Investment Management Software Market Outlook:

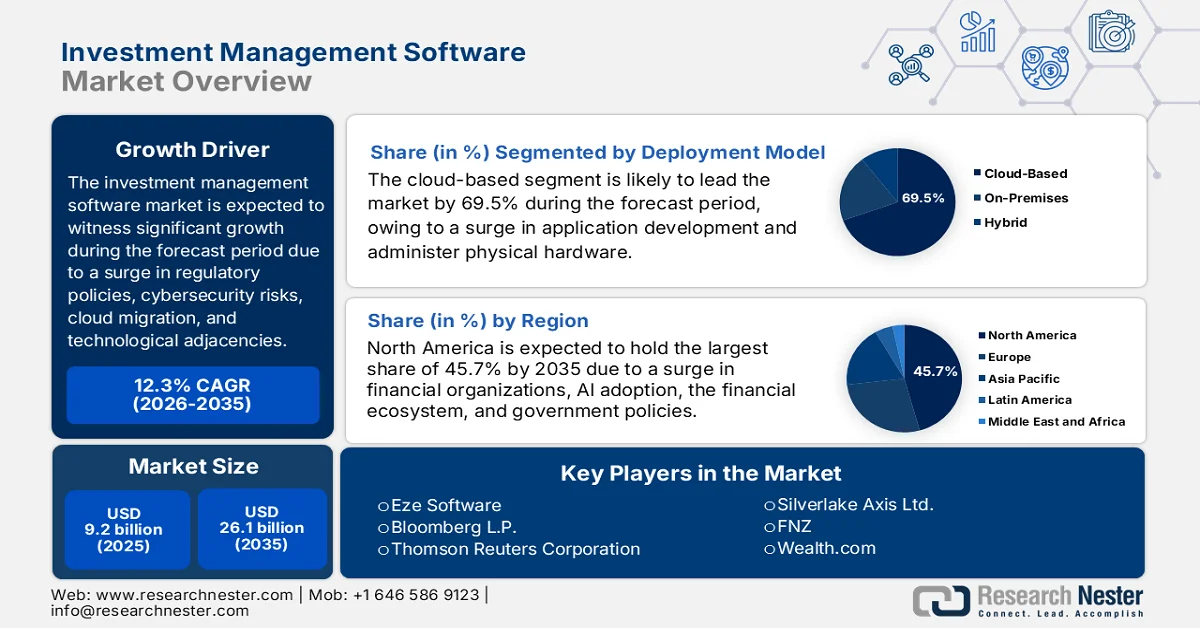

Investment Management Software Market size was valued at over USD 9.2 billion in 2025 and is projected to reach USD 26.1 billion by the end of 2035, with a CAGR of 12.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of investment management software is estimated at USD 10.3 billion.

The worldwide investment management software market is being readily shaped by the core dynamics of cloud migration, cybersecurity concerns, and regulatory pressure, along with behavioral transitions among technological adjacencies and end users for repurposing structural and financial changes across investment organizations. According to official statistics published by the Dev Pro Insights in January 2023, AWS is significantly leading with 34% of the cloud service industry, which is followed by 21% of Azure and 11% of GCP. Besides, Tencent Cloud, Oracle, IBM, and Alibaba are suitable players geographically and service-wise. Moreover, with more than 94% of organizations utilizing cloud computing, and the worldwide public cloud expenditure’s predicted growth of 20.7% as of 2023 for USD 591 billion, is ultimately the silver lining for digitalized transformation. Therefore, based on organizational attribution and the expected growth of cloud services, the market is gradually expanding globally.

Furthermore, the decentralized finance protocol integration, voice-activated command interfaces, white-labelling for niche micro-communities, predictive cash flow forecasting for private clients, and the social trading feed adoption are a few trends that are bolstering the investment management software market worldwide. As stated in an article published by NLM in June 2023, a decline in cash flow measures to 1 unit has the ability to increase organizational performance by an estimated 6.8% for accounts receivables turning days (ARTD), 0.03% for inventory turning days (ITD), and 7.2% for accounts payable turning days (APTD). In addition, a 1 unit decline in cash conversion cycle can enhance firm performance by roughly 3.8%. Besides, 66.6% of China-based data sets are significantly characterized by a large-scale average ratio of working capital to fixed capital, which is positively impacting the investment management software market development.

