Glass Packaging Market Outlook:

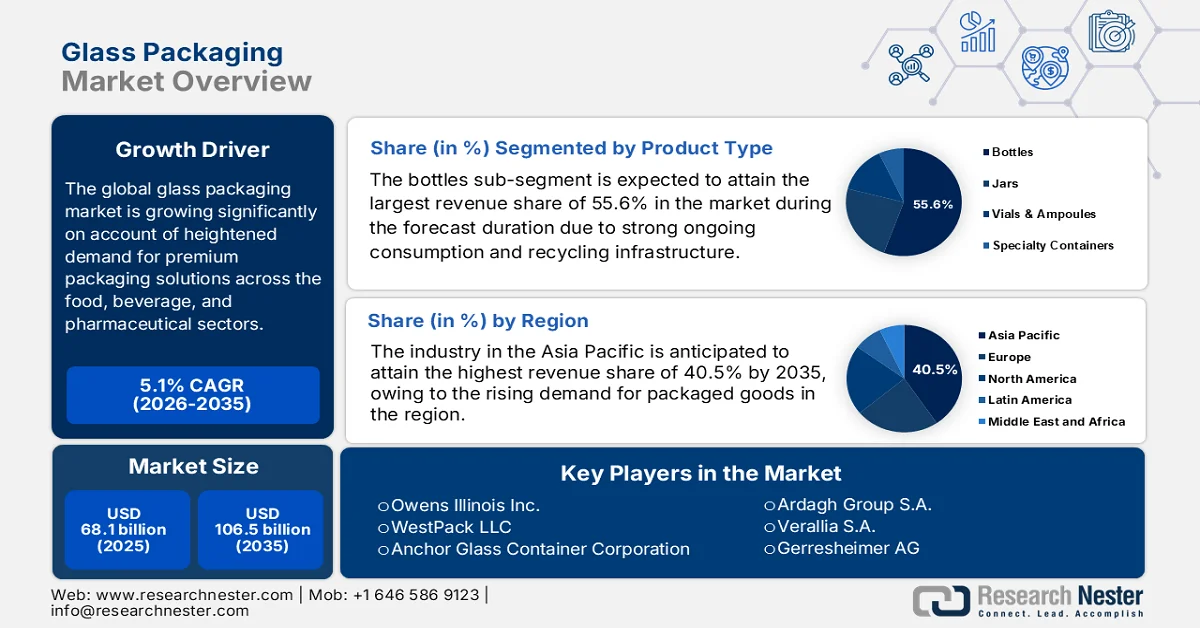

Glass Packaging Market size was valued at USD 68.1 billion in 2025 and is projected to reach USD 106.5 billion by the end of 2035, rising at a CAGR of 5.1% during the forecast period, which is from 2026 to 2035. In 2026, the industry size of glass packaging is estimated at USD 71.5 billion.

The escalating demand for premium packaging solutions across the food, beverage, and pharmaceutical sectors is responsible for uplifting the global glass packaging market. According to the article published by the World Metrics Organization in February 2026, the global glass packaging production reached a significant value of 135 million metric tons in 2022, and it is anticipated to surpass 148 million metric tons by 2027, wherein beverage applications account for 70% of total output. In addition, the report also stated that operational efficiency is improving, with automation in production lines increased by 18% between 2020 and 2023, and robotics handling 35% of material movement tasks. On the demand side, 68% of consumers prefer glass packaging for safety and sustainability, whereas 72% of millennials are willing to pay a 5% premium for recyclable glass packaging.

Furthermore, the expansion of the alcoholic beverage industry is efficiently fueling the heightened demand for bottles and containers, hence stimulating consistent business for pioneers in the glass packaging market. According to the article published by the U.S. International Trade Commission (USITC) in October 2024, glass wine bottles are extensively used for packaging wine due to their ability to preserve taste as well as quality. It also mentions the U.S. key manufacturers, which include Ardagh Glass Inc., Gallo Glass Company, and O-I Glass, whereas major global producers operate in Chile, China, and Mexico. The U.S. glass wine bottles industry is growing at a rapid pace, positively influenced by wineries and distributors as primary buyers. In 2023, total apparent U.S. consumption reached a total value of 13.6 million gross and was valued at USD 1.2 billion, supported by both domestic production and imports.

U.S. Glass Wine Bottle Industry 2023: Consumption, Production, and Import Statistics

|

Category |

Quantity (Million Gross) |

Value (Million USD) |

Market Share (%) |

|

Total Consumption |

13.6 |

1,200 |

100 |

|

U.S. Domestic Shipments |

9.7 |

662.3 |

71.2 (Qty) / 56.6 (Value) |

|

Imports (Subject Countries) |

3.0 |

374.6 |

22.2 (Qty) / 32.0 (Value) |

|

Imports (Non-subject Countries) |

0.9 |

133.2 |

6.6 (Qty) / 11.4 (Value) |

Source: USITC

Key Glass Packaging Market Insights Summary:

Regional Highlights:

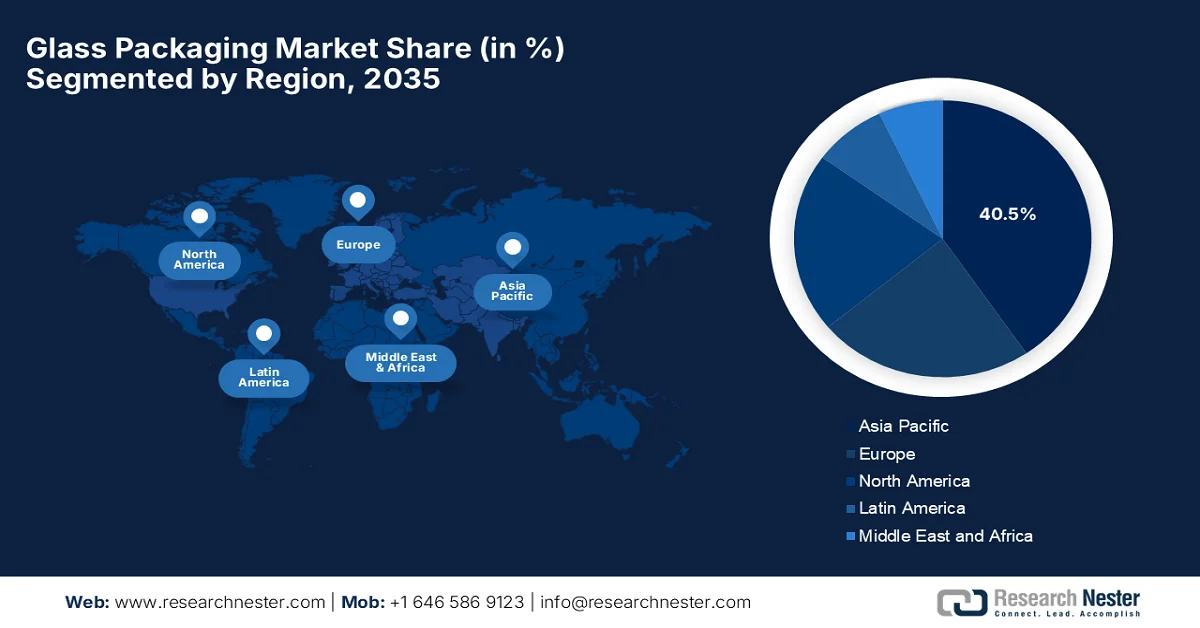

- Asia Pacific glass packaging market is projected to hold a dominant 40.5% share by 2035, bolstered by rising demand for packaged food, beverages, and pharmaceuticals alongside increasing urbanization shifting consumer preference toward sustainable packaging.

- North America is expected to witness the fastest growth through 2026–2035, fueled by high alcoholic beverage consumption and rapid adoption of advanced glass packaging technologies.

Segment Insights:

- In the glass packaging market, the bottles segment is estimated to capture a leading 55.6% share by 2035, propelled by extensive production volumes and strong recycling infrastructure supporting circular economy practices.

- The food and beverage segment is forecast to secure a significant share by 2035, stimulated by surging demand for packaged drinks and processed food products.

Key Growth Trends:

- Rising demand for sustainable packaging

- Increasing consumption of packaged food products

Major Challenges:

- High transportation & handling costs

- Energy-intensive production

Key Players: Owens Illinois Inc. (U.S.), WestPack LLC (U.S.), Anchor Glass Container Corporation (U.S.), Ardagh Group S.A. (Luxembourg), Verallia S.A. (France), Gerresheimer AG (Germany), HEINZ GLAS GmbH & Co. KGaA (Germany), Vetropack Holding AG (Switzerland), Bormioli Rocco S.p.A. (Italy), Vidrala S.A. (Spain), Ba Glass B.V. (Netherlands), Beatson Clark (UK), Nihon Yamamura Glass Co., Ltd. (Japan), Toyo Seikan Group Holdings, Ltd. (Japan), Koa Glass Co., Ltd. (Japan), Amcor Plc (Australia), Corning Inc. (U.S.), BA Glass (Poland), CANPACK Group (Poland), Piramal Glass Pvt. Ltd. (India), Hindustan National Glass & Industries Ltd. (India), PGP Glass Private Limited (India), Borun Glass Works Ltd. (Malaysia).

Global Glass Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 68.1 billion

- 2026 Market Size: USD 71.5 billion

- Projected Market Size: USD 106.5 billion by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 31 March, 2026

Glass Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for sustainable packaging: Consumers across most nations are showcasing an increased preference towards glass due to its recyclability. This aligns with global sustainability goals and helps companies meet regulatory agendas, thus boosting the glass packaging market. As per an article published by Environmental Engineering Research in September 2024, the worldwide glass manufactured is 130 million tons annually, and global recycling rates average 21% of total glass produced. Besides, container glass achieves the highest recovery at about 32%, whereas flat glass lags at only 11%. In the U.S, 12.3 million tons of glass were generated in a year, with bottle deposit programs reaching 63% when compared to only 24% in states without supportive schemes, hence highlighting the urgent need for awareness programs to boost glass recycling adoption.

- Increasing consumption of packaged food products: There has been a growth in consumption of ready‑to‑eat foods, which fuels demand for glass bottles and jars due to glass’s ability to preserve taste along with freshness. According to the article published by the National Institute of Health (NIH) in October 2025, the study analyzed consumer perceptions of ready-to-eat pulses, which were packaged in metal cans, glass jars, and plastic pouches. In this, metal cans performed most consistently in blind taste tests, and glass jars were perceived as the highest quality and most sustainable packaging, thus benefiting the glass packaging market. It also stated that age, diet type, and sustainability attitudes influenced these perceptions, reflecting encouraging opportunities for product innovation and the need for consumer education about packaging sustainability.

- Expansion of the pharmaceutical sector: Glass is inbuilt with chemical inertness and certain barrier properties, making it a preferred choice for vials, ampoules, and injectable drug packaging, supporting growth in the glass packaging market. In July 2024, the U.S. Food & Drug Administration (FDA) provided recommendations for reporting and implementing post approval changes to container closure systems consisting of glass vials and stoppers for approved sterile drug products, including biologics administered parenterally. In addition, the guidance also outlines pathways for obtaining FDA feedback and introduces risk-based tools to support safe and efficient changes to glass vial and stopper components. Therefore, this underscