Military Antenna Market Outlook:

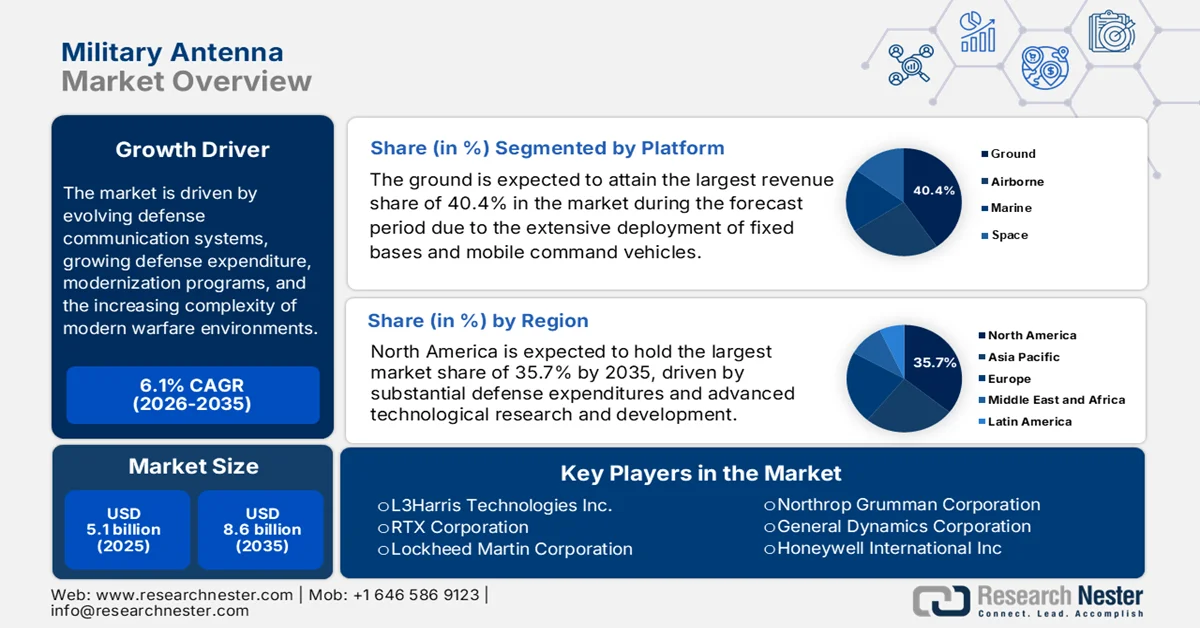

Military Antenna Market was valued at USD 5.1 billion in 2025 and is expected to grow to USD 8.6 billion by 2035, at a CAGR of 6.1% over the forecast year, i.e., 2026-2035. In 2026, the industry size of military antenna is evaluated at USD 5.4 billion.

The military antenna market is positioned for sustained strategic growth, which is driven by evolving defense communication systems, growing defense expenditure, modernization programs, and the increasing complexity of modern warfare environments. According to the official statistics published by Stockholm International Peace Research Institute (SIPRI) in April 2024, the global military spending increased for the ninth consecutive year in 2023, which surpassed a total value of USD 2,443 billion in 2023, marking a 6.8 per cent year-on-year rise. Meanwhile, the global military burden rose to 2.3% of world GDP, whereas the military spending as a share of total government expenditure increased by 0.4 percentage points to 6.9 per cent. On a per capita basis, world military spending reached USD 306, the highest level in the past few decades.

Top 10 Countries by Military Expenditure in 2023: Officially-Reported Defense Spending Analysis

|

Country |

Military Expenditure (USD Billion) |

Share of Global Spending (%) |

|

U.S. |

916 |

37 |

|

China |

296 |

12 |

|

Russia |

109 |

4.5 |

|

India |

83.6 |

3.4 |

|

Saudi Arabia |

75.8 |

3.1 |

|

UK |

74.9 |

3.1 |

|

Germany |

66.8 |

2.7 |

|

Ukraine |

64.8 |

2.7 |

|

France |

61.3 |

2.5 |

|

Japan |

50.2 |

2.1 |

Source: SIPRI

Furthermore, the growth in 2023 was largely driven by the ongoing war in Ukraine and escalating cross-border tensions in Asia and Oceania and the Middle East, wherein the military expenditure increased across all five geographical regions, particularly in Europe, Asia, Oceania, and the Middle East. In addition, the report from the U.S. Department of Defense in June 2025 disclosed that the U.S. Army Research Laboratory and C5ISR Center are advancing experiments into diamond-based semiconductor materials and silicon photonic device structures for next-generation radar and communications systems. The planned financial year 2025 work includes phased array antennas with chip-scale photonic beamformers, multi-layer meta surface designs for smart radar enclosures, and multiband anti-jam antenna arrays integrated into army communications and navigation systems, hence driving growth in the military antenna market.

