Global Industrial Electric Heating (Induction Furnace) Market

1. An Outline of the Global Industrial Electric Heating (Induction Furnace) Market

1.1. Market Definition and Segmentation

1.2. Study Assumptions and Abbreviations

2. Research Methodology & Approach

2.1. Primary Research

2.2. Secondary Research

2.3. Data Triangulation

2.4. SPSS Methodology

3. Executive Summary

4. Growth Drivers

5. Major Roadblocks

6. Opportunities

7. Prevalent Trends

8. Government Regulation

9. Growth Outlook

10. Competitive White Space Analysis – Identifying Untapped Market Gaps

11. Risk Overview

12. SWOT

13. Technological Advancement

14. Technology Maturity Matrix for the Industrial Electric Heating (Induction Furnace) Market: Recent News

15. Regional Demand

16. Global Industrial Electric Heating (Induction Furnace) by Geography – Strategic Comparative Analysis

17. Strategic Segment Analysis: Industrial Electric Heating (Induction Furnace) Demand Landscape

18. Industrial Electric Heating (Induction Furnace) Demand Trends Driven by rapid industrialization, growing steel production, rising adoption of energy-efficient and low-emission technologies, and increasing automation in metal processing industries (2026-2036)

19. Root Cause Analysis (RCA) for discovering problems of the Industrial Electric Heating (Induction Furnace) Market

20. Porter Five Forces

21. PESTLE

22. Comparative Positioning

23. Global Industrial Electric Heating (Induction Furnace) – Key Player Analysis (2036)

24. Competitive Landscape: Key Suppliers/Players

25. Competitive Model: A Detailed Inside View for Investors

26. Company Market Share, 2036 (%)

26.1. ABP Induction Systems

26.2. Inductotherm Group

26.3. SMS group GmbH

26.4. Otto Junker GmbH

26.5. Tenova S.p.A.

26.6. Electrotherm (India) Limited

26.7. Danieli & C. Officine Meccaniche S.p.A.

26.8. EFD Induction

26.9. Nabertherm GmbH

26.10. Pillar Induction

27. Global Industrial Electric Heating (Induction Furnace) Market Outlook

27.1. Market Overview

27.1.1. Market Revenue by Value (USD Billion), and Compound Annual Growth Rate (CAGR)

27.2. Industrial Electric Heating (Induction Furnace) Market Segmentation Analysis (2026-2036)

27.2.1. By Furnace Type

27.2.1.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1. By Furnace Capacity

27.2.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2. By Application

27.2.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3. Regional Synopsis, Value (USD Billion), 2026-2036

27.2.3.1. North America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.3.2. Europe Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.3.3. Asia Pacific Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.3.4. Latin America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

27.2.3.5. Middle East and Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

28. North America Market

28.2. Overview

28.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

28.2.2. Increment $ Opportunity Assessment, 2026-2036

28.3. Segmentation (USD Billion), 2026-2036, By

27.2.2. By Furnace Type

27.2.2.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.2.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1. By Furnace Capacity

28.3.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2. By Application

28.3.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

28.3.3. Country Level Analysis, Value (USD Billion)

28.3.3.1. U.S. Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

28.3.3.2. Canada Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29. Europe Market

29.2. Overview

29.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

29.2.2. Increment $ Opportunity Assessment, 2026-2036

29.3. Segmentation (USD Billion), 2026-2036, By

27.2.3. By Furnace Type

27.2.3.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.3.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1. By Furnace Capacity

29.3.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2. By Application

29.3.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

29.3.3. Country Level Analysis, Value (USD Billion)

29.3.3.1. UK Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.2. Germany Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.3. France Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.4. Italy Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.5. Spain Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.6. Netherlands Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.7. Russia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.8. Switzerland Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.9. Poland Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.10. Belgium Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

29.3.3.11. Rest of Europe Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30. Asia Pacific Market

30.2. Overview

30.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

30.2.2. Increment $ Opportunity Assessment, 2026-2036

30.3. Segmentation (USD Billion), 2026-2036, By

27.2.4. By Furnace Type

27.2.4.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.4.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1. By Furnace Capacity

30.3.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2. By Application

30.3.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

30.3.3. Country Level Analysis, Value (USD Billion)

30.3.3.1. China Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.2. India Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.3. South Korea Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.4. Australia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.5. Indonesia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.6. Malaysia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.7. Vietnam Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.8. Thailand Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.9. Singapore Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.10. New Zealand Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

