Global Military GPS Receiver Market

1. An Outline of the Global Military GPS Receiver Market

1.1. Market Definition and Segmentation

1.2. Study Assumptions and Abbreviations

2. Research Methodology & Approach

2.1. Primary Research

2.2. Secondary Research

2.3. Data Triangulation

2.4. SPSS Methodology

3. Executive Summary

4. Growth Drivers

5. Major Roadblocks

6. Opportunities

7. Prevalent Trends

8. Government Regulation

9. Growth Outlook

10. Competitive White Space Analysis – Identifying Untapped Market Gaps

11. Risk Overview

12. SWOT

13. Technological Advancement

14. Technology Maturity Matrix for the Military GPS Receiver Market: Recent News

15. Regional Demand

16. Global Military GPS Receiver by Geography – Strategic Comparative Analysis

17. Strategic Segment Analysis: Military GPS Receiver Demand Landscape

18. Military GPS Receiver Demand Trends Driven by rising defense modernization programs, increasing reliance on precision-guided navigation, and growing needs for secure, jam-resistant positioning in contested environments (2026-2037)

19. Root Cause Analysis (RCA) for discovering problems of the Military GPS Receiver Market

20. Porter Five Forces

21. PESTLE

22. Comparative Positioning

23. Global Military GPS Receiver – Key Player Analysis (2037)

24. Competitive Landscape: Key Suppliers/Players

25. Competitive Model: A Detailed Inside View for Investors

26. Company Market Share, 2037 (%)

26.1. RTX Corporation

26.2. Lockheed Martin

26.3. Northrop Grumman

26.4. L3Harris Technologies

26.5. BAE Systems

26.6. Thales Group

26.7. Honeywell International

26.8. Collins Aerospace

26.9. Safran Electronics & Defense

26.10. Elbit Systems

26.11. General Dynamics

26.12. Leonardo S.p.A.

26.13. Israel Aerospace Industries

26.14. Garmin

26.15. Trimble Inc.

27. Global Military GPS Receiver Market Outlook

27.1. Market Overview

27.1.1. Market Revenue by Value (USD Million), and Compound Annual Growth Rate (CAGR)

27.2. Military GPS Receiver Market Segmentation Analysis (2026-2037)

27.2.1. By Technology

27.2.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2. Integrated GPS Modules

27.2.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.3. Hybrid GPS Systems

27.2.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1.3.4. Communication and Data Link

27.2.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

27.2.2. By Frequency

27.2.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

27.2.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

27.2.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3. By Platform

27.2.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

27.2.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4. By Application

27.2.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

27.2.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

27.2.5. By Accuracy

27.2.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

27.2.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

27.2.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

27.2.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

27.2.1. Regional Synopsis, Value (USD Million), 2026-2037

27.2.1.1. North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.1.2. Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.1.3. Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.1.4. Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

27.2.1.5. Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

28. North America Market

28.2. Overview

28.2.1. Market Value (USD Million), Current and Future Projections, 2026-2037

28.2.2. Increment $ Opportunity Assessment, 2026-2037

28.3. Segmentation (USD Million), 2026-2037, By

28.3.1. By Technology

28.3.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.2. Integrated GPS Modules

28.3.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.3. Hybrid GPS Systems

28.3.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

28.3.1.3.4. Communication and Data Link

28.3.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

28.3.2. By Frequency

28.3.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

28.3.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

28.3.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

28.3.3. By Platform

28.3.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

28.3.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

28.3.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

28.3.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

28.3.4. By Application

28.3.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

28.3.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

28.3.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

28.3.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

28.3.5. By Accuracy

28.3.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

28.3.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

28.3.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

28.3.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

28.3.6. Country Level Analysis, Value (USD Million)

28.3.6.1. U.S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

28.3.6.2. Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29. Europe Market

29.2. Overview

29.2.1. Market Value (USD Million), Current and Future Projections, 2026-2037

29.2.2. Increment $ Opportunity Assessment, 2026-2037

29.3. Segmentation (USD Million), 2026-2037, By

29.3.1. By Technology

29.3.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.2. Integrated GPS Modules

