Hip Replacement Market Outlook:

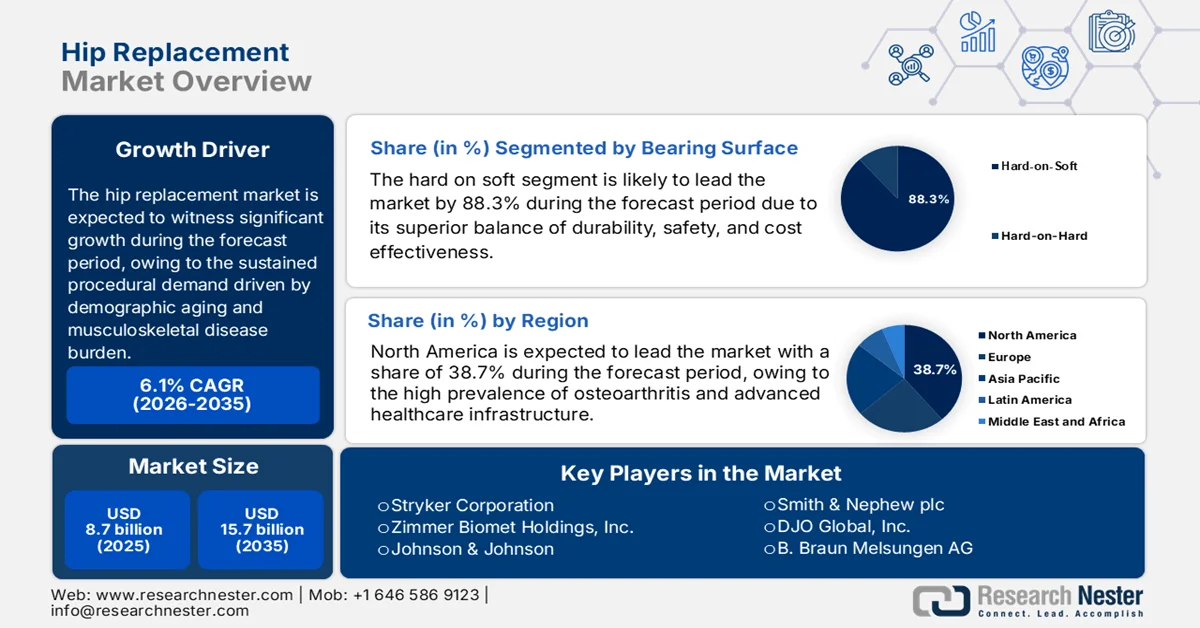

Hip Replacement Market size was valued at USD 8.7 billion in 2025 and is projected to reach USD 15.7 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of hip replacement is evaluated at USD 9.2 billion.

The market is driven by the sustained procedural demand driven by demographic aging, musculoskeletal disease burden, and public healthcare financing capacity. According to the OECD November 2023 data, nearly 172 per 100,000 population have undergone hip replacement, and 119 per 100 000 for knee replacement. These surgeries are projected to rise steadily with the rising elderly population. Moreover, osteoarthritis remains the dominant driver for the market growth. As per the article published by WHO in June 2023, 70% of women are living with rheumatoid arthritis, and 55% are aged above 55. The continued migration of hip replacement procedures to outpatient and short-stay settings is aligned with CMS site-of-care payment reforms, influencing procurement strategies toward standardized implants, bundled pricing, and long-term supplier contracts.

Hip Replacement Surgery in 2022

|

Country |

Hip Replacements per 100 000 Population |

|

Germany |

326 |

|

UK |

175 |

|

Switzerland |

338 |

|

Austria |

302 |

|

Denmark |

283 |

|

France |

256 |

Source: OECD November 2023

Further, the market activity mirrors the public investment trends in aging care and mobility preservation. According to the World Health Organization data in July 2022, musculoskeletal conditions are the leading contributors to years lived with disability worldwide, affecting 1.7 billion people, creating a sustained surgical demand in both the emerging and developed health systems. On the other hand, countries such as Germany UK, and France are performing a high rate of hip replacement surgeries largely financed via public insurance models. Additionally, national health systems across Europe continue to allocate increasing proportions of hospital capital budgets to orthopedic capacity expansion. Collectively, these data indicate the market has long-term growth and is primarily shaped by government spending trajectories, procedural throughput, and hospital purchasing consolidation rather than discretionary demand cycles.

Key Hip Replacement Market Insights Summary:

Regional Highlights:

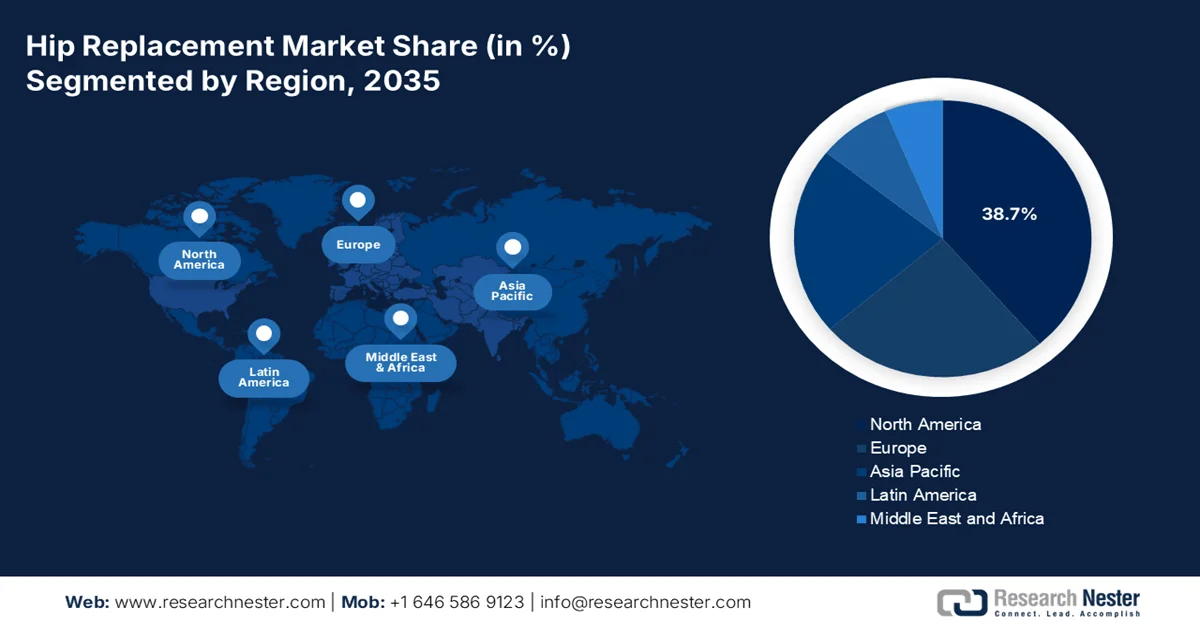

- North America in the hip replacement market is projected to secure a 38.7% revenue share by 2035, fueled by the high prevalence of osteoarthritis and early adoption of robotic-assisted surgery and advanced bearing technologies.

- Asia Pacific is anticipated to register a CAGR of 7.8% during 2026–2035, stimulated by a massive aging population and expanding government initiatives to enhance healthcare access.

Segment Insights:

- The hard-on-soft bearing surface segment of the hip replacement market is projected to account for 88.3% share by 2035, attributed to the superior balance of durability, safety, and cost effectiveness enabled by highly cross-linked polyethylene advancements.

- The primary hip replacement segment is anticipated to witness robust expansion during 2026–2035, propelled by the rapidly aging global population and rising prevalence of osteoarthritis.

