Global Maritime Internet of Things Market

- An Outline of the Global Maritime Internet of Things Market

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Maritime Internet of Things

- Recent News

- Regional Demand

- Global Maritime Internet of Things by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: Maritime Internet of Things Demand Landscape

- Global Maritime Internet of Things Demand Trends Driven by Safety, Vessel Management and Technological Advancements (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the Maritime Internet of Things Porter Five Forces

- PESTLE

- Comparative Positioning

- Maritime Internet of Things– Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- Business Profile of Key Enterprise

- ABB Marine & Ports

- Kongsberg Gruppen

- ORBCOMM

- Marine Traffic

- Navis

- Inmarsat

- Maersk Line

- Business Profile of Key Enterprise

- Global Maritime Internet of Things Market Outlook

- Market Overview

- Market Revenue by Value (USD Million), Volume (Million Tons), and Compound Annual Growth Rate (CAGR)

- Global Segmentation Maritime Internet of Things Analysis (2026-2036)

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Regional Synopsis, Value (USD Million), 2026-2036

- North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Market Overview

- North America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036,

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- U.S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Europe Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036,

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Asia Pacific Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036,

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zeeland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Latin America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036,

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

Global Maritime Internet of Things Market

- An Outline of the Global Maritime Internet of Things Market

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Maritime Internet of Things

- Recent News

- Regional Demand

- Global Maritime Internet of Things by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: Maritime Internet of Things Demand Landscape

- Global Maritime Internet of Things Demand Trends Driven by Safety, Vessel Management and Technological Advancements (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the Maritime Internet of Things Porter Five Forces

- PESTLE

- Comparative Positioning

- Maritime Internet of Things– Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- Business Profile of Key Enterprise

- ABB Marine & Ports

- Kongsberg Gruppen

- ORBCOMM

- Marine Traffic

- Navis

- Inmarsat

- Maersk Line

- Business Profile of Key Enterprise

- Global Maritime Internet of Things Market Outlook

- Market Overview

- Market Revenue by Value (USD Million), Volume (Million Tons), and Compound Annual Growth Rate (CAGR)

- Global Segmentation Maritime Internet of Things Analysis (2026-2036)

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Regional Synopsis, Value (USD Million), 2026-2036

- North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Market Overview

- North America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

-

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- U.S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Europe Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

-

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Asia Pacific Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

-

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zeeland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Latin America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036, By

-

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

-

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- Service, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Moel

- On-board, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud based, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Satellite and Communication, Market Value (USD Million), and CAGR, 2026-2036F

- Wireless Sensor Network, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud Computing, Market Value (USD Million), and CAGR, 2026-2036F

- Machine Learning & Analytics, Market Value (USD Million), and CAGR, 2026-2036F

- Blockchain Technology, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Vessel Tracking, Market Value (USD Million), and CAGR, 2026-2036F

- Predictive Maintenance, Market Value (USD Million), and CAGR, 2026-2036F

- Fleet Management, Market Value (USD Million), and CAGR, 2026-2036F

- Inventory Management, Market Value (USD Million), and CAGR, 2026-2036F

- Safety & Surveillance, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- By Component

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

Maritime Internet of Things Market Outlook:

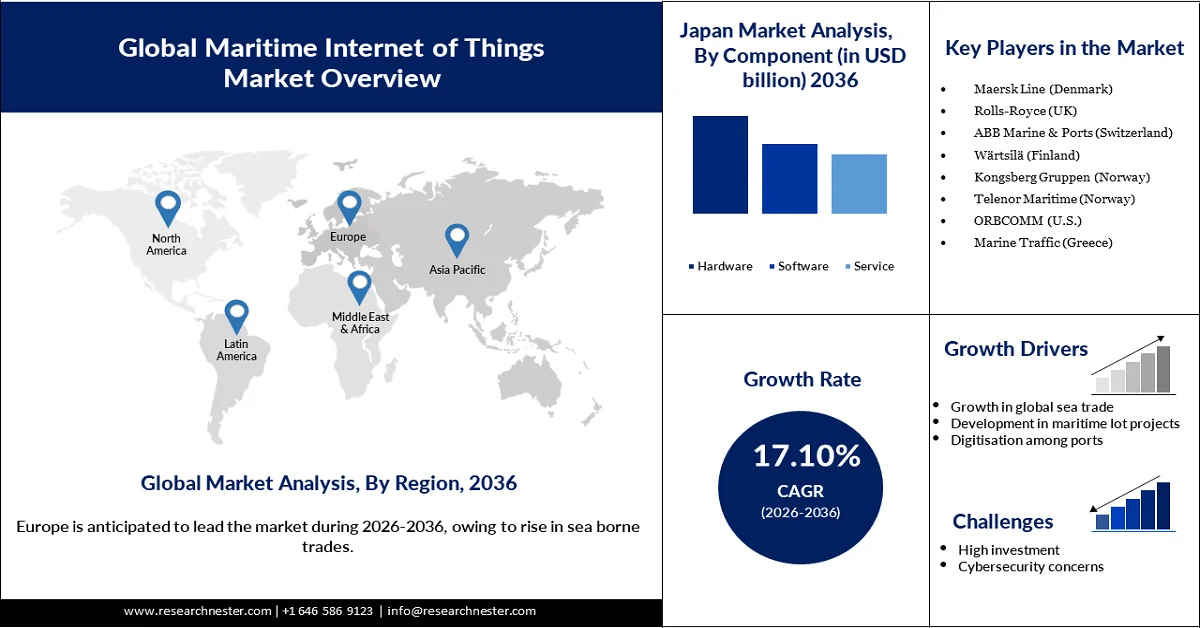

Maritime Internet Of Things (IoT) Market is valued at USD 799.53 billion in 2025 and is expected to grow to USD 3.62 trillion by 2036, registering a CAGR of 17.10%. In 2026, the industry size of maritime Internet of Things is estimated at USD 933.56 billion.

Tourism has increased significantly over time, particularly with the growth of cruise travel, which has expanded passenger numbers and seasonal itineraries across global destinations. According to the Cruise Lines International Association (CLIA), cruise travel passenger volumes are forecast to reach around 37.7 million in 2025, reflecting ongoing growth in cruise tourism demand worldwide. The importance of IoT in maritime logistics and safety is underscored by data on global and regional trade flows. In 2024, maritime transport accounted for 75.6 % of the physical volume of all European Union imports and 73.7 % of exports, illustrating how critical sea transport remains for global commerce, where IoT plays an increasingly central role in tracking, monitoring, and operational decision-making.

Advances in IoT and satellite communications have also enabled more effective management of navigation and safety systems at sea. Modern IoT platforms integrate real-time GPS tracking with advanced sensors to monitor environmental factors such as vessel speed, route deviations, temperature, and humidity, all of which are critical for safe navigation and cargo integrity across long sea voyages. Furthermore, the incorporation of AI and data analytics with IoT systems enhances decision-making capabilities for maritime operators by enabling predictive maintenance, automated alerts, and performance forecasting, key features in modern maritime operations that help reduce downtime and support route optimization.

Key Marine Internet of Things (IoT) Market Insights Summary:

Regional Highlights:

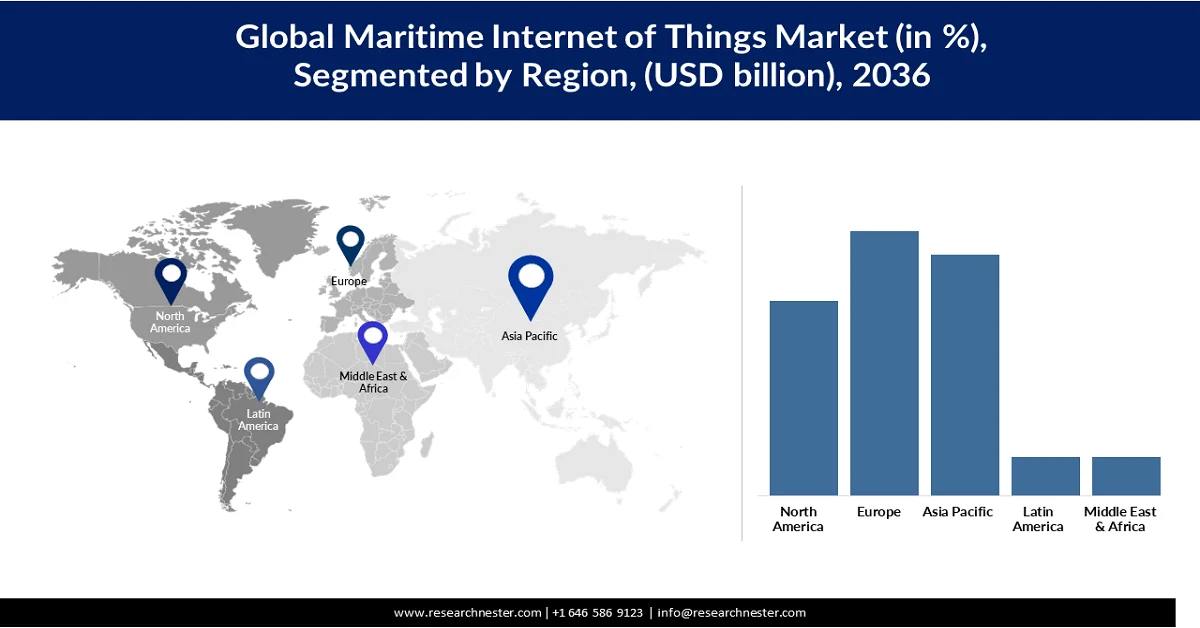

- Europe maritime internet of things market is anticipated to command a 34% share by 2036, impelled by expanding intra-EU trade volumes and accelerating development of autonomous ships reliant on real-time monitoring and smart port initiatives.

- Asia Pacific is forecast to capture a 31% share by 2036, propelled by large-scale cargo shipments, manufacturing hub dominance, and strong governmental push toward real-time tracking and smart port systems.

Segment Insights:

- The hardware segment in the maritime internet of things market is projected to account for a 48% share by 2036, driven by extensive deployment of sensors, chips, and satellite-dependent communication systems requiring continuous servicing and upgrades.

- The vessel tracking segment is expected to dominate by 2036, fueled by rising sea-borne trade traffic and growing demand for real-time vessel positioning to enhance safety and operational efficiency.

Key Growth Trends:

- Growth in global sea trade

- Development in marine IoT projects

Major Challenges:

- High investment

- Cybersecurity concerns

Key Players: Maersk Line (Denmark), Rolls-Royce (UK), ABB Marine & Ports (Switzerland), Wärtsilä (Finland), Kongsberg Gruppen (Norway), Telenor Maritime (Norway), ORBCOMM (U.S.), Marine Traffic (Greece), Navis (U.S.), Inmarsat (UK).

Global Marine Internet of Things (IoT) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 799.53 billion

- 2026 Market Size: USD 933.56 billion

- Projected Market Size: USD 3.62 trillion by 2036

- Growth Forecasts: 17.10% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Europe (34% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, Brazil, Indonesia, Vietnam, Mexico