29.3.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.3. Hybrid GPS Systems

29.3.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

29.3.1.3.4. Communication and Data Link

29.3.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

29.3.2. By Frequency

29.3.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

29.3.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

29.3.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

29.3.3. By Platform

29.3.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

29.3.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

29.3.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

29.3.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

29.3.4. By Application

29.3.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

29.3.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

29.3.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

29.3.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

29.3.5. By Accuracy

29.3.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

29.3.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

29.3.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

29.3.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

29.3.6. Country Level Analysis, Value (USD Million)

29.3.6.1. UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.2. Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.3. France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.4. Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.5. Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.6. Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.7. Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.8. Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.9. Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.10. Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

29.3.6.11. Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30. Asia Pacific Market

30.2. Overview

30.2.1. Market Value (USD Million), Current and Future Projections, 2026-2037

30.2.2. Increment $ Opportunity Assessment, 2026-2037

30.3. Segmentation (USD Million), 2026-2037, By

30.3.1. By Technology

30.3.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.2. Integrated GPS Modules

30.3.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.3. Hybrid GPS Systems

30.3.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

30.3.1.3.4. Communication and Data Link

30.3.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

30.3.2. By Frequency

30.3.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

30.3.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

30.3.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

30.3.3. By Platform

30.3.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

30.3.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

30.3.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

30.3.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

30.3.4. By Application

30.3.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

30.3.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

30.3.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

30.3.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

30.3.5. By Accuracy

30.3.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

30.3.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

30.3.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

30.3.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

30.3.6. Country Level Analysis, Value (USD Million)

30.3.6.1. China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.2. India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.3. South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.4. Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.5. Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.6. Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.7. Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.8. Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.9. Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.10. New Zealand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

30.3.6.11. Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31. Latin America Market

31.2. Overview

31.2.1. Market Value (USD Million), Current and Future Projections, 2026-2037

31.2.2. Increment $ Opportunity Assessment, 2026-2037

31.2.3. Year-on-Year Growth Forecast (%)

31.3. Segmentation (USD Million), 2026-2037, By

31.3.1. By Technology

31.3.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.2. Integrated GPS Modules

31.3.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.3. Hybrid GPS Systems

31.3.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

31.3.1.3.4. Communication and Data Link

31.3.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

31.3.2. By Frequency

31.3.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

31.3.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

31.3.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

31.3.3. By Platform

31.3.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

31.3.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

31.3.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

31.3.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

31.3.4. By Application

31.3.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

31.3.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

31.3.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

31.3.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

31.3.5. By Accuracy

31.3.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

31.3.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

31.3.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

31.3.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

31.3.6. Country Level Analysis, Value (USD Million)

31.3.6.1. Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.3.6.2. Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.3.6.3. Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

31.3.6.4. Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32. Middle East & Africa Market

32.2. Overview

32.2.1. Market Value (USD Million), Current and Future Projections, 2026-2037

32.2.2. Increment $ Opportunity Assessment, 2026-2037

32.2.3. Year-on-Year Growth Forecast (%)

32.3. Segmentation (USD Million), 2026-2037, By

32.3.1. By Technology

32.3.1.1. Stand-Alone GPS Receivers, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.1.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.1.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.1.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.1.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.1.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.2. Integrated GPS Modules

32.3.1.2.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.2.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.2.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.2.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.2.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.3. Hybrid GPS Systems

32.3.1.3.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.3.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.3.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

32.3.1.3.4. Communication and Data Link

32.3.1.3.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

32.3.2. By Frequency

32.3.2.1. L1/L2, Market Value (USD Million), and CAGR, 2026-2037F

32.3.2.2. L1/L2/L5, Market Value (USD Million), and CAGR, 2026-2037F

32.3.2.3. L1/L2/L5/QZSS, Market Value (USD Million), and CAGR, 2026-2037F

32.3.3. By Platform

32.3.3.1. Airborne, Market Value (USD Million), and CAGR, 2026-2037F

32.3.3.2. Land-Based, Market Value (USD Million), and CAGR, 2026-2037F

32.3.3.3. Maritime, Market Value (USD Million), and CAGR, 2026-2037F

32.3.3.4. Space-Based, Market Value (USD Million), and CAGR, 2026-2037F

32.3.4. By Application

32.3.4.1. Navigation and Guidance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.4.2. Surveillance and Reconnaissance, Market Value (USD Million), and CAGR, 2026-2037F

