Grid Optimization Solution Market Outlook:

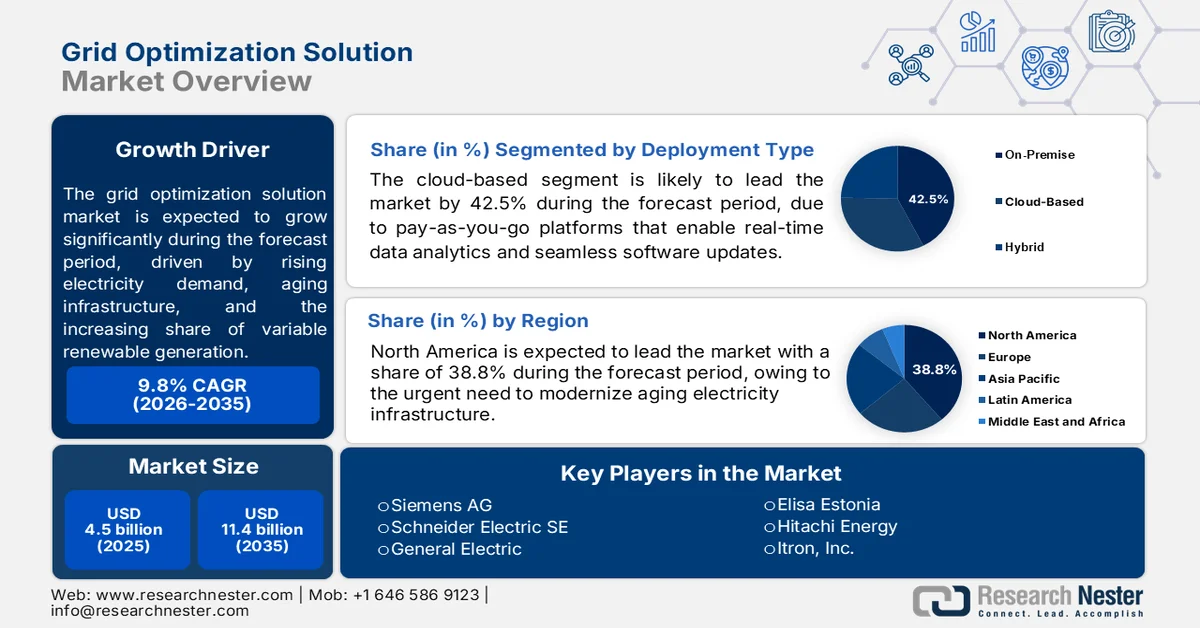

Grid Optimization Solution Market size was valued at USD 4.5 billion in 2025 and is projected to reach USD 11.4 billion by the end of 2035, registering around 9.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of grid optimization solution is evaluated at USD 4.9 billion.

Grid optimization solutions are gaining priority across utility, transmission, and distribution networks as grid operators address rising electricity demand, aging infrastructure, and the growing share of variable renewable generation. According to the U.S. Energy Information Administration (EIA), U.S. utility-scale solar generation increased from approximately 163 billion kWh to more than 238 billion kWh, while wind generation remained above 430 billion kWh, increasing the need for advanced grid planning, congestion management, and network balancing capabilities. The U.S. Department of Energy estimates that electricity demand growth could accelerate significantly over the coming decade due to electrification, industrial expansion, and data-center development.

Market expansion is also supported by reliability and resilience objectives established by governments and energy agencies. The DOE’s 2026 data National Transmission Needs Study estimated that U.S. transmission capacity may need to expand by roughly 60% by 2030 and potentially triple to accommodate projected electricity demand and clean-energy deployment. Utilities and system operators are therefore increasing investments in optimization solutions that support transmission planning, outage management, distributed energy resource integration, voltage control, and real-time operational decision-making. Public-sector funding programs, reliability compliance requirements, and long-term infrastructure expansion plans continue to create a favorable environment for solution providers serving electric utilities, grid operators, and energy infrastructure stakeholders.

