Hybrid Intelligence Market Outlook:

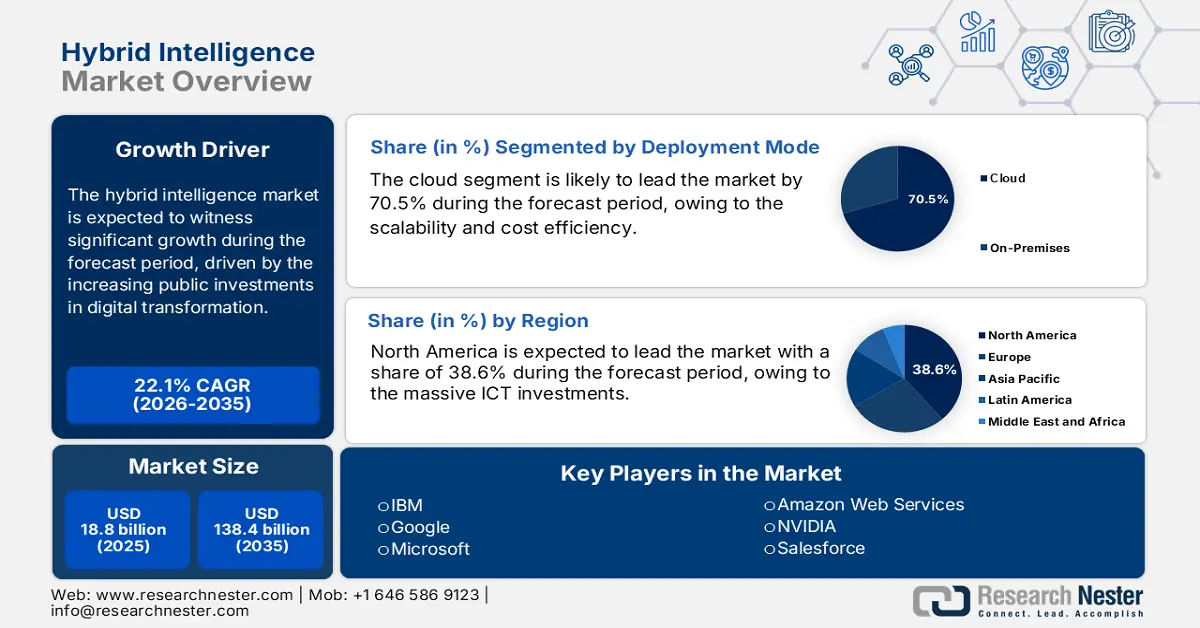

Hybrid Intelligence Market size was valued at USD 18.8 billion in 2025 and is projected to reach USD 138.4 billion by the end of 2035, rising at a CAGR of 22.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of hybrid intelligence is estimated at USD 22.95 billion.

The multi-tiered global supply chain, rising input costs, and increasing public investments in digital transformation are the key drivers of the hybrid intelligence market. Nearly USD 10,929.0 million worth of products in the computer and electronic products category in December 2024 were imported by the U.S., according to the Census report in February 2025. This data is highly related to the market, as it reflects the foundational infrastructure fueling its growth. On the other hand, the AI algorithms, machine learning models, and real-time data processing are powered by these imported technological components, which include processors, GPUs, embedded systems, and edge devices. Further, the Bureau of Labor Statistics (BLS) Producer Price Index for General-purpose electronic computers has shown fluctuations, reflecting the complex cost structures of manufacturing the hardware required for data processing and analysis.

Investments in technological development Investments in technological development are the key to the adoption of hybrid intelligence. The NITRD data for the fiscal year 2019 to 2025 has depicted that the federal R&D budget in AI accounted for USD 3,316.1 million, with a notable allocation to hybrid system optimization and human AI collaboration research. The Federal Reserve Bank of St. Louis data in 2025 depicts that the producer price index for electronic computer manufacturing stood at 101.374, based on a February 2023 = 100 index reference point. The consumer price index for information technology-related services has increased, indicating the cost compression at production levels and moderate inflation in downstream services. These opposing index movements indicate a mature market with enhanced manufacturing efficiencies and sustained consumer demand. The integration of hybrid intelligence technologies into supply networks and production cycles is increasingly positioned as a cost-stabilizing mechanism rather than a speculative innovation driver.