32.3.4.3. Target Acquisition and Tracking, Market Value (USD Million), and CAGR, 2026-2037F

32.3.4.4. Communication and Data Link, Market Value (USD Million), and CAGR, 2026-2037F

32.3.4.5. Electronic Warfare, Market Value (USD Million), and CAGR, 2026-2037F

32.3.5. By Accuracy

32.3.5.1. Sub-Meter, Market Value (USD Million), and CAGR, 2026-2037F

32.3.5.2. Meter, Market Value (USD Million), and CAGR, 2026-2037F

32.3.5.3. Decimeter, Market Value (USD Million), and CAGR, 2026-2037F

32.3.5.4. Centimeter, Market Value (USD Million), and CAGR, 2026-2037F

32.3.6. Country Level Analysis, Value (USD Million)

32.3.6.1. Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.2. UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.3. Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.4. Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.5. Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.6. Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.7. South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

32.3.6.8. Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2037F

33. Global Economic Scenario

33.2. World Economic Outlook

34. About Research Nester

34.2. Our Global Clientele

34.3. We Serve Clients Across World

Military GPS Receiver Market Outlook:

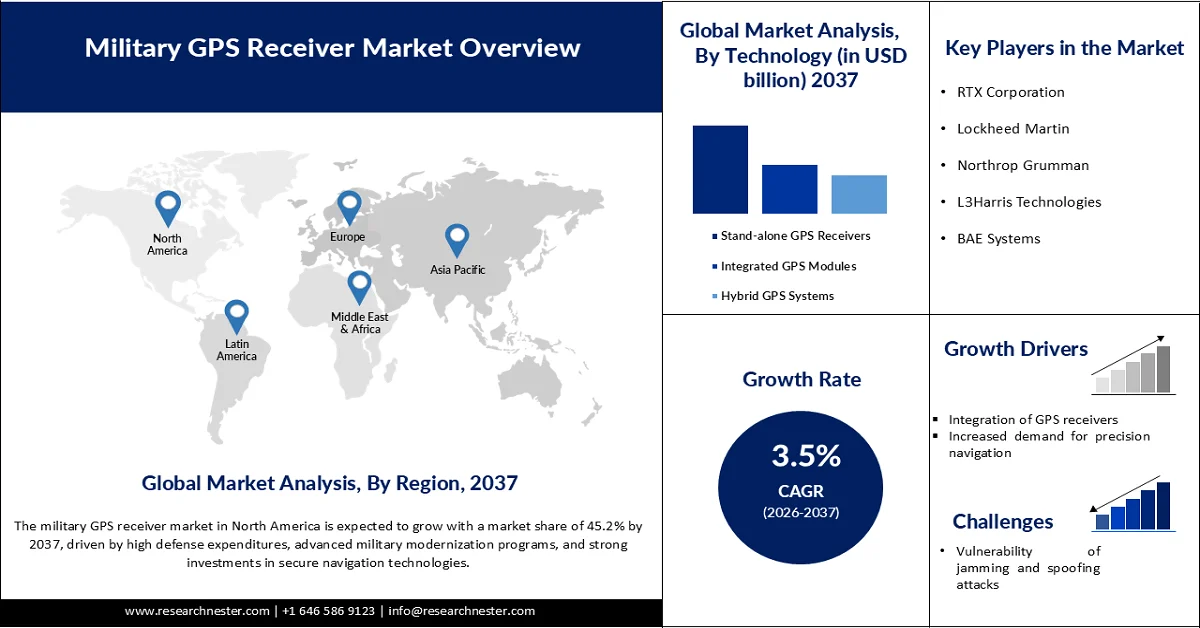

Military GPS Receiver Market size was valued at USD 2.03 billion in 2025 and is anticipated to surpass USD 3.07 billion by 2037, expanding at a CAGR of 3.5% during the forecast period, i.e., 2026 to 2037. In 2026, the industry size of military GPS receiver is estimated at USD 2.10 billion.

The primary growth driver of the global military GPS receiver market is the increasing demand for secure, jam-resistant navigation systems in contested environments. Modern conflicts have demonstrated the vulnerability of conventional GPS signals to jamming and spoofing, making resilient receivers essential for military operations. The U.S. Government Accountability Office (GAO) reported that GPS modernization programs, including the deployment of encrypted M-code signals, have faced delays of over 10 years, but remain critical to ensuring reliable positioning, navigation, and timing (PNT) capabilities for defense forces. Similarly, the RAND Corporation highlights that GPS resilience is vital for missile guidance, troop movement, and logistics, as adversaries increasingly target satellite-based navigation systems.

