Grouting Materials Market Outlook:

Grouting Materials Market size was valued at USD 7.1 billion in 2025 and is expected to surpass a value of USD 10.2 billion by the end of 2035, expanding at a CAGR of 4.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of grouting materials is assessed at USD 7.4 billion.

The heightened demand arising from construction, infrastructure, and industrial sectors is responsible for the uplift of the grouting materials market. Public infrastructure funding increases construction activity, requiring grouting for structural support, crack injection, and void filling across public works. For example, the U.S. Geological Survey (USGS) revealed that in January 2025, total U.S. shipments of portland and blended cement, including imports, were 5.73 million tons, and Type IL (portland-limestone cement) accounted for 96 % of blended cement tonnage, primarily supplied for Texas. The report also stated that clinker production, excluding Puerto Rico, totaled 4.27 million tons, with Missouri, California, Texas, Florida, and Michigan as the top producers. Hence, this significant production and shipment volume underscores the strong upstream supply supporting grouting materials over the years ahead.

Monthly Portland and Blended Cement Shipments by U.S. Districts (January-July 2024) - Key Regional Volumes

|

District |

January (Metric Tons) |

April (Metric Tons) |

July (Metric Tons) |

|

New England & Middle Atlantic |

245,228 |

422,005 |

431,939 |

|

East North Central |

288,885 |

734,341 |

921,022 |

|

West North Central |

509,389 |

1,376,526 |

1,538,139 |

|

South Atlantic |

1,096,332 |

1,351,470 |

1,263,946 |

|

East South Central |

426,003 |

654,163 |

607,586 |

|

West South Central |

800,200 |

1,142,489 |

1,177,780 |

|

Mountain and Pacific |

1,245,308 |

1,628,993 |

1,663,419 |

|

U.S. Total |

4,611,344 |

7,309,986 |

7,603,831 |

Source: USGS

In terms of raw material supply chain and trade, cement, polymers, and epoxy resins are the important inputs for grouting materials. In this context, in May 2025, the official statistics, which were published by the U.S. International Trade Commission (USITC) show that China has rapidly shifted to become a major net exporter of epoxy resins, with its export-to-import ratio rising from 32.1% in 2021 to 162.6% in the first quarter of 2024, which underscores that there is a strong export focus. In addition, the trade data also suggests some epoxy resin imports labeled as Canada-based are actually transshipments originating from China, supported by a 104% increase in Canada’s imports from 2021 to 2023 and communications indicating China’s products are routed through Canada before entering the U.S. market. Hence, these dynamics reflect the growing prominence of China as a key exporter, benefiting the overall grouting materials market.

Key Grouting Materials Market Insights Summary:

Regional Highlights:

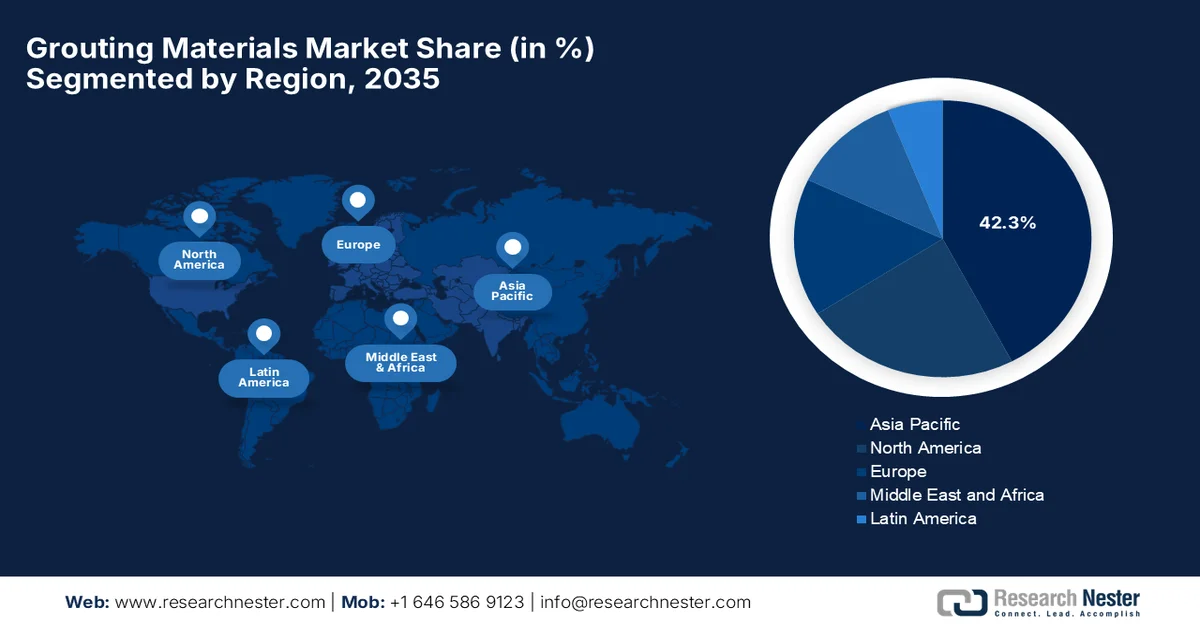

- The asia pacific grouting materials market is anticipated to hold a 42.3% share by 2035, driven by rapid urbanization and extensive infrastructure development across emerging economies

- North America is expected to witness notable growth through 2035, fueled by strong focus on infrastructure modernization and renovation of aging buildings

Segment Insights:

- The epoxy-based grouts segment in the grouting materials market is projected to account for a 54.4% share by 2035, propelled by superior mechanical strength, chemical resistance, and long-term durability

- The cementitious grout segment is anticipated to capture a significant revenue share by 2035, driven by rising adoption in structural repair, foundation stabilization, and tunnel construction projects

Key Growth Trends:

- Infrastructure development and construction boom

- Sustainability and regulatory trends

Major Challenges:

- Environmental regulations and emission standards

- Supply chain disruptions

Key Players: Sika AG, BASF SE, Master Builders Solutions Holdings GmbH, MAPEI S.p.A., Fosroc International Limited, Saint-Gobain Weber, Ardex Group, Five Star Products, Inc., LATICRETE International, Inc., The Euclid Chemical Company, GCP Applied Technologies Inc., W. R. Meadows, Inc., Custom Building Products, Holcim Group, CEMEX S.A.B. de C.V., Normet Group, Pidilite Industries Limited, MYK LATICRETE India Pvt. Ltd., Sika Australia Pty Ltd, Vortex Companies, Kyung-In Synthetic Co., Ltd.

Global Grouting Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 7.1 billion

- 2026 Market Size: USD 7.4 billion

- Projected Market Size: USD 10.2 billion by 2035

- Growth Forecasts: 4.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: South Korea, Brazil, United Arab Emirates, Indonesia, Vietnam

Last updated on : 19 March, 2026

Grouting Materials Market - Growth Drivers and Challenges

Growth Drivers

- Infrastructure development and construction boom: The huge rise in investments for infrastructure projects such as highways, bridges, tunnels, dams, and metro lines is increasing demand for grouting materials, which are utilized in soil stabilization, foundation support, and structural reinforcement. In this context, in October 2025, the data, which was kept forward by Voxdev, revealed that infrastructure and construction are vital components for economic growth in certain countries, which accounted for about 50% of total investment, and provided essential networks such as roads, bridges, airports, and social facilities, thereby supporting upstream industries. The report also stated that the construction industry is mostly dependent on foreign contractors for 50% to 75% of large projects, denoting a huge growth potential for the grouting materials market in the years ahead.

- Sustainability and regulatory trends: The emphasis on sustainable construction and environmental regulations has become responsible for shifting demand toward low-VOC and eco-friendly grouting products. Stricter building codes mandating safety and structural integrity also encourage the use of grouting solutions, prompting a favorable ecosystem for the grouting materials market. In June 2024, the article, which was published by the World Economic Forum, stated that green building strategies across the building value chain can reduce more than 80% of emissions and unveil a total of USD 1.8 trillion market opportunity by 2030, particularly with China, the largest construction sector, which is leading sustainable practices. It also stated that key enablers include biomaterials, financing, and regulatory alignment, thereby enabling net-zero, nature-positive, resilient buildings globally.

- Infrastructure repair & maintenance: Aging infrastructure in developed regions is the primary growth driver for grouts in repair, strengthening, and water‑seal applications, rather than only new builds. For instance, in December 2023, Amtrak reported that it had allocated contracts for the replacement of the 117-year-old Susquehanna River Rail Bridge, with a total of USD 2.08 billion in FRA funding. Besides, this particular project includes the construction of two new two-track fixed bridges, modernization of power, signals, and safety systems, and demolition of 10 remnant piers from an 1866 bridge, thereby addressing capacity and reliability constraints on the Northeast Corridor. From a strategic perspective, such instances efficiently drive demand in the grouting materials market in the repair and maintenance projects.

Challenges

- Environmental regulations and emission standards: The regulations that negatively affect the growth of the grouting materials market. The cement production is mostly associated with high carbon emissions, due to which governments across almost all nations are implementing stricter emission standards and environmental compliance requirements. In this context, manufacturers need to make investments in emission-reduction technologies, alternative raw materials, and cleaner production processes with a prime goal of meeting regulatory guidelines. In addition, there are certain restrictions on chemical additives and resin-based materials that may limit formulation options for grouting products. Therefore, these regulatory pressures create operational complexities for manufacturers in this field.

- Supply chain disruptions: The supply chains for construction materials and chemical inputs are highly vulnerable to disruptions, which are mostly caused by geopolitical tensions, transportation issues, and trade restrictions. Also, these grouting materials are dependent on a combination of cementitious binders, mineral fillers, polymers, and specialty chemicals, which need to be sourced from multiple regions. Meanwhile, any disruption in the supply of these components can delay production schedules and increase procurement costs. The aspects of shipping delays, port congestion, and fluctuating freight rates also impact the timely delivery of materials to construction sites. Furthermore, proper maintenance of the supply chain and logistics in the grouting materials market is a critical challenge for manufacturers and distributors.

Grouting Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

4.2% |

|

Base Year Market Size (2025) |

USD 7.1 billion |

|

Forecast Year Market Size (2035) |

USD 10.2 billion |

|

Regional Scope |

|

Grouting Materials Market Segmentation:

Type Segment Analysis

The epoxy-based grouts in the type segment are expected to dominate the entire global dynamics with a share of 54.4% in the grouting materials market during the forecast period. The segment’s dominance is largely attributable to its superior mechanical strength, exceptional chemical resistance, and high durability, offering negligible shrinkage. The epoxy-based grouts also offer excellent bonding that ensures long-term structural integrity under heavy loads and harsh conditions, whereas their waterproofing capability and temperature versatility make them highly suitable for demanding applications. For instance, in March 2025, BASF and Sika together reported that they launched Baxxodur EC 151, which is a new epoxy hardener especially designed for sustainable construction solutions, hence suitable for bolstering the segment’s growth and exposure.

Material Form Segment Analysis

In the material form segment, the cementitious grout is predicted to grow with a considerable revenue share in the grouting materials market by the conclusion of 2035. The strong adoption in structural repair, foundation stabilization, and tunnel construction projects is the main factor driving the subtype’s leadership. As per the National Institute of Health (NIH) article in October 2025, cement-based grouting materials, which are modified with graphene oxide and nano-silica hybrids, significantly enhance mechanical strength, reduce setting time, and improve durability. In addition, the research shows that a low-dosage combination (2 wt% NS + 0.01 wt% GO) increases flexural and compressive strengths by 13.5% and 45.5%, which is due to synergistic effects optimizing hydrate morphology and pore structure. Hence, these findings provide a scientific basis for designing high-strength cementitious grouts for construction and infrastructure applications.