30.3.3.11. Rest of Asia Pacific Excluding Japan Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31. Latin America Market

31.2. Overview

31.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

31.2.2. Increment $ Opportunity Assessment, 2026-2036

31.2.3. Year-on-Year Growth Forecast (%)

31.3. Segmentation (USD Billion), 2026-2036, By

27.2.5. By Furnace Type

27.2.5.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.5.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1. By Furnace Capacity

31.3.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2. By Application

31.3.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

31.3.3. Country Level Analysis, Value (USD Billion)

31.3.3.1. Brazil Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.3.2. Argentina Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.3.3. Mexico Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

31.3.3.4. Rest of Latin America Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32. Middle East & Africa Market

32.2. Overview

32.2.1. Market Value (USD Billion), Current and Future Projections, 2026-2036

32.2.2. Increment $ Opportunity Assessment, 2026-2036

32.2.3. Year-on-Year Growth Forecast (%)

32.3. Segmentation (USD Billion), 2026-2036, By

27.2.6. By Furnace Type

27.2.6.1. Coreless Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

27.2.6.2. Channel Furnace, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1. By Furnace Capacity

32.3.1.1. Upto 3 tons, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.2. 3-10 tons, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.3. 10-30 tons, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.4. 30-50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.1.5. Above 50 tons, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2. By Application

32.3.2.1. Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.1.1. Grey Iron Castings, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.1.2. Other, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.2. Steel, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.3. Non-Ferrous Metals, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.3.1. Aluminium, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.3.2. Copper Alloys, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.2.3.3. Others, Market Value (USD Billion), and CAGR, 2026-2036F

32.3.3. Country Level Analysis, Value (USD Billion)

32.3.3.1. Saudi Arabia Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.2. UAE Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.3. Israel Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.4. Qatar Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.5. Kuwait Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.6. Oman Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.7. South Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

32.3.3.8. Rest of Middle East & Africa Market Value (USD Billion) and CAGR & Y-o-Y Growth Trend, 2026-2036F

33. Global Economic Scenario

33.2. World Economic Outlook

34. About Research Nester

34.2. Our Global Clientele

34.3. We Serve Clients Across World

Industrial Electric Heating (Induction Furnace) Market Outlook:

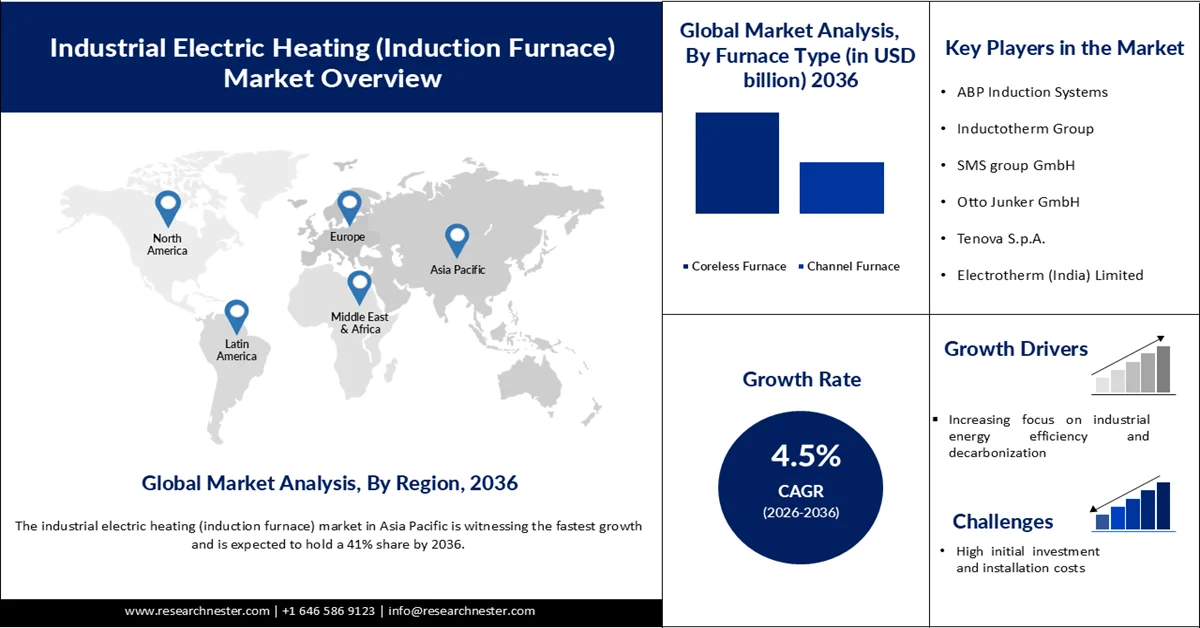

Industrial Electric Heating (Induction Furnace) Market size was valued at USD 2.70 billion in 2025 and is projected to reach USD 4.38 billion by 2036, growing at a CAGR of 4.5% during the forecast period, i.e., 2026-2036. In 2026, the industry size of industrial electric heating (induction furnace) is estimated at USD 2.82 billion.

The primary growth driver of the global industrial electric heating (induction furnace) market is the accelerating shift toward energy-efficient, low-emission industrial manufacturing processes, especially in the steel and metal processing industries. Induction furnace technology offers faster heating, higher thermal efficiency, and lower carbon emissions than conventional fossil-fuel-based heating systems, making it increasingly attractive for industrial modernization initiatives. According to the International Energy Agency (IEA), scrap-based electric arc furnace steel production is 60% to 70% less energy intensive than traditional primary steel production routes, significantly supporting the adoption of electric heating technologies in heavy industry.

Another major factor driving industrial electric heating (induction furnace) market expansion is the rapid growth of industrial automation, electric mobility, and renewable energy infrastructure, which is increasing demand for precision metal processing and high-performance heating systems. Governments and industries worldwide are investing heavily in cleaner steelmaking and electrification technologies to meet sustainability targets and reduce industrial emissions. The IEA states that global steel demand is expected to grow by more than one-third by 2050, while low-emission steel production projects and electric furnace adoption continue to increase globally. Additionally, hydrogen-based direct reduced iron electric arc furnace projects are emerging as key decarbonization pathways, further strengthening demand for advanced industrial electric heating systems and induction furnaces.

Key Industrial Electric Heating (Induction Furnace) Market Insights Summary:

Regional Highlights:

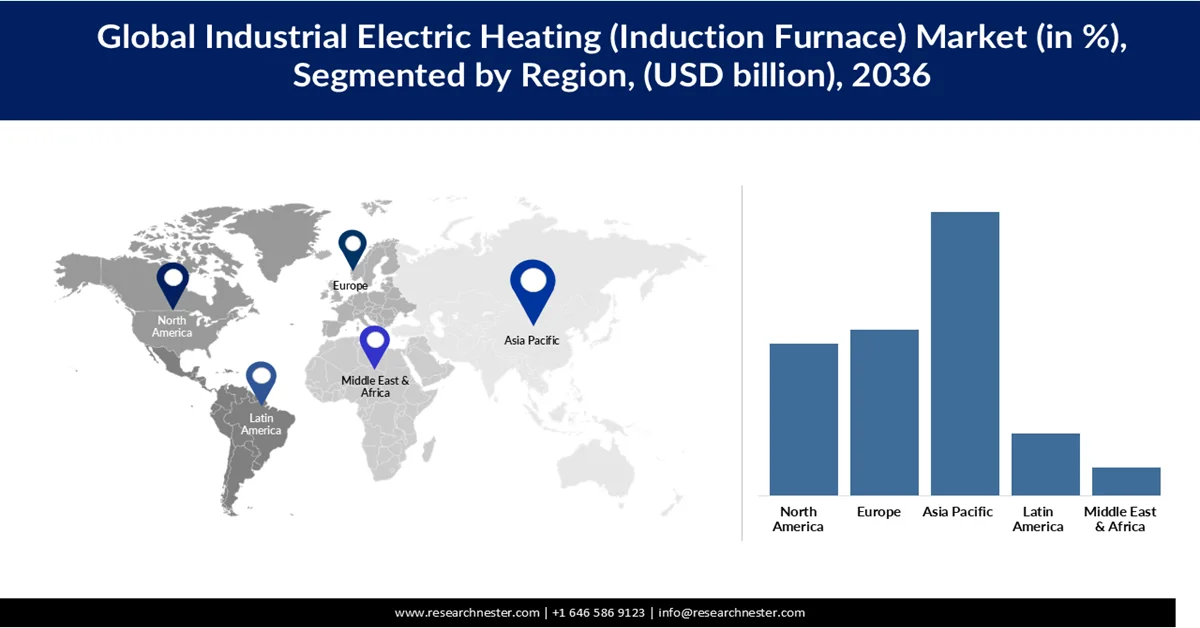

- The Industrial electric heating (induction furnace) market in Asia Pacific is anticipated to secure 41% share by 2036, underpinned by rapid industrialization and expanding steel production capacity