Key Growth Trends:

- Rapid population aging and public geriatric care budgets

- Rising hip fracture incidence and public trauma care spending

Major Challenges:

- Stringent regulatory hurdles and costly approval pathways

- High costs of R&D and surgical robotics integration

Key Players: Stryker Corporation, Zimmer Biomet Holdings, Inc., Johnson & Johnson, Smith & Nephew plc, DJO Global, Inc., B. Braun Melsungen AG, Medtronic plc, MicroPort Scientific Corporation, Exactech, Inc., Corin Group, Waldemar Link GmbH & Co. KG, Baumer SA.

Global Hip Replacement Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 8.7 billion

- 2026 Market Size: USD 9.2 billion

- Projected Market Size: USD 15.7 billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, Canada

- Emerging Countries: China, India, Brazil, South Korea, Mexico

Last updated on : 12 February, 2026

Hip Replacement Market - Growth Drivers and Challenges

Growth Drivers

- Rapid population aging and public geriatric care budgets: Population aging is the most structural demand driver for hip replacement procedures. According to the United Nations June 2023 report, the global population aged above 65 will rise from 761 million in 2021 to 1.6 billion by 2050 with the fastest growth occurring in Europe and Asia. Older populations exhibit a higher prevalence of hip osteoarthritis and fracture risk, directly increasing the surgical demand. The governments are responding via expanded aging care budgets. Moreover, the public health expenditure for elderly people is higher with the orthopedic surgery embedded in chronic disease and disability budgets. Further, Japan allocates a significant percentage of total healthcare spending to the elderly population.

- Rising hip fracture incidence and public trauma care spending: Hip fractures, mainly among the older adults, are a significant driver of the emergency hip replacement demand. The NLM study in June 2023 on the analysis of the global hip fracture study shows that the global hip fracture rate is estimated to be 14.2 million, driven by the aging population. Moreover, the CDC January 2026 data depict that hip fractures account for over 300,000 U.S. hospitalizations annually among adults aged above 65, with Medicare covering the majority of surgical costs. Further, the governments increasingly classify hip fracture surgery as a time-critical intervention in terms of funding. Additionally, expanded public trauma networks and bundled payment models for fracture care are accelerating rapid surgical intervention rates, directly supporting sustained procedural volumes for hip replacement implants in publicly funded health systems.

- Rising technological advancements and innovations: Advancements in implant design and system integration are shaping demand in the market by improving the clinical outcomes, procedural efficiency, and suitability. The August 2022 launch of Exactech’s Spartan Stem and Logical Cup System highlights the market shift toward modular streamlined implant systems designed to support reproducible outcomes and efficient surgical workflows which are increasingly valued by hospitals operating under efficient surgical workflows which are increasingly valued by the hospitals operating under bundled payment and cost-containment models. Similarly, Smith+Nephew’s August 2023 launch of the OR3O Dual Mobility System in India reflects rising global adoption of dual mobility technology to address instability and dislocation risk, one of the costliest complications in hip arthroplasty. These innovation shows an active market growth.

Challenges

- Stringent regulatory hurdles and costly approval pathways: Entering the market requires navigating the extensive regulatory frameworks, such as the FDA and MDR. These processes demand multi-year clinical trials proving safety and efficacy, costing millions and creating a formidable barrier. Moreover, the implementation of the EU MDR caused significant backlogs, delaying the market access for all manufacturers. Further, the smaller innovators spent nearly a decade gaining U.S. FDA approval for their optimized positioning system, a testament to the resource-intensive journey.

- High costs of R&D and surgical robotics integration: Innovation is capital-intensive, mainly with the market shift towards robotic-assisted surgery. Developing a new implant system alone is costly, but creating a competitive robotic platform requires billions in R&D. New entrants lack the scale for such investment. Further, the top players entered the robotic space with significant and sustained investment and strategic acquisitions, highlighting the high financial barrier.