Technology Segment Analysis

By the end of the forecast period, pressure grouting in the technology segment is anticipated to grow with a significant revenue share in the grouting materials market. The subtype’s critical role in foundational and geotechnical engineering is the main factor which responsible for driving its growth. It allows precise placement of grout into voids and soil or rock masses by ensuring deep penetration and uniform consolidation. Besides, the pressure grouting enhances the load-bearing capacity, seismic resilience, and overall stability of structures such as dams, tunnels, and high-rise buildings. In addition, this particular technology is considered to be highly effective in mitigating ground settlement, controlling soil deformation, and waterproofing subterranean structures, making it indispensable for projects that have complex geotechnical concerns. Furthermore, its adaptability to different materials solidifies its dominance, positioning it as the preferred solution for modern large-scale civil infrastructure development.

Our in-depth analysis of the grouting materials market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Material Form |

|

|

Technology |

|

|

Application |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Grouting Materials Market - Regional Analysis

APAC Market Insights

The Asia Pacific grouting materials market is predicted to dominate with the largest revenue share of 42.3% during the stipulated timeframe. The region’s leadership is mainly propelled by rapid urbanization and extensive infrastructure development in emerging economies. The region's growth is also carried forward by the modernization of transport networks, such as high-speed rail and airports. As per the officially reported data in February 2025, a research team from the Shibaura Institute of Technology, Japan, has developed a carbon-neutral grout called colloidal silica, which is recovered from geothermal fluids by repurposing silica-rich waste from geothermal plants into a high-performance soil-stabilizing material. In this context, laboratory tests show 50% greater liquefaction resistance when compared to conventional grouts, with low viscosity and controlled gelling for deep soil penetration, hence denoting a positive outlook for the region’s growth.

The commercial and residential construction growth efficiently fuels the grouting materials market in China. The market is transitioning from a reliance on cementitious grouts toward high-performance chemical and resin-based systems, which is influenced by a focus on manufacturing automation and the need for precision anchoring in industrial facilities. In September 2025, the article published by the International Trade Administration reported that China is the world’s largest construction industry, which was valued at USD 4.82 trillion in 2025, and is shifting toward green, low-carbon building and urban renewal projects. Demand is highly witnessed in Tier 1 cities such as Beijing and Shanghai, driven by sustainable construction and the country’s dual carbon goals of peaking emissions by 2030 and achieving carbon neutrality by 2060. Furthermore, the report states that opportunities exist for green building materials, smart building technologies, and energy-efficient solutions.

In India, the grouting materials market is witnessing exponential growth due to government-led infrastructure initiatives, metro rail expansions, and high-speed road corridors. Cementitious grouts have gained popularity in the country for cost-sensitive projects. In this context, the article published by India Brand Equity Foundation in November 2025 states that the country’s cement industry is poised for robust growth, with demand projected to rise 6% to7% in FY25, which is followed by 453 million tons of production in FY25, up from 426.29 million tons in FY24. Major players such as UltraTech, Ambuja, ACC, and Shree Cement are investing heavily, with USD 14.63 billion planned for capacity expansion between FY25 and FY27, targeting 850 MTPA by 2030. In addition, the Mumbai-Ahmedabad Bullet Train corridor consumes 20,000 cubic meters of cement daily, driving demand along with government allocations of USD 33.08 billion for roads and highways in FY26, hence denoting a huge growth potential for grouting materials.