U.S. Army Funding Allocation (FY 2024-FY 2026) for Advanced Radar and Communications Systems

|

Fiscal Year |

Funding Allocation (USD Million) |

|

FY 2024 |

4.523 |

|

FY 2025 |

4.562 |

|

FY 2026 |

3.704 |

Source: U.S. Department of Defense

Key Military Antenna Market Insights Summary:

Regional Highlights:

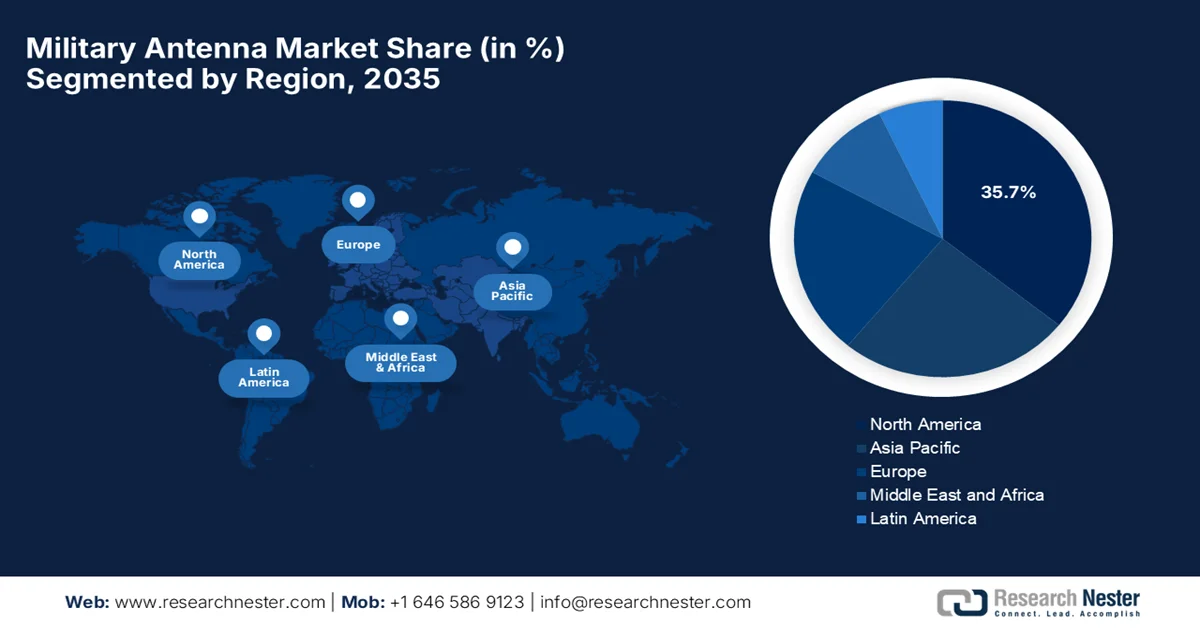

- North America is projected to capture 35.7% share of the military antenna market by 2035, attributed to substantial defense spending and continuous technological R&D strengthening secure communication, surveillance, and electronic warfare capabilities.

- Asia Pacific is anticipated to witness accelerated growth during 2026–2035, supported by expanding investments in indigenous defense technologies and increasing demand for advanced communication, intelligence, and surveillance systems.

Segment Insights:

- The Ground platform segment is projected to capture a 40.4% share by 2035, fueled by extensive deployment of antennas across fixed bases, mobile command vehicles, tactical shelters, and forward operating bases supporting battlefield communications.

- The Communication application segment is expected to register a substantial share in the military antenna market by 2035, stimulated by the growing need for secure, high-bandwidth, and frequency-agile antennas enabling resilient multi-domain military communications.