Another major driver is rising defense investment in GPS modernization. The GAO confirms that the U.S. Department of Defense has already invested over 20 years into GPS modernization, underscoring the scale and importance of secure GPS receivers for future military capability. The International Institute for Strategic Studies (IISS) notes that peer-state competition is pushing militaries to prioritize resilient technologies, including GPS receivers, as part of broader modernization strategies. Supporting this, global defense budgets continue to allocate billions toward navigation and timing systems, with GPS modernization identified as essentially too big to fail by GAO. These investments ensure that GPS receivers remain central to maintaining operational superiority in air, land, and naval domains.

Key Military GPS Receiver Market Insights Summary:

Regional Insights:

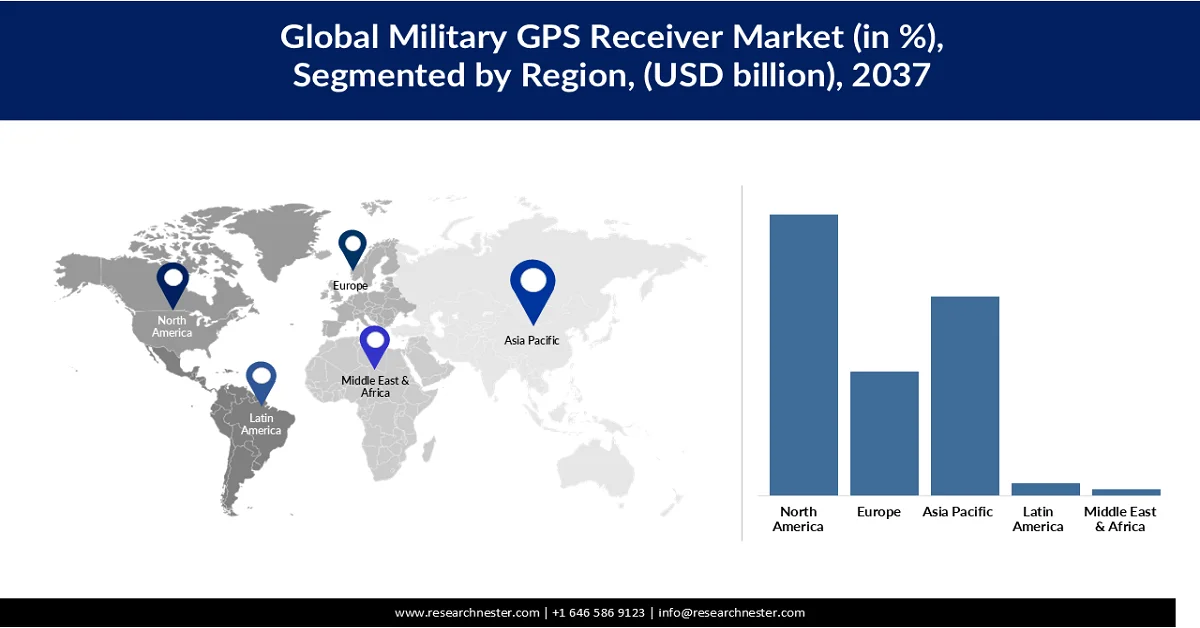

- North America military GPS receiver market is anticipated to command 45.2% share by 2037, propelled by high defense expenditures, advanced military modernization programs, and strong investments in secure navigation technologies.

- Asia Pacific is projected to witness the fastest expansion in the market throughout 2026-2037, stimulated by rising defense spending, regional security tensions, and rapid military modernization programs.

Segment Insights:

- The stand-alone segment is projected to capture 49.2% of the global military GPS receiver market by 2037, reinforced by its reliability, operational flexibility, and cost-effectiveness across defense applications worldwide.

- The L1/L2 frequency configuration segment is forecast to hold 51.3% share of the global market by 2037, fueled by its ability to deliver highly accurate, reliable, and resilient dual-frequency positioning capabilities for modern defense operations worldwide.

