Industrial Robotics Market Outlook:

Industrial Robotics Market size was valued at USD 19.7 billion in 2025 and is projected to reach USD 61.8 billion by the end of 2035, rising at a CAGR of 12.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of industrial robotics is assessed at USD 22.1 billion.

The global industrial robotics market represents a critical capital goods sector focused on programmable automation for manufacturing and logistics. The industrial robotics deployment continues to scale in response to the measurable labor productivity and manufacturing resilience pressures documented by the public institutions and multilateral organizations. According to the International Federation of Robotics, September 2023 data, there are nearly 553,052 industrial robot installations recorded in factories around the globe, with a growth rate of 5% in 2022. Moreover, the integration of artificial intelligence boosts robotic systems and optimizes the supply chain operations via predictive analytics. Additionally, the adoption of industrial robots in the manufacturing sector is stimulated to meet the customer demand and ensure for an on-time delivery.

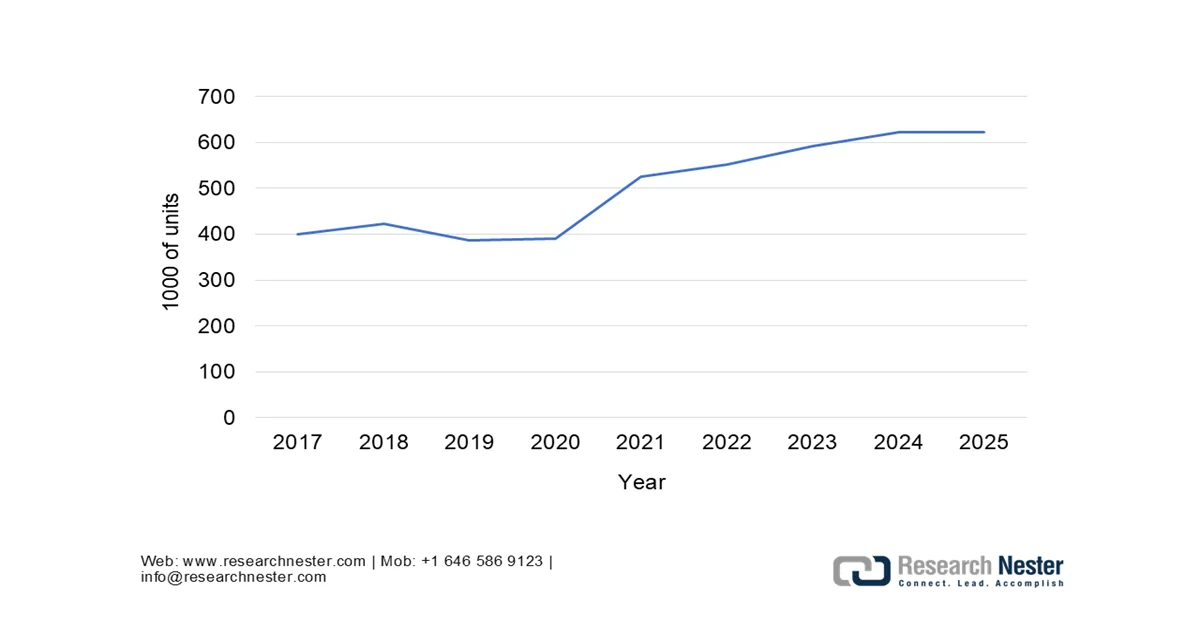

Annual Installation of Industrial Robots

Source: IFR September 2025

Besides, the manufacturing productivity growth across the advanced economies has increasingly depended on capital deepening, with the automation investments offsetting structural labor shortages mainly in aging economies such as Germany, South Korea, and Japan. On the other hand, it is noted that countries with higher robot adoption demonstrate stronger manufacturing value-added resilience during economic shocks, including post-pandemic recovery. As per the data indicated in the U.S. Census Bureau's February 2024 report, the manufacturing capital expenditure reached USD 314.3 billion in 2022, with automation and machinery representing one of the fastest-growing investment categories. Further, the government-backed industrial data point to the industrial robotics market is driven by long-term productivity economics, labor constraints, and policy-supported manufacturing competitiveness.