Hip Replacement Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 8.7 billion |

|

Forecast Year Market Size (2035) |

USD 15.7 billion |

|

Regional Scope |

|

Hip Replacement Market Segmentation:

Bearing Surface Segment Analysis

Within the hip replacement market, the hard-on-soft bearing surface is the dominant and the fastest growing sub-segment projected to hold a share value of 88.3% by 2035. The segment is driven by the comprising metal or ceramic femoral heads articulating against the advanced polyethylene liners dominates due to its superior balance of durability, safety, and cost effectiveness. The critical innovation is the development of highly cross-linked polyethylene, which reduces the wear particle generation, which is the primary cause of osteolysis and implant failure, compared to the traditional materials. Further, the NLM study in June 2025 has concluded that the hard-on-soft bearing combination is safe to use, and longer follow ups is required. Additionally, this bearing configuration benefits from broad surgeon familiarity, easier revision options, and consistent clinical outcomes across diverse patient populations, further reinforcing its widespread adoption in both primary and revision hip arthroplasty.

Procedure Segment Analysis

The primary hip replacement is leading the procedure segment in the market and is driven by the rapidly aging global population and the rising prevalence of osteoarthritis, coupled with the expanding surgical indications to include the younger and more active patients seeking improved quality of life. The growth is further stimulated by the shift towards minimally invasive surgical techniques and outpatient surgery centers, which reduce the costs and improve the recovery times, hence making the procedure accessible to a broader patient base. As per the article published by the WHO in July 2023, nearly 528 million people globally are living with osteoarthritis, raising the volume of hip arthroplasty procedures and highlighting the sustained demand.

Fixation Type Segment Analysis

The cementless fixation is leading the segment in the hip replacement market. The segment is driven by the long-term stability and bone-preserving benefits. This press fit technique allows for biological fixation where the patient’s bone grows into a porous coating on the implant, creating a durable, lasting interface. Its dominance is fueled by the demographic shift towards younger arthroplasty patients who require implants that can last decades and withstand higher activity levels. Cementless stems also facilitate faster operative times in outpatient settings by eliminating the step of cement preparation and curing. According to the NLM study in August 2022, the use of cementless fixation in total hip arthroplasty cases was nearly 91%, indicating the rising demand in the sector.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Material |

|

|

Fixation Type |

|

|

End user |

|

|

Bearing Surface |

|

|

Procedure |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Hip Replacement Market - Regional Analysis

North America Market Insights

North America market is dominating and is poised to hold the regional revenue share of 38.7% by 2035. The market is driven by the high prevalence of osteoarthritis, advanced healthcare infrastructure, and early adoption of premium technologies such as robotic-assisted surgery and advanced bearing surfaces. The key drivers include the shift to outpatient ambulatory surgical centers to control costs, a well-established value-based care framework via CMS models, and a growing active aging population demanding improved mobility. The U.S. and Canada are driving the growth of the market. Moreover, the Medicare and provincial health reimbursement support for total joint arthroplasty, coupled with structured elective surgery backlog reduction programs, is reinforcing procedural volumes across both inpatient and ASC settings.