Key Growth Trends:

- Defense modernization efforts

- Increasing demand for secure military communications

Major Challenges:

- High research & development costs

- Spectrum congestion & frequency management

Key Players: L3Harris Technologies, Inc., RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, General Dynamics Corporation, Honeywell International Inc., Viasat, Inc., Antenna Products Corporation, Southwest Antennas, MTI Wireless Edge Ltd, Cobham Limited, BAE Systems plc, Thales Group, Rohde & Schwarz GmbH & Co. KG, Saab AB, ASELSAN A.Ş., HENSOLDT AG, Airbus SE, Bharat Electronics Limited, Eylex Pty Ltd, Global Invacom Group Limited, ThinKom Solutions, Orbit Communication Systems.

Global Military Antenna Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2024 Market Size: USD 5.1 billion

- 2025 Market Size: USD 5.4 billion

- Projected Market Size: USD 8.6 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Russia, United Kingdom, Germany

- Emerging Countries: India, Japan, South Korea, Brazil, Australia

Last updated on : 10 March, 2026

Military Antenna Market - Growth Drivers and Challenges

Growth Drivers

- Defense modernization efforts: The consistent administrative efforts to modernize military systems are the major growth booster for the military antenna market. These programs also include the upgrades to antenna and communication systems to replace legacy hardware. Based on the government data, which was published in July 2025, the strategic defense review commits the UK to spend 2.5% of GDP on defense by 2027 and aims for 3% in the next parliament. It has already made an investment of USD 6.7 billion in the same year and a USD 14.7 billion annual investment budget. In addition, the review modernizes the armed forces with integrated warfighting, autonomous systems, drones, AI, CyberEM Command, enhanced NATO leadership, and a whole-of-society approach to national security. Thus, such instances will drive demand for advanced communications, radar, and sensor antennas, increasing the growth potential of the military antenna market in the upcoming years.

UK Strategic Defense Review 2025: Key Defense Investments and Spending

|

Project |

USD (billion) |

Notes |

|

Nuclear warhead programme |

20.1 |

Sovereign nuclear deterrent, continuous at-sea deterrent |

|

Homeland defense |

1.34 |

Air & missile defense, CyberEM Command |

|

Munitions |

8 |

Includes procurement and production |

|

“Always-on” munitions pipeline |

2 |

Ensures continuous supply and readiness |

|

Military accommodation/infrastructure |

9.4 |

Renewal of forces housing and facilities |

|

Armed Forces modernization |

- |

Integrated warfighting, autonomous systems, drones, AI, NATO |

Source: UK Government

- Increasing demand for secure military communications: The modern military operations require secure, jam-resistant communications across tactical, strategic, and coalition networks. In this context, antennas have become central to C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance & Reconnaissance) and network-centric warfare systems, driving upliftment of the military antenna market. In July 2025, the U.S. Space Force’s Space Systems Command (SSC) announced the Protected Tactical SATCOM (PTS) Family of Systems, which is to rapidly deliver anti-jam wideband satellite communications to warfighters globally. This initiative efficiently enhances protected tactical waveform capabilities, enabling secure, resilient, all-weather communications in contested and uncontested environments, hence suitable for driving the market’s demand and exposure.

- Proliferation of unmanned platforms: There has been an increased adoption of UAVs, UGVs, and unmanned naval systems, which creates strong demand for lightweight, compact, high-performance antennas to support command and control. Also, these unmanned systems require specialized frequency bands, driving the need for suitable antenna solutions. Small Business Innovation Research (SBIR) topic 2025 AF254-D0801 reported that it is seeking development of high-gain S-band MANET antennas for large (>300 lbs) unmanned aerial systems (UAS) to enable air-to-air and air-to-ground data links of at least 1 Mb/s over 50 miles. It also mentioned that this particular effort focuses on overcoming range limitations of current S-band radios by addressing challenges of orientation, size, weight, and power constraints, with AES-256 encryption for all transmissions, hence contributing to military antenna market expansion.