Key Grid Optimization Solution Market Insights Summary:

Regional Highlights:

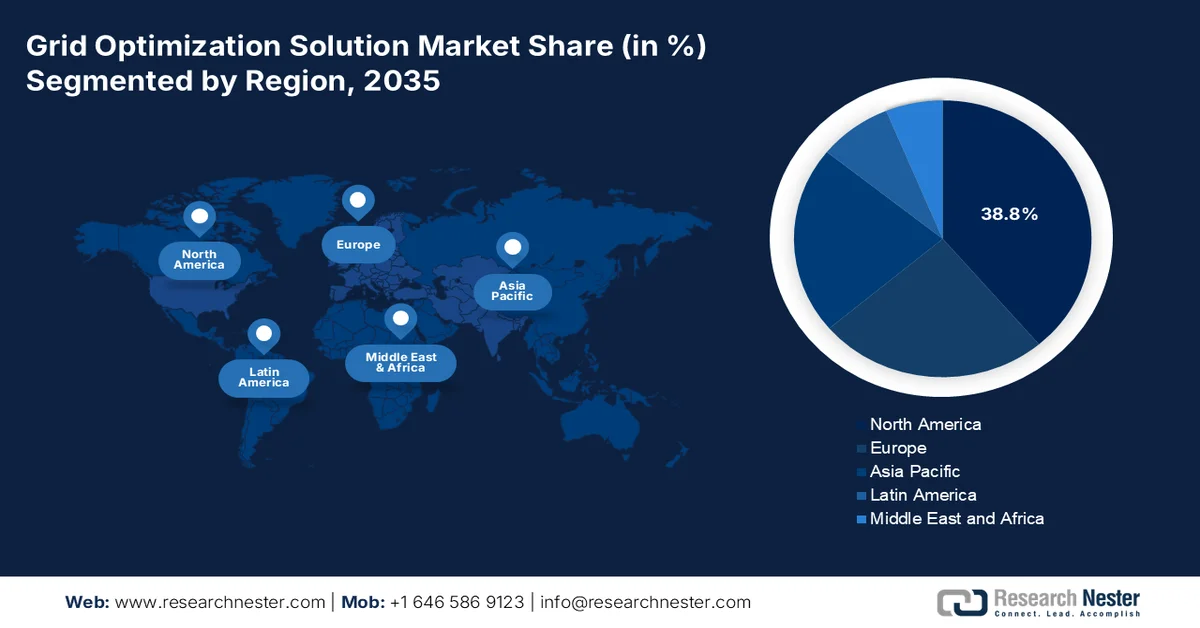

- North America is expected to capture 38.8% share by 2035, reinforced by the modernization of aging electricity infrastructure and the accelerating integration of distributed renewable energy resources

- Asia Pacific is forecast to witness rapid growth in the grid optimization solution market throughout 2026-2035, fueled by rapid urbanization, rising electricity demand, and ambitious renewable energy targets across developed and emerging economies

Segment Insights:

- Cloud Based is projected to account for 42.5% of the grid optimization solution market by 2035, propelled by utilities shifting from legacy on-premise infrastructure to scalable cloud platforms enabling real-time analytics and seamless software updates

- Software Component is anticipated to maintain its leading position throughout the 2026-2035 forecast period, bolstered by the increasing adoption of predictive AI modules for proactive grid asset maintenance and outage prevention

Key Growth Trends:

- Rising government investment in grid modernization programs

- Renewable energy integration

Major Challenges:

- High R&D and capital intensity

- Shortage of skilled workforce with domain expertise

Key Players: Siemens AG, Schneider Electric SE, General Electric, Elisa Estonia, Hitachi Energy, Itron, Inc.

Global Grid Optimization Solution Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.5 billion

- 2026 Market Size: USD 4.9 billion

- Projected Market Size: USD 11.4 billion by 2035

- Growth Forecasts: 9.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, South Korea, Singapore, Saudi Arabia, Brazil

Last updated on : 1 July, 2026

Grid Optimization Solution Market - Growth Drivers and Challenges

Growth Drivers

- Rising government investment in grid modernization programs: Government-led grid modernization spending is a primary demand driver for grid optimization solutions because utilities require advanced planning, monitoring, and operational tools to maximize the value of new infrastructure investments. The IEA July 2023 data depicted that, the Department of Energy (DOE) awarded up to USD 10.5 billion through the Grid Resilience and Innovation Partnerships (GRIP) Program to strengthen transmission and distribution networks. Similarly, the European Commission's energy transition strategy prioritizes smart grid deployment to improve system efficiency and cross-border power flows. As government budgets continue targeting resilient and efficient electricity systems, demand for grid optimization technologies is expected to expand across transmission operators, distribution utilities, and public energy agencies.

