Inverter Systems Market Outlook:

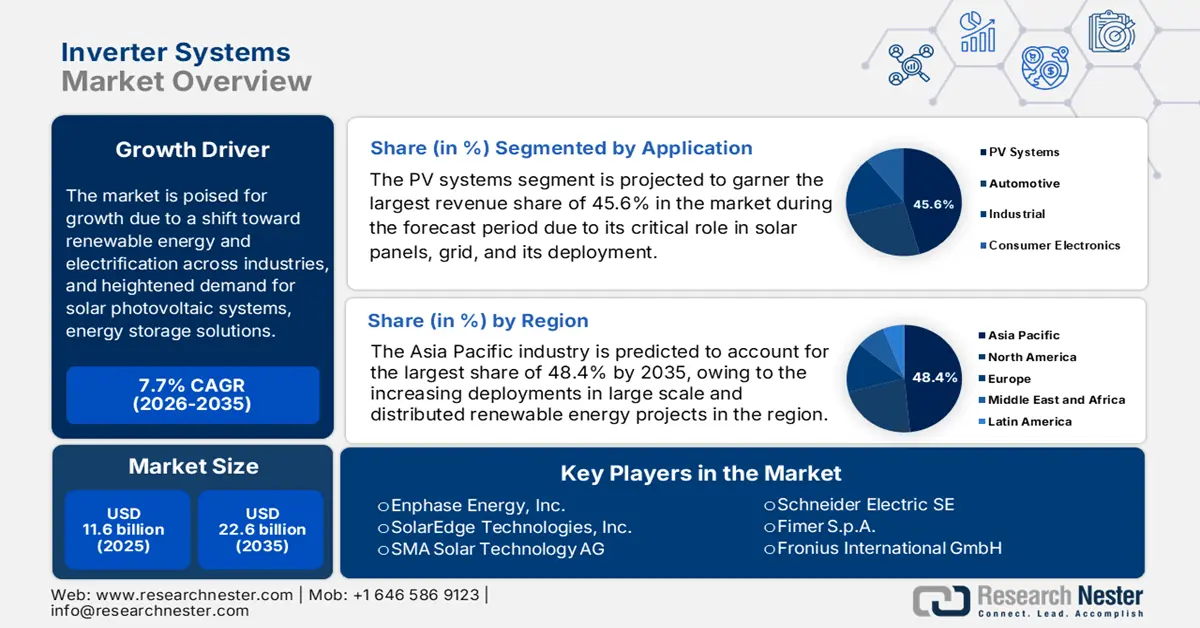

Inverter Systems Market size was valued at USD 11.6 billion in 2025 and is projected to reach USD 22.6 billion by the end of 2035, rising at a CAGR of 7.7% during the forecast period, i.e., 2026 - 2035. In 2026, the industry size of inverter systems is assessed at USD 12.4 billion.

The global inverter systems market is poised for tremendous growth facilitated by a shift toward renewable energy and electrification across industries, coupled with the heightened demand for solar photovoltaic systems, energy storage solutions, and efficient power management in industrial and commercial applications. Also, the photovoltaic solar installations and their integration with energy storage and grid infrastructure are propelling steady growth in this sector. As of the NREL report May 2025, there has been a historic surge in global solar photovoltaic installations in 2023, wherein China led deployment and the U.S. grabbed the second-largest share, adding 32-40 GWdc of PV capacity. It also stated that global PV shipments doubled from 2022, reaching 564 GW, whereas the U.S. domestic production remained modest at around 7 GW, with imports rising sharply to 55.6 GWdc, hence reflecting the rapid expansion of solar infrastructure.