Challenges

- High research & development costs: The development of military-specific antennas is capital intensive process in terms of research and development in order to meet optimum performance, reliability, and security standards. The aspects of phased array, AESA, and multi-band antennas need proper materials, precision engineering, and extensive testing under severe environmental conditions. Therefore, these factors make the design, prototyping, and certification costly as well as time-intensive. In addition, the smaller vendors operating in the military antenna market mostly struggle to compete with established defense contractors, creating a barrier to market entry. On the other hand, the large companies also need to carefully manage budgets and timelines to prevent cost overruns.

- Spectrum congestion & frequency management: The present-day military antennas need to operate across numerous frequency bands, which include HF, VHF, UHF, SHF, and EHF. As militaries across different nations deploy more communication, radar, and electronic warfare systems, spectrum congestion becomes a highly considerable issue. Interference can degrade system performance, affecting situational awareness, targeting accuracy, and command communication. Therefore, designers in the military antenna market must implement frequency-agile and adaptive technologies to address interference by making sure of compliance with national and international spectrum allocation regulations. Furthermore, proper planning, testing, and certification are required to avoid any type of operational risks, which increases complexity and cost for manufacturers.

Military Antenna Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 5.1 billion |

|

Forecast Year Market Size (2035) |

USD 8.6 billion |

|

Regional Scope |

|

Military Antenna Market Segmentation:

Platform Segment Analysis

In the platform segment, ground is expected to attain the largest revenue share of 40.4% in the military antenna market during the forecast period. The sheer volume of deployed assets, i.e., fixed bases, mobile command vehicles, tactical shelters, and forward operating bases requiring multi-functional antennas for battlefield communications, is the main factor driving its leadership. Besides the ground-based deployments, scale extensively in conflict theaters and allied modernization budgets, positioning this segment as central to military antenna deployments. In January 2024, Silvus Technologies reported that it received a total of USD 3.5 million contract from the U.S. Army PEO C3T to supply ground-based StreamCaster MANET radios for expanded deployment in the army's integrated tactical network as part of Phase II Operational Demonstration testing for FY 2025. Therefore, this deployment underscores the prominence of ground-based antennas in supporting battlefield communications.

Application Segment Analysis

By the conclusion of the forecast period, the communication, which is a part of the application segment, is anticipated to garner a significant share in the military antenna market. The growth of the sub-segment is mainly attributable to secure, resilient voice or data exchange across land, sea, air, and space domains, which is foundational for network-centric warfare and command‑and‑control infrastructures. Modern military networks are looking for high-bandwidth, frequency‑agile, and encrypted link‑capable antennas to support tactical data links, and beyond‑line‑of‑sight (BLOS) SATCOM connectivity. In addition, the increasing adoption of multi-domain operations has driven demand for antennas that can integrate communications across joint forces. Furthermore, militaries are also prioritizing antennas that are capable of supporting rapid redeployment and modularity to match dynamic mission requirements, hence denoting a positive military antenna market outlook.

Type Segment Analysis

The array antennas are predicted to grow at a considerable rate in the military antenna market by 2035. Their capability for electronic beam steering, multi-beam operation, and integration in multi-domain platforms is the main factor behind the subtype’s leadership. These systems support high-resolution radar, electronic warfare, and SATCOM functions with rapid directional agility without mechanical movement. In September 2024, Viasat, Inc. reported that it was allocated a total amount of USD 33.6 million contract by the U.S. Air Force Research Laboratory under the DEUCSI program to develop AESA phased array antennas for tactical aircraft, including rotary-wing platforms. The antennas consist of multi-beam, low SWAP designs with no moving parts, enabling resilient, multi-frequency, multi-orbit satellite communications with LPI and jamming resistance, hence contributing to a wider market expansion.

Our in-depth analysis of the military antenna market includes the following segments:

|

Segment |

Subsegments |

|

Platform |

|

|

Application |

|

|

Type |

|

|

Frequency Band |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Military Antenna Market - Regional Analysis

North America Market Insights

The North America military antenna market is predicted to attain the largest revenue share of 35.7% during the forecast period. The region’s leadership is mainly propelled by high defense spending and technological R&D. The region is witnessing incremental demand fueled by the modernization programs, need for secure, high-frequency communication, surveillance technologies, and electronic warfare capabilities. The U.S. Department of War in June 2024 reported that BAE Systems Information and Electronic Systems in Nashua, New Hampshire, received a total of USD 17,032,142 contract modification to produce and deliver OE-120/UPX antenna group systems for the U.S. Navy and the government of Canada. The contract includes retrofit and installation kits, supporting systems such as identification friend or foe, secondary surveillance, and air traffic control radar, hence suitable for bolstering military antenna market growth in the region.