- Renewable energy integration: The rapid deployment of renewable energy resources is increasing operational complexity across power networks. The International Energy Agency April 2024 data reported that approximately 1,500 GW of renewable energy projects worldwide were awaiting grid connection due to network constraints. Variable solar and wind generation create fluctuations in power supply that require enhanced forecasting, dispatch optimization, and congestion management. Governments worldwide continue to support renewable deployment through incentives, creating long-term demand for advanced operational technologies. Utilities increasingly use optimization solutions to manage intermittent generation while maintaining reliability standards. As renewable penetration rises, optimization capabilities become essential for integrating generation assets efficiently without compromising grid performance.

Challenges

- High R&D and capital intensity: Developing advanced ADMS, DERMS, and AI-based analytics requires sustained, multi-year investment in software engineering and domain expertise. Smaller entrants struggle to match the R&D budgets of established giants like Siemens or GE, delaying time-to-market and limiting feature parity.

- Shortage of skilled workforce with domain expertise: Developing grid optimization algorithms requires expertise in power systems, machine learning, and control theory—a scarce combination. New entrants compete with tech giants and utilities for this talent, driving up recruitment and retention costs.

Grid Optimization Solution Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.8% |

|

Base Year Market Size (2025) |

USD 4.5 billion |

|

Forecast Year Market Size (2035) |

USD 11.4 billion |

|

Regional Scope |

|

Grid Optimization Solution Market Segmentation:

Deployment Type Segment Analysis

Under the deployment type, the cloud based is dominating in the grid optimization solution market and is poised to hold the share value of 42.5% by the end of 2035. The segment is driven by the utilities are abandoning legacy on‑premise infrastructures for scalable, pay‑as‑you‑go platforms that enable real‑time data analytics and seamless software updates. Cloud solutions drastically reduce capital expenditure while offering near‑infinite storage for high‑resolution phasor measurement unit data, which is critical for predictive outage management. They also facilitate integration with third‑party weather and market pricing services, allowing dynamic dispatch decisions. Furthermore, FedRAMP‑certified cloud providers have alleviated cybersecurity concerns, accelerating adoption among investor‑owned utilities.

Component Segment Analysis

The software component dominates the grid optimization solution market, with predictive AI modules emerging as its fastest‑growing subset. Argonne National Laboratory's recent innovations in artificial intelligence are revolutionizing grid asset maintenance, enabling U.S. power companies to detect incipient transformer failures, insulator degradation, and conductor sagging days or weeks before outages occur, as per the ANL May 2024. These AI algorithms ingest high‑frequency sensor data, weather patterns, and historical failure logs to generate prioritized work orders, slashing unplanned downtime and extending equipment life. The U.S. Department of Energy reported Argonne‑led pilot that AI‑based predictive maintenance reduced forced outage events across participating Midwest utilities compared to traditional time‑based inspection schedules.

End user Segment Analysis

Distribution system operators dominate the grid optimization solution market as they face mounting regulatory mandates to integrate renewable energy, reduce outages, and ensure grid transparency—much like broadcasting regulators enforce EPG compliance. The DSI July 2023 data explicitly lays out a roadmap for establishing DSOs as independent, non‑profit entities to manage active distribution networks with high DER penetration. The report emphasizes that DSOs will be responsible for real‑time operation, grid security, and market facilitation, directly driving demand for advanced distribution management systems (ADMS), forecasting tools, and cyber‑secure ICT infrastructure. This regulatory push positions DSOs as the primary end‑user segment, as they will procure optimization solutions to integrate rooftop solar, EVs, and storage while reducing Aggregate Technical & Commercial (AT&C) losses from ~22% toward the 12–15% target by 2025.

Our in-depth analysis of the grid optimization solution market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Type |

|

|

Component |

|

|

Technology |

|

|

Grid Level |

|

|

Application |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Grid Optimization Solution Market - Regional Analysis

North America Market Insights

North America is dominating the grid optimization solution market and is poised to hold the share value of 38.8% by the end of 2035. The region is driven by the urgent need to modernize aging electricity infrastructure and integrate growing shares of distributed renewable resources. Utilities across the region are actively deploying advanced distribution management systems, artificial intelligence-based predictive analytics, and robust cybersecurity frameworks to enhance grid reliability and resilience against extreme weather events. The market is characterized by strong regulatory support, with federal and state-level policies encouraging non-wires alternatives and demand response programs. Major technology providers dominate the landscape, offering comprehensive software suites. Cross-border coordination between the U.S. and Canada system operators further drives the need for interoperable, scalable optimization platforms.