Key Investment Management Software Market Insights Summary:

Regional Highlights:

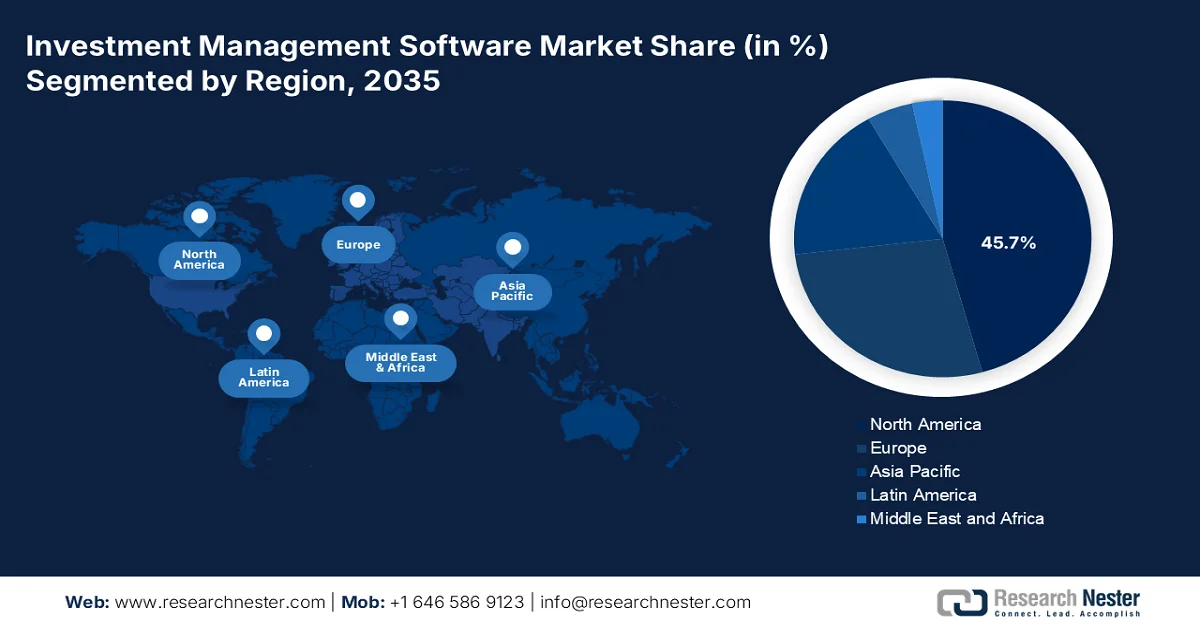

- North America investment management software market is projected to command a 45.7% share by 2035, bolstered by rising adoption of AI-driven analytics and expanding fintech usage

- Asia Pacific is expected to witness the fastest growth through 2026-2035, fueled by accelerating digital transformation and increasing retail investor participation

Segment Insights:

- Cloud-based sub-segment of investment management software market is anticipated to capture a 69.5% share by 2035, propelled by scalable infrastructure enabling seamless application development without physical hardware dependency

- Large enterprises segment is set to hold the second-largest share over 2026-2035, driven by the need to manage complex multi-system architectures and achieve enterprise-wide standardization

Key Growth Trends:

- Expansion in direct indexing platforms

- Rise in outcome-based investment frameworks

Major Challenges:

- Cybersecurity threats and data privacy risks

- Talent scarcity and implementation expertise

Key Players: SS&C Technologies Holdings, Inc. (U.S.), BlackRock, Inc. (Aladdin) (U.S.), SimCorp A/S (Denmark), Charles River Development (U.S.), Temenos AG (Switzerland), FIS Global (U.S.), Broadridge Financial Solutions, Inc. (U.S.), Murex SAS (France), Finastra (UK), Iress Limited (Australia), SunGard (now part of FIS) (U.S.), Misys (UK), Eze Software (U.S.), Bloomberg L.P. (U.S.), Thomson Reuters Corporation (U.S.), Infosys Limited (India), Tata Consultancy Services Limited (India), Hitachi, Ltd. (Japan), Samsung SDS Co., Ltd. (South Korea), Silverlake Axis Ltd. (Malaysia), FNZ (UK), Wealth.com (U.S.), Advent International (U.S.), Wolters Kluwer Tax and Accounting (Netherlands).