North America Market Insights

The huge emphasis on infrastructure modernization and the renovation of aging residential and commercial buildings propels the growth of the grouting materials market in North America. Strict building codes are important factors driving the high adoption of epoxy-based grouts in industrial applications due to their superior chemical resistance. There is an increasing preference for pre-mixed grout formulations, which minimize on-site errors and labor requirements. In February 2026, Vortex Companies announced a tactical distribution agreement with Minicam by making Vortex’s MaxLiner division the premier distributor of Minicam’s Dancutter robotic cutting systems, as well as Sewertronics LED UV curing systems for small-diameter rehabilitation. The partnership consolidates sales, service, training, and technical support across MaxLiner’s Charlotte and Orlando locations. Hence, with such developmental strategies by the pioneers, the region is expected to witness extensive growth in the upcoming years.

The advancements in application equipment are enhancing efficiency in commercial construction projects, which is a responsible factor driving the grouting materials market in the U.S. The market is seeing increased adoption of digital and automated solutions, which are aimed at improving precision and mitigating persistent labor shortages. In this context, the U.S. Environmental Protection Agency (EPA) in August 2024, notified a new label program to help federal purchasers identify and buy lower-carbon, climate-friendly construction materials, which include concrete, steel, glass, and asphalt. Besides, this program is supported by the Inflation Reduction Act, and it mainly aims to reduce greenhouse gas emissions from construction materials. Furthermore, federal funding, including USD 2 billion for the Federal Highway Administration, incentivizes the use of clean materials in transportation and building projects, thereby supporting the adoption of sustainable construction products.

Canada grouting materials market is all set to witness solid growth due to a strong focus on infrastructure renewal and heavy industrial applications, especially in the mining and oil and gas sectors, which require specialized ground reinforcement. Demand is highly influenced by government investments through the Canada Infrastructure Bank for projects that involve tunneling, bridge rehabilitation, and seismic retrofitting. Based on the government data, which was published in February 2026, the Canada Infrastructure Bank (CIB) outlined its priorities to accelerate transformative infrastructure projects, committing to make investments in housing, transportation, clean energy, and digital infrastructure while leveraging private capital. Besides, the CIB underscores the adoption of off-site and prefabricated construction methods and low-carbon materials to support sustainable, resilient, and energy-efficient infrastructure. Hence, such initiatives in the country are expected to drive demand for advanced construction materials, including grouting products, across the country’s infrastructure projects.

Europe Market Insights

The grouting materials market in Europe is a highly organized and mature sector, which is primarily shaped by a shift from new construction to the maintenance and retrofitting of historical landmarks. The sustainable, stringent regulations have accelerated the transition toward bio-based resin systems with minimal environmental impact. In September 2024, the European Climate, Infrastructure and Environment Executive Agency (CINEA) notified that it has launched the CEF Transport calls, making a total of USD 2.7 billion available to modernize the Trans-European Transport Network (TEN‑T), covering railways, inland waterways, ports, and roads. The funding supports sustainable, smart, and resilient infrastructure, advancing multimodal transport, safety, and interoperability across the region’s member states and associated countries, hence denoting a positive outlook for the region’s growth.

The grouting materials market in Germany is significantly growing based on innovation, which is currently focused on digitalization, integration of smart monitoring sensors, and automated injection technologies to address high labor costs. The country’s grouting materials market also benefits from the demand for high-performance and early-strength formulations that allow for rapid construction and minimal service disruption in very dense urban areas. In July 2025, the country’s Federal Government released a total of USD 1.2 billion for the renovation of key motorway infrastructure, including USD 430 million for bridge upgrades and USD 780 million for road surfaces linked to bridges and tunnels. The report underscored that this funding enables Autobahn GmbH to immediately award contracts and advance critical construction projects on major routes like the A7 and A3, hence making it suitable for standard market growth.

The demand for high-performance solutions in major rail, tunnel, and energy projects is responsible for uplifting the grouting materials market in the UK. The large-scale public investments and various water management upgrades are also prompting a profitable business environment in the country. Based on the country’s government data, which was published in March 2026, its National Infrastructure and Service Transformation Authority (NISTA) published an updated UK Infrastructure Pipeline, which shows USD 890 billion in planned public and private investment in major infrastructure projects over the next decade, covering transport, energy, utilities, and other civil works across the country. Therefore, this scale of investment highlights that there is a long‑term demand for construction inputs, including grouting materials used in foundations, soil stabilization, tunnel works, and structural rehabilitation.

