Robotic Welding Market Outlook:

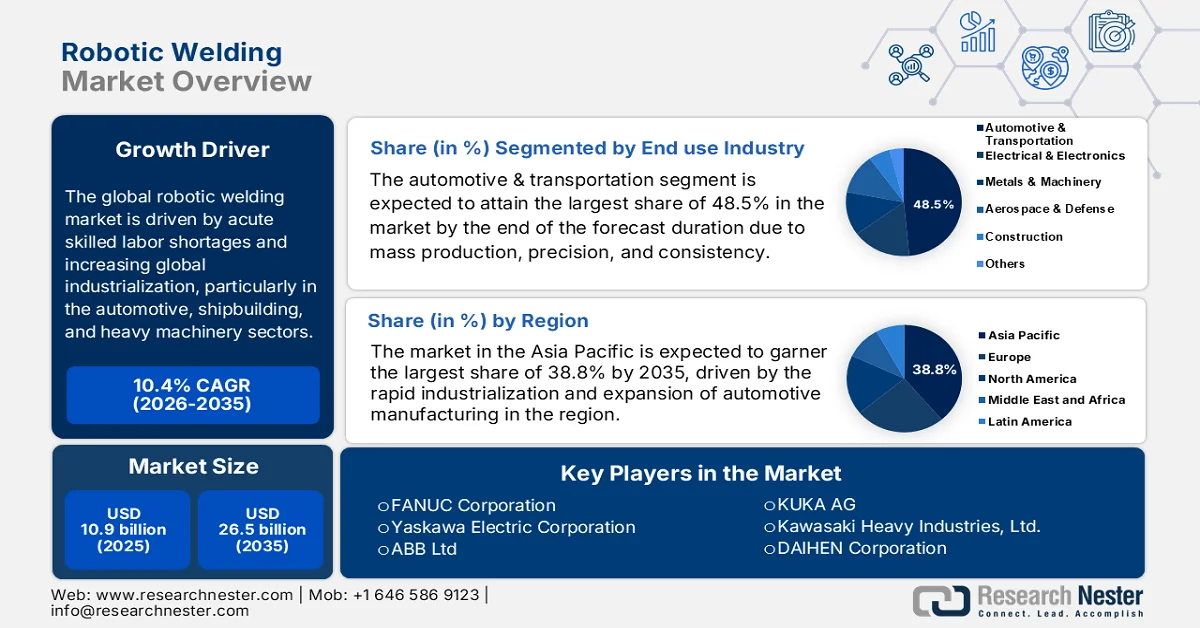

Robotic Welding Market size was valued at USD 10.9 billion in 2025 and is expected to attain USD 26.5 billion by 2035, growing at a CAGR of 10.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of robotic welding is assessed at USD 12 billion.

The robotic welding market is poised for extensive growth in the upcoming years, mainly propelled by acute skilled labor shortages and increasing global industrialization, particularly in the automotive, shipbuilding, and heavy machinery sectors. As per the article published by the International Federation of Robotics (IFR) in September 2025, global industrial robot installations doubled over the past decade and surpassed almost 542,000 units in 2024, wherein Asia led this with a substantial 74% of deployments. Besides, the report also mentioned that China dominated the market with 295,000 installations, surpassing foreign suppliers domestically, whereas Japan, Korea, and India maintained strong positions. Europe recorded 85,000 installations, led by Germany, while America installed 50,100 units, with the U.S. accounting for most, thus denoting a positive outlook for the market’s expansion and exposure.

Furthermore, the visible trend reshaping the future dynamics of the market is the rise of user-friendly collaborative robots, i.e., cobots, which allow smaller enterprises to adopt flexible automation without complex integration, thus broadening the market beyond massive factories. In December 2024, the reports from IFR observed that in 2023, collaborative robots (cobots) accounted for almost 10.5% of the 541,302 industrial robots installed worldwide. The report notes that Cobots are designed for safe human-robot collaboration, thereby offering ease of programming and fenceless operation, though they trade off payload and speed when compared to traditional robots. In addition, their lightweight design enables flexible relocation and integration, making them popular in industries with low-volume, high-mix production such as automotive, electronics, and logistics.