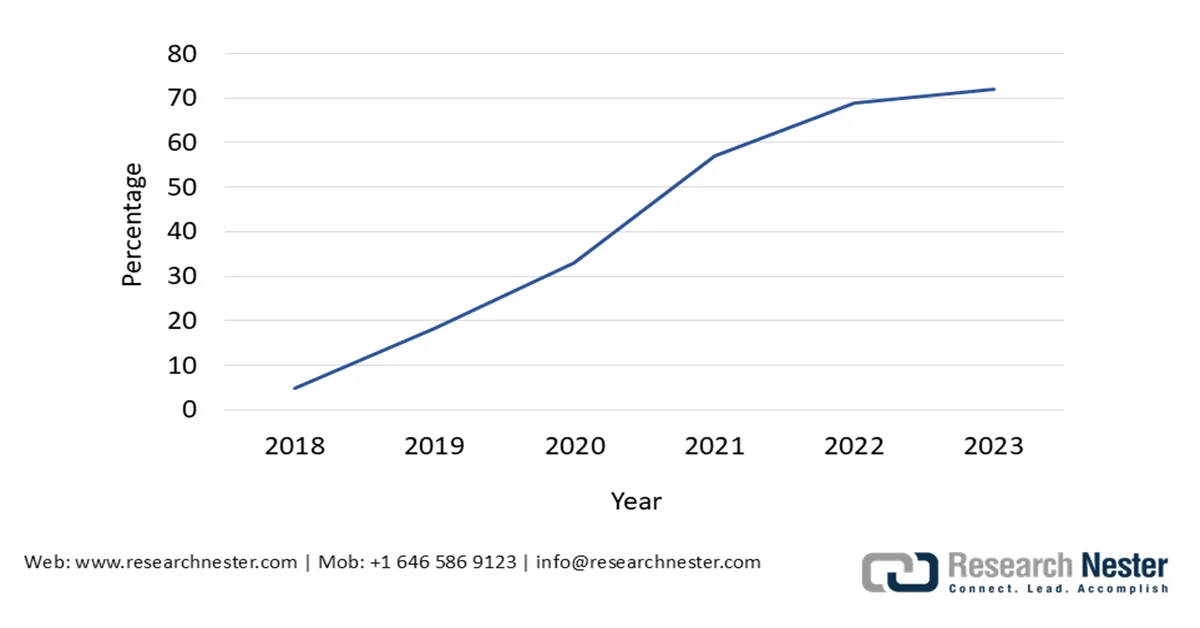

Strong procedure volumes, public reimbursement stability, and demographic pressure are actively shaping the market in the U.S. According to the American Academy of Orthopedic Surgeons, November 2025 data, the U.S. performs over 4 million total hip and knee replacement procedures annually, with volumes remaining structurally elevated post-pandemic due to deferred elective care recovery. Moreover, the AAHKS data in September 2024 indicates that the percentage of Medicare joint replacements in the hospital outpatient facilities increased from 14% to 72% in 2023, reflecting the removal of hip arthroplasty from the inpatient-only list and favoring cost-efficient delivery models. Collectively, these factors underpin sustained U.S. market growth driven by government reimbursement, site-of-care optimization, and aging-related demand rather than discretionary utilization.

Percentage of Medicare Joint Replacements in Outpatient

Source: AAHKS September 2024

Publicly funded procedure volumes, bundled payment structures, and targeted government investments to address surgical backlogs are shaping the hip replacement market in Canada. According to the NLM March 2025 study, approximately 110,000 hip and knee replacement procedures were performed in Canada, underscoring the essential and non-deferrable nature of joint arthroplasty within the public healthcare system. Moreover, the U.S. government health data indicates a 71% increase in total hip arthroplasty volumes by 2030, a trend that closely mirrors Canada’s aging demographics and osteoarthritis prevalence. Further, the NLM October 2025 study depicts that the bundled pricing frameworks, such as an introductory USD 9,630.84 bundle price for total hip arthroplasty, highlight government efforts to control episode-of-care spending while maintaining access. These data show a stable and policy-driven growth in the Canadian market.

APAC Market Insights

The Asia Pacific hip replacement market is the fastest-growing market and is expected to grow at a CAGR of 7.8% during the forecast period 2026 to 2035. This expansion is driven by a massive aging population, rising disposable income, and significant government initiatives to expand healthcare access. The key trends include the rapid development of medical tourism hubs in Thailand and India, the expansion of universal health coverage schemes, and the increasing localization of manufacturing to reduce costs. Moreover, the market is highly fragmented with a stark and high-volume cost-sensitive demand in emerging economies. The region's growth is also propelled by increasing obesity rates and a cultural shift towards addressing mobility issues in the elderly.