- Europe is projected to account for 24% share during the forecast period, reinforced by strict environmental regulations and a strong emphasis on reducing industrial carbon emissions

Segment Insights:

- In the Industrial electric heating (induction furnace) market, the Coreless Induction Furnace segment is forecast to capture 66% share by 2036, fueled by its high energy efficiency, operational flexibility, and ability to process a wide range of metals

- The Up to 3 Tons Furnace Capacity segment is expected to witness robust demand throughout 2026-2036, supported by strong adoption in small-scale foundries, precision casting units, and specialty metal processing applications

Key Growth Trends:

- Increasing focus on industrial energy efficiency and decarbonization

- Rising adoption of automation and smart manufacturing technologies

Major Challenges:

- High initial investment and installation costs

- Dependence on stable and high-capacity electricity supply

Key Players: ABP Induction Systems (Germany), Inductotherm Group (U.S.), SMS group GmbH (Germany), Otto Junker GmbH (Germany), Tenova S.p.A. (Italy), Electrotherm (India) Limited (India), Danieli & C. Officine Meccaniche S.p.A. (Italy), EFD Induction (Norway), Nabertherm GmbH (Germany), Pillar Induction (U.S.).

Global Industrial Electric Heating (Induction Furnace) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.70 billion

- 2026 Market Size: USD 2.82 billion

- Projected Market Size: USD 4.38 billion by 2036

- Growth Forecasts: 4.5% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: China, India, Japan, United States, Germany

- Emerging Countries: Vietnam, Indonesia, Thailand, Mexico, Brazil

Last updated on : 2 June, 2026

Industrial Electric Heating (Induction Furnace) Market - Growth Drivers and Challenges

Growth Drivers

- Increasing focus on industrial energy efficiency and decarbonization: Growing pressure on industries to reduce energy consumption and carbon emissions is driving the adoption of industrial electric heating systems, including induction furnaces. Compared to conventional fuel-fired furnaces, induction heating systems offer significantly higher energy efficiency, lower heat loss, and cleaner operation, making them suitable for sustainable manufacturing environments. Governments and regulatory agencies worldwide are implementing stricter emission standards for heavy industries, encouraging the transition toward electrified heating technologies. According to the IEA in 2022, the industrial sector accounted for approximately 37% of global final energy consumption, highlighting the critical need for energy-efficient industrial technologies. The increasing integration of renewable electricity into industrial operations is further supporting demand for electric heating systems across steel and metal processing and manufacturing industries.

- Rising adoption of automation and smart manufacturing technologies: The growing implementation of Industry 4.0 and smart manufacturing systems is accelerating demand for advanced induction heating technologies capable of delivering precise temperature control, automation compatibility, and real-time process monitoring. Modern induction furnaces are increasingly integrated with digital control systems, sensors, and predictive maintenance technologies to improve operational efficiency and reduce downtime. Industries such as aerospace, automotive, and machinery manufacturing are adopting automated production lines that require highly controlled and repeatable heating processes, thereby supporting industrial electric heating (induction furnace) market growth. According to the National Institute of Standards and Technology NIST in 2024, manufacturers adopting smart manufacturing technologies reported significant improvements in productivity, operational efficiency, and maintenance optimization across industrial facilities. The ability of induction heating systems to support automated and high-precision operations is strengthening their adoption in technologically advanced manufacturing environments.

- Growth of renewable energy and electrical infrastructure development: Rapid expansion of renewable energy projects and electrical infrastructure is increasing demand for processed steel, copper, aluminum, and specialty alloys, thereby driving the adoption of induction furnace technologies in metal processing industries. Components used in wind turbines, solar infrastructure, electric grids, and energy storage systems require high-quality metal products manufactured through efficient and controlled heating processes. According to the International Renewable Energy Agency (IRENA), global renewable energy capacity increased by approximately 473 gigawatts in 2023, representing the highest annual increase ever recorded. This rapid infrastructure expansion is creating strong demand for industrial metal production and recycling operations, where induction furnaces are widely utilized due to their efficiency and lower environmental impact. Increasing investments in grid modernization and electrification projects are expected to further support industrial electric heating (induction furnace) market expansion during the forecast period.