U.S. Solar Manufacturing Growth Indicators Influencing the Inverter Industry

|

Metric |

Details / Values |

Time Period |

|

Shipments by the top 10 module manufacturers |

226 GW (+40% year-over-year) |

H1 2024 |

|

U.S. PV module production |

4.2 GW (+75% YoY); ~50% thin-film, ~50% c-Si |

H1 2024 |

|

Added U.S. solar manufacturing capacity |

>95 GW total (including 42 GW new module capacity) |

Since the IRA passage |

|

U.S. c-Si production ramp-up |

Expected to begin increasing |

H2 2024 |

|

IRS 48D investment tax credit |

25% credit for domestic ingot and wafer producers |

Announced Oct 22, 2024 |

Source: Energy.gov

Furthermore, the aspect of accelerating cost reductions, policy incentives, and expanded deployment of solar technologies is readily driving business in the inverter systems market, stimulating both domestic manufacturing and global trade. World Energy in August 2025 revealed that the country’s MNRE has issued draft guidelines mandating rooftop solar inverters for 30 GW of systems to connect to national servers, ensuring grid stability, cybersecurity, and data-driven deployment. It also stated that the policy focuses on vendor-neutral protocols, M2M SIMs for secure communication, and BIS certification with a minimum 50% local content, thereby promoting domestic manufacturing and reducing dependency on imported finished inverters. In addition, phased rollout with both technical and financial support is recommended to help manufacturers and installers adapt, positively impacting inverter systems market growth.

Key Inverter Systems Market Insights Summary:

Regional Highlights:

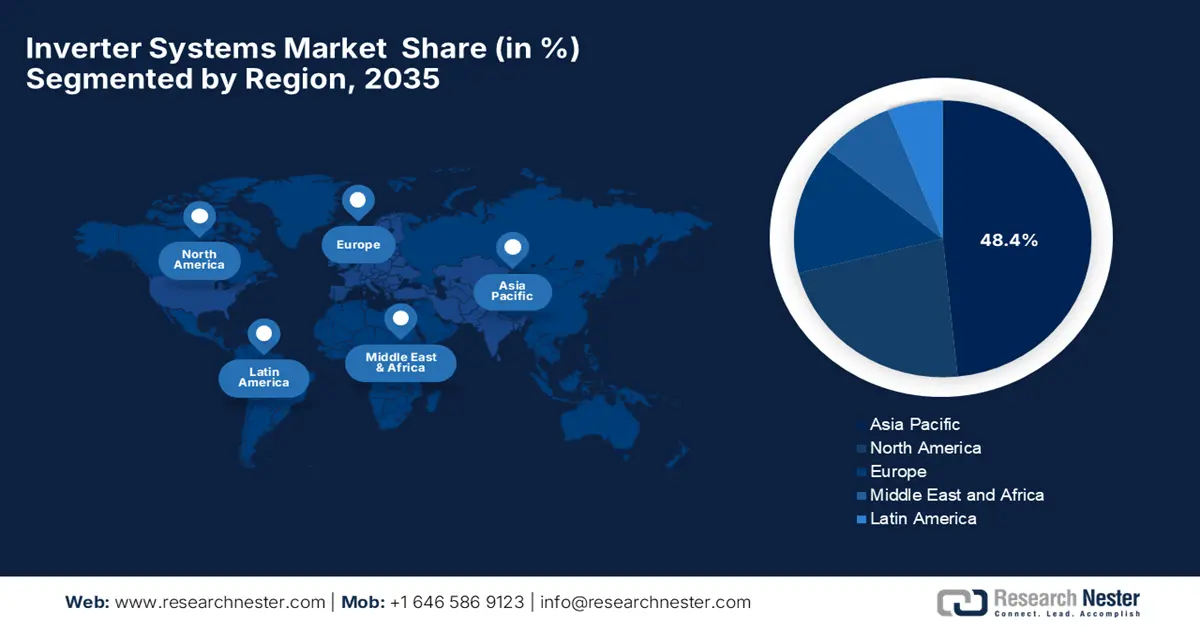

- By 2035, the Asia Pacific region is projected to command a 48.4% share in the inverter systems market, its lead being reinforced by accelerating deployments across both distributed and utility-scale renewable energy projects.