Global Investment Management Software Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.2 billion

- 2026 Market Size: USD 10.3 billion

- Projected Market Size: USD 26.1 billion by 2035

- Growth Forecasts: 12.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Japan, Germany

- Emerging Countries: India, South Korea, Singapore, Australia, Canada

Last updated on : 21 April, 2026

Investment Management Software Market - Growth Drivers and Challenges

Growth Drivers

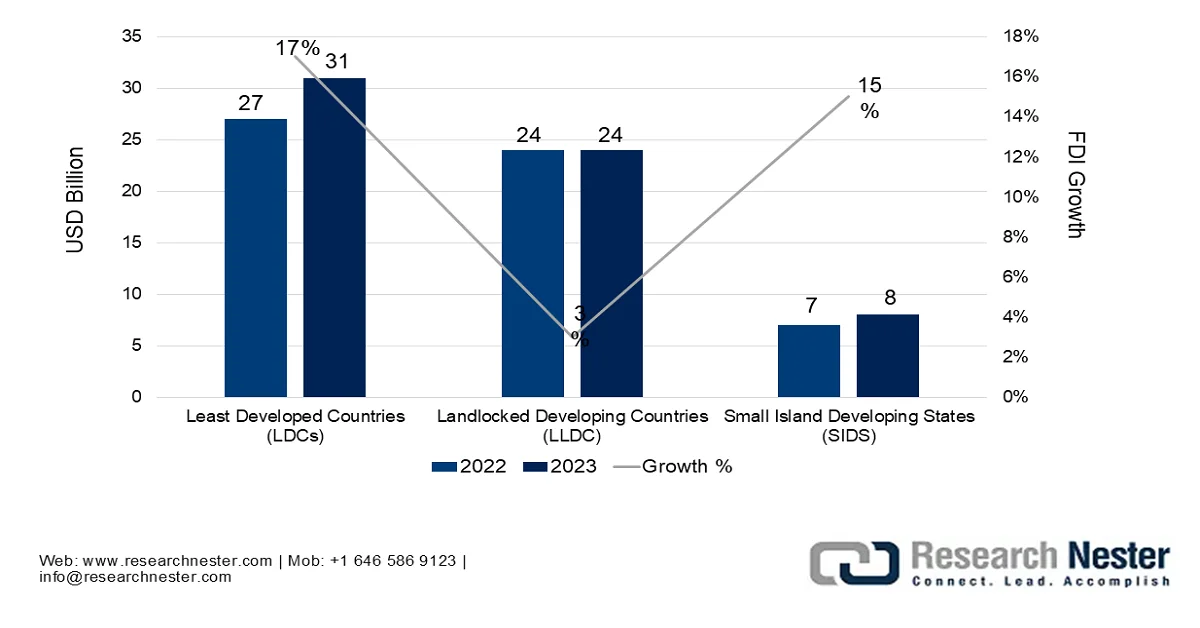

- Expansion in direct indexing platforms: Brokers increasingly provide direct indexing, based on which investors tend to own individual stocks rather than ensuring tax-loss harvesting, which is driving the investment management software market globally. According to official statistics published by the UN Trade and Development (UNCTAD) in June 2024, there has been an increase in foreign direct investment (FDI) across developed nations by USD 31 billion, which is 2.4% of worldwide flows. Likewise, small-scale island developing states and landlocked developing nations also witnessed an increase, with FDI effectively remaining concentrated. Therefore, with this FDI flow increase across weak countries is highly responsible for bolstering the market growth and expansion globally.