Challenges

- High initial investment and installation costs: The adoption of industrial electric heating systems, including induction furnaces, is often restrained by the high upfront capital investment required for equipment procurement, installation, and supporting electrical infrastructure. Induction furnace systems require advanced power supply units, cooling systems, and high-capacity electrical connections, which significantly increase initial setup costs, especially for small and medium-sized manufacturers. In addition, upgrading existing production facilities to accommodate electric heating technologies may involve substantial operational modifications and downtime. These financial barriers can limit adoption in cost-sensitive industries and developing regions where conventional fuel-based furnaces remain comparatively cheaper. As a result, many manufacturers delay modernization investments despite the long-term efficiency benefits offered by induction heating systems.

- Dependence on stable and high-capacity electricity supply: Industrial electric heating systems are highly dependent on continuous and reliable electricity availability, which can create operational challenges in regions with unstable power infrastructure or high electricity costs. Induction furnaces consume large amounts of electrical energy during high-temperature processing, making energy pricing and grid reliability critical factors for industrial users. Power fluctuations, outages, or inadequate grid capacity can disrupt production cycles, reduce equipment efficiency, and increase maintenance requirements. In several developing economies, inconsistent electricity supply and rising industrial power tariffs continue to limit widespread adoption of electric heating technologies. This dependence on stable power infrastructure remains a key restraint for industrial electric heating (induction furnace) market growth, particularly in energy-intensive manufacturing sectors.

Industrial Electric Heating (Induction Furnace) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2036 |

|

CAGR |

4.5% |

|

Base Year Market Size (2025) |

USD 2.70 billion |

|

Forecast Year Market Size (2036) |

USD 4.38 billion |

|

Regional Scope |

|

Industrial Electric Heating (Induction Furnace) Market Segmentation:

Furnace Type Segment Analysis

The coreless induction furnace segment is a significant driver of market growth and is expected to hold a 66% industrial electric heating (induction furnace) market share by 2036, due to its high energy efficiency, operational flexibility, and ability to process a wide range of metals, including steel, iron, copper, and aluminum. These furnaces are widely adopted in foundries and metal recycling operations because they provide rapid and uniform heating, lower contamination risk, and improved process control compared to conventional fuel-based furnace systems. Their increasing adoption is closely associated with the global transition toward scrap-based and lower-emission steelmaking technologies. According to the IEA, the blast furnace-basic oxygen furnace (BF-BOF) route accounted for nearly 70% of global steel production and recorded an average production cost of approximately USD 490/t between 2015 and 2020. As industries increasingly seek more energy-efficient, lower-emission alternatives to conventional steelmaking processes, demand for electric melting technologies such as coreless induction furnaces is rising steadily across the automotive, construction, and industrial manufacturing sectors.

Furnace Capacity Segment Analysis

The up to 3 tons furnace capacity segment is driving steady growth in the industrial electric heating (induction furnace) market due to its strong adoption in small-scale foundries, precision casting units, and specialty metal processing applications. These compact furnaces are widely preferred for their low capital investment, ease of installation, and ability to support flexible batch production, making them highly suitable for small and medium enterprises. They are commonly used in producing automotive components, jewelry, specialty alloys, and repair-based metal casting, where high precision and frequent material changeovers are required. The segment also benefits from increasing demand for customized and low-volume manufacturing driven by the aerospace, medical devices, and electronics industries. In addition, their lower energy consumption and minimal infrastructure requirements make them attractive in developing regions where cost-sensitive manufacturing dominates industrial activity.

Application Segment Analysis

The steel segment is expected to grow at a significant industrial electric heating (induction furnace) market share between 2026 and 2036 due to its extensive reliance on efficient and high-temperature metal melting technologies. Induction furnaces are increasingly used in secondary steelmaking processes where scrap steel is remelted and refined, supporting cost-efficient and lower emission production methods. The growing shift toward electric-based steel production is accelerating adoption as manufacturers aim to reduce dependence on blast furnace and basic oxygen furnace routes and improve energy efficiency. Rising demand for steel from automotive construction, infrastructure, and renewable energy sectors further strengthens the need for flexible and high-throughput melting solutions, directly boosting induction furnace usage in steel applications.