The hip replacement market in India is expanding steadily and is driven by rising osteoarthritis prevalence, demographic aging, and increasing government investment in the tertiary care orthopedic infrastructure. According to the NLM March 2024 study, nearly 4.7 million deaths and 226.8 million disability-adjusted life years were attributed to non-communicable disease in India, with musculoskeletal disorders recognized as a growing contributor to disability. Moreover, the PIB October 2025 data reports that the population aged 60 years and above is expected to reach over 230 million by 2036, expanding the pool of patients requiring mobility-restoring interventions such as hip replacement. Additionally, Government of India health expenditure increased to approximately 2.5% of GDP in 2025, strengthening the surgical capacity in state-run medical colleges and district hospitals, based on the PIB January 2023. Collectively, these factors are positioning India as a high-volume, government-supported growth market for hip replacement procedures.

The hip replacement market in China is expanding rapidly and is supported by demographic aging, rising osteoarthritis prevalence, and sustained government investment in hospital-based surgical capacity. According to the People’s Republic of China data in October 2024, the population aged 60 years and above exceeded 297 million in 2023, accounting for over 21.1% of the total population, significantly increasing age-related joint degeneration and fracture risk. The demand is further supported by the policy expansion under the Basic Medical Insurance system, which covers over 95% of the population and reimburses the total hip arthroplasty across urban and rural schemes based on the Frontiers study in December 2023. Additionally, the musculoskeletal conditions are among the leading causes of disability in China, reinforcing government prioritization of mobility-restoring interventions. These factors collectively underpin strong policy-driven growth in China’s market.

Europe Market Insights

The market in Europe is defined by the advanced and cost-conscious healthcare system. The market is expanding significantly with the aging population and a high prevalence of osteoarthritis. The market is highly regulated under the EU Medical Device Regulation, which ensures safety and a robust product approval and innovation speed. The key drivers include government led initiative to reduce the orthopedic surgery waiting lists, which spurred the gradual adoption of value-based healthcare models that prioritize the long term patient outcomes and cost efficiency over the immediate device price. The growth is mainly driven by the stringent price negotiations from national health services and payer organizations, leading to a competitive environment where demonstrating superior clinical and economic value is paramount for market success.

The market in Germany is strongly supported by a high osteoarthritis disease burden and elevated procedure rates funded via statutory health insurance. According to the NLM November 2023 study, nearly 80% of the people with symptomatic osteoarthritis experience limited mobility, while 25% are unable for the normal daily activities. This data shows the clinical and functional need for definitive interventions, such as total hip arthroplasty, rather than prolonged conservative management. This burden translates into high surgical utilization in Germany. Moreover, the NLM study in April 2023 shows that Germany recorded over 300.8 total hip replacements per 100,000 population in 2021, reflecting strong access to reimbursement coverage and hospital capacity. Further, as population aging continues and mobility preservation remains a public health priority, these factors collectively support stable volume-driven growth in the market in Germany.

The rising procedure volumes in the centrally funded system, along with the persistent regional and socioeconomic variation in access is driving the hip replacement market in UK. As per the NLM April 2023, the rate of hip replacement increased from 27 to 36 procedures per 10,000 person-years, reflecting the sustained growth in the demand driven by aging and osteoarthritis burden. Moreover, the mean patient age of 70 years, with 60% female representation, aligns closely with the demographic risk profiles and reinforces a long-term procedural demand. Further, the clinical Commissioning Groups (CCGs) serving less deprived populations demonstrate higher procedure rates, highlighting capacity and referral variability rather than budget withdrawal. These trends indicate that government-funded volumes continue to expand, further increasing hip arthroplasty activity over the medium term, supporting stable implant demand across the UK.

Key Hip Replacement Market Players:

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Smith & Nephew plc (UK)

- DJO Global, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Medtronic plc (Ireland)

- MicroPort Scientific Corporation (China)

- Exactech, Inc. (U.S.)

- Corin Group (UK)

- Waldemar Link GmbH & Co. KG (Germany)

- Baumer SA (Brazil)

- Japan Medical Dynamic Marketing (JMDM) (Japan)

- Kyocera Corporation (Japan)

- LimaCorporate S.p.A. (Italy)

- Tecomet, Inc. (U.S.)