FDI Growth in Structural Vulnerable, Small, and Weak Nations, 2022-2023

Source: UN Trade and Development (UNCTAD)

- Rise in outcome-based investment frameworks: Global institutional investors are readily transitioning from benchmark-based performance to absolute outcome targets, including funding a specific pension liability in 2045, which is also responsible for bolstering the investment management software industry worldwide. As stated in an article published by the Invest India Government in April 2026, there is a huge surge in investment opportunities in India, since it is the 4th largest economy, along with an estimated gross domestic product (GDP) growth for 6.6% between 2025 and 2026. In addition, the strong FDI accounts for 69.1% of overall inflows, with a massive boom in exports constituting USD 433 billion during 2023 and 2024, thereby denoting a huge growth opportunity for the investment management software market.

- Demand for cross-border tax optimization: Worldwide investors readily manage accounts across different tax jurisdictions, and currently demand effective software that automatically improves asset location, thereby positively fueling the investment management software market growth. As per an article published by Finance Research Letters in August 2024, in terms of research and development tax incentives, the U.S. comprises more than USD 11.7 billion in funding, while competitors, including China, have almost USD 6.7 billion. Besides, 33 of 38 OECD-based nations offered preferred tax treatment to business research and development spending at the central and subnational government levels as of 2023, thereby making it suitable for fueling the market expansion globally.

Challenges

- Cybersecurity threats and data privacy risks: The investment management software service has become increasingly cloud-based and interconnected with external data sources, trading venues, and banking APIs, based on which the attack surface for malicious actors has expanded exponentially. These platforms store the most sensitive financial data imaginable: client net worth, proprietary trading algorithms, unannounced merger arbitrage positions, and custodial credentials. A single breach can trigger cascading market manipulation, identity theft, and irreversible reputational damage. The industry faces sophisticated threats, including ransomware targeting backup systems, supply chain attacks through third-party integrations, and insider threats from disgruntled employees with legitimate access, thus negatively impacting the investment management software market globally.

- Talent scarcity and implementation expertise: The successful deployment and ongoing optimization of the sophisticated investment management software market requires a rare hybrid professional: someone who deeply understands both financial instrument mechanics, from derivatives pricing to collateral management, and modern software engineering practices, including cloud infrastructure, data science, and API integration. This talent pool is extraordinarily shallow and concentrated in a handful of global financial hubs. Even when institutions secure budget approval for new software, they face months-long delays in finding implementation partners or internal staff who can configure the platform correctly without introducing logical errors.

Investment Management Software Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.3% |

|

Base Year Market Size (2025) |

USD 9.2 billion |

|

Forecast Year Market Size (2035) |

USD 26.1 billion |

|

Regional Scope |

|

Investment Management Software Market Segmentation:

Deployment Model Segment Analysis

The cloud-based sub-segment, part of the deployment model segment, is anticipated to garner the largest share of 69.5% in the investment management software market by the end of 2035. The sub-segment’s uplift is primarily due to readily available facilities that enable increased application creation and deployment without the need to manage physical hardware. According to official statistics published by the World Data Group in 2026, of the total data generated, less than 1% is analyzed and utilized, leading to a missed opportunity to effectively capitalize on data for economic and social growth. Besides, as stated by an article published by the National Science Foundation in August 2022, the Broadband Equity, Access, and Deployment Program generously authorized USD 42.4 billion for digitalized infrastructure investment by prioritizing unserved and underserved regions, thus proliferating the sub-segment’s growth.

End user Segment Analysis

Based on the end user, the large enterprises segment is projected to hold the second-largest share in the investment management software market during the forecast period. The segment’s growth is effectively driven by its pivotal role as the most demanding and structurally complex category of end-users within the investment management software market. These organizations, global asset managers, multi-national banks, pension funds, and insurance companies, operate with sprawling organizational hierarchies, multiple investment desks across different time zones, and portfolios that span every conceivable asset class. Their primary roadblock is not the lack of capital for technology investment, but rather the immense difficulty of achieving system-wide standardization. A single large enterprise may run dozens of legacy systems acquired through mergers, each with its own data schema, reporting logic, and operational workflow.