Key Robotic Welding Market Insights Summary:

Regional Highlights:

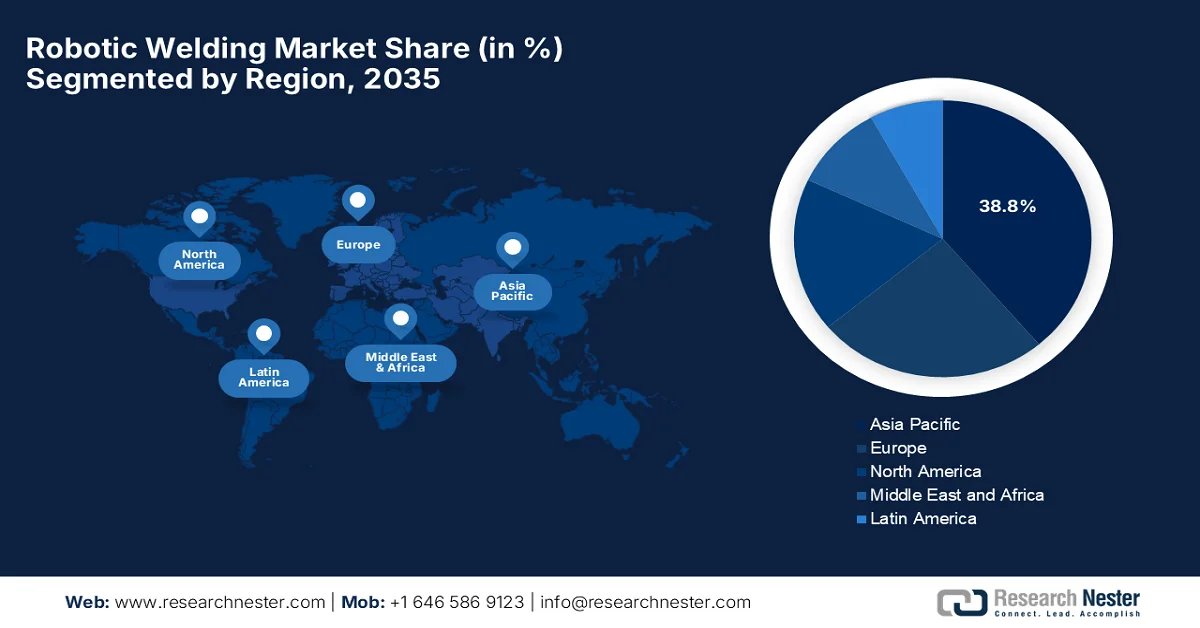

- Asia Pacific robotic welding market is projected to hold a dominant 38.8% share by 2035, propelled by rapid industrialization and expanding automotive manufacturing

- North America is anticipated to witness the fastest growth over 2026–2035, fueled by escalating labor shortages and rising automation adoption across industries

Segment Insights:

- Automotive & transportation segment in the robotic welding market is expected to capture a 48.5% share by 2035, driven by extensive reliance on robotic welding for mass production, precision, and consistency

- Arc welding segment is forecast to secure a significant share over 2026–2035, owing to its widespread applicability in heavy manufacturing and metal fabrication

Key Growth Trends:

- Increasing adoption of industrial automation

- Shortage of skilled welders

Major Challenges:

- Shortage of skilled workforce and technical expertise

- Complex programming and lack of flexibility

Key Players: FANUC Corporation (Japan), Yaskawa Electric Corporation (Japan), ABB Ltd. (Switzerland), KUKA AG (Germany), Kawasaki Heavy Industries, Ltd. (Japan), DAIHEN Corporation (Japan), Panasonic Holdings Corporation (Japan), Nachi-Fujikoshi Corp. (Japan), Comau S.p.A. (Italy), Hyundai Robotics (South Korea), Lincoln Electric Holdings, Inc. (U.S.), Miller Electric Mfg. LLC (U.S.), ESAB Corporation (U.S.), Teradyne Inc. (U.S.), Mitsubishi Electric Corporation (Japan), Denso Corporation (Japan), Novarc Technologies (Canada), Universal Robots A/S (Denmark), Stäubli International AG (Switzerland), Siasun Robot & Automation Co., Ltd. (China), AMADA Co., Ltd. (Japan).

Global Robotic Welding Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 10.9 billion

- 2026 Market Size: USD 12 billion

- Projected Market Size: USD 26.5 billion by 2035

- Growth Forecasts: 10.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 14 April, 2026

Robotic Welding Market - Growth Drivers and Challenges

Growth Drivers

- Increasing adoption of industrial automation: Most of the industries are adopting automation with the main goal of improving productivity and efficiency in terms of manufacturing processes. These robotic welding systems enable continuous operation with minimal downtime, higher speed, and reduced human intervention. In January 2022, the reports published by the World Economic Forum (WEF) stated that industrial automation matters as it remarkably improves productivity by enabling faster, more efficient, and more consistent manufacturing processes. It also strengthens the industrial workforce by allowing remote monitoring, data-driven decision-making, and safer human-machine collaboration. In addition, the industrial automation deliberately helps reduce environmental impact by optimizing energy use, minimizing waste, and improving resource efficiency across production systems, thus benefiting the overall robotic welding market.

- Shortage of skilled welders: There has been a worldwide shortage of skilled welders, and the aging workforce is encouraging manufacturers to opt for robotic solutions. Welding requires precision and expertise, which are becoming harder to source consistently. In this context, robotic welding systems help bridge this gap by performing complex tasks with programmed accuracy. In April 2024, the Marketplace Organization reported that a growing shortage of skilled welders is causing limitations in terms of efforts to expand manufacturing and clean energy projects. It also mentioned there will be a shortage of about 300,000 to 330,000 welders in the next four years, reflecting a major workforce gap. As a result, industries, i.e., construction, defense, and clean energy, are competing for the same limited labor pool, making training and on-the-job skill development highly essential, thus driving a heightened demand in the market.

- Expansion of manufacturing & infrastructure projects: The expansion of infrastructure, construction, shipbuilding, and heavy machinery industries drives the extensive need for welding operations. These sectors require large-scale, high-strength, and repetitive welding tasks that robotic systems have demonstrated to perform more efficiently. In May 2025, WEF stated that heavy industry, such as shipbuilding, construction, and offshore energy, is generally manual, but robotics and AI are now beginning to transform these sectors by enabling automation of large and complex production tasks. It also mentioned that a new Large Structure Production (LSP) Center in Denmark, which is supported by Europe and Danish funding, along with co-financing from the University of Southern Denmark, has been built. The center is the representation of robotic systems, AI-driven process planning, and digital twin technologies, which can enable welding and production directly from digital design data, thus making it suitable for bolstering the market.

Challenges

- Shortage of skilled workforce and technical expertise: Automation reduces manual labor, but the robotic welding systems require skilled people for programming, operation, and maintenance. There has been a heightened shortfall of technicians and engineers who have experience in robotics, welding processes, and automation software. This skill gap is mostly witnessed in emerging economies where industrial training infrastructure is still in the nascent stage. Other than that, any type of improper handling or lack of expertise can cause inefficiencies, downtime, and quality issues. However, to address this, companies need to make investments in workforce training and upskilling, which adds to operational costs. The challenge is again intensified by rapid technological advancements that require continuous learning by the workforce, thus negatively impacting the robotic welding market.

- Complex programming and lack of flexibility: The robotic welding systems are considered to be complex to program, especially for customized or low-volume production runs. The normal traditional robots are often designed for repetitive tasks, making it difficult to adapt them to high-mix, low-volume manufacturing environments. Reprogramming robots for new tasks requires time, expertise, and sometimes additional software tools, which can disrupt production schedules in the market. Therefore, this lack of flexibility limits their adoption in industries that require design changes or product customization most often. Meanwhile, the collaborative robots and AI-based solutions are improving flexibility, but many of the existing systems still face limitations in handling dynamic and unpredictable manufacturing conditions.

Robotic Welding Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.4% |

|

Base Year Market Size (2025) |

USD 10.9 billion |

|

Forecast Year Market Size (2035) |

USD 26.5 billion |

|

Regional Scope |

|

Robotic Welding Market Segmentation:

End use Industry Segment Analysis

The automotive & transportation segment is expected to attain the largest share of 48.5% in the robotic welding market by the end of the forecast duration. The dominance of the segment is largely attributable to its extensive reliance on robotic welding for mass production, precision, and consistency. In addition, government-backed industrial automation initiatives and manufacturing upgrades are accelerating adoption globally. In September 2023, at FABTECH 2023, FANUC America demonstrated advanced automation solutions, including robotic welding systems, which are especially designed for automotive manufacturing applications. The showcase included industrial robots such as the R-2000iD/210FH 210 kg payload, 2,605 mm reach, performing simulated spot welding on a truck cab, highlighting their use in high-precision, high-volume vehicle production. These demonstrations reflect the prominence of robotic welding in automotive manufacturing, with the main goal to support efficiency as well as mass production.

Type Segment Analysis

The arc welding, which is under the type segment, is expected to attain a significant share in the market during the discussed timeframe. Its widespread applicability in heavy manufacturing and metal fabrication is the key factor driving the sub-segment’s leadership. There has been a heightened demand for high-quality welds, and automation in industrial production is propelling the segment’s growth. As per the National Institute of Health (NIH) study in September 2023, which analyzed metal arc welding of heterogeneous thin steel plates, highlighted its importance in joining dissimilar metals, which are used in engineering applications. Besides this particular research, which used experimental welding parameters and applied a full factorial design and ANOVA to analyze weld quality and tensile strength. The results showed that arc welding remarkably affects weld strength and structural performance in steel fabrication, thereby confirming its relevance in industrial metal joining and manufacturing processes.

Component Segment Analysis

Based on component hardware is predicted to grow at a considerable rate in the robotic welding market by the conclusion of 2035. The segment’s growth is largely propelled by robotic systems, controllers, and welding equipment, which form the foundation of automation infrastructure. Rising labor shortages are also encouraging industries toward robotic hardware investments to maintain productivity. In addition, the advancements in terms of sensors, vision systems, and AI-enabled controllers are efficiently enhancing the precision and adaptability of robotic welding hardware. At the same time, automotive, aerospace, and heavy manufacturing industries are increasingly deploying integrated robotic systems to improve production efficiency and consistency. The demand for high-performance welding torches, robotic arms, and power supplies is rising, facilitated by the aspect of large-scale industrial automation. Overall, continuous innovation in core robotic components is solidifying the growth outlook of the hardware segment.

Our in-depth analysis of the robotic welding market includes the following segments:

|

Segment |

Subsegments |

|

End use Industry |

|

|

Type |

|

|

Component |

|

|

Payload Capacity |

|

|

Robot Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Robotic Welding Market - Regional Analysis

APAC Market Insights

The Asia Pacific robotic welding market is anticipated to dominate with the largest share of 38.8% by the conclusion of the forecast period. The region’s leadership is effectively propelled by rapid industrialization and the expansion of automotive manufacturing, which are key growth drivers. High vehicle demand in the region deliberately increases the need for robotic welding applications. In this context, the International Trade Administration (ITA) in December 2024 reported that in Australia, half of welding workshops are operating below 80% capacity, influenced by a lack of skilled workers, encouraging fabricators to automate processes across industries from mining equipment to locomotives. The report also mentioned that the country’s energy transition will require over 11,000 wind towers and 25,000 transmission towers, creating massive demand for robotic welding precision. Defense projects, including naval fleet expansion, further solidify the requirement for welding robots as essential for efficiency and advanced infrastructure fabrication.

The intense automation and rising industrial modernization are responsibly driving the market in China. Influenced by government initiatives and the adoption of AI and IoT technologies, the industry is making a shift toward smart welding systems to enhance productivity. Based on government data published in August 2025, China entered into the testing phase of its intelligent offshore welding robot system, which was developed by COOEC under CNOOC. The system integrates three advanced platforms capable of welding massive components up to 30 tons, with a 20-year service life and over 80% hardware localization. At the same time, Taiwan’s Ministry of Economic Affairs announced the launch of three AI robotics initiatives in 2025. These include Taiwan’s first AI endoscopic robot to improve diagnostic safety, medical service robots that reduce healthcare workloads by 20%, and a digital twin welding robot that doubles efficiency while cutting costs in half, thus making it suitable for standard market growth.

India robotic welding market is entering into a new phase of growth owing to the widespread adoption across diverse engineering and fabrication sectors. The need to achieve superior weld consistency, high-productivity arc-on times, and enhanced workplace safety, allowing domestic manufacturing to meet stringent global quality standards. At the same time, automotive components, two-wheelers, white goods, heavy engineering, railway coach fabrication, and construction equipment sectors are the primary drivers of this growth. As stated by Press Information Bureau (PIB) in February 2026, India’s Technology Advisory Group under the Empowered Technology Group was to chart a strategic roadmap for robotics. The main focus areas were the need for a coherent policy framework, indigenization of critical components, shared national data infrastructure, and mission-oriented R&D. The meeting underscored robotics as a strategic imperative for India’s self-reliance, competitiveness, and integration into defense, healthcare, and industrial sectors.