- North America is anticipated to secure a substantial share of the market by 2035, its progress being influenced by expanding solar PV adoption, rising energy-storage integration, and growing demand for advanced smart inverter capabilities.

Segment Insights:

- The PV systems segment in the inverter systems market is anticipated to hold a dominant 45.6% share during 2026–2035, its prominence being sustained by rising solar deployment across residential, commercial, and utility-scale projects.

- The solar inverters segment is expected to capture a 40.3% share by 2035, its expansion being influenced by declining PV costs, favorable incentives, and advancing high-capacity inverter technologies.

Key Growth Trends:

- Renewable energy deployment

- Government research, standardisation, and manufacturing support

Major Challenges:

- High initial costs and price pressure

- Supply chain constraints

Key Players: Enphase Energy, Inc., SolarEdge Technologies, Inc., SMA Solar Technology AG, Schneider Electric SE, Fimer S.p.A., Fronius International GmbH, TMEIC Corporation, Yaskawa Solectria Solar LLC, Delta Electronics, Inc., Luminous Power Technologies Pvt. Ltd., Servotech Renewable Power Systems Ltd., Q CELLS (Hanwha Q CELLS Co., Ltd.), KACO New Energy GmbH, ABB (ABB Power Grids), Schneider Electric (Malaysia).

Global Inverter Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 11.6 billion

- 2026 Market Size: USD 12.4 billion

- Projected Market Size: USD 22.6 billion by 2035

- Growth Forecasts: 7.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (48.4% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Australia, United Kingdom, Italy

Last updated on : 26 November, 2025

Inverter Systems Market - Growth Drivers and Challenges

Growth Drivers

- Renewable energy deployment: This, coupled with grid integration requirements, is prompting an extremely profitable business environment for the inverter systems market. Also, the rapid expansion of solar photovoltaic capacity, which necessitates the use of inverters to convert DC output into grid-compatible AC, is encouraging both national and international players to establish their footprint in this field. In this regard, the U.S. Department of Energy reported that the Essential Grid Operations from Solar project, led by NREL, Sandia, and PNNL under DOE funding, accelerates the development and adoption of reliability standards for inverter-based resources connecting to the U.S. power grid. It also stated that the project addresses system stability, interconnection, and performance verification, ensuring IBRs such as solar, wind, and battery storage operate reliably at scale.

Global Solar Capacity Additions in H1 2025 by Country/Region

|

Region/Country |

H1 2025 Installations (GW) |

YoY Change (%) |

Share of Global H1 2025 (%) |

|

World Total |

380 |

+64 |

100 |

|

China |

256 |

>100 |

67 |

|

Rest of World |

124 |

+15 |

33 |

|

India |

24 |

+49 |

6.3 |

|

U.S. |

21 |

+4 |

5.5 |

|

Other countries |

65 |

+22 |

17 |

Source: Ember Energy.Org

- Government research, standardisation, and manufacturing support: Government agencies are readily making investments in inverter technology R&D and establishing reliability standards, which support the growth of the inverter systems market. Testifying to this, the DOE reported that its SETO FY21 Systems Integration and Hardware Incubator program provides USD 45 million to advance solar technologies that enhance grid reliability, resilience, and U.S. manufacturing. Key initiatives include the UNIFI Consortium for grid-forming inverters, projects integrating behind-the-meter PV data into utility systems, and hardware incubators developing cost-effective components and advanced inverter-storage solutions. Therefore, these efforts accelerate large-scale deployment of domestic solar technologies, thereby supporting innovation, standards development, and secure, efficient grid integration.