Investment Style Segment Analysis

By the end of the stipulated timeline, the active management sub-segment, which is part of the investment style segment, is expected to account for the third-largest share in the investment management software market. The sub-segment’s development is highly propelled by its utilization by managers for modifying the associated risks and adopting the appropriate strategy to reduce volatility in the banking portfolio. As per a data report published by the UN Trade and Development (UNCTAD) in February 2024, in terms of FDI, there has been a surge in the flow, particularly in Europe, from negative USD 106 billion as of 2022 to USD 16 billion, owing to volatility in conduit economies. In addition, FDI-based inflows in other parts of the region were diminished by 14%. Besides, Greenfield-specific project announcements across developing nations eventually increased by more than 1,000, thereby denoting an optimistic outlook for the market growth.

Our in-depth analysis of the investment management software market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Model |

|

|

End user |

|

|

Investment Style |

|

|

Functionality |

|

|

Asset Class |

|

|

Organization Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Investment Management Software Market - Regional Analysis

North America Market Insights

North America in the investment management software market is anticipated to garner the highest share of 45.7% by the end of 2035. The market’s upliftment in the region is highly attributed to the existence of major financial institutions, an increase in the adoption of AI-based analytics, strict regulatory compliance requirements, a strong financial ecosystem, the incorporation of machine learning, and generous spending on cybersecurity solutions. According to official statistics published by the Federal Deposit Insurance Corporation (FDIC) in October 2024, more than half of the population in the region utilizes fintech to effectively manage their regular finances, accounting for 48%, with a rise in services from 42% to 44%. Additionally, domestic consumers also demonstrated a 10% year-over-year (YoY) increase in fintech applications, thus driving the market growth.

The investment management software market in the U.S. is growing significantly, owing to the domestic Securities and Exchange Commission (SEC) outsourcing rule push for registered investment advisers, state-level fiduciary rule fragmentation, and the defined contribution plan rollover automation. As stated in an article published by the U.S. Bureau of Economic Analysis (BEA) in January 2026, the difference between domestic residents’ international financial liabilities and assets accounted for -USD 27.6 trillion by the end of 2025. In addition, total assets in the country were worth USD 41.2 trillion, while liabilities were valued at USD 68.8 trillion. Besides, there has been an increase in domestic assets by USD 1.7 trillion to an overall USD 41.2 trillion by the end of the third quarter of 2025, which indicates market expansion.

Selected Size Asset Type in the U.S., 2025

|

Components |

Outstanding (USD Billion) |

Growth % |

Average Yearly Growth % |

|

Public Equities |

74,410 |

15.6 |

8.9 |

|

Residential Real Estate |

61,101 |

1.4 |

6.2 |

|

Treasury Securities |

28,518 |

6.0 |

8.3 |

|

Commercial Real Estate |

20,524 |

-5.6 |

5.4 |

|

Investment-Grade Corporate Bonds |

8,156 |

4.3 |

7.8 |

|

Farmland |

3,558 |

4.2 |

5.6 |

|

High-Yield and Unrated Corporate Bonds |

1,724 |

5.2 |

6.1 |

|

Leveraged Loans |

1,494 |

7.3 |

12.2 |

Source: Federal Reserve Government

The presence of CRM2 report evolution, the client relationship model, the implementation of the open banking framework, the indigenous wealth management, and the land claims settlement administration are a few trends that are fueling the investment management software market in Canada. As per a data report published by the Fraser Institute Organization in November 2025, the banking system in the country comprises 6 large-scale banks that effectively control an estimated 90% of assets that have mutated from being engaged in commercial and corporate business. Based on this mutation, business lending in the nation readily represented 30% to 60% of banks’ balance sheets. Meanwhile, household lending has become steadily important, gradually rising from 20% to 40% and 60% in recent years, thereby making it suitable for proliferating the market growth.

