rate of 3.7% by the end of 2027. Based on this future growth, China is continuing to support OLEDs at the national level, along with LCDs. In addition, Japan and Taiwan are significantly increasing their generous investment in next-generation micro-LED technology. Therefore, with such developments in this industry, the optical film market is proliferating across different nations.

- Demand for anti-microbial optical films: Self-service terminals, interaction directories, and ticketing machines in high-traffic public locations are rapidly specified with anti-microbial optical films. Moreover, these films incorporate silver-ion or copper-based additives within the coating matrix that disrupt bacterial cell membranes upon contact. However, the challenge lies in maintaining optical clarity and touch sensitivity while achieving effective microbial reduction. Besides, transportation hubs and healthcare facilities are leading adopters, specifying films that reduce surface contamination by specified log values between cleaning cycles. Therefore, based on this, there is a huge growth opportunity for the optical film market globally.

Challenges

- Intense margin pressure from downstream consolidation: Supply chain in the optical film market operates under severe pricing asymmetry caused by extreme buyer power concentration. Major electronics original equipment manufacturers and display panel producers have consolidated into a handful of global giants controlling the majority of smartphone, television, and laptop production. These downstream behemoths leverage their purchasing volume to force annual price reductions on optical film suppliers while simultaneously demanding tighter optical uniformity, thinner profiles, and broader temperature stability, along with improvements that typically raise production costs. Additionally, many large panel makers have internalized basic optical film production, creating a captive supply that erodes external suppliers' market share across commoditized film types.

- Raw material constraints and supply chain fragility: The aspect of manufacturing in the optical film market depends on a narrow set of ultra-high-purity polymers, specialized optical coatings, and precision-grade release liners sourced from a concentrated supplier base. This creates pronounced vulnerability to upstream disruption. Any supply irregularity in optical-grade polyethylene terephthalate, polycarbonate, or triacetyl cellulose can paralyze multiple film conversion lines simultaneously, as substitute materials rarely meet the stringent optical clarity, haze control, and birefringence requirements mandated by premium displays. Furthermore, the manufacturing equipment required for micro-replication of prismatic structures on brightness enhancement films is highly proprietary, with lead times for new tooling extending beyond standard business planning horizons.

Optical Film Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.5% |

|

Base Year Market Size (2025) |

USD 33.1 billion |

|

Forecast Year Market Size (2035) |

USD 63.4 billion |

|

Regional Scope |

|

Optical Film Market Segmentation:

End use Segment Analysis

The consumer electronics segment is anticipated to garner the largest share of 65.6% in the optical film market by the end of 2035. The segment’s upliftment is driven primarily by its increased use in modern life to enhance daily communication, entertainment, and productivity, while fueling worldwide economic growth through continuous advancement. According to official statistics published by NLM in September 2023, electronics exports and imports in the global electronics industry have increased by 210% and 219%, respectively, over the past 20 years. In addition, G-7 countries exported 34% and imported 37% of electronics, and significantly cater to 22% of the worldwide high-tech product exports. Besides, there has been growth in trade facilities for computer and electronic components by 4% and 12%, thereby bolstering the segment’s exposure.

2024 Computer Export and Import Global Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

185 billion |

- |

|

Taipei |

60.6 billion |

- |

|

Mexico |

56.7 billion |

- |

|

U.S. |

- |

140 billion |

|

Hong Kong |

- |

32.6 billion |

|

Germany |

- |

28.9 billion |

|

Global Trade Valuation |

504 billion |

|

|

Global Trade Share |

2.2% |

|

|

Product Complexity |

1.0 |

|

|

Export Growth |

24.7% |

|

Source: OEC

Film Type Segment Analysis

During the forecast period, the polarizing film sub-segment, which is part of the film type segment, is projected to capture the second-largest share in the optical film market. The sub-segment’s growth is highly fueled by its importance for enhancing contrast, reducing glare, and controlling light in optics and technology. As stated in an article published by NLM in November 2023, poly film is readily supplied by Kuraray Co., Ltd., which comprises a polymerization degree of 1,700, along with 99.9% of saponification degree, and 75 μm thickness. Besides, a Bruker Avance 500 spectrometer is also utilized by operating at 500 MHz, while DMSO-d6 is used as a suitable solvent, and TMS serves significantly as the internal standard. Therefore, with the presence of such materials, the utilization of polarizing film is eventually increasing across different nations.

Application Segment Analysis

The smartphones and tablets sub-segment, part of the application segment, is expected to grab the third-largest share in the optical film market by the end of the stipulated timeline. The sub-segment’s development is highly driven by its increased utilization for replacing tools in modern life and providing instant accessibility to information, on-the-go productivity, and constant connectivity. As per an article published by NLM in August 2025, the number of mobile Internet consumers, particularly in China, was estimated at just more than 1 billion in December 2022, which accounted for 36 million more than in December, and over 99% of people in the country accessed the Internet through smartphones. However, an analytical study was conducted on 125,000 children and adolescents in the U.S., which demonstrated that spending over 2 hours a day on screens increased depression, thereby indicating limited smartphone and other device utilization.

Our in-depth analysis of the optical film market includes the following segments:

|

Segment |

Subsegments |

|

End use |

|

|

Film Type |

|

|

Application |

|

|

Function |

|

|

Material |

|

|

Manufacturing Process |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Optical Film Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the optical film market is anticipated to account for the highest share of 60.3% by the end of 2035. The market’s upliftment in the region is primarily attributed to display panel manufacturing across South Korea, Japan, and China, along with a rise in consumer electronics consumption in Southeast Asia and India. According to official statistics published by the ICRIER Organization in October 2024, the region caters to more than 50% of the global population and over 35% of the worldwide gross domestic product (GDP). Besides, the e-commerce industry in the region was significantly valued at USD 2.9 trillion as of 2022 and is further projected to be worth USD 6.1 trillion by the end of 2030. Besides, increased urbanization, as well as an upsurge in technological developments, have led to the upliftment of the market in the overall region.

The optical film market in China is growing significantly, owing to the massive demand for polarizer films, optical clear adhesives, brightness enhancement films, government procurement strategies, and strong electric vehicle mandates. As stated in a data report published by the U.S. International Trade Commission in April 2024, there has been an increase in electric vehicle exports in the country by 10.1% as of 2023 to almost 1.6 million. In addition, this demonstrated an increase in export valuation of more than 123.3% from USD 295 million to USD 36.7 billion in the same year. In addition, the average unit of domestic electric vehicle exports in quantity has increased from USD 2,000 to USD 23,100. Moreover, the high-income nations’ share of the country’s exports by volume surged from 4.95 to 60.0%, thus driving the market development.

The aspects of the governmental scheme for electronics manufacturing, an increase in smartphone user base, growth in television penetration, the Make in India approach, the establishment of module assembly facilities, and a focus on component localization are certain factors for proliferating the optical film market in India. Based on government estimates published by the PIB in November 2025, the country’s television network readily connects 900 million viewers across 230 million households globally. In addition, 918 privately owned satellite channels were operational in March 2025 that reflected a vibrant broadcast ecosystem. Furthermore, 65 million DD Free Dish homes are also driving digital inclusion. Therefore, based on all these expansions, there is a huge market demand and growth in the overall country.

Europe Market Insights

Europe in the optical film market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by premium consumer electronics, medical display applications, automotive display implementation, advanced manufacturing bases, robust automotive industries, and an increase in the adoption of digitalized cockpit displays. According to official statistics published by Europe Automobile Manufacturers’ Association in April 2026, in terms of vehicle trade, production, and sales, there was a rise in the region’s GDP by 1.5% as of 2025, along with headline inflation expected to account for 2% target by the end of 2026. Besides, the regional car production landscape led to Germany producing 21% of cars, which is followed by Slovakia, Czechia, France, and Spain, and regional manufacturers supplied 73% of the industry. Therefore, with this continuous increase, there is a huge demand for optical films in the region.