Key Growth Trends:

- Integration of GPS receivers

- Increased demand for precision navigation

Major Challenges:

- Vulnerability to jamming and spoofing attacks

- High development and procurement costs

Key Players: RTX Corporation (U.S.), Lockheed Martin (U.S.), Northrop Grumman (U.S.), L3Harris Technologies (U.S.), BAE Systems (UK), Thales Group (France), Honeywell International (U.S.), Collins Aerospace (U.S.), Safran Electronics & Defense (France), Elbit Systems (Israel), General Dynamics (U.S.), Leonardo S.p.A. (Italy), Israel Aerospace Industries (Israel), Garmin (Switzerland), Trimble Inc. (U.S.).

Global Military GPS Receiver Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.03 billion

- 2026 Market Size: USD 2.10 billion

- Projected Market Size: USD 3.07 billion by 2037

- Growth Forecasts: 3.5% CAGR (2026–2037)

Key Regional Dynamics:

- Largest Region: North America (45.2% Share by 2037)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Russia, India, United Kingdom

- Emerging Countries: Japan, South Korea, Australia, Germany, France

Last updated on : 21 May, 2026

Military GPS Receiver Market - Growth Drivers and Challenges

Growth Drivers

- Integration of GPS receivers: Modern armed forces increasingly embed GPS receivers into aircraft, missiles, naval vessels, armored vehicles, drones, and soldier communication systems to support real-time positioning, navigation, and timing (PNT) operations. According to the U.S. GAO, the Department of Defence plans to integrate modernized M-code GPS technology into approximately 700 weapons systems, demonstrating the massive scale of military GPS deployment worldwide. The U.S. military has also maintained a constellation requirement of 24 M-code-capable satellites, with plans to expand further for higher accuracy and resilience. These large-scale integrations are essential for network-centric warfare, where multiple defence platforms must communicate and coordinate seamlessly in real time. As countries continue adopting interconnected battlefield systems, demand for secure and interoperable military GPS receivers is accelerating globally.

- Increased demand for precision navigation: Modern warfare depends heavily on precision-guided munitions, autonomous drones, surveillance systems, and coordinated troop deployment, all of which require highly accurate GPS-based navigation. The U.S. Department of Defence has been modernizing GPS technology for more than 20 years to introduce secure and jam-resistant M-code signals that improve battlefield accuracy and operational reliability. The Space Force currently operates more than 24 M-code-capable satellites to support secure military navigation and precision strike capabilities. Furthermore, the growing use of smart weapons and ISR (Intelligence, Surveillance, and Reconnaissance) platforms has significantly increased demand for anti-jamming and anti-spoofing GPS receivers. As nations focus on minimizing collateral damage and improving combat efficiency, investments in high-precision military GPS systems continue to rise steadily.

- Emerging markets and defense modernization: Countries such as India, China, South Korea, Saudi Arabia, and Brazil are increasing defense spending to upgrade military infrastructure with advanced navigation, surveillance, and electronic warfare systems. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached approximately USD 2.44 trillion in 2023, representing a 6.8% increase over the previous year, with Asia and the Middle East witnessing particularly strong defense growth. Governments are investing heavily in modern combat aircraft, naval fleets, missile systems, and unmanned systems that require highly secure GPS receivers for navigation and targeting. In parallel, GPS modernization itself remains a multibillion-dollar effort, involving next-generation satellites, control systems, and upgraded military receivers. Rising geopolitical tensions, border security concerns, and military digitization programs across developing nations are therefore creating strong demand for advanced and jam-resistant military GPS receivers in global defense markets.

Challenges

- Vulnerability to jamming and spoofing attacks: Military GPS systems operate through satellite-based radio signals that can be disrupted or manipulated by hostile electronic warfare systems. According to the U.S. Department of Homeland Security, GPS signals arriving at Earth are relatively weak and therefore susceptible to intentional interference. Adversaries such as Russia and China have significantly expanded electronic warfare capabilities designed to jam navigation systems during combat operations. These threats force defense organizations to invest heavily in anti-jam technologies, increasing overall system costs and deployment complexity.

- High development and procurement costs: Advanced military GPS receivers require encrypted M-code capability, anti-spoofing protection, ruggedized hardware, and secure integration with defense platforms, making them significantly more expensive than commercial GPS devices. Additionally, upgrading legacy military platforms with modern GPS technology often requires extensive system modifications and testing. These high procurement and maintenance costs can limit adoption among developing countries with constrained defense budgets, slowing overall military GPS receiver market expansion.