- Policy-driven mandates: This is one of the important growth drivers for the inverter systems market. Governments across all nations are increasingly enforcing regulations that require smart, grid-compliant inverters for renewable energy integration. Hence, these measures encourage domestic production, reduce reliance on imported components, and stimulate investment in local R&D and manufacturing capacities. In this regard, SEIA reported that the U.S. Solar Investment Tax Credit is a federal incentive providing a 30% tax credit for residential, commercial, and utility-scale solar installations, driving more than 200-fold growth in the U.S. solar industry over the last two decades. It further underscored that the 2022 extension under the Inflation Reduction Act benefited energy storage, domestic manufacturing, and low-income area criteria, ensuring long-term market certainty.

Recent Global Inverter Launches and Innovations (2023-2024)

|

Year |

Company |

Product |

Key Features |

|

2024 |

SolarEdge Technologies |

TerraMax Inverter (SE330K) |

99% efficiency, 200% DC oversizing, supports 80-module strings, built-in safety, advanced MLPE, compatible with H1300 Power Optimizers |

|

2023 |

Voith Group |

Future Inverter Platform (FIP) |

High power density, compact (25 kg), integrated Drive Management Unit (DMU), cybersecurity compliance |

Source: Company Official Press Releases

Challenges

- High initial costs and price pressure: The inverter systems market faces severe difficulties in terms of high initial costs and pricing pressures as well. Despite the presence of declining component prices, the upfront costs of advanced inverter systems remain expensive, especially for small and medium-scale users. Also, the need for high-efficiency designs, quality semiconductors, and smart control features adds to manufacturing expenses, making it challenging for small-scale manufacturers. Simultaneously, there has been an intense competition among manufacturers, particularly from low-cost producers, which creates downward price pressure. Therefore, this imbalance between cost and pricing power limits profitability in this field, ultimately slowing down adoption in cost-sensitive emerging markets.

- Supply chain constraints: The inverter systems industry necessitates a proper supply of raw materials, which is posing a major hurdle hindering widespread adoption in this field. In this regard, the supply of semiconductors, control chips, and power electronic components is facing disruptions such as chip shortages or logistics delays, which can significantly affect production schedules. In addition, limited local manufacturing capacity in some regions makes firms reliant on imports, which often increases lead times and costs. Therefore, this is prompting the project developers to face uncertainty in deployment timelines, hence limiting the industry from witnessing rapid deployments in this field.

Inverter Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.7% |

|

Base Year Market Size (2025) |

USD 11.6 billion |

|

Forecast Year Market Size (2035) |

USD 22.6 billion |

|

Regional Scope |

|

Inverter Systems Market Segmentation:

Application Segment Analysis

Based on the application PV systems segment is projected to garner the largest revenue share of 45.6% in the inverter systems market during the forecast period. The subtype remains the critical gateway between the solar panels, grid, and its deployment is directly associated with installation rates of new solar projects. Also, the growth in both utility-scale and distributed generation solar installations ensures that PV systems application remains the primary driver since the new solar array, from residential rooftops to massive solar farms, necessitates at least one inverter. In addition, rising government incentives for solar adoption and continuous technological advancements in inverter efficiency further strengthen this segment’s dominance. Furthermore, the integration of smart monitoring features and hybrid energy storage compatibility is expected to sustain robust demand throughout the analyzed timeframe.

Type Segment Analysis

In terms of the type of solar inverters segment is likely to attain a significant share of 40.3% in the inverter systems market by the end of 2035. The worldwide energy transition and supportive government policies are the key factors driving the subsegment’s leadership. The declining costs of photovoltaic modules and financial incentives, such as tax credits, are making solar installations more accessible, fueling the need for inverters. GE Vernova, in September 2024, introduced a 6 MVA, 2000 Vdc utility-scale solar inverter, which is set for a multi-megawatt pilot installation in North America. The company also stated that this inverter increases power output by up to 30%, reducing costs and improving scalability for large solar farms. Furthermore, the inverter was developed in collaboration with Shoals Technologies Group and a PV module supplier, which marks a major step toward lowering the levelized cost of energy and accelerating renewable energy adoption, hence indicating a positive inverter systems market outlook.