The growing federal support for grid modernization and rising infrastructure investment aimed at improving reliability and operational efficiency is shaping the grid optimization solution market in the U.S. According to the U.S. Energy Information Administration February 2024 data, total U.S. electricity sales reached approximately 4.08 trillion kWh in 2024, reflecting increasing network utilization and the need for advanced grid management capabilities. Additionally, the U.S. Department of Energy October 2024 data announced up to USD 1.5 billion in funding through the Transmission Facilitation Program to accelerate high-capacity transmission projects across the country. These developments are encouraging utilities and transmission operators to adopt optimization solutions for load forecasting, congestion management, asset performance monitoring, and transmission planning, supporting continued market expansion across the U.S. power sector.

The aging electricity infrastructure and strengthen grid reliability amid rising electrification is shaping the grid optimization solution market in Canada. According to the Carbon Breif April 2024 data, Canada generated approximately 636 terawatt-hours (TWh) of electricity in 2023, highlighting the scale of network operations requiring advanced optimization and monitoring capabilities. In addition, the Government of Canada June 2026 announced investments of more than USD 4.5 billion through the Smart Renewables and Electrification Pathways Program (SREPs) as of 2024 to support clean electricity, grid modernization, and electrification projects nationwide. These investments are increasing demand for grid optimization platforms that support transmission planning, distributed energy resource integration, outage management, and asset performance analysis. Utilities are increasingly leveraging digital grid solutions to improve operational efficiency while accommodating future electricity demand growth.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the grid optimization solution market. The region is driven by the rapid urbanization, soaring electricity demand, and ambitious renewable energy targets across both developed and emerging economies. The region faces unique challenges, including extreme weather events, island grid constraints, and the need to electrify vast rural populations, which accelerate the adoption of AI-based forecasting, fault detection, and Volt-VAR optimization. Regulatory frameworks are evolving rapidly, with nations like India proposing independent Distribution System Operators (DSOs) to manage active distribution networks. Multinational vendors compete alongside strong domestic players, fostering innovation in edge computing, battery-integrated optimization, and interoperable communication protocols tailored to local grid conditions.

The transmission infrastructure and strengthens grid digitalization to support rising electricity demand is shaping the grid optimization solution market in India. According to the PIB June 2025 data, India's installed power generation capacity reached approximately 476 GW in June 2025, creating greater requirements for advanced grid management, forecasting, and network optimization tools. These developments are encouraging utilities and transmission operators to adopt grid optimization solutions for congestion management, real-time monitoring, renewable energy integration, and asset utilization, supporting efficient and reliable operation of India's evolving power network.

The power system modernization and renewable energy integration is shaping the grid optimization solution market in China. According to the BRICS 2025 data, China’s total installed power generation capacity reached approximately 3.35 billion kW, increasing the complexity of grid operations and driving demand for advanced optimization platforms. In addition, the National Bureau of Statistics of China reported that the country generated electricity, reflecting continued growth in power consumption and network utilization. These trends are encouraging grid operators and utilities to invest in solutions for transmission optimization, load forecasting, renewable integration, and real-time system management to enhance reliability and operational efficiency across China’s expanding electricity network.

Europe Market Insights

Europe stands as a highly mature and regulation-driven market for grid optimization solutions, propelled by the European Green Deal and ambitious climate neutrality targets. The region is characterized by deep integration of renewable energy sources, particularly offshore wind and solar, which necessitates advanced distribution management systems and real-time grid balancing tools. Distribution System Operators across the UK, Germany, France, and the Nordics are actively deploying AI-driven predictive analytics, Volt-VAR optimization, and flexible DERMS platforms to manage bidirectional power flows from millions of prosumers. Interoperability and standardization, guided by IEC 61850 and CIM frameworks, are critical priorities. The market sees strong collaboration between incumbent vendors like Siemens and Schneider Electric with innovative startups focused on edge computing and blockchain-based peer-to-peer energy trading. Cybersecurity remains a top focus, with ENISA guidelines shaping procurement.