Key Industrial Robotics Market Insights Summary:

Regional Highlights:

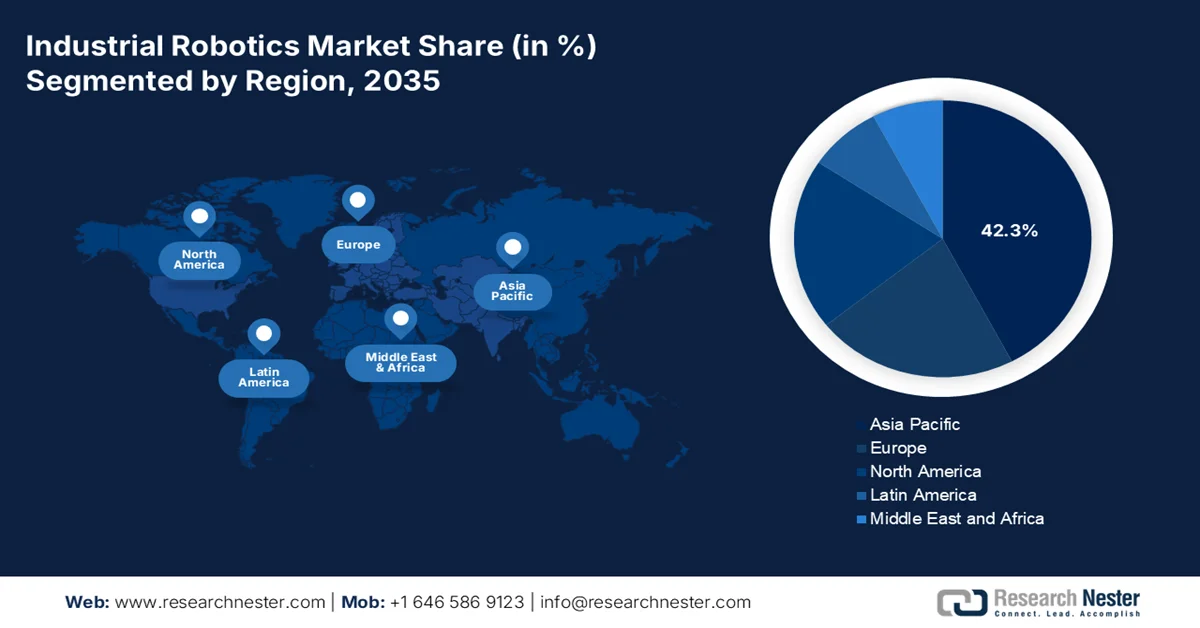

- In the industrial robotics market, Asia Pacific is projected to command a 42.3% revenue share by 2035, propelled by massive government-led industrial policies, a vast manufacturing base advancing automation for cost competitiveness, and substantial investments in next-generation industries.

- North America is anticipated to expand at a CAGR of 10.5% during 2026–2035, impelled by strong federal funding for semiconductor and EV battery manufacturing alongside persistent labor shortages accelerating automation adoption.

Segment Insights:

- In the industrial robotics market, the Sold and Installed sub-segment is projected to account for 80.4% share by 2035, fueled by large-scale manufacturers’ preference for capital expenditure ownership enabling long-term asset control and seamless integration into proprietary production systems.

- The Handling sub-segment is anticipated to hold the largest share by 2035, stimulated by rapid e-commerce expansion and persistent labor shortages in logistics demanding high-throughput flexible automation.

Key Growth Trends:

- Government led manufacturing modernization

- Rising public spending to address labor shortages

Major Challenges:

- Complexity of integration and lack of skilled workforce

- Rapid technological obsolescence and R&D pressure

Key Players: Fanuc (Japan), Yaskawa Electric Corporation (Japan), ABB (Switzerland), KUKA AG (Germany), Kawasaki Heavy Industries (Japan), Mitsubishi Electric (Japan), Denso Corporation (Japan), Nachi-Fujikoshi Corp. (Japan), Seiko Epson Corporation (Japan), OMRON Corporation (Japan), Stäubli International AG (Switzerland), Universal Robots (Denmark), Hyundai Robotics (South Korea), Doosan Robotics (South Korea), Rockwell Automation (U.S.), Teradyne (U.S.), Comau (Italy), FANUC America (U.S.), Hiwin Technologies (Taiwan), Siasun Robot & Automation (China)

Global Industrial Robotics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 19.7 billion

- 2026 Market Size: USD 22.1 billion

- Projected Market Size: USD 61.8 billion by 2035

- Growth Forecasts: 12.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, Japan, South Korea, United States, Germany

- Emerging Countries: India, Mexico, Vietnam, Indonesia, Brazil

Last updated on : 17 February, 2026

Industrial Robotics Market - Growth Drivers and Challenges

Growth Drivers

- Government led manufacturing modernization: The national governments are explicitly funding automation to strengthen the domestic manufacturing competitiveness in the industrial robotics market. According to the NIST March 2024 data, the U.S. CHIPS and Science Act allocates USD 52.7 billion toward semiconductor manufacturing and advanced industrial infrastructure, directly increasing the demand for robotics in fabrication, assembly, and materials handling facilities. Similarly, the European Commission’s October 2025 data states Horizon Europe and Digital Europe programs budget amounts of 95 million euros for advanced manufacturing robotics and AI-enabled industrial systems. Moreover, the countries with active industrial automation policies recorded higher manufacturing value-added growth. Further, the robotics suppliers that are aligned with government-funded factory expansion, reshoring, and strategic sector programs face structurally lower demand risk and faster procurement cycles driven by public capital flows rather than private discretionary spending.

- Rising public spending to address labor shortages: Labor availability constraints are the primary driver in the industrial robotics market. According to the Manufacturing Institute's May 2021 data, there are nearly 2.1 million unfilled manufacturing jobs by 2030, driven by retirements and skill mismatches. Moreover, the 2026 Work Japan report indicates that Japan’s Ministry of Economy and Industry reports that over 60% of manufacturers face labor shortages, stimulating the automation subsidies. Additionally, the robot adoption is highest in economies experiencing workforce aging, with the robot density rising fastest in Japan, Germany, and South Korea. The demand is strongest where the governments explicitly position robotics as a labor replacement strategy, not just productivity enhancement, supporting sustained capex even during economic slowdowns.

- Advancements in AI technology: AI is shaping the industrial robotics market by improving the system adaptability, precision, and uptime, making automation viable across a broader set of manufacturing environments. According to the Congress.gov September 2024 data, the federal funding for AI-related research accounted for USD 200 million, with a significant share allocated for advanced manufacturing robotics and autonomous systems. This public investment has stimulated the deployment of machine vision, real-time quality inspection, and predictive maintenance capabilities in industrial robots, directly improving the throughput and reducing the defect rates. From the demand perspective, AI integration shifts robotics purchasing decisions from labor substitution toward operational efficiency and asset optimization, supporting high average system value and repeat investments.

Challenges

- Complexity of integration and lack of skilled workforce: Integrating robots into brownfield and legacy MES is highly complex. The critical shortage of skilled engineers for programming, maintenance, and system integration stalls deployment. The leading players in the industrial robotics market tackle this with user-friendly, easy programming software and global training academies. The International Federation of Robotics highlights the skills gap as the key challenge, with governments such as Germany’s funding initiatives, such as Robotics in Care, to build talent pipelines.

- Rapid technological obsolescence and R&D pressure: The pace of innovation in AI vision and machine learning requires continuous high R&D investment to avoid product obsolescence. Top players invest a billion annually, partnering with top companies to embed AI and Isaac Sim platform, ensuring robots evolve with next-gen software capabilities. This sustained R&D intensity elevates cost pressures and entry barriers, favoring large companies with strong capital reserves while accelerating consolidation and strategic partnerships across the industrial robotics market.

Industrial Robotics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.1% |

|

Base Year Market Size (2025) |

USD 19.7 billion |

|

Forecast Year Market Size (2035) |

USD 61.8 billion |

|

Regional Scope |

|

Industrial Robotics Market Segmentation:

Function Segment Analysis

The sold and installed sub-segment is the leading sub-segment in the industrial robotics market and is poised to hold the share value of 80.4% by 2035. The dominance is driven by the preference of large-scale manufacturers for capital expenditure ownership, which provides long-term asset control and integration into proprietary production systems. According to the IFR September 2024, nearly 70% of newly deployed robots were installed in Asia, 17% in Europe, and 10% in the U.S. Additionally, the sold and installed model enables deeper customization, higher uptime, and tighter integration with the Industry 4.0 architecture, reinforcing its appeal among automotive electronics and heavy manufacturing sectors. The government-backed automation incentives and reshoring initiatives in Asia, Europe, and the U.S. are further stimulating the upfront robot installations over service-based or rental models.

Application Segment Analysis

The handling sub-segment is leading and is poised to hold the largest share in the industrial robotics market. The handling operations encompass machine tending, palletizing, and pick and place. The segment’s growth is propelled by the e-commerce expansion and persistent labor shortages in logistics, necessitating high-throughput flexible automation. The government statistics highlight this sector acceleration. For example, the productivity in the warehousing and shortage sector is heavily reliant on automation for handling increased by a significant percentage, a surge largely attributed to accelerated technological adoption during and post pandemic. Furthermore, public investments in smart logistics infrastructure and national automation roadmaps across the U.S., Europe, and Asia are reinforcing the adoption of robotic handling systems to enhance supply chain resilience and operational continuity.