Federal Budget for AI R&D

|

Year |

Budget Allocation (USD million) |

|

2021 |

2,409.6 |

|

2022 |

2,914.1 |

|

2023 |

3,121.9 |

|

2024 |

2,977.5 |

|

2025 |

3,316.1 |

Source: NITRD 2025

Key Hybrid Intelligence Market Insights Summary:

Regional Insights:

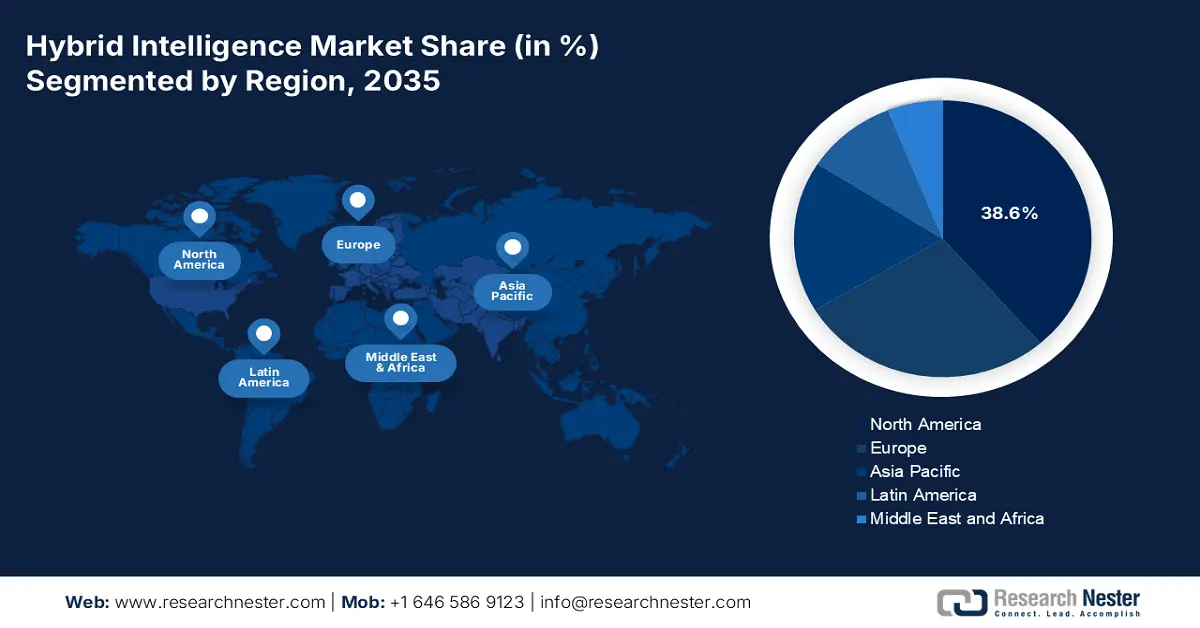

- By 2035, North America is anticipated to command a 38.6% share of the hybrid intelligence market, supported by massive ICT investments, early AI adoption, and government-led broadband expansion impelled by public digital infrastructure spending.

- Asia Pacific is projected to register a 12% CAGR during 2026–2035, underpinned by large-scale digitalization programs, rapid AI–IoT integration, and sovereign AI initiatives stimulated by national innovation strategies.

Segment Insights:

- The cloud deployment mode is set to capture a 70.5% share by 2035, fueled by scalability, cost efficiency, and flexible access to AI resources.

- Large enterprises are forecast to secure a dominant share by 2035, bolstered by substantial capital capacity and the need for advanced automation across complex legacy systems.