The electricity network to support renewable integration and improve system flexibility is driving the grid optimization solution market in Germany. According to the Federal Network Agency (Bundesnetzagentur), Germany had approximately many kilometer of transmission line projects under the Federal Requirements Plan either completed or approved, reflecting substantial investment in grid expansion. In addition, NLM June 2025 study show that renewable energy sources accounted for 59.4% of Germany’s domestic electricity generation in 2024, the highest share recorded to date. The increasing penetration of variable renewable energy and continued transmission development are driving utilities and grid operators to deploy optimization solutions for congestion management, grid balancing, network planning, and real-time operational control.

The grid operators invest in digital infrastructure to manage growing renewable generation and maintain network reliability is driving the grid optimization solution market in the UK. According to the Department for Energy Security and Net Zero, renewable sources generated approximately 50.8% of the UK’s electricity in 2024, increasing the need for advanced forecasting, balancing, and grid optimization capabilities. Additionally, Ofgem approved an initial investment package of under the RIIO-T3 framework to support electricity transmission network upgrades and future energy system requirements. These developments are encouraging transmission operators and utilities to deploy optimization solutions for asset management, congestion reduction, renewable integration, and real-time grid performance monitoring across the UK electricity sector.

Key Grid Optimization Solution Market Players:

- Siemens AG (Germany)

- Schneider Electric SE (France)

- General Electric (U.S.)

- Elisa Estonia (Tallinn)

- Hitachi Energy (Japan)

- Itron, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Siemens AG stands as a global leader in the grid optimization solution market, offering its comprehensive Spectrum Power™ suite for advanced distribution management (ADMS) and energy management (EMS).

- Schneider Electric SE commands a strong position in the grid optimization solution market through its EcoStruxure™ Grid platform, which unifies IoT sensors, edge control, and cloud analytics for end-to-end visibility.

- General Electric (GE) remains a formidable force in the grid optimization solution market, primarily through its Grid Solutions division, which offers the Advanced Energy Management System (AEMS) and Distribution Management System (DMS).

- Elisa Estonia has carved a niche in the grid optimization solution market though primarily a telecommunications and ICT provider, by leveraging its 5G and low-power wide-area network (LPWAN) infrastructure to enable ultra-reliable data transport for smart grid sensors.

- Hitachi Energy, born from the merger of Hitachi’s power systems and ABB’s grid division, is a powerhouse in the grid optimization solution market, offering the Lumada™ Asset Performance Management and the TXpert™ digital transformer ecosystem.

Here is a list of key players operating in the global grid optimization solution market:

The grid optimization market is highly consolidated, dominated by European and U.S. giants with deep software portfolios and utility relationships. Key players aggressively pursue mergers and partnerships with AI startups to enhance real-time analytics and distributed energy resource management. Siemens and Schneider focus on edge-to-cloud platforms, while Hitachi Energy and Toshiba leverage Japan’s microgrid expertise. US firms emphasize cybersecurity and renewables integration. India and Malaysia players are rising through cost-competitive SCADA and distribution management systems, often collaborating with state utilities. Strategic initiatives now prioritize grid-edge intelligence, predictive maintenance, and interoperability with IoT devices to accommodate EV charging and storage.

Corporate Landscape of the Grid Optimization Solution Market:

Recent Developments

- In May 2026, Elisa Estonia deployed Elisa Industriq’s Gridle battery optimization solution across its mobile network to strengthen network resilience and enable its base station batteries to help balance the Estonian electricity system operated by Elering.

- In January 2026, Hitachi Energy announced the launch of AxoniQ™, its comprehensive portfolio of solutions for multi-terminal direct current (MTDC) systems. As global electricity demand accelerates, MTDC systems are becoming critical to ensuring a secure, affordable, and sustainable power grid.

- In January 2026, Itron, Inc., is collaborating with Snowflake, the AI Data Cloud company, to advance the future of grid planning and utility analytics. This collaboration brings together Itron’s expertise in grid edge intelligence and Snowflake’s fully managed, high-performance data platform to empower utilities to solve some of the industry’s most pressing challenges.

- Report ID: 8651

- Published Date: Jul 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.