Our in-depth analysis of the industrial electric heating (induction furnace) market includes the following segments:

|

Segments |

Subsegments |

|

Furnace Type |

|

|

Furnace Capacity |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Industrial Electric Heating (Induction Furnace) Market - Regional Analysis

Asia Pacific Market Insights

The Asia Pacific is witnessing the fastest growth in the industrial electric heating (induction furnace) market and is expected to hold a 41% share by 2036, driven by rapid industrialization and expanding steel production capacity. Countries such as China, India, and Japan are heavily investing in electric arc and induction-based steelmaking technologies to improve efficiency and reduce emissions. Strong growth in the automotive, construction, and manufacturing industries is further boosting demand for metal processing equipment. In addition, the increasing availability of scrap metal and lower production costs are supporting widespread adoption of induction furnace systems across the region.

The Japan industrial electric heating (induction furnace) market is growing steadily, supported by its advanced manufacturing base and strong focus on high-precision metal processing. The Japan market is projected to grow from USD 191.7 million in 2025 to USD 370.0 million by 2036, registering a compound annual growth rate of 6.2% during the forecast period, driven by automotive electronics and specialty steel industries that require high-quality and consistent metal output. Japan’s emphasis on energy-efficient and low-emission production technologies is encouraging the adoption of electric-based melting systems, including induction furnaces. The country’s strong recycling ecosystem also supports greater use of scrap-based steelmaking, which benefits furnace demand. Additionally, continuous investment in smart manufacturing and automation is improving furnace efficiency and process control across industrial facilities.

The India industrial electric heating (induction furnace) market is experiencing strong growth driven by rapid industrialization, expanding infrastructure development, and rising steel consumption. Increasing demand from the construction, automotive, and engineering sectors is boosting the need for efficient and cost-effective metal melting technologies. Small and medium-scale foundries widely use induction furnaces due to their lower installation cost and flexibility in operations. Government initiatives supporting manufacturing growth, such as Make in India, are further accelerating industrial expansion and metal processing demand. Additionally, increasing availability of scrap metal and a shift toward electric-based steel production are strengthening the adoption of induction furnace systems across the country.

Europe Market Insights

Europe is showing consistent growth in the industrial electric heating (induction furnace) market and is projected to hold a share of 24% during the forecast period, due to strict environmental regulations and a strong emphasis on reducing industrial carbon emissions. The European Union’s decarbonization policies are encouraging steel producers to shift toward electric and scrap-based production methods. Demand is also supported by well-established automotive and engineering industries that require high-quality metal processing technologies. Furthermore, increasing investments in circular economy initiatives and metal recycling infrastructure are strengthening the adoption of induction furnace systems across the region.

The Germany industrial electric heating (induction furnace) market is growing steadily, driven by its strong automotive engineering base and advanced industrial manufacturing ecosystem. The country’s strict environmental regulations under the EU framework are accelerating the shift toward energy-efficient and low-emission metal processing technologies. Increasing demand for high-precision components in automotive machinery and industrial equipment is further supporting the adoption of induction furnace systems. In addition, Germany’s focus on circular economy practices and high metal recycling rates is strengthening the use of electric melting technologies in steel and foundry operations.

The UK industrial electric heating (induction furnace) market is experiencing moderate growth, supported by demand from construction, infrastructure, and metal fabrication industries. Rising emphasis on decarbonization and reduction of industrial carbon emissions is encouraging the adoption of electric-based furnace technologies. Growth in the automotive, aerospace, and energy sectors is also contributing to increased demand for high-quality metal processing solutions. Additionally, the expansion of recycling-based steel production and the modernization of aging industrial facilities are further supporting the uptake of induction furnace systems across the country.

North America Market Insights

North America is experiencing steady growth in the industrial electric heating (induction furnace) market and is expected to have a share of 22% by 2036, driven by the modernization of aging steel infrastructure and the rising focus on energy-efficient manufacturing. The region is increasingly adopting electric-based steelmaking technologies to support decarbonization goals and reduce reliance on traditional blast furnace systems. Strong demand from automotive, aerospace, and industrial machinery sectors is also supporting market expansion. Additionally, advancements in automation and smart manufacturing are improving furnace efficiency and operational control across facilities.