Military GPS Receiver Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2037 |

|

CAGR |

3.5% |

|

Base Year Market Size (2025) |

USD 2.03 billion |

|

Forecast Year Market Size (2037) |

USD 3.07 billion |

|

Regional Scope |

|

Military GPS Receiver Market Segmentation:

Technology Segment Analysis

The stand-alone segment is projected to account for 49.2% of the global military GPS receiver market by 2037, driven by its reliability, operational flexibility, and cost-effectiveness across defense applications worldwide. These receivers are extensively deployed in ground combat vehicles, handheld military communication devices, naval systems, and soldier navigation equipment, where accurate and independent positioning capabilities are critical. Their ability to function efficiently without requiring complex integration with broader defense networks makes them highly suitable for both modern and legacy military platforms operating in remote and challenging environments. Military organizations across North America, Europe, Asia-Pacific, and the Middle East continue to prefer stand-alone GPS receivers because of their rugged design, secure signal reception, and dependable performance under extreme battlefield conditions. In addition, the growing emphasis on precision navigation, troop mobility, mission coordination, and real-time situational awareness is further accelerating global demand for stand-alone military GPS receivers.

Frequency Segment Analysis

The L1/L2 frequency configuration segment is anticipated to account for 51.3% of the global military GPS receiver market by 2037, owing to its ability to deliver highly accurate, reliable, and resilient dual-frequency positioning capabilities for modern defense operations worldwide. The L1 frequency supports standard navigation and timing signals, while the L2 frequency enables correction of ionospheric errors, significantly improving positioning precision and signal stability in demanding operational environments. This enhanced accuracy is critical for mission-sensitive applications such as precision targeting, intelligence and surveillance missions, tactical troop movement, and navigation of advanced military platforms. In addition, L1/L2 GPS receivers provide stronger resistance to signal interference, jamming, and spoofing threats, making them highly effective in electronic warfare and contested battlefield conditions. Their compatibility with existing military infrastructure and ongoing GPS modernization programs across major defense economies further supports their widespread global adoption. As defense forces continue prioritizing secure and high-precision navigation technologies, demand for L1/L2 military GPS receivers is expected to grow steadily across international markets.

Platform Segment Analysis

The airborne platform segment is projected to account for a significant share of the global military GPS receiver market between 2026 and 2037, driven by its vital role in modern aerial defense and combat operations worldwide. Military aircraft such as fighter jets, surveillance and reconnaissance aircraft, unmanned aerial vehicles (UAVs), and transport helicopters rely heavily on advanced GPS receivers for accurate real-time positioning, navigation, targeting, and mission coordination. The rapid global expansion of drone warfare and autonomous aerial systems is further increasing demand for compact, lightweight, and high-performance GPS receivers that integrate efficiently with advanced avionics systems. In addition, airborne military platforms frequently operate in dynamic and electronically contested environments, creating a strong demand for GPS technologies with anti-jamming, anti-spoofing, and multi-constellation capabilities. Defense modernization initiatives across major economies, including North America, Europe, and Asia-Pacific, are also driving investments in next-generation air combat and surveillance systems equipped with secure navigation technologies. As global defense forces continue strengthening aerial intelligence, precision strike, and surveillance capabilities, the adoption of military GPS receivers in airborne platforms is expected to grow steadily.

Our in-depth analysis of the military GPS receiver market includes the following segments:

|

Segments |

Sub-segments |

|

Technology |

|

|

Frequency |

|

|

Platform |

|

|

Application |

|

|

Accuracy |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Military GPS Receiver Market - Regional Analysis

North America Market Insights

North America is expected to hold the largest share of 45.2% of the global military GPS receiver market by 2037, driven by high defense expenditures, advanced military modernization programs, and strong investments in secure navigation technologies. The region benefits from extensive deployment of GPS-enabled systems across air, land, naval, and space defense platforms. Ongoing upgrades to anti-jamming and M-code GPS technologies, along with increasing focus on electronic warfare and integrated battlefield communication systems, continue to support military GPS receiver market growth. In addition, the presence of major defense contractors and advanced satellite infrastructure strengthens North America’s leadership in military GPS innovation and deployment.