APAC Market Insights

The Asia Pacific in the investment management software market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is primarily fueled by rapid digital transformation, a rise in household wealth, an increase in retail investor participation across emerging countries, a surge in systematic investment plans, the robo-advisory adoption, and governmental strategies. According to official statistics published by the International Monetary Fund (IMF) in November 2025, in terms of urbanization, the population dynamics in the Philippines and India are predicted to expand by over 15%, while other countries, such as Korea and Japan, by over 10%. Besides, as per the January 2023 JCER Organization article, there has been an increase in the per capita household wealth in China from 49.5% to 61.7%, along with the wealth share of the top 10% wealthiest households upsurged from 37.2% to 48.4%, which is fueling the market development.

Change in Wealth Share in Asia-Pacific-Based Households, 2023

|

Countries |

Wealth Share |

|

China |

48.4% |

|

India |

62.1% |

|

New Zealand |

52.9% |

|

Australia |

46.5% |

|

Korea |

41.5% |

|

Japan |

34.3% |

Source: JCER Organization

The investment management software market in China is gaining increased traction, owing to rapid and massive expansion in household wealth base, an increase in capital-economy participation from the middle-class population, robust governmental strategies for promoting financial industry modernization, and suitable reforms for encouraging digital transformation of financial services. As stated in an article published by the State Council Information Office in October 2025, the banking and insurance industry in the country offered USD 24 trillion in the latest funding for the real economy. Besides, suitable loans for science and technology research and development, along with long-lasting loans for infrastructure and manufacturing, grew by a yearly average of 27.2%, 10.1%, and 21.7%, respectively, thereby driving the market expansion and exposure.

The aspects of implementing mutual fund policies, the government’s Digital India campaign has escalated digital transformations, the rapid extension of financial literacy, an increase in retail investor participation, and the robust economic performance are a few trends that are responsible for fueling the investment management software market development in India. As per an article published by the IBEF Organization in April 2026, the mutual fund industry in the country for assets rose to 12.2% to USD 790 billion, which further added USD 85.7 billion as of 2026. Besides, in March 2026, inflows into proactively managed equity mutual funds surged to USD 4.3 billion, reaching the highest level since July 2025, from USD 2.7 billion in February. Therefore, with this continuous development in mutual fund services, there is a huge growth opportunity for the market in the country.

Europe Market Insights

Europe in the investment management software market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by a strict regulatory framework, cross-border asset management complexities, the existence of the majority of global financial infrastructures, increased demand for compliance automation, an escalation in cloud-driven deployments, and the incorporation of AI-based risk analytics. According to official statistics published by the Europe Commission in 2026, 75% of businesses in the region are expected to utilize cloud-edge technologies for their operational activities. Based on this projection, 10,000 climate-neutral and highly secured edge nodes are to be deployed across the overall region to enable increased data transfers and offer necessary connectivity, thus boosting the market expansion.

The investment management software market in Germany is gaining increased exposure, owing to the existence of the decentralized asset management landscape, the increased emphasis on IT security, outsourcing oversight, risk management systems, compulsory shift from LIBOR to risk-free rates, and real-time risk aggregation mandates. Based on government estimates published by the ITA in August 2025, the cybersecurity expenditure in the country significantly reached more than USD 10 billion as of 2024. Meanwhile, 46% of domestic organizations are presently utilizing cloud computing technology for conducting their business processes, while more 11% are on the verge of implementing. Moreover, 53% of companies increased their investment in artificial intelligence as of 2025, and 55% of these adopted the technology by more than 40%, thereby enhancing the investment management software market development in the country.

The concentration of more than FCA-authorized asset managers managing assets, the ongoing existence of worldwide software vendors’ regional headquarters, aggressive regulatory modernization agenda, and focus on technology modernization are factors that are fueling the investment management software market in the UK. As per an article published by the UK Government in March 2023, the country has successfully seized the science and technology sector, with increased application in fintech facilities, demonstrating approximately 11% of the worldwide industry share, and readily attracting USD 11.6 billion in investments. In addition, this significantly represents a 217% increase in investment opportunities in the overall country. Therefore, with the growth in the fintech industry, along with generous investments, the market is gradually expanding in the country.

Key Investment Management Software Market Players:

- SS&C Technologies Holdings, Inc. (U.S.)