Sales Channel Segment Analysis

Based on sales channel direct sales segment is projected to gain a lucrative share of 35.8% in the inverter systems market during the forecast duration. The growth of the segment is highly subject to technical complexity and the high value of commercial and utility-scale inverter systems. Also, the large-scale projects necessitate customized engineering, integration services, and long-term maintenance contracts that are best facilitated through a direct manufacturer relationship. In addition, these channels allow technical support, streamlined logistics for large orders, and the negotiation of service-level agreements, which are highly essential for the operational reliability of major energy and industrial projects, making it the preferred model. Furthermore, the rise of strategic partnerships between inverter manufacturers and EPC contractors is reinforcing the dominance of direct sales channels, hence denoting a wider segment scope.

Our in-depth analysis of the inverter systems market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Type |

|

|

Sales Channel |

|

|

Connection Type |

|

|

Phase |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Inverter Systems Market - Regional Analysis

APAC Market Insights

During the forecasted timeline, the inverter systems market in the Asia Pacific is expected to dominate the global dynamics, capturing the largest revenue share of 48.4%. This dominance is efficiently propelled by their increasing deployments in large-scale and distributed renewable energy projects. Also, smart inverters with grid-interactive features are gaining prominence in the region, particularly in the urban areas where rooftop solar is rising. Vikram Solar, in October 2025, announced the launch of its new N-Type solar module, Hypersol Pro, which comprises advanced unidirectional current flow for minimized energy loss and enhanced efficiency. The product is available in G12R and M10R variants, supports rooftop, utility-scale, floating, and hybrid installations, thereby offering hotspot-resistant performance and smart energy-ready compatibility, hence denoting a positive inverter systems market outlook.

China is considered to be the global hub for inverter system manufacturing as well as deployment, wherein the domestic firms have gained a significant revenue share. The country’s market is efficiently driven by intense competition among strong home-grown brands, high adoption of PV-linked inverters, and a shift toward higher‑power string and central units for utility-scale solar systems. BorgWarner, in July 2025, announced that it had secured a new dual inverter contract with a major OEM based in China, continuing its collaboration in the new energy vehicle sector. The dual inverter comprises a compact, high-density design enabling synchronous dual-motor control, reduced weight, and enhanced efficiency. Thus, the move will help China’s market by enhancing hybrid vehicle efficiency, reducing costs, and supporting the rapid adoption of new energy vehicles.

India is gaining momentum in the regional inverter systems market owing to the growth in rooftop solar installations, utility-scale PV projects, and increasingly by hybrid systems combining solar with battery storage. The integration of AI in inverter monitoring and control, and preferences toward hybrid and storage-capable inverters are identified as the key trends in this landscape. In this regard, Tata Power Renewables in October 2025 announced the launch of scale sustainably with the Tata Power initiative in Chhattisgarh to accelerate rooftop solar adoption among commercial and industrial customers in energy-intensive sectors. It also reported that the program offers end-to-end solutions, which include financing, customized installations, and long-term maintenance, supporting industries in the clean energy transition. Furthermore, it also leverages supportive policies and a strong service network, thus expanding rooftop solar capacity in the country.

North America Market Insights

In North America, the inverter systems market is evidently shaped by factors such as renewable energy deployment, especially solar PV, and increasing adoption of energy storage and electric vehicle charging infrastructure. The region also benefits from the residential, commercial, and industrial inverter segments, wherein the smart inverter functionalities and grid support features are increasingly required by utilities. The firms in the region are contributing through continued innovations around hybrid inverters, microinverter solutions for rooftops, and modular central inverters for large projects, hence attracting international players to make investments in this field. Furthermore, manufacturers are also responding to supply chain dynamics and localization pressures to serve the region, hence positively impacting inverter systems market growth.