The optical film market in Germany is gaining increased traction, owing to the existence of a strong automotive display industry, innovative electronics manufacturing, robust chemical industry foundations, different federal programs, and sustainability. As stated in an article published by the Germany Trade & Invest (GTAI) in February 2026, the German Electrical and Electronic Manufacturers' Association demonstrated a surge in the electrical and digital industry by 5.1% to almost USD 300.9 billion as of 2025. Besides, as per the June 2025 Deutschland article, the electronics industry made a suitable contribution to the country’s GDP with a turnover of USD 280.7 billion every year. In addition, over 14,000 organizations secured almost 900,000 employment opportunities, thereby making it extremely suitable for driving the optical film market expansion in the country.

The government’s commitment to supporting innovative materials manufacturing, a focus on industrial decarbonization, hydrogen fuel switching, energy-efficient production methods, and contributions initiated by domestic manufacturers are a few trends that are responsible for driving the optical film market in the UK. As per an article published by the UK Government in February 2026, the country’s manufacturing value chain readily contributed USD 446.6 billion and also supported 4.3 million full-time equivalent employment opportunities as of 2022. This demonstrates an estimated 15% of national value added and 14% of employment in the country, in comparison to 9.1% of value added and 7.1% employment from previous years. Therefore, with this continuous expansion in the manufacturing industry, the optical film market demand is deliberately growing in the nation.

North America Market Insights

North America in the optical film market is projected to experience considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the presence of an innovative consumer electronics industry, military-grade display requirements, automotive display integration, the adoption of premium display technologies in electric vehicles, and a rise in the need for anti-glare films and high-brightness. According to official statistics published by the U.S. International Trade Commission in September 2023, there was an increase in electronics products exports in the U.S. from USD 16.7 million to USD 302.8 billion, by 5.8% growth as of 2022. Additionally, there was also an increase in domestic re-exports from USD 11.3 billion to USD 135.7 billion, accounting for a 9.1% growth in the same year, thereby enhancing the market demand in the overall region.

Electronic Products and Country Export Analysis in the U.S., 2022

|

Electronic Products |

Export to Countries |

||

|

Product Type |

Valuation (USD) |

Country |

Valuation (USD) |

|

Medical Goods |

2.6 billion |

Mexico |

1.9 billion to 19.7 billion |

|

Measuring, Testing, and Controlling Instruments |

1.8 billion |

The Netherlands |

1.3 billion to 10.6 billion |

|

Computers, Peripherals, and Parts |

739 million |

Canada |

981 million to 10.6 billion |

|

Circuit Apparatuses |

690 million |

China |

3.5 billion to 18.3 billion |

Source: U.S. International Trade Commission

The optical film market in the U.S. is gaining increased exposure, owing to workplace wellness and display eye strain mitigation, modernization in aerospace and defense display, automotive display integration, energy efficiency and smart building retrofits, as well as consumer preference for premium display performance. As stated in an article published by the U.S. General Services Administration in June 2024, the Administrator of the U.S. General Services Administration (GSA) invested USD 80 million from the Inflation Reduction Act (IRA) into smart building technologies. This resulted in diminishing emissions, enhancing efficiencies, lowering expenses, and increasing comfort accessibility across roughly 560 domestic federal buildings. Therefore, with such generous investment opportunities, the market is gradually gaining exposure in the overall country.

The adoption of consumer display and electronics, the integration of automotive display, an expansion in polarizer film across different industries, technological innovations in display technologies, and stabilized consumer electronics supply chain implementation are a few factors that are driving the optical film market in Canada. As per an article published by the ITA in October 2024, the country unveiled the Digital Services Tax (DST), demonstrating a 3% tax on large-scale technological company revenues. Besides, the government has readily committed more than USD 1.4 billion towards developing sovereign AI-based compute capacity and cloud facilities. Moreover, the domestic digital transformation industry reached USD 74.0 billion by the end of 2025, along with a growth rate of 25% since 2024, thus denoting an optimistic outlook of the optical film market growth.