The U.S. is the leading contributor to the North American military GPS receiver market due to its extensive defense modernization efforts and leadership in global GPS infrastructure. According to the U.S. Department of Defense, USD 849.8 billion was requested for the Department of Defense for Fiscal Year 2025. The U.S. Space Force operates a constellation of 31 GPS satellites that provide positioning, navigation, and timing services worldwide. In addition, the U.S. Government Accountability Office reported that the GPS Next Generation Operational Control System (OCX) program’s total acquisition cost estimate increased to USD 7.6 billion. Strong investments in advanced combat aircraft, autonomous defense systems, and electronic warfare capabilities continue to increase demand for secure and anti-jamming military GPS receivers across the country.

Canada is experiencing steady growth in the military GPS receiver market as the country strengthens defense modernization and NATO interoperability initiatives. According to the Government of Canada – National Defence, Canada announced an investment of USD 8.1 billion over five years starting in 2024-25 to enhance defense readiness and military capabilities. The government also stated that defense spending is projected to rise to 1.76% of GDP by 2029-30 under its updated defense policy. Furthermore, the Canadian government plans to invest USD 73 billion over 20 years through its Our North, Strong and Free defense strategy to modernize military infrastructure and defense technologies. Rising procurement of advanced fighter aircraft, surveillance systems, and Arctic security equipment is expected to support increasing adoption of secure military GPS receivers across Canadian defense forces.

Asia Pacific Market Insights

The Asia Pacific military GPS receiver market is experiencing the fastest global growth due to rising defense spending, regional security tensions, and rapid military modernization programs. Countries such as China, India, Japan, South Korea, and Australia are investing heavily in secure, anti-jamming GNSS technologies for missiles, drones, naval systems, and armored vehicles. The increasing adoption of indigenous navigation systems is also accelerating demand for advanced military receivers. Growth is further supported by expanding electronic warfare capabilities and the need for precision-guided operations across the Indo-Pacific region.

China military GPS receiver market is growing rapidly due to heavy investments in defense modernization and its indigenous BeiDou Navigation Satellite System network. The People’s Liberation Army is increasingly deploying advanced anti-jamming and anti-spoofing GNSS receivers for missiles, drones, aircraft, and naval platforms. Asia-Pacific is currently the fastest-growing region for military GPS/GNSS systems, with China leading regional demand through precision-strike and network-centric warfare programs. The country is also pushing self-reliance by reducing dependence on the U.S. GPS and expanding BeiDou integration into military equipment. Growing geopolitical tensions in the Indo-Pacific are further accelerating procurement and R&D investments in secure navigation technologies.

India military GPS receiver market is expanding steadily as the country modernizes its armed forces and strengthens indigenous navigation capabilities through NavIC. Rising defense budgets and programs such as Atmanirbhar Bharat are driving demand for secure GNSS receivers across army, navy, and air force platforms. India is increasingly integrating NavIC-enabled systems into missiles, drones, vehicles, and battlefield communication networks to reduce dependence on foreign GPS services. Recent satellite launches and upgrades to the NavIC constellation are expected to improve reliability and encourage wider military adoption. Border security concerns with China and Pakistan, along with the need for precision-guided systems, continue to support long-term military GPS receiver market growth.

Europe Market Insights

Europe military GPS receiver market is growing steadily as NATO countries increase defense budgets and strengthen battlefield interoperability amid ongoing geopolitical tensions. Nations such as Germany, France, and the UK are upgrading military platforms with dual-mode GPS and Galileo-enabled receivers that offer secure and jam-resistant navigation. The Russia-Ukraine conflict has accelerated investments in electronic warfare protection, encrypted positioning systems, and resilient communication networks. European defense modernization programs and rising procurement of advanced land, air, and naval systems are expected to continue driving long-term market expansion across the region.

Germany military GPS receiver market is growing steadily due to the country’s large-scale Bundeswehr modernization programs and increased defense spending after the Russia-Ukraine conflict. The government is investing heavily in digital battlefield systems, armored vehicles, air-defense platforms, and secure navigation technologies integrated with NATO standards. Demand is rising for anti-jamming, encrypted, and multi-constellation GNSS receivers compatible with GPS and Europe’s Galileo system. Germany’s focus on network-centric warfare and indigenous European defense capabilities is also encouraging domestic production and R&D in advanced military navigation systems.