- BlackRock, Inc. (Aladdin) (U.S.)

- SimCorp A/S (Denmark)

- Charles River Development (U.S.)

- Temenos AG (Switzerland)

- FIS Global (U.S.)

- Broadridge Financial Solutions, Inc. (U.S.)

- Murex SAS (France)

- Finastra (UK)

- Iress Limited (Australia)

- SunGard (now part of FIS) (U.S.)

- Misys (UK)

- Eze Software (U.S.)

- Bloomberg L.P. (U.S.)

- Thomson Reuters Corporation (U.S.)

- Infosys Limited (India)

- Tata Consultancy Services Limited (India)

- Hitachi, Ltd. (Japan)

- Samsung SDS Co., Ltd. (South Korea)

- Silverlake Axis Ltd. (Malaysia)

- FNZ (UK)

- Wealth.com (U.S.)

- Advent International (U.S.)

- Wolters Kluwer Tax and Accounting (Netherlands)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SS&C Technologies Holdings, Inc. has established itself as a dominant force in the investment management software market through an aggressive acquisition strategy that has absorbed numerous competing platforms and service providers. The company offers a vertically integrated suite spanning front-to-back office operations, making it a preferred partner for asset managers seeking to outsource entire workflows rather than just deploy software.

- BlackRock, Inc. (Aladdin) began as an internal risk management tool but has evolved into one of the most widely adopted investment management ecosystems across institutional investors globally. The platform is unique in that its provider is also the world's largest asset manager, creating a powerful feedback loop where real-world portfolio experience continuously shapes software development.

- SimCorp A/S is recognized as a European powerhouse in investment management software, particularly strong among pension funds, insurance companies, and sovereign wealth funds requiring sophisticated front-to-back capabilities. The company has maintained its competitive edge by focusing on deep functional specialization rather than broad diversification, particularly in investment accounting and performance measurement modules.

- Charles River Development has built its reputation on providing an open, cloud-native investment management platform that prioritizes seamless interoperability with third-party data providers, execution venues, and custodians. The company, now a subsidiary of State Street Corporation, benefits from deep integration with one of the world's largest custodial banks, offering clients a uniquely unified data and operations workflow.

- Temenos AG brings its extensive banking software heritage to the investment management space, offering solutions designed specifically for wealth managers and private banks rather than institutional asset managers. The Swiss-based company leverages its headquarters in a global private banking hub to maintain close regulatory and operational alignment with the needs of family offices and high-net-worth wealth advisory firms.

Here is a list of key players operating in the global investment management software market:

The worldwide investment management software market is highly competitive, characterized by a few dominant players controlling significant market share alongside numerous specialized niche providers. Moreover, notable firms are aggressively pursuing strategic initiatives centered on cloud migration, artificial intelligence integration, and strategic acquisitions to consolidate capabilities. Besides, SS&C Technologies and BlackRock's Aladdin platform continue expanding through acquisitions of smaller fintech firms. SimCorp and Temenos are investing heavily in SaaS-based delivery models to capture mid-tier asset managers. Moreover, in December 2025, FNZ effectively launched the AI-Powered Investment Firm, which is a landmark global study, for revealing the speed and scale at which artificial intelligence is readily transforming the global asset and wealth management industry, thus driving the investment management software industry.

Corporate Landscape of the Investment Management Software Market:

Recent Developments

- In April 2026, Wealth.com successfully raised USD 65 million in an oversubscribed Series B round through participation with investors, such as Dynasty Financial Partners, The K Fund, Pruven Capital, and Titanium Ventures, for developing the most innovative central intelligence layer for modernized wealth management.

- In December 2025, Advent International initiated a tactical investment in Skyone through Advent’s Latin American Private Equity Fund VII, which manages USD 2 billion of committed capital in Brazil.

- In October 2025, Wolters Kluwer Tax and Accounting released a future-ready accountant report to effectively highlight notable trends in the global tax and accounting sector by drawing insights from more than 2,700 professionals globally.

- Report ID: 8521

- Published Date: Apr 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.