Key Growth Trends:

- Strategic government investment and national AI strategies

- Escalating cybersecurity threats and evolving frameworks

Major Challenges:

- Divergent data localization and privacy laws

- Lack of global technical standards

Key Players: Google (Alphabet Inc.) (USA), Microsoft (USA), Amazon Web Services (AWS) (USA), NVIDIA (USA), Salesforce (USA), SAP (Germany), Siemens (Germany), Bosch (Germany), ABB (Switzerland/Sweden), SAS Institute (USA), Oracle (USA), Intel (USA), Accenture (Ireland), C3.ai (USA), Samsung SDS (South Korea), NEC Corporation (Japan), Fujitsu (Japan), Tata Consultancy Services (India), Infosys (India).

Global Hybrid Intelligence Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 18.8 billion

- 2026 Market Size: USD 22.95 billion

- Projected Market Size: USD 138.4 billion by 2035

- Growth Forecasts: 22.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, Singapore, South Korea, Brazil, United Arab Emirates

Last updated on : 19 November, 2025

Hybrid Intelligence Market - Growth Drivers and Challenges

Growth Drivers

- Strategic government investment and national AI strategies: Governments are investing heavily in AI as a matter of national policy. These initiatives, including the U.S.’s National AI Initiative and China’s Next Generation Artificial Intelligence Development Plan, are directly funding R&D and creating pilot programs that stimulate the market demand. For example, the Australian Bureau of Statistics data in August 2025 states that businesses are increasingly their investment in AI R&D, nearly USD 668.3 million was invested into AI R&D from 2023 to 2024. This driver creates a strong emphasis on shaping the type of hybrid solution that gains traction. Companies actively join in publicly supported consortia to gain access to funds, data, and early-adopter markets, and they should match their R&D and product development plans with these national priorities.

- Escalating cybersecurity threats and evolving frameworks: The frequency and developments in cyber-attacks make the security operations fall short. Hybrid intelligence, combining AI’s pattern recognition with human strategic oversight, is becoming vital in threat detection and response. Frameworks such as the NIST Cybersecurity Framework 2.0 integrate governance and supply chain risk, where AI-driven analytics are vital. The Industrial Cyber data in November 2025 reported that the ransomware attacks were up by 25% in October, thus fueling the market demand. The EU's NIS2 Directive promotes businesses to use cutting-edge security measures, which speeds up market expansion. Organizations should implement a hybrid intelligence platform that leverages AI for continuous network monitoring and log analysis, freeing up human analysts to manage complex incident response.

- Industry specific digital transformation pressures: Every sector is including healthcare and finance, is undergoing rapid digital transformation with hybrid intelligence at its core. In healthcare, it aids in diagnostic imaging, and in finance, it helps in fraud detection, which learns from the human investigator's feedback. As this digital transformation is the key driver, the transformation varies with respect to the sector region, such as automotive in Germany and Japan, and fintech in Southeast Asia. Companies focus on developing vertical-specific solutions rather than generic platforms. A hybrid intelligence system tailored to radiologists, incorporating their feedback to improve diagnostic algorithms, will see faster adoption than a general-purpose image analysis tool.

Challenges

- Divergent data localization and privacy laws: Complying with the conflicting data sovereignty regulations, including the EU’s GDPR, China’s PIPL, and India’s Digital Personal Data Protection Act, pushes suppliers to create more region-specific data architectures. This increases the development costs and delays the market entry. For example, the new data protection laws in India have delayed the product launches for various multinational tech firms, as they reconfigured the data processing workflows to address the local compliance requirements.

- Lack of global technical standards: As the universally accepted standards for AI interoperability, safety, and ethics are in process, creating market friction. Suppliers must adapt their product to various national certifications; on the other hand, the government risks vendor to lock in with proprietary systems. The International Organization for Standardization (ISO) and the International Telecommunication Union (ITU) are developing standards, but widespread adoption remains years away, constraining seamless global integration.

Hybrid Intelligence Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

22.1% |

|

Base Year Market Size (2025) |

USD 18.8 billion |

|

Forecast Year Market Size (2035) |

USD 138.4 billion |

|

Regional Scope |

|

Hybrid Intelligence Market Segmentation:

Deployment Mode Segment Analysis

The cloud deployment mode is leading the hybrid intelligence market and is poised to hold the share value of 70.5% by 2035. The segment is driven by its scalability, cost efficiency, and flexibility. The cloud platforms provide vast computational resources and pre-built AI services, which make the development and deployment of a hybrid system accessible. This eliminates the requirement for massive upfront investment in op on-premises hardware. The report from the UK Department for Science, Innovation and Technology data in September 2025 states that over 85% of the businesses in the UK have adopted AI, which is primarily used as cloud-based AI software or services. This preference is fueled by the need for rapid iteration, seamless updates, and the ability to use the distributed data sources, which are intrinsic advantages of the cloud model for iterative human-AI collaboration.

Organization Size Segment Analysis

By 2035, the large enterprises are projected to lead the organization size segment and maintain a dominant market share. These organization requires the necessary capital that is dedicated to data science teams, and extensive legacy system landscapes which require advanced hybrid intelligence solutions for automation and integration. Their scale allows them to take a significant initial investment and transform the complex change management. As per the U.S. Census Bureau data, U.S. firms are actively adopting AI and machine learning to automate the process. This high adoption rate highlights their role as the key early adopters and revenue drivers in the market, aiming for enterprise-wide optimization and competitive advantage.

Component Segment Analysis

The software segment's dominance is fueled by the critical need for AI platforms, development frameworks, and Explainable AI tools that enable seamless human-AI collaboration. Regulatory pressure, such as from the EU AI Act, mandates transparency and human oversight in high-risk AI systems, directly driving demand for sophisticated software that provides auditable decision trails. To further solidify this sub-segment's lead, the National Institute of Standards and Technology (NIST) is creating a thorough AI Risk Management Framework that highlights the necessity of dependable and comprehensible AI software.

Our in-depth analysis of the hybrid intelligence market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Technology |

|

|

Deployment Mode |

|

|

Organization Size |

|

|

Application |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Hybrid Intelligence Market - Regional Analysis

North America Market Insights

By 2035, North America is expected to dominate the hybrid intelligence market, holding a market share of 38.6%. the massive ICT investments and early AI adoption across healthcare, finance, and defense drive the market. Integration of AI with edge computing for real time analytics and robust focus on the ethical AI frameworks are the key drivers of the market growth. Government spending is the critical catalyst. The Broadband and USA data in 2021 depict that the U.S. Infrastructure Investment and Jobs Act allocates USD 65 billion for broadband, which directly impacts the deployment of hybrid intelligence. Further, in 2023, most of the households in the U.S. gained access to advanced services via federal broadband initiatives. Agencies like the FCC and NTIA work to close the digital divide, while Canada bodies like ISED fund 5G and AI research, creating a robust infrastructure foundation for market growth.

The U.S. Department of State has stated that the International Technology Security and Innovation Fund nearly USD 500 million, is to promote the development and adoption of trustworthy and secure telecommunications networks to ensure semiconductor supply chain diversification and security. As the semiconductors are the key components in all AI and hybrid intelligence systems, which enable computation, machine learning inference, and sensor integration, this funding directly supports the hardware backbone on which hybrid intelligence operates. Furthermore, the National Science Foundation directs hundreds of millions in funding towards human-AI interaction research, as detailed on the NSF. Data from the FCC shows that accelerated mid-band spectrum auctions have facilitated the dense, low-latency networks required for real-time hybrid intelligence applications, making technologies like autonomous logistics and remote surgery increasingly viable.

The hybrid intelligence market in Canada fueled by the strong public policy aimed at ethical AI and bridging digital divides. The application of hybrid systems in natural resource management and public health is the key driver for the market growth, leveraging the country’s strengths. According to the government of Canada data in October 2025, the revenue size of the ICT sector reached USD 298 billion in 2024, driving automation and enhanced decision-making in various sectors. The cloud migration is the key trend in the market, and companies are actively adopting cloud native in their business for data management, and the adoption rate is set to rise with the rise in the hyperscale data center deployments. Federal investment in Gen AI, provincial digital ID mandates, and support for electronic records and telehealth to redefine the market landscape. Government spending follows digital transformation and citizen-facing service modernization, as OpenText, Shopify, and major cloud providers expand AI and SaaS offerings, surging the market-driven product innovation.

APAC Market Insights

Asia Pacific is experiencing the fastest growth rate during the forecast period 2026 to 2035 and is expected to grow at a CAGR of 12%. The market is propelled by the massive government digitalization initiatives and rapid AI adoption across healthcare and manufacturing. Integration of AI with IoT in the smart factories and the push for sovereign AI capabilities are the drivers driving the market. Recent developments in the region, such as, for example, in July 2025, BDx Data Centers has announced its launch in Southeast Asia’s first hybrid quantum AI testbed in Singapore. The launch aims to support enterprises, government agencies, and start-ups in enhancing the AI-quantum innovation. National strategies, such as Japan's Society 5.0 and China's Made in China 2025, are funneling significant state investment into the underlying ICT infrastructure, making APAC the fastest-growing market for hybrid intelligence solutions.

Government led initiative are driving the Japan’s market to overcome the demographic challenge and boost productivity. The Ministry of Economy, Trade and Industry is the key player funding the integration of AI and IoT in manufacturing via its Connected Industries policy. The main focus is the healthcare, where the Japan Agency for Medical Research and Development (AMED) actively promotes AI-driven drug discovery and diagnostic tools to support an aging society. According to METI April 2024 data, the Japan government has allocated nearly ¥72.5 billion specifically for AI research and development, underscoring its key commitment to making Japan a leader in applied, human-centric AI solutions that augment the workforce rather than replace it.

The vast digital public infrastructure in India is the primary driver in India, fueling the hybrid intelligence market. Further, creating a scalable solution for a variety of industries, including agriculture and multilingual citizen services, is the main goal fueling the demand. The PIB report on transforming India with AI data released in October 2025 depicts that the government has approved an initial outlay of over ₹10,300 crore for the IndiaAI Mission for 2024-2025, aimed at bolstering computing infrastructure and foundational AI models. The report further states that AI adds USD 1.7 trillion to India’s economy by 2035. This investment is designed to catalyze both public sector innovation and private enterprise development. With a growing developer base and robust policy support, India is positioned as a key driver of hybrid intelligence innovation in the Asia-Pacific region.

Europe Market Insights

The hybrid intelligence market is defined by a strong, regulatory-driven, and ethically focused approach to adoption driven by significant public investment. The EU market creates a standardized legal framework that mandates human oversight for high-risk AI systems, thereby structurally embedding hybrid models into the region's digital economy. The European Commission's Digital Europe Programme, which has set aside large sums of money expressly for the deployment of AI throughout member states, supports this regulatory push by fostering innovation through a network of European Digital Innovation Hubs. The key demand is based on the region's advanced industrial and manufacturing base, mainly in Germany and the Nordic countries. These countries are leading in hybrid intelligence as they are advancing Industrie 4.0 initiatives, optimizing supply chains, and enhancing precision in sectors like automotive and pharmaceuticals. This combination of top-down governance and bottom-up industrial application creates a stable, high-value market environment.

Germany holds the highest revenue share in the Europe market, and the dominance is propelled by the largest manufacturing and industrial base. Germany is leading in the Industrie 4.0 initiative and provides high-value applications for the collaboration of AI and humans in predictive maintenance and robotic process automation. The government actively fuels the demand via the updated AI strategy, which is administered by the Federal Ministry for Economic Affairs and Climate Action. This technique has committed over €5 billion in public funding for AI research and application, as per the European Commission data in September 2021. The EU's Digital Europe Programme, which supports a network of European Digital Innovation Hubs (EDIHs), including several in Germany, to assist SMEs in adopting AI, amplifies this state-level support. Furthermore, industry associations like Bitkom report that over half of German industrial companies are already implementing or planning AI projects, creating a massive and mature domestic market for hybrid solutions.