- Elite Surgical Supplies (PTY) Ltd (South Africa)

- Meril Life Sciences Pvt. Ltd (India)

- Samyang Holdings Corp. (South Korea)

- Orthocare Innovations (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Stryker Corporation is a dominant player in the market, largely driven by its active acquisition of surgical corporations. Their key strategic initiative is the integration of the robotic arm-assisted surgery with their proprietary implants. This creates a premium data-driven ecosystem where surgeons can pre-plan the procedures and execute with enhanced precision, improving the outcomes.

- Zimmer Biomet Holdings, Inc. maintains a leading position in the hip replacement market via a dual strategy of comprehensive portfolio breadth and technological integration. Their strategic initiative focuses on delivering intelligent orthopedics exemplified by the robotic surgical system. Moreover, by combining the data analytics and robotic platform, they aim to optimize the surgical workflow and patient recovery, securing their role as a full solutions provider.

- Johnson & Johnson competes at the forefront of the hip replacement market via its subsidiary DePuy Synthes. A core strategic initiative is the expansion of its VELYS Digital Surgery platform. This focus on connected digital ecosystems along the advanced bearing surfaces, such as the ceramic and highly cross-linked polyethylene, aims to improve the surgical predictability, implant longevity, and overall value-based care.

- Smith & Nephew plc differentiates itself in the hip replacement market with a strong focus on minimally invasive surgery and advanced bearing technology. Their strategic initiatives are centered on the Real Intelligence suite, which combines the surgical system materials and the acetabular system. By promoting bone conservation, reducing wear, and enabling efficient same-day discharge pathways, they target the growing demand for value-based outpatient joint replacement procedures.

- DJO Global, Inc., is a major player in the broader orthopedic rehabilitation holds a significant position in the hip replacement market via its surgical division. Their strategic initiative emphasizes innovation in implant materials and smart instrumentation. The Acetabular Cup system and proprietary cross-linked polyethylene liners are designed for stability and longevity, supported by surgical tools that enhance accuracy, appealing to surgeons seeking reliable, high-performance implant systems.

Here is a list of key players operating in the global market:

The global hip replacement market is dominated by the multinational giants with the top players holding a significant majority share. The competition is intense driven by the continuous innovation in materials, robotic-assisted surgical platforms, and value-based care models. The key strategic initiatives include heavy investment in R&D for premium durable implants, strategic acquisition to expand the product portfolios and geographic reach, and the development of integrated digital surgery ecosystems that combine implants, instrumentation, and data analytics to improve the surgery outcomes and hospital efficiency. For example, in March 2024, Stryker announced that it had completed the announced acquisition of SERF SAS, a France-based joint replacement company, from Menix.

Corporate Landscape of the Hip Replacement Market:

Recent Developments

- In October 2025, Zimmer Biomet Holdings, Inc., announced the U.S. Food and Drug Administration (FDA) has granted Breakthrough Device Designation for the company's first-to-world iodine-treated total hip replacement system. This is the first product in Zimmer Biomet history to receive this designation.

- In June 2025, Johnson & Johnson MedTech, announced the launch of the KINCISE Surgical Automated System, which is a next-generation automated power tool engineered to improve surgical efficiency, provide control, and aims to reduce physical burden on surgeons compared to manual impaction across both primary and revision hip and revision knee replacement procedures.

- In December 2024, Smith+Nephew announced that its CORIOGRAPH Pre-Op Planning and Modeling Services are now cleared for total hip arthroplasty (THA) by the United States Food and Drug Administration.

- In December 2024, OrthAlign, Inc. announced a significant milestone with the successful first clinical use of its Lantern Hip handheld technology. The procedure was performed by Edwin Su, MD, a renowned orthopedic surgeon at the Hospital for Special Surgery (HSS) in New York, NY.

- Report ID: 4440

- Published Date: Feb 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.