Key Grouting Materials Market Players:

- Sika AG (Switzerland)

- BASF SE (Germany)

- Master Builders Solutions Holdings GmbH (Germany)

- MAPEI S.p.A. (Italy)

- Fosroc International Limited (UK)

- Saint-Gobain Weber (France)

- Ardex Group (Germany)

- Five Star Products, Inc. (U.S.)

- LATICRETE International, Inc. (U.S.)

- The Euclid Chemical Company (U.S.)

- GCP Applied Technologies Inc. (U.S.)

- W. R. Meadows, Inc. (U.S.)

- Custom Building Products (U.S.)

- Holcim Group (Switzerland)

- CEMEX S.A.B. de C.V. (Mexico)

- Normet Group (Finland)

- Pidilite Industries Limited (India)

- MYK LATICRETE India Pvt. Ltd. (India)

- Sika Australia Pty Ltd (Australia)

- Vortex Companies (U.S.)

- Kyung-In Synthetic Co., Ltd. (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Sika AG is one of the leading manufacturers in the market, which has an extensive product portfolio consisting of cementitious, epoxy, polyurethane, and PMMA-based grout systems. The company operates in many countries and maintains a strong presence in large-scale infrastructure and tunneling projects.

- MAPEI S.p.A. is identified as a major global supplier of specialty construction chemicals and grouting materials, which are widely used in building repair, underground construction, and transportation infrastructure. The firm’s global distribution network and region-specific formulations have helped it expand significantly across Europe, the Middle East, and the Asia Pacific.

- Fosroc International Limited is a prominent player in this field, which supplies construction chemicals, including precision grouting materials. The company has developed strong relationships with engineering, procurement, and construction contractors across different regions, which are allowing it to maintain a strong position on a global scale.

- BASF SE plays a key role in the grouting materials market through its improved construction chemical technologies and specialty admixture solutions. The company offers grout systems under specialized product platforms designed for deep foundation stabilization, mining applications, and infrastructure repair.

- LATICRETE International, Inc. is a central player in this field, and it is a well-known manufacturer of construction chemicals, adhesives, and grout solutions. The company provides epoxy-based, polymer-modified, and cementitious grout products, which are especially designed for structural reinforcement, heavy machinery foundations, and tile installation systems.

Below is the list of some prominent players operating in the global grouting materials market:

The global grouting materials market is consolidated and is led by construction chemical manufacturers that have extensive product portfolios and global distribution networks. Companies such as Sika AG, BASF SE, MAPEI S.p.A., and Fosroc International are maintaining leading market positions, which is facilitated by their presence in large infrastructure projects worldwide. Major firms in this field are highly preferring expansion through mergers and acquisitions, capacity enhancements, and regional manufacturing investments to strengthen supply chains and access emerging markets. In this context, Henkel in July 2025, notified that it has acquired Nordbak (Pty) Ltd, which provides epoxy-based crusher backing, grouting compounds, and others. The acquisition aims to strengthen its adhesive technologies business and expand its maintenance, repair, and overhaul solutions in the region’s mining, infrastructure, and industrial sectors, hence denoting a positive grouting materials market outlook.

Corporate Landscape of the Grouting Materials Market:

Recent Developments

- In February 2026, Vortex Companies rebranded its I & I Guard polyurethane foam grout line as Maverick Grouts. The Maverick Grouts family includes solutions for inflow and infiltration, void filling, soil stabilization, and structural lifting.

- In February 2025, Saint-Gobain reported that it had completed the acquisition of FOSROC, which is a global construction chemicals leader with a strong presence in India, the Middle East, and Asia Pacific. FOSROC offers a wide range of solutions, including concrete admixtures, adhesives, sealants, waterproofing, and flooring.

- Report ID: 4324

- Published Date: Mar 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.