Last updated on : 16 February, 2026

Maritime Internet of Things Market - Growth Drivers and Challenges

Growth Driver

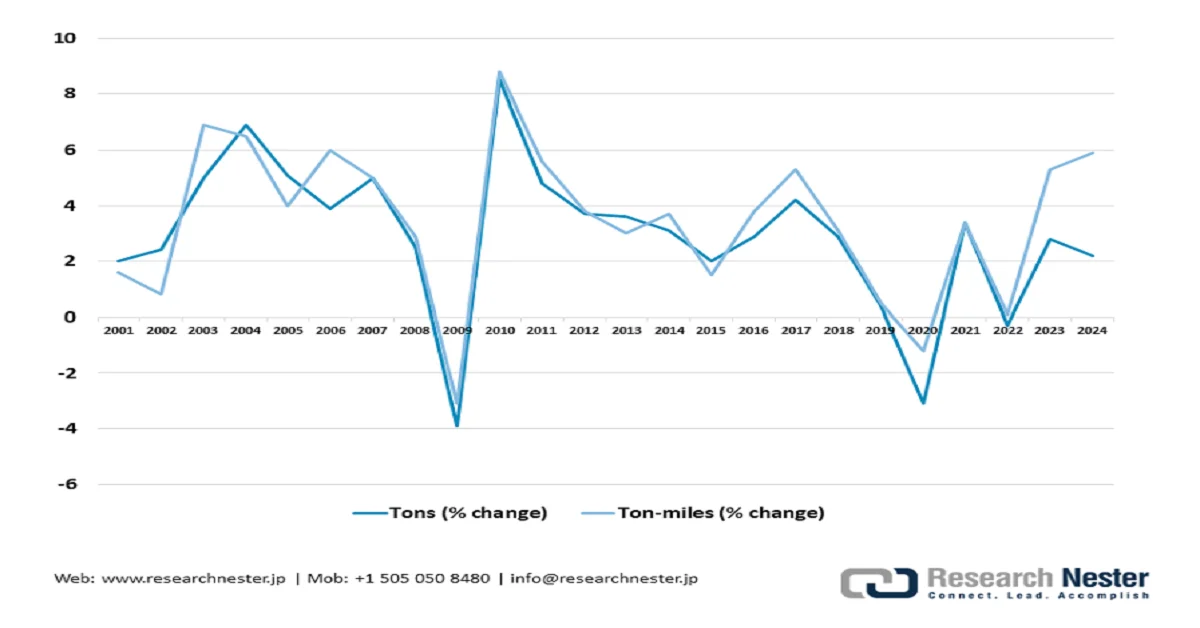

- Growth in global sea trade: Rising volumes and longer distances in global seaborne trade are increasing operational complexity across the shipping industry, directly driving demand for maritime Internet of Things (IoT) solutions. According to UNCTAD, global seaborne trade expanded by 2.2% in 2024, while trade measured in ton-miles grew by 5.9%, reflecting widespread vessel rerouting and longer voyages. Maritime transport still accounts for over 80% of global merchandise trade, making real-time monitoring and data visibility essential for safe and efficient operations. Extended sailing distances raise fuel costs, emissions, and navigational risks, encouraging ship operators to deploy IoT-enabled systems for route optimization, engine monitoring, and predictive maintenance. UNCTAD further notes that ton-mile growth is occurring at nearly three times the pace of volume growth, amplifying the need for digital tracking and analytics. As shipping routes lengthen and trade networks expand, maritime IoT adoption becomes critical to maintaining efficiency, safety, and supply-chain resilience.

Growth in Maritime trade, tons and ton-miles, annual percentage change, 2001-2024

- Development in marine IoT projects: Governments are accelerating investment for IoT and cloud computing in major ports, aimed towards enhancing efficiency in terms of visibility and maintenance, propelling the growth of the maritime internet of things (IoT) market. The initiative is supporting the development of sustainable port operations and minimizing operational expenses. According to the U.S. Department of Transportation, the Infrastructure Investment and Jobs Act provided an aid funding of 2.25 billion for the PIDP program over a five-year tenure (2022-2026). The funding assures the development of the important ports, including digitization to ensure effective vessel management

- Digitalization among the ports: Countries worldwide are accelerating the digitization of ports to enhance operational safety, efficiency, and trade effectiveness through the deployment of cloud computing and AI-driven analytics. To strengthen cross-sector connectivity, transparency, and ethical trade practices, ports are rapidly adopting digital platforms and automated systems, supported by significant government investments. As global trade volumes rise, effective traffic and port-call management has become increasingly critical, prompting the use of automation to reduce reliance on manual labor while improving safety for port workers and seafarers. Automated systems enable real-time monitoring, predictive maintenance, and optimized vessel scheduling, which help minimize congestion and operational risks. This shift is reflected in the United States, where a 2024 Government Accountability Office (GAO) report confirms that all 10 major U.S. ports have implemented some form of automation technology to enhance port operations. Collectively, these digital advancements are reshaping port infrastructure and supporting safer, more resilient global maritime trade.

Challenges

- High investment: The integration of IoT technologies within ports requires substantial capital investment, which often acts as a barrier to widespread adoption. This challenge is more pronounced in mid-tier and small ports, where lower cargo volumes and limited financial resources reduce the incentive to invest in advanced digital infrastructure. Many smaller ports operate with aging or insufficient infrastructure that does not meet the technical requirements for IoT deployment, such as high-capacity connectivity, sensor networks, and data platforms. Additionally, small-scale operations struggle to justify the return on investment for sophisticated automation and monitoring systems. As a result, these structural and financial constraints slow IoT implementation and hinder overall maritime internet of things (IoT) market growth.

- Cybersecurity concerns: The integration of IoT and other smart systems in maritime operations raises significant cybersecurity concerns, as vulnerabilities can lead to data breaches, system manipulation, and misuse of sensitive information. Cyber threats targeting connected devices and networks can disrupt critical port and vessel operations, slowing the adoption of maritime IoT solutions. Because IoT platforms often control multiple interconnected systems such as navigation, cargo handling, and traffic management, unauthorized access can result in serious operational and safety risks. These concerns make ports and maritime operators cautious about deploying advanced digital technologies. Consequently, heightened cybersecurity risks remain a key restraint on the widespread adoption of maritime IoT across the maritime internet of things (IoT) market.

Marine Internet of Things (IoT) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2036 |

|

CAGR |

17.10% |

|

Base Year Market Size (2025) |

USD 799.53 billion |

|

Forecast Year Market Size (2036) |

USD 3.62 trillion |

|

Regional Scope |

|

Maritime Internet of Things Market Segmentation:

Component Segment Analysis

The hardware segment is expected to hold a maritime internet of things (IoT) market share of 48% by the end of 2036, owing to the use of different components, such as sensors and chips, with the systems that support the features and functionality of maritime IoT systems. Ships and vessels use communication systems that are dependent on satellites that exchange messages and commands from shore. These maritime IoT systems engage multiple hardware components, which demand frequent servicing and upgrades, enhancing the core focus on the segment. The growing IoT capabilities and the utilisation of hardware systems within the IoT systems are supporting the growth of the segment.

Application Segment Analysis

The vessel tracking segment will hold the largest share by the end of 2036 due to increased traffic in sea-borne trade and passenger carriages. IoT is utilized by ships and vessels to enhance safety and reduce the risk of collisions in poor visibility. Maritime IoT systems are engaged by ports to determine the real-time positioning of the vessels, understanding the need for logistical solutions, enhancing the availability of cranes and other support equipment needed to load and unload the materials in an effective way. Other segments, such as predictive maintenance is also expected to hold a significant share in the maritime internet of things (IoT) market owing to easy access to maintenance needs and reducing operational costs.

Technology Segment Analysis

The satellite and communication technology is anticipated to hold a significant share by 45% by the end of 2036 because of rising traffic propelled by the influx of trade among countries. Satellite communication serves as a key aspect in maritime operations. The growth of IoT has significantly helped in enhancing satellite and communication technologies, propelling the expansion of the maritime internet of things (IoT) market. The integration of IoT in ships supports remote communication, enhancing cross-communication between other vessels and maintaining a safer distance from them. The cloud computing segment will also hold a significant share in the future because of growing predictive analysis among the ports.

Our in-depth analysis of the global IoT market includes the following segments:

|

Segments |

Subsegments |

|

Component |

|

|

Deployment Model |

|

|

Technology |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Maritime Internet of Things Market - Regional Analysis

Europe Market Insights

The region is expected to hold a share of 34% by the end of 2036, owing to the large-scale export and import of products and increased trade between EU countries. The growing development in autonomous ships and vessels is propelling the maritime internet of things (IoT) market expansion, as such vessels largely depend on real-time monitoring and tracking. The high demand for trade within the region is pushing the government to develop smart initiatives that will help predict maintenance of the ports to ensure seamless availability of ports for large vessels.

The UK is playing a pivotal role in advancing autonomous shipping technologies, which is driving the adoption of maritime Internet of Things (IoT) systems. The IMO is actively promoting the development of autonomous ships, with the UK contributing significantly through research, pilot projects, and smart port initiatives. Ports across the UK are implementing IoT-enabled systems for real-time vessel tracking, predictive maintenance, and traffic management, improving operational efficiency and safety.

In Germany, the Port of Hamburg serves as a model for IoT integration in maritime operations. The port uses IoT sensors and AI-driven analytics to monitor vessel traffic, optimize resource utilization, and predict maintenance needs, enhancing both efficiency and safety. Germany’s ports handled over 267.8 million tons of cargo in 2023, highlighting the scale of operations and the critical role of digital technologies in managing traffic and logistics. These smart systems also help reduce congestion, improve environmental performance, and maintain smooth operations for large-scale maritime trade, reinforcing Germany’s leadership in the adoption of maritime IoT technologies across Europe.

Asia Pacific Markets Insights

Asia Pacific is expected to hold a share of 31% owing to the development in ports and ships, where a large volume of cargo is shipped in various regions. Moreover, certain countries in the region are considered the hubs of manufacturing, where a large number of shipments move from one place to another. The adoption of maritime IoT within the region is helping the ports to seamlessly manage the traffic and enhance safety among the vessels. The continuous encouragement from the governments to employ smart systems to monitor the real-time tracking and environmental impact has further enhanced the scope of the maritime internet of things (IoT) market in the region.

China is recognized as one of the largest manufacturing hubs across the world because of its low-cost manufacturing capabilities. According to China Power, China contributed to nearly 28% of the global manufacturing in 2023, giving rise to increased trade volumes. The increasing trade and manufacturing capabilities of China are propelling the growth of the maritime Internet of Things. The growth of 5G communication in China is propelling the integration of IoT ecosystems, enhancing remote communication between ships and offshore control rooms.