Key Optical Film Market Players:

- 3M Company (U.S.)

- Nitto Denko Corporation (Japan)

- Sumitomo Chemical Co., Ltd. (Japan)

- Toray Industries, Inc. (Japan)

- LG Chem Ltd. (South Korea)

- Samsung SDI Co., Ltd. (South Korea)

- Saint-Gobain S.A. (France)

- Mitsubishi Polyester Film, Inc. (Japan)

- Teijin Limited (Japan)

- Zeon Corporation (Japan)

- Kolon Industries, Inc. (South Korea)

- Hyosung Chemical Co., Ltd. (South Korea)

- SKC Co., Ltd. (South Korea)

- Toyobo Co., Ltd. (Japan)

- Fujifilm Corporation (Japan)

- Shinhwa Intertek Corporation (South Korea)

- BenQ Materials Corporation (Taiwan)

- Sanritz Automation Co., Ltd. (Japan)

- MNTech Co., Ltd. (South Korea)

- Eternal Materials Co., Ltd. (Taiwan)

- Kuraray Co., Ltd. (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Samsung Display (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- 3M Company leverages its deep expertise in micro-replication and multilayer optical film technologies to supply advanced brightness enhancement and reflective polarizer solutions for backlight units across consumer electronics displays. The company continuously innovates in durable, anti-glare, and privacy films tailored for automotive and handheld smart devices.

- Nitto Denko Corporation is a dominant force in the polarizing film segment, supplying critical light-management layers that enable high contrast and color accuracy in LCD and OLED panels. The company focuses on ultra-thin, flexible, and high-durability optical stacks for foldable smartphones and large-format televisions.

- Sumitomo Chemical Co., Ltd. maintains a strong position in the polarizer and optical compensation film markets, supporting high-resolution display performance in premium electronics. The company invests heavily in large-area film manufacturing and automotive display optics to align with evolving panel architectures.

- Toray Industries, Inc. specializes in high-performance polyester optical films, including light diffusion, reflection, and prism sheets used in backlight units for televisions and monitors. The company focuses on ultra-purity film substrates and surface engineering to meet stringent display uniformity and brightness requirements.

- LG Chem Ltd. is a major producer of polarizing plates and brightness enhancement films, closely integrated with leading display panel manufacturers to co-develop next-generation optical stacks. The company prioritizes material science breakthroughs in transparent, flexible, and high-transmission films for rollable and foldable smart devices.

Here is a list of key players operating in the global optical film market:

The optical film market is characterized by a highly concentrated competitive landscape dominated by manufacturers headquartered in the Asia Pacific, particularly Japan, South Korea, and China. Moreover, recent industry consolidation through strategic mergers and acquisitions has reshaped the global supply structure, with leading players transitioning from volume leadership toward technology differentiation. For instance, Japan and South Korea-based companies continue to lead in premium segments such as OLED-optimized polarizers and ultra-thin functional films. Besides, in June 2025, Kuraray Co., Ltd. expanded its production facilities for optical-utilization poval film, which is a base material for polarizing films that are used in liquid crystal displays (LCDs) IN Japan, thereby making it suitable for bolstering the optical film industry globally.

Corporate Landscape of the Optical Film Market:

Recent Developments

- In April 2026, Vishay Intertechnology, Inc. launched its latest thin film submount platform, which is designed to effectively support next-generation optical transceivers, advanced electronic packaging applications, and RF modules that require increased thermal performance, high-frequency signal integrity, and precision alignment.

- In August 2025, Samsung Display introduced the newest foldable display brand, MONT FLEX ™, which aimed to differentiate the company’s industry-specific foldable OLED technology, thus escalating premium differentiation through technology and branding.

- In March 2025, Toray Industries, Inc. unveiled PICASUS™ VT, which is a comprehensive nano-multiplier film that readily reflects light only from oblique angles, and is applied to head-up display (HUD) technology for delivering double image-free high-definition displays across a full-screen area of windshields.

- Report ID: 8552

- Published Date: May 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.