In the U.S., inverter systems are integrated with the upliftment of residential solar, along with commercial PV, and storage-enabled renewable systems. Besides, the trend in the country is moving toward inverter architectures that support grid stability, two-way communication, and integration with battery storage and electric vehicles as well. In this regard, OSTI in February 2024 reported that the PV Fleet Performance Data Initiative analyzed over 1,100 U.S. photovoltaic systems to analyze inverter availability and system performance. It was observed that there has been a lower availability in the starting six months, improving at a steady pace by the end of the first year, with smaller inverters displaying higher reliability when compared to larger utility-scale units. Therefore, these insights highlight the benefits of string inverters and inform industry guidance on expected system availability for both distributed and utility-scale PV deployments, hence denoting a positive market outlook.

Canada is set to witness extensive growth in the upcoming years in the inverter systems market, which is characterised by a rise in remote, off-grid, and micro-grid applications, particularly in terms of low-populated regions. It also benefits from renewable plus storage systems, wherein the hybrid inverters combination of solar PV, battery storage, and generator backup is gaining traction. In May 2024, GoodWe announced that it had entered the country’s inverter systems market through an exclusive distribution partnership with Guillevin Co., which is a top electrical distributor. Hence, this collaboration enables the company to offer its advanced residential inverters, hybrid systems, and scalable battery solutions across Canada’s vast geography. Furthermore, Guillevin’s Greentech division will now feature GoodWe products, enhancing its renewable energy portfolio, hence making it suitable for standard market growth.

Europe Market Insights

Europe’s inverter systems market represents one of the mature landscapes, which is propelled by heightened demand for retrofit installations, grid-interactive systems, and residential solar plus storage. The emerging inverter technologies in the region are suitable for complex grid environments where there is a strong focus on energy management factors and lifecycle services. In July 2025, Enphase Energy announced the launch of the IQ8P Microinverter in Italy and Switzerland, thereby expanding its presence in Europe. The product offers an output of 480 W, which supports high-powered solar modules up to 670 W DC, maximizing both energy production and efficiency. Hence, the launch underscores the firm’s commitment to advancing smart, high-quality energy technologies and aiding homeowners in the region with greater energy independence.

Germany serves as the key growth engine for the inverter systems market in Europe throughout the discussed timeframe. The country benefits from strong emphasis on advanced inverter functions, integration with energy storage systems, and grid support capabilities. On the other hand, residential solar installations coupled with battery storage and smart inverters are also exacerbating this demand, encouraging more players to operate in this field. For instance, in June 2023, LG Energy Solution introduced its new hybrid inverter system for households in Europe. The product is offered in both high-voltage and low-voltage options, and it integrates with LGES batteries to deliver flexible energy capacity up to 32kWh. Hence, the launch is expected to accelerate the growth of the market by offering a highly reliable, user-friendly, and integrated energy solution.

The U.K. is one of the most prominent players in the inverter systems market, which is oriented towards residential and commercial solar installations. This is coupled with battery storage and smart energy management systems, is also prompting a profitable business environment for the players operating in this field. Growth is also supported by national net-zero targets and policies that promote distributed generation and home storage solutions. In addition, inverter products in the country emphasize UK grid standards, modularity for rooftop systems, and integration with home energy systems. Furthermore, the domestic and international players are adapting to the country-specific grid codes and consumer expectations, which are redefining growth dynamics in the U.K.

Key Inverter Systems Market Players:

- Enphase Energy, Inc.- U.S.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- SolarEdge Technologies, Inc.- Israel

- SMA Solar Technology AG- Germany

- Schneider Electric SE- France

- Fimer S.p.A.- Italy

- Fronius International GmbH- Austria

- TMEIC Corporation- Japan

- Yaskawa Solectria Solar LLC- U.S.