The U.S. military antenna market’s growth is positively influenced by a strategic shift toward network-centric warfare, which increases the demand for high-bandwidth communication systems across land, air, and sea platforms. In addition, the aspect of continued geopolitical tensions and the rising importance of electronic warfare also contribute to market growth, as the military has a higher priority towards multi-functional antenna technologies. In November 2024, Honeywell reported that it had been allocated a USD 16 million contract by the U.S. Navy to build, test, and integrate 25 antenna array panels for the surface electronic warfare improvement program block 2. These panels enhance shipboard electronic warfare capabilities, supporting early threat detection, analysis, warning, and protection against anti-ship missiles, hence denoting a positive outlook for the market’s growth and exposure.

The systematic reinvestment in national defense, with a prime focus on arctic sovereignty and high-latitude connectivity are responsible for uplifting the military antenna market in Canada. Technological evolution and government backing are also central factors, driving the country’s market. In December 2025, the government of Canada announced a strategic partnership with Telesat Corporation and MDA Space to enhance the country’s Armed Forces’ military satellite communications (MILSATCOM) capabilities through the enhanced satellite communications project - Polar (ESCP-P). This initiative is led by the newly formed Defense Investment Agency, which aims to provide reliable wideband and narrowband connectivity for Arctic operations and strengthen national and continental defense. The project is supported with an initial USD 2.92 million contract for engineering and options analysis work.

APAC Market Insights

The Asia Pacific military antenna market is entering a transformative phase of growth, largely fueled by nations confronting dynamic security environments and investing heavily in communications, intelligence, surveillance, and reconnaissance. Countries in the region are concentrating on accelerating indigenous technology development to reduce dependency on foreign equipment. Ministry of Defense, through Press Information Bureau (PIB), in November 2024, stated that the governments of India and Japan signed a Memorandum of Implementation in Tokyo for the co-development of UNICORN masts, advanced unified complex radio antenna systems, for fitment on India’s Navy ships. The masts will be co-developed with Bharat Electronics Limited and will enhance the stealth and communication capabilities of naval platforms, marking the first-ever India-Japan co-development of defense equipment.

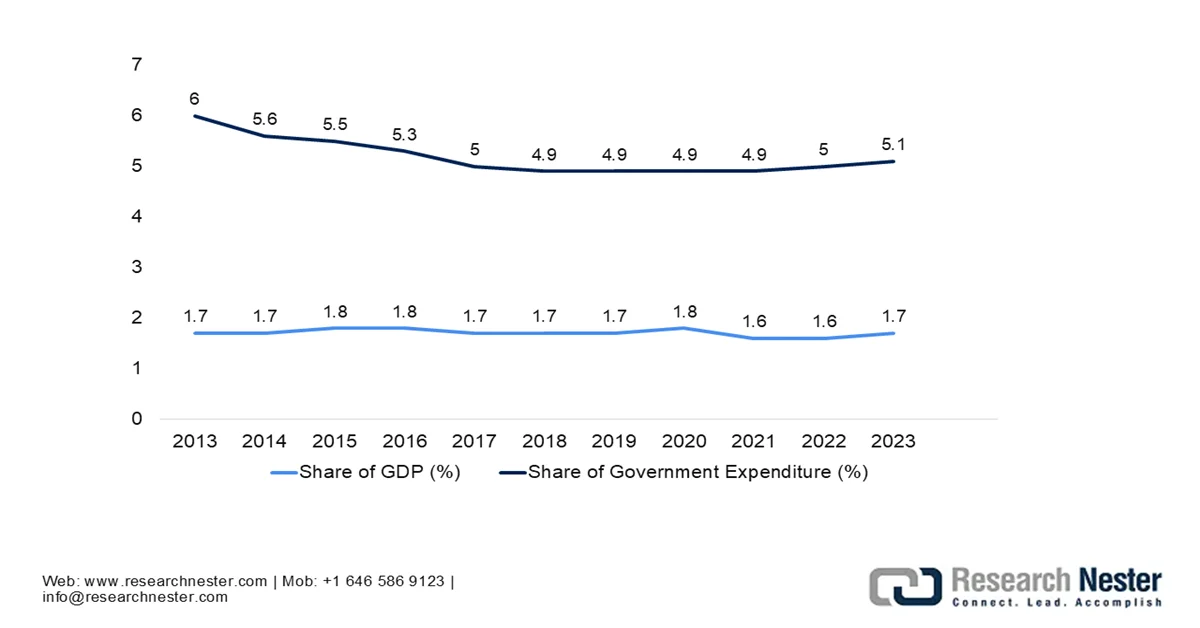

Parallel investments in space and ground-based communication infrastructure are fueling the growth of the military antenna market in China. The army’s transition into a fully digitized, information-centric force under its ongoing modernization drive also fosters a profitable business environment for pioneers in the market. Observer Research Foundation (ORF) in September 2025 revealed that the country’s People’s Liberation Army (PLA) has accelerated its military modernization, commissioning platforms such as the fourth aircraft carrier and tenth Type-055 Renhai-class cruiser, equipped with integrated antennas, radar, and missile systems. China is also reorganizing its forces with the information support force to enhance networked, joint, and all-domain operations. Hence, these reforms aim to build a world-class military by 2049, strengthen China’s regional and global power projection, and accelerate investments in next-generation military communication infrastructure.

China’s Defense Budget Trends (2013-2023): Share of GDP and Government Expenditure Analysis

Source: ORF

The strong indigenous production and national push toward Aatmanirbhar Bharat are boosting the military antenna market in India. The country is aggressively deploying advanced software-defined radios, negotiating co-development agreements for complex antenna masts with partners such as Japan, and preparing influential military communication satellites. In June 2024, PIB reported that the Ministry of Defense announced a partnership between the Military College of Telecommunication Engineering, Indian Army, and SAMEER under MeitY with a collective goal to advance next-generation wireless technologies, including antenna design and satellite communications, for enhanced military capabilities. It also stated that this collaboration includes establishing an Advanced Military Research and Incubation Centre at MCTE to support R&D, innovation, and production with involvement from academia, industry, and startups, hence suitable for bolstering the military antenna market growth in the overall country.

Europe Market Insights

Europe military antenna market is entering a new phase of progress influenced by the coordinated NATO requirements and shared defence priorities that drive standardised antenna specifications across member nations. Countries such as Germany and the UK are integrating advanced signal processing and encrypted communication systems into terrestrial and airborne platforms to support rapid coalition operations. In February 2026, the Space Development Agency (SDA) reported that it assigned a total of USD 30 million HALO Europa prototype agreement to AST SpaceMobile to demonstrate commercial tactical satellite communications (TACSATCOM) using its commercial space vehicles. The demonstrations are expected by December 2027, and this initiative, under the hybrid acquisition for proliferated low-earth orbit program, leverages commercial investments to accelerate capability delivery, reduce risk, and provide companies with experience supporting future SDA space-based operational layers.

The priority on precision and integration excellence, with a strong focus on software-defined radios and adaptable antenna solutions are propelling a favourable ecosystem for Germany military antenna market. Investments in tactical communication technologies are designed to ensure flexibility across land, air, and naval domains, focusing on long service life and compatibility with multinational forces. In July 2024, Germany’s armed forces, the Bundeswehr, awarded Airbus Defence and Space a USD 2.3 billion prime contract for SATCOMBw 3, which is the secure military satellite communications system comprising two new GEO satellites, an upgraded ground segment, launch, and 15 years of operations. The satellites are based on the Eurostar Neo platform, and will enhance secure, high-capacity data transmission and ensure autonomous global communications for the Bundeswehr and NATO commitments into the 2040s, hence suitable for standard market growth.

The focus on secure communications for joint force deployments and expeditionary missions is the main factor driving the growth of the UK military antenna market. The defence programmes, such as satellite communication upgrades and next-generation tactical networks, place a premium on multi-band antenna solutions that can integrate legacy systems with emerging digital architectures. In March 2025, the UK Ministry of Defence announced that the SKYNET 6 satellite 6A had completed its initial testing phase at the National Satellite Test Facility in Harwell. This is co-sponsored by Strategic Command and UK Space Command, wherein the programme represents the country’s largest government investment in its space sector and will deliver advanced, secure SATCOM capabilities with enhanced digital processing and radio frequency performance. This particular military capability is designed, built, and tested entirely in the UK with industry partners such as Airbus Defence and Space UK and Science and Technology Facilities Council. SKYNET 6A will provide reliable military communications for at least 15 years.