The U.S. industrial electric heating (induction furnace) market is witnessing steady growth driven by the modernization of steel manufacturing infrastructure and the increasing adoption of energy-efficient electric melting technologies. Strong demand from automotive, aerospace, construction, and industrial machinery sectors is supporting the shift toward induction-based metal processing systems. The country’s focus on decarbonization and reduction of emissions from heavy industry is further accelerating the replacement of conventional fuel-based furnaces. In addition, rising investment in electric arc and induction furnace-based steel recycling is strengthening market expansion across foundries and secondary metal production facilities.

The Canada industrial electric heating (induction furnace) market is growing at a moderate but steady pace, supported by expansion in construction infrastructure and metal fabrication industries. Increasing use of steel and non-ferrous metals in energy transportation and industrial applications is driving demand for efficient melting technologies. The country’s strong focus on sustainable manufacturing and carbon reduction targets is encouraging the adoption of electric-based furnace systems. Additionally, growth in scrap metal recycling activities and small to medium-scale foundry operations is further supporting the use of induction furnaces across the industrial sector.

Key Industrial Electric Heating (Induction Furnace) Market Players:

- ABP Induction Systems (Germany)

- Inductotherm Group (U.S.)

- SMS group GmbH (Germany)

- Otto Junker GmbH (Germany)

- Tenova S.p.A. (Italy)

- Electrotherm (India) Limited (India)

- Danieli & C. Officine Meccaniche S.p.A. (Italy)

- EFD Induction (Norway)

- Nabertherm GmbH (Germany)

- Pillar Induction (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Inductotherm Group is a leading manufacturer of induction melting and heating systems serving the steel, foundry, and metal processing industries worldwide. The company focuses on energy-efficient furnace technologies, automation, and customized thermal processing solutions. Its strong global distribution network and continuous investment in R&D support its competitive position. The company also emphasizes sustainable manufacturing solutions to meet growing environmental standards.

- ABP Induction Systems specializes in induction melting and heating technologies for ferrous and non-ferrous metal applications. The company is recognized for its advanced digital monitoring systems and high-performance induction furnaces that improve operational efficiency. It serves major industrial sectors, including automotive, casting, and steel manufacturing. ABP also focuses on smart furnace solutions integrated with Industry 4.0 capabilities.

- SMS group GmbH provides metallurgical plant engineering and induction furnace solutions for steel and non-ferrous metal production. The company is driving innovation through sustainable electric heating technologies and intelligent process automation systems. Its solutions help manufacturers improve energy efficiency, reduce emissions, and enhance production quality. SMS group maintains a strong global presence through strategic collaborations and large-scale industrial projects.

- Electrotherm (India) Limited is a prominent supplier of induction melting equipment and electric heating technologies across emerging and developed markets. The company offers cost-effective and energy-efficient induction furnace systems primarily for steel manufacturing applications. Its focus on technological innovation and localized manufacturing supports strong market penetration in Asia. Electrotherm is also expanding its product portfolio to address rising industrial automation demand.

- Tenova S.p.A. delivers advanced furnace technologies and sustainable industrial solutions for the metals and mining industries. The company emphasizes environmentally friendly electric heating systems designed to optimize productivity and lower carbon emissions. Its induction furnace technologies are widely adopted in specialty steel and high-quality metal production applications. Tenova continues to strengthen its industrial electric heating (induction furnace) market position through digitalization and green technology initiatives.

Below is the list of the key players operating in the global industrial electric heating (induction furnace) market:

Key players in the industrial electric heating (induction furnace) market are driving growth through continuous technological advancements focused on energy efficiency, automation, and precision heating solutions. Companies are investing in smart induction systems, sustainable electric melting technologies, and low-emission manufacturing processes to meet evolving environmental regulations. Strategic partnerships, capacity expansions, and integration of Industry 4.0 technologies are further strengthening their industrial electric heating (induction furnace) market presence. Rising demand from the steel, automotive, aerospace, and electronics industries is also encouraging manufacturers to develop high-performance furnaces with improved productivity and consistent output quality.

Corporate Landscape of the Global Industrial Electric Heating (Induction Furnace) Market:

Recent Developments

- In August 2025, Vinton Steel entered into a new agreement with Tenova, a leading developer and supplier of sustainable solutions for the metals industry, to supply a state-of-the-art walking hearth reheating furnace. This development represents an important milestone in the ongoing technological partnership between the two companies and highlights their shared commitment to advancing innovation in high-quality steel production.

- Report ID: 8598

- Published Date: Jun 02, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.