- Delta Electronics, Inc.- Taiwan

- Luminous Power Technologies Pvt. Ltd.- India

- Servotech Renewable Power Systems Ltd.- India

- Q CELLS (Hanwha Q Cells Co., Ltd.)- South Korea

- KACO New Energy GmbH- Germany

- ABB (ABB Power Grids)- Switzerland/Sweden

- Schneider Electric- Malaysia

- Enphase Energy, Inc. is the predominant leader in this field, which has pioneered micro‑inverter technology for residential solar systems and has shipped tens of millions of units across the world. The company has readily expanded into energy‑storage and monitoring services to build an integrated home energy solution. Furthermore, the company’s strategy emphasizes premium performance, long warranties, and deep installer partnerships to defend its leadership in module-level conversion, hence contributing to overall market growth.

- SolarEdge Technologies, Inc., founded in 2006 and headquartered in Herzliya, Israel, SolarEdge developed the DC‑optimized inverter system combining string inverters with power optimizers at the panel level. It serves residential, commercial, and utility‑scale segments and has shipped tens of gigawatts of systems globally. However, in recent years, it has faced an inventory build-up, soft installation growth in Europe, and has initiated multiple rounds of job cuts to realign its cost base.

- SMA Solar Technology AG is a leading inverter maker for residential, commercial, and utility-scale solar plants. The company is known for engineering robustness, a global service network, and a broad product portfolio. SMA emphasises R&D and high reliability to target premium segments and grid‑support applications. Increasing commoditisation of inverters and mounting competition from low-cost manufacturers, prompting SMA to lean into differentiated features such as high‑voltage SiC architectures and digital services, are a few strategic steps taken by the firm to secure its market position.

- FIMER S.p.A. (Italy). FIMER, headquartered in Italy, gained major global scale. With manufacturing plants in Italy and India, FIMER has positioned itself as a global supplier across residential, commercial, and large-scale utility inverter segments. In India, it supports the Aatma Nirbhar Bharat initiative via local manufacturing and supply to over solar‑power projects. FIMER’s strategy is expansion into emerging markets, scaling manufacturing capacity (5 GW+ in India), and leveraging its utility-scale inverter heritage to capture large project value share.

- Schneider Electric SE (France). Schneider Electric, headquartered in Rueil-Malmaison, France, is a global leader in energy management and automation, and its solar‑inverter and power‑electronics offerings tie into its broader sustainability and green‑grid ambitions. The company has emphasised digitalisation, green revenue growth, and acquisitions to build hardware‑and software platforms. For inverter systems, Schneider leverages its global service network, expertise in grid‑integration, energy‑storage system (ESS) coupling, and prefers high-value industrial/community solar segments.

Below is the list of some prominent players operating in the global inverter systems market:

The inverter systems market is extremely competitive, wherein the Europe-based firms, such as SMA and Schneider Electric, compete against U.S. innovators, such as Enphase, and Asian players, including Q CELLS, Luminous, and Servotech. Vertical integration with energy storage and smart controls, regional manufacturing to bypass tariffs, and partnerships with utility-scale solar developers are a few strategies implemented by the players to uplift the inverter systems market growth extensively. For instance, in August 2024, Enphase reported that it had partnered with SolarSquare to expand rooftop solar adoption, which is a combination of Enphase’s modular microinverters with SolarSquare’s high-quality solar panels and eight-hour installation services. In this regard, the partnership aims to provide homeowners in India a scalable, high-performance, and sustainable solar solution with guaranteed energy savings and long-term reliability, hence suitable for long-term market growth.

Corporate Landscape of the Inverter Systems Market:

Recent Developments

- In September 2025, Alpex Solar announced that it successfully raised ₹260.17 crore (USD 31.7 million) through a preferential issue of 21,46,600 equity shares and warrants to fund its vision of becoming an integrated solar cell and module manufacturer.

- In April 2025, Hitachi Industrial Equipment Systems announced the launch of its next-generation Grid Forming Inverter to stabilize power grids amid the growing share of renewable energy.

- Report ID: 8270

- Published Date: Nov 26, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.