India is rapidly expanding its trade and business across various countries, fueling the demand for maritime IoT systems. Certain Indian ports, such as Mumbai and Chennai, are strategically located, which supports seamless cargo movements between Middle Eastern countries, enhancing the dependency. The large volume of ship movements through Indian ports is demanding the use of IoT systems to improve navigation and gain real-time tracking of ships. Maritime IoT also helps in keeping the movement of vessels safe and secure, leading to higher adoption, especially in ports with high demand.

North America Market Insights

The region is expected to hold a share of 25% owing to increased vessel and trade activity. The IoT market is highly developed in terms of technological advancements, which is propelling development within the maritime Internet of Things. The region is also accelerating in terms of research and development, where new technologies and smart sensors are being researched that improve communication among the vessels and ships. Manufacturing facilities across the region are ramping up, where critical and complex minerals are exported to different countries, which increases the reliance on sea trade, propelling the maritime internet of things (IoT) market expansion.

In the U.S., some of the world’s largest ports have experienced significant growth in trade and logistics, creating a strong demand for IoT-enabled operations. The Port of Los Angeles, for example, leads in automation initiatives aimed at reducing vessel wait times and improving cargo handling efficiency. The integration of data-driven analytics and blockchain technologies enhances shipment tracking and operational transparency, reinforcing the utilization of IoT systems across U.S. ports and supporting more efficient and secure maritime logistics.

The Port of Vancouver in Canada is one of the largest ports in North America, handling substantial volumes of cargo and passenger traffic, which drives the adoption of maritime Internet of Things (IoT) systems. These technologies enable predictive maintenance, optimize operational efficiency, and reduce overall expenses. The port also employs advanced surveillance and monitoring systems in control rooms to assess port availability and estimate vessel waiting times, ensuring smoother operations. Rising transportation volumes and the increasing demand for next-generation surveillance solutions are further accelerating the adoption of maritime IoT technologies.

Key Maritime Internet of Things Market Players:

- Maersk Line (Denmark)

- Rolls-Royce (UK)

- ABB Marine & Ports (Switzerland)

- Wärtsilä (Finland)

- Kongsberg Gruppen (Norway)

- Telenor Maritime (Norway)

- ORBCOMM (U.S.)

- Marine Traffic (Greece)

- Navis (U.S.)

- Inmarsat (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Kongsberg Gruppen, a leading producer of maritime technology and connected solutions, which focuses on autonomous ships and real-time data analytics for vessels and maritime transport. The organization is also experiencing a push towards IoT-based developments for maritime surveillance and communication.

- Telenor Maritime focuses on connectivity solutions for maritime products and IoT applications for vessels and ships. Telenor is also a leading producer of satellite communication for fleet management and remote monitoring of the ships with a global presence.

- ORBCOMM, a global leader in satellite communication and IoT solutions for remote tracking of ships and other assets. It develops systems for efficient cargo management, where the temperature and humidity of the cargo. The products developed by the business are aimed at improving the vessel performance and predicting maintenance needs

- Marine Traffic, a leader in maritime analytics and vessel tracking, provides real-time analysis of ship movements along with location coordinates. The systems are also designed to facilitate traffic management and enhance operational efficiency within the ports

Below is the list of the key players operating in the global Maritime Internet of Things market:

The players operating in the global maritime Internet of Things market are expected to face intense competition during the forecast timeline. The IoT market is associated with both established key players and new entrants. However, the IoT market is moderately fragmented. New entrants impose immense competition for the existing players, prohibiting them from acquiring the majority of the revenue share. Specialised manufacturers maintain a competitive landscape in the IoT market. Key players in the market are significantly supported by the governments for research and innovation.

Competitive Landscape of the Maritime Internet of Things Market:

Recent Developments

- In June 2025, Maersk Lines launched its new cargo tracking solutions named OneWireless, which can seamlessly track the vessel and enhance the monitoring. The system has already been installed in more than 450 owned vessels, which can support various technologies.

- In May 2024, Telenor Maritime launched 5G installation in an offshore setting, enhancing connectivity in the North Sea. The integration will employ 700MHz and 2100MHz to ensure high-speed connectivity.

- Report ID: 3692

- Published Date: Feb 16, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.