Key Military Antenna Market Players:

- L3Harris Technologies, Inc. (U.S.)

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- Viasat, Inc. (U.S.)

- Antenna Products Corporation (U.S.)

- Southwest Antennas (U.S.)

- MTI Wireless Edge Ltd (Israel)

- Cobham Limited (UK)

- BAE Systems plc (UK)

- Thales Group (France)

- Rohde & Schwarz GmbH & Co. KG (Germany)

- Saab AB (Sweden/Europe)

- ASELSAN A.Ş. (Turkey)

- HENSOLDT AG (Germany)

- Airbus SE (Netherlands)

- Bharat Electronics Limited (India)

- Eylex Pty Ltd (Australia)

- Global Invacom Group Limited (Singapore)

- ThinKom Solutions (U.S.)

- Orbit Communication Systems (Israel)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- L3Harris Technologies, Inc. is one of the leading U.S. defense and aerospace solutions providers that supplies an extensive range of military antennas for land, maritime, airborne, and space applications. The company’s strong global defense relationships and broader portfolio across communication, electronic warfare, and SATCOM systems solidify its leadership in this field.

- Lockheed Martin Corporation integrates improved antenna technologies into its core platforms, which also include modern fighter jets, naval vessels, and satellite systems. The firm’s innovations in phased‑array and stealth-compatible antennas support mission-critical communication and missile defense capabilities.

- Thales Group is yet another prominent player in this sector, which develops military antennas suitable for secure communication, SATCOM, and electronic warfare. The company is focused mainly on innovation for multi-domain interoperability and integration across defense networks, which helps it maintain a strong presence in the allied markets.

- RTX Corporation is well recognized for its RF, radar, and communication systems, wherein the military antennas are forming a core part of its defense electronics portfolio. The company concentrates on phased array and electronically steerable designs that enhance platform connectivity and situational awareness in contested environments.

- BAE Systems plc combines deep defense systems knowledge with antenna technology across airborne, land, and naval platforms. The organization is well known for battlefield-proven solutions, and it focuses on high-performance multi-band antennas incorporated into broader communications and C4ISR systems.

Below is the list of some prominent players operating in the global military antenna market:

The companies in the military antenna market are intensely competing through strong R&D and global supply capabilities. U.S. giants such as L3Harris, RTX, Lockheed Martin, and Northrop Grumman dominate through integrated systems and platform‑level contracts, whereas the Europe-specific players such as Cobham, Thales, and Rohde & Schwarz are focused on advanced SATCOM, secure comms, and EW antennas. Indigenous defense programs, strategic partnerships, and export growth are a few factors heightening competency amongst the global leaders. In February 2026, Communications & Power Industries announced that its Antenna Technologies division was awarded a total of USD 151 billion IDIQ contract under the Missile Defense Agency’s SHIELD program. The contract covers a wide range of military antenna and communication capabilities, enabling rapid deployment of innovative solutions for the warfighter, hence making it suitable for standard market growth.

Corporate Landscape of the Military Antenna Market:

Recent Developments

- In February 2026, Global Invacom Group Limited announced the launch of a new rapid‑deploy XY antenna range, which is especially designed to offer fast, reliable multi-orbit and multi-band connectivity for mission-critical government, defense, and commercial operations.

- In December 2025, Orbit Communication Systems notified that it secured a total of USD 2.4 million order from a leading defense integrator, which is based in Europe, for its OceanTRx4 MIL satellite communication systems, featuring 1.15-meter antennas.

- In August 2025, MTI Wireless Edge Ltd announced it had secured a total of USD 1.6 million in new contracts from three local and international defense companies. The contracts cover a range of military antennas, which include airborne communication antennas, anti-jamming GPS systems, and beam-forming antennas for UAV and drone operations.

- In August 2025, ThinKom Solutions reported that it is developing VICTS-based phased array antennas for directed energy weapons applications, such as C-UAS and integrated air and missile defense, to offer a GW-level power handling and precision beam steering.

- Report ID: 8431

- Published Date: Mar 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.