North America Market Insights

In North America, the robotic welding market is expected to grow at the quickest rate from 2026 to 2035. The region’s prominence is highly driven by escalating labor shortages, the need for enhanced precision, and the booming adoption of automation across automotive, aerospace, and manufacturing sectors. In June 2025, the Conference Board reported that slowing population growth and an aging workforce are creating huge labor shortages in the U.S., which may weaken long-term economic growth and competitiveness. It notes that at the onset of the pandemic, about 8.2 million workers exited the labor force, and even with recovery, the economy is still missing roughly 3 million workers when compared to pre-pandemic trends. The report also estimates that the U.S. would need to add about 4.6 million workers annually to maintain labor supply-demand balance, emphasizing the urgent need for automation and immigration reform, thus positively impacting market growth.

The extensive infrastructure development and the modernization of energy pipelines are the responsible factors for uplifting the U.S. robotic welding market. In addition, the remarkable resurgence in the automotive and aerospace industries, particularly with the rise of electric vehicle production, also prompts a profitable business environment for pioneers in this field. The country is witnessing an increased demand for advanced welding consumables, such as specialized flux-cored wires, and smart, inverter-based welding power sources that offer enhanced energy efficiency as well as portability. As per the official statistics published by IEA, in the U.S., electric car sales surged to a significant 55% in 2022, reaching a market share of 8% of total car sales. It mentioned that until 2023, EV adoption continued to accelerate, thereby contributing to the global total of 14 million electric cars sold. Therefore, U.S. growth reflects expanding model availability, improved performance, and strong policy incentives, positioning the country at the forefront of robotic welding globally.

There is a huge opportunity for the market in Canada to grow in the next decade, mainly propelled by demand from sectors such as infrastructure development, construction, automotive, and oil and gas. The country’s market is witnessing increasing investments in renewable energy projects such as wind and solar. Based on the government data published in June 2023, it’s observed that CanmetMATERIALS provides advanced welding and joining R&D focused on high‑strength steels for pipelines, lightweight materials for transport, high‑temperature alloys for power generation, and defense applications. Besides, their lab capabilities include laser welding, hybrid welding, brazing, diffusion bonding, additive manufacturing, and conventional arc processes such as SMAW, FCAW, and GTAW. In addition, it is equipped with a six‑axis robotic welding cell and a 3‑kilowatt fiber laser, and the facility supports industrial‑scale techniques such as pipeline welding, electron beam, friction stir, and resistance spot welding.

Europe Market Insights

Europe robotic welding market has acquired a strong position in the global dynamics owing to the proliferating Industry 4.0 adoption, increasing demand for high-precision manufacturing, and the need for enhanced productivity in different sectors. In addition, the important market drivers include the push for electric vehicle production, the requirement for superior welding quality, and the expansion of heavy-duty, high-payload robotic systems. Based on the official press release, a Italy based company was looking for industrial pilot partners from 2026 to 2027 to test and validate an AI-driven robotic welding system, which is designed for metal fabrication SMEs facing skilled labour shortages. The solution integrates robotic welding hardware with vision systems and AI algorithms to automatically generate welding paths, reducing setup time and minimizing the need for highly skilled welders, thus suitable for bolstering regional market growth.

The advanced automation in automotive manufacturing is considered to be the primary growth driver for the market in Germany. The country’s market also benefits from the deployment of automation to enhance precision, flexibility, and production efficiency across automotive, aerospace, metal fabrication, and shipbuilding sectors. Meanwhile, government-supported initiatives, such as digitalization funding and sustainability policies, are readily promoting green manufacturing procedures and are accelerating the incorporation of robotic solutions. In this context, a study in Baden-Württemberg in 2022 analyzed SME adoption of collaborative robot welding by taking reference from 16 interviews, observing the benefits such as improved safety, autonomy, quality, and flexibility. Besides, it mentioned that early-adopter SMEs proved successful, wherein workers quickly adapted to cobot programming. The findings show that cobot welding is feasible even for smaller firms, thus positively impacting the market’s growth in the overall country.

The UK robotic welding market maintains a strong position in the regional landscape due to a shortage of labor in traditional welding roles, which is accelerating the uptake of automated welding cells and articulated robots. The market is making a shift towards smarter technology, influenced by rising demand for AI-enabled systems, real-time monitoring, and cobots that offer easier integration for small and medium-sized enterprises. In December 2025, the UK launched the ISPARK project at the University of Leicester to develop an autonomous robotic system for in-orbit welding, and it is supported by TWI’s expertise in materials joining. Besides, it was funded under the UK Space Agency’s National Space Innovation Programme, and the project will test welding in vacuum environments and use digital twin simulations to validate performance before space deployment. Further, it aims to enable sustainable space operations by allowing repair, adaptation, and construction of large structures in orbit, thus strengthening the market’s potential in the country.

Key Robotic Welding Market Players:

- FANUC Corporation (Japan)

- Yaskawa Electric Corporation (Japan)

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- Kawasaki Heavy Industries, Ltd. (Japan)

- DAIHEN Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- Nachi-Fujikoshi Corp. (Japan)

- Comau S.p.A. (Italy)

- Hyundai Robotics (South Korea)

- Lincoln Electric Holdings, Inc. (U.S.)

- Miller Electric Mfg. LLC (U.S.)

- ESAB Corporation (U.S.)

- Teradyne Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Denso Corporation (Japan)

- Novarc Technologies (Canada)

- Universal Robots A/S (Denmark)

- Stäubli International AG (Switzerland)

- Siasun Robot & Automation Co., Ltd. (China)

- AMADA Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB Ltd. is one of the most influential players in the global market. The company offers an extensive portfolio of arc welding, spot welding, and collaborative robotic systems integrated with improved digital platforms such as simulation and AI-based process optimization.

- FANUC Corporation is yet another dominant force in this market, leading in terms of industrial welding robotics, known for its highly reliable and durable robotic arms. Besides, the firm’s welding robots are being deployed in automotive assembly lines for arc and spot-welding applications requiring extreme precision and uptime.

- Yaskawa Electric Corporation has registered itself as a major competitor in the robotic welding space. The company’s strength arises from its motion control capabilities and the ability to integrate robots with welding power sources for proper automation. Yaskawa is readily expanding its footprint globally by targeting emerging markets.

- KUKA AG is a Europe-based robotics manufacturer with extensive knowledge in automotive welding automation systems. The firm is a prominent provider of highly flexible robotic welding cells used in body-in-white production lines across major car manufacturers.

- Lincoln Electric Holdings, Inc. is a specialist player that is combining welding consumables expertise with robotic welding automation systems. The company is best known for offering integrated robotic welding packages that include robots, welding power sources, and software solutions for industrial fabrication and heavy manufacturing.

Below is the list of some prominent players operating in the global market:

The global market is being dominated by established players such as FANUC, ABB, Yaskawa, and KUKA, which collectively drive technological leadership through AI integration, IoT-enabled monitoring, and high-precision welding systems. Pioneers in this sector are making heavy investments in collaborative robots, vision-guided welding, and smart factory solutions. At the same time, tactical strategies adopted by players in the market are mergers, acquisitions, and partnerships to expand geographic reach. On the other hand, mid-tier firms focus on cost-effective and modular systems to serve SMEs. In August 2023, DAIHEN CORPORATION announced the acquisition of LORCH to strengthen its presence in Europe while preserving LORCH’s brand, workforce, and dealer network. The partnership will enhance customer value through new welding systems for EV bodies and thick plate applications, thus creating an optimistic market opportunity.

Corporate Landscape of the Robotic Welding Market:

Recent Developments

- In July 2025, KUKA received a follow-up order for 12 additional friction stir welding cells to support electric vehicle production in the U.S., building on last year’s delivery of 23 cells. These advanced KR FORTEC robots will weld battery cases and cooling jackets, enabling flexible, sustainable production lines for combustion, hybrid, and electric vehicles.

- In May 2025, Novarc Technologies unveiled NovAI, which is an AI-powered welding system that uses computer vision and real-time adaptation to deliver consistent, traceable, high-quality welds. It reduces defects, eliminates over-welding, and accelerates production while integrating seamlessly with leading robotic systems.

- In August 2023, Novarc Technologies Inc. announced the completion of a Series A fundraising round with Caterpillar Venture Capital Inc., along with Graham Partners and EDC. The investment will accelerate Novarc’s development of AI-powered robotic welding solutions, expanding global reach.

- Report ID: 3625

- Published Date: Apr 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Robotic Welding Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.