The UK military GPS receiver market is expanding through ongoing defense modernization initiatives across the Royal Navy, British Army, and Royal Air Force. Rising investments in autonomous systems, drones, precision-guided weapons, and electronic warfare resilience are driving demand for secure GPS/GNSS receivers with anti-spoofing capabilities. The UK is also emphasizing sovereign and NATO-interoperable navigation technologies, especially after Brexit, which has increased focus on domestic defense technology development. Integration of GPS with Galileo and advanced battlefield communication systems is expected to further strengthen long-term military GPS receiver market growth in the country.

Key Military GPS Receiver Market Players:

- RTX Corporation (U.S.)

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- L3Harris Technologies (U.S.)

- BAE Systems (UK)

- Thales Group (France)

- Honeywell International (U.S.)

- Collins Aerospace (U.S.)

- Safran Electronics & Defense (France)

- Elbit Systems (Israel)

- General Dynamics (U.S.)

- Leonardo S.p.A. (Italy)

- Israel Aerospace Industries (Israel)

- Garmin (Switzerland)

- Trimble Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- RTX Corporation is a major defense technology company providing advanced military GPS and navigation solutions for missile systems, aircraft, and battlefield platforms. The company focuses heavily on anti-jamming and secure positioning technologies to support modern combat operations. Its defense divisions work closely with the U.S. Department of Defense and allied nations on precision-guided weapon programs. Continuous R&D investments and integration of electronic warfare capabilities strengthen its position in the global military GPS receiver market.

- Lockheed Martin plays a significant role in the military GPS receiver market through its advanced defense electronics and navigation systems. The company integrates secure GPS technologies into fighter aircraft, missile defense systems, naval platforms, and space programs. Its strong portfolio in precision-strike and network-centric warfare solutions supports growing global defense demand. Long-term government contracts and modernization programs continue to drive its market expansion.

- Northrop Grumman develops high-performance military navigation and positioning systems designed for secure and resilient battlefield operations. The company specializes in anti-spoofing GPS receivers and advanced avionics for unmanned systems, aircraft, and defense platforms. It benefits from rising investments in electronic warfare and autonomous military technologies worldwide. Strong partnerships with defense agencies and continuous innovation reinforce its competitive market position.

- Thales Group is a leading European defense company offering military-grade GNSS and secure navigation systems for air, land, and naval applications. The company emphasizes cybersecurity, encrypted positioning, and interoperability with NATO and Galileo-based systems. Its advanced solutions support European defense modernization and growing demand for resilient battlefield communications. Expansion in electronic warfare and defense electronics has further strengthened its global presence.

- BAE Systems provides advanced military GPS receivers and navigation technologies integrated into combat vehicles, aircraft, and maritime defense systems. The company focuses on secure and jam-resistant positioning solutions to enhance operational effectiveness in contested environments. Increasing investments in defense modernization and electronic warfare programs support its business growth globally. Its collaborations with NATO allies and government defense agencies continue to expand its market opportunities.

Below is the list of the key players operating in the global military GPS receiver market:

Key players in the military GPS receiver market are driving growth through continuous investments in anti-jamming, anti-spoofing, and encrypted navigation technologies to improve battlefield reliability. Companies are developing multi-constellation GNSS receivers compatible with GPS, Galileo, BeiDou, and NavIC systems for higher positioning accuracy and operational resilience. Strategic partnerships with defense agencies and military modernization programs are also accelerating product deployment across air, land, and naval platforms. In addition, the rising demand for autonomous drones, precision-guided weapons, and network-centric warfare systems is spurring innovation in compact, ruggedized receivers. Leading firms are further expanding their military GPS receiver market presence through defense contracts, R&D initiatives, and integration of AI and electronic warfare protection capabilities into navigation systems.

Corporate Landscape of the Global Military GPS Receiver Market:

Recent Developments

- In April 2026, Lockheed Martin and the U.S. United States Space Force further enhanced the Global Positioning System (GPS) constellation to its highest level of capability with the successful launch of GPS III Space Vehicle 10 (SV10), the final spacecraft in the GPS III series. The SV10 satellite introduces important improvements in accuracy and resilience for the GPS network, including an experimental optical crosslink payload. This payload is designed to demonstrate in-space optical communication between satellites, enabling them to exchange data directly without relying solely on ground stations. By enabling satellites to communicate with one another in orbit, these optical crosslinks are expected to significantly strengthen the constellation’s operational resilience, improve data-flow efficiency, and support the next generation of more robust and interconnected GPS capabilities.

- Report ID: 7134

- Published Date: May 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Military GPS Receiver Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.