The UK is expected to be the second-largest market in Europe and is driven by its strategic focus on AI research in the life sciences and financial services sectors. The UK government's approach that is coordinated by the Department for Science, Innovation & Technology (DSIT), has made significant financial commitments, which are allocated for compute infrastructure as part of its National AI Strategy. This investment is mainly designed to build the foundational capacity that is needed for developing and scaling complex hybrid intelligence models. A less centralized regulatory framework following Brexit also strengthens the UK's competitive advantage, potentially enabling quicker adoption in fields like autonomous financial trading and AI-assisted medicinal research.

Key Hybrid Intelligence Market Players:

- IBM (USA)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Google (Alphabet Inc.) (USA)

- Microsoft (USA)

- Amazon Web Services (AWS) (USA)

- NVIDIA (USA)

- Salesforce (USA)

- SAP (Germany)

- Siemens (Germany)

- Bosch (Germany)

- ABB (Switzerland/Sweden)

- SAS Institute (USA)

- Oracle (USA)

- Intel (USA)

- Accenture (Ireland)

- C3.ai (USA)

- Samsung SDS (South Korea)

- NEC Corporation (Japan)

- Fujitsu (Japan)

- Tata Consultancy Services (India)

- Infosys (India)

- In the hybrid intelligence market, IBM uses its Watson platform to create an AI-powered decision support system. The company integrates its hybrid cloud infrastructure with advanced natural language processing to help human experts in fields such as drug discovery and supply chain management analyze the datasets. In 2024, the company generated a revenue of USD 62.8 billion.

- Google integrates AI across its core services and is the dominant player in the market. Its strategic initiative aims to develop tools such as Vertex AI and TensorFlow that enable businesses to build custom human-in-the-loop systems. Google promotes the collaborative ecosystem by improving areas like intelligent search and autonomous systems with human feedback.

- Microsoft leads the hybrid intelligence market by offering via Azure AI and its Copilot ecosystem. These initiatives are designed to augment human productivity by integrating AI assistants directly into tools such as GitHub, Dynamics 365, and Microsoft 365. This method makes professionals focus on the complex task as AI can handle the regular tasks.

- AWS propels the hybrid intelligence market by making advanced machine learning accessible via its vast cloud infrastructure. Services such as SageMaker, which is used for building models and Augmented AI for easily integrating human review, AWS enables companies to automate the process while ensuring critical decisions are validated by humans.

- NVIDIA provides critical software and hardware for complex AI computation and is the foundational player in the hybrid intelligence market. Its CUDA and GPUs platform are industry standards for training the deep learning models that power hybrid systems. The annual report of the company states that the revenue increased by 126% in 2024.

Here is a list of key players operating in the global hybrid intelligence market:

The hybrid intelligence market is highly competitive and is dominated by the leading U.S. tech giants, and is diversified by the leaders from Japan and Europe. Giant players are following a dual strategy of technological integration and strategic partnerships. Companies are actively focusing on AI integration within the existing systems and enterprise software to create a seamless human-AI collaborative environment. Additionally, acquiring AI startups and establishing industry-specific partnerships are typical strategies to obtain specialized personnel and technology with the goal of providing tailored, scalable solutions that enhance human decision-making in the manufacturing, finance, and healthcare sectors. For example, in November 2025, Capgemini announced the acquisition of Cloud4C, which is a leading provider of automation-driven services for hybrid, private and public cloud environments. This race is defined by creating the intuitive and powerful synergy among human intuition and artificial cognitive power.

Corporate Landscape of the Hybrid Intelligence Market:

Recent Developments

- In September 2025, Digital Realty, the largest global provider of cloud- and carrier-neutral data center, colocation, and interconnection solutions, has announced its launch of its Innovation Lab to accelerate AI and hybrid cloud implementation.

- In August 2025, UMNAI Beta has launched a pioneering hybrid intelligence framework, which is a change in the evolution of AI technology, fusing the power of neural networks with human-understandable logic, unlocking a new generation of AI solutions that vault beyond the limitations of current AI.

- In June 2025, HPE reimagines the hybrid IT operations with GreenLake Intelligence. The GreenLake Intelligence transforms the GreenLake cloud into an agentic-AI-powered hybrid cloud, which is capable of learning, acting, and optimizing IT in real time.

- Report ID: 8248

- Published Date: Nov 19, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.