Type Segment Analysis

The articulated robots are the market leaders in the industrial robotics market. Their human arm design offers unmatched versatility for complex tasks such as welding, assembly, and material handling across diverse industries. From automotive to general manufacturing. Government trade and industrial production data substantiate this demand. According to the Jet Propulsion Laboratory, January 2022 data, RoboSimian is an articulated research robot that is used for a variety of planetary analogue mobility and mobile manipulation tasks. The robot is nearly 120 kg and has the ability to carry 20 kg of payload. Additionally, national manufacturing modernization programs and robotics adoption incentives are accelerating the deployment of articulated robots, as their high payload capacity, extended reach, and reprogrammability align with the growing demand for flexible, multi-purpose automation across both traditional and emerging industrial applications.

Our in-depth analysis of the industrial robotics market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Component |

|

|

Payload |

|

|

Application |

|

|

Industry |

|

|

Function |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Industrial Robotics Market - Regional Analysis

APAC Market Insights

The Asia Pacific industrial robotics market is the dominant player and is expected to hold the regional revenue share of 42.3% by 2035. The market is driven by the massive government-led industrial policies, vast manufacturing base undergoing automation to maintain cost competitiveness and significant investments in the next-gen industries. According to the IFR 2024 data, nearly 404,391 units of industrial robots were installed in Asia in 2022. Moreover, the nations like South Korea and Japan continue to leverage their technological leadership as major OEMs, while India’s production-linked incentive schemes aim to build domestic manufacturing capacity, hence directly increasing the automation demand. Key trends include the localization of robot supply chains in China, the rapid growth of collaborative robots in SMEs, and the strategic focus on robotics for electric vehicle (EV) battery and semiconductor manufacturing across the region.

Strong government-led manufacturing and automation initiatives are shaping the industrial robotics market in India. According to the International Federation of Robotics May 2023 data, the industrial robot installations in India reached a record 4,945 units in 2023, showing a 54% YoY increase and positioning India among the top ten countries globally for the annual installations and indicating the automation intensity. This growth is supported by the substantial public investment, with the Government of India allocating over USD 165 billion toward the advanced manufacturing and industrial modernization through 2024, as stated in the International Trade Administration's March 2025 report. Further, the Production Linked Incentive scheme launched with a USD 24 billion budget targets 14 strategic manufacturing sectors and is directly stimulating the capital expenditure on automated production systems across automotive, electronics, pharmaceuticals, and aerospace. Collectively, these indicators point to a positive impact on market growth in India.

Large-scale manufacturing investment, policy-driven adoption, and rapid domestic supplier expansion are responsible for boosting the industrial robotics market in China. According to the People’s Republic of China, in August 2024, data showed that China produced 430,000 industrial robots in 2023, while newly installed robots accounted for more than 50% of global installations over the past three years, reinforcing its position as the world’s largest market for the eleventh consecutive year. Moreover, the International Federation of Robotics in September 2024 shows that 1.76 million industrial robots were operating in China factories in 2023, reflecting a 17% YoY increase with 276,288 units installed during the year, representing 51% of global demand despite a modest annual decline. Further, the demand remains concentrated in electrical and electronics manufacturing, where 77,464 robots were installed in 2023, accounting for 62% of global electronics-sector installations, highlighting China’s central role in shaping global robotics demand and supply dynamics.

China Industrial Robot Installations by Industry (2023)

|

End-use Industry |

Robot Installations (Units, 2023) |

YoY Change vs. 2022 |

CAGR (2018–2023) |

Share of Global Installations (2023) |

Share of Chinese Suppliers |

|

Electrical / Electronics |

77,464 |

23% |

11% |

62% |

54% |

|

Automotive |

64,882 |

12% |

11% |

48% |

22% |

|

Metal & Machinery |

41,578 |

35% |

- |

- |

85% |

Source: IFR September 2024

North America Market Insights

The North America industrial robotics market is anticipated to register the fastest CAGR of 10.5% during the forecast period 2026 to 2035. The market is driven by a confluence of policy necessity and technological advancement. The key drivers include substantial federal spending via the CHIPS and Science Act and the Inflation Reduction Act, which are catalyzing investments in semiconductor and EV battery manufacturing, both highly automated sectors. Furthermore, the chronic labor shortage in U.S. manufacturing job openings persistently makes automation a strategic imperative for operational continuity. The region is a leader in adopting collaborative robots and AI-driven vision systems, expanding robotics into SMEs and complex non-automotive applications such as logistics and food processing. A strong trend toward reshoring and nearshoring of critical supply chains is fueling the demand for new flexible automation lines. The market is defined by high innovation with significant R&D focused on software-defined automation and mobile robotics, positioning North America for sustained growth as it modernizes its industrial base.

The sustained automation investment across large-scale manufacturing sectors, particularly automotive, is driving the industrial robotics market in U.S. According to IFR September 2024 data, total industrial robot installations in the U.S. have increased by 12% to 44,303 units, indicating continued capital expenditure despite broader economic uncertainty. Moreover, the automotive manufacturing remains a core demand anchor, accounting for 33% of all U.S. industrial robot installations, as car and component manufacturers installed a record 14,678 robots in 2023, following a 47% year-on-year surge in 2022 to 14,472 units. This sustained shift reflects a structural automation requirement of a country that ranks as the second-largest producer of cars and light vehicles globally, where robotics is critical for welding, assembly, painting, and quality consistency. Further, these deployment trends underscore an active upliftment in the U.S. market.

Annual Installations of Industrial Robots in U.S.

|

Year |

1000 of units |

|

2019 |

33 |

|

2020 |

31 |

|

2021 |

36 |

|

2022 |

40 |

|

2023 |

44 |

Source: IFR September 2024

Strong automotive-sector demand and concentrated enterprise adoption are driving the demand for the industrial robotics market in Canada. According to the IFR September 2024 data, robot installations in Canada reached 4,616 units, representing a 43% increase YoY, with the automotive industry accounting for 55% of total installations. Further, the Government of Canada's August 2024 reports that in 2022, 2.0% of Canada enterprises had adopted robotics technologies, representing 7.5% of total employment and 11.5% of total revenue. Additionally, the adoption is heavily skewed toward manufacturing, where 8.4% of firms use robotics, particularly in food processing, transportation equipment, plastics, and machinery manufacturing. On the other hand, Ontario and Québec lead adoption, reflecting automotive and industrial concentration. This data indicates that there is a high demand in Canada market growth with measurable productivity and innovation gains.

Europe Market Insights

The industrial robotics market in Europe is growing significantly due to advanced manufacturing, strong regulatory frameworks, and strategic initiatives to boost technological advancements and the green transition. The demand is mainly driven by the need to enhance productivity amid high labor costs and aging demographics, along with stringent environmental regulations pushing for efficient precision manufacturing. Moreover, the European Union Factories of the Future initiatives under Horizon Europe and the Recovery and Resilience Facility provide critical funding for digitalization and automation, mainly for SMEs. According to the IFR 2024 data, in Europe there are nearly 92,393 units of industrial robots installed. The region is leading via high-precision engineering for automotive, aerospace, and pharmaceutical sectors, with Germany as the central hub.

Germany is one of the world’s most advanced and automation-intensive industrial robotics markets, supported by the deep manufacturing penetration and a sustained replacement demand. According to the International Federation of Robotics 2024 report, Germany accounted for approximately 5% of global industrial robot installations in 2023, ranking as the fifth largest robot market worldwide. Further GTAI October 2025 report depicts that automation intensity is among the highest globally, with 449 industrial robots per 10,000 employees in 2024, the highest robot density in Europe, and fourth worldwide in 2023 at 429, behind South Korea, Singapore, and China. At the same time, the International Trade Administration in August 2025 indicates a rising competition for Germany automation suppliers. Overall, the industrial robotics market in Germany continues to sustain stable robotics investment and long-term market growth.

New Installation of Industrial Robots

|

Industry |

Automotive |

Metal & Machinery |

Plastic & Chemical Products |

Electrical Components & Electronics |

|

2021 |

9,167 |

3,522 |

1,832 |

1,746 |

|

2022 |

7,120 |

4,234 |

2,072 |

1,543 |

|

2023 |

9,190 |

4,916 |

2,057 |

1,377 |

Source: International Trade Administration in August 2025

The industrial robotics market in UK has reached a historic expansion point in 2023 and is driven by fiscal incentives and concentrated investment in automotive manufacturing. According to the International Federation of Robotics, September 2024 data, the industrial robot installations in the UK climbed to a record 3,830 units in 2023, representing a 51% YoY increase. Moreover, the growth was heavily supported by the automotive sector, where installations surged 297% to 1,924 units, accounting for 50% of total robot demand, largely linked to the completion of major electric vehicle assembly projects. Further, the food and beverage industry also contributed to market expansion, with robot installations rising 59% to 555 units, while demand from the metal industry increased 20% to 324 units. Overall, these factors indicate that the UK industrial robotics market growth is set to boom with all time high growth.

Key Industrial Robotics Market Players:

- Fanuc (Japan)

- Yaskawa Electric Corporation (Japan)

- ABB (Switzerland)

- KUKA AG (Germany)

- Kawasaki Heavy Industries (Japan)

- Mitsubishi Electric (Japan)

- Denso Corporation (Japan)

- Nachi-Fujikoshi Corp. (Japan)

- Seiko Epson Corporation (Japan)

- OMRON Corporation (Japan)

- Stäubli International AG (Switzerland)

- Universal Robots (Denmark)

- Hyundai Robotics (South Korea)

- Doosan Robotics (South Korea)

- Rockwell Automation (U.S.)

- Teradyne (U.S.)

- Comau (Italy)

- FANUC America (U.S.)

- Hiwin Technologies (Taiwan)

- Siasun Robot & Automation (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Fanuc is a titan in the industrial robotics market and is renowned for its high-speed, precise, and reliable automation cells. Its strategic initiatives center on Zero Downtime achieved via its FIELD system and AI-driven predictive maintenance. By deeply integrating robotics with IoT and machine learning, the company enables factories to avoid failures and optimize the production flow, boosting its dominance in automotive and electronics manufacturing.

- Yaskawa Electric Corporation is another leading Japanese player in the industrial robotics market and actively pushes its Mechatronics concept. This strategy focuses on the seamless digital integration of robotics, motion control, and data analytics. Yaskawa’s initiative, such as its cloud-based platform, aims to create smart factories where the robots are intelligent connected nodes providing actionable insights to dramatically improve efficiency and flexibility for customers.

- ABB competes in the global industrial robotics market with a strategy built on a full automation ecosystem. A key initiative is its focus on collaborative robots such as the YuMi and SWIFTI series, designed to work safely alongside humans. The ABB expands its reach via strategic software platforms, such as its RobotStudio simulation suite, and by targeting high-growth sectors such as logistics and healthcare to move beyond traditional heavy industry applications.

- KUKA AG is a major European player in the industrial robotics market leverages its strategy to drive digital transformation. Its initiatives revolve around platform connectivity, offering solutions such as KUKA Connect for cloud-based robot management and analytics. By emphasizing open interfaces and partnerships within the smart factory landscape, KUKA aims to provide flexible, future-proof automation that adapts to evolving industry standards.

- Kawasaki Heavy Industries maintains a strong position in the industrial robotics market via a dual strategy of robust hardware and smart solutions. Its key initiatives are the Kawasaki Robotics Solution Suite, which integrates advanced sensor technology and AI to enable tasks such as precise bin picking and quality inspection. This focus on adding intelligent value-driven automation to its durable industrial robots allows Kawasaki to target complex applications in manufacturing and logistics.

Here is a list of key players operating in the global industrial robotics market:

The industrial robotics market is defined by intense competition and rapid technological evolution with the key players aggressively pursuing strategic initiatives to dominate the market. The leading companies are focusing on collaborative robots, AI, and machine learning integration, and industry-specific solutions to capture market share. The strategic partnerships, acquisitions, and heavy R&D investment are commonplace as manufacturers aim to provide comprehensive automation ecosystems. For example, in January 2024, ABB announced the acquisition of Sevensense, expanding its leadership in next-generation AI-enabled mobile robotics. The landscape is currently dominated by established Europe- and Asia-based players who leverage scale and innovation, while new players and specialized firms focus on competing via agility and niche applications. This dynamic environment is stimulating the adoption across diverse sectors globally.

Corporate Landscape of the Industrial Robotics Market:

Recent Developments

- In November 2025, Agile Robots acquired the assets of systems manufacturer thyssenkrupp Automation Engineering in Europe and North America, which had previously been part of thyssenkrupp AG's Automotive Technology segment.

- In October 2025, SoftBank Group Corp announced that it has entered into a definitive agreement with ABB Ltd, a global technology leader in electrification and automation, to acquire ABB’s robotics business for a total purchase price of USD 5.375 billion.

- In May 2025, NEURA Robotics announced the acquisition of B.A.H. Industrial Solutions GmbH, a long-established specialist in control system construction, quality inspection, industrial assembly and engineering with around 140 employees.

- Report ID: 3087

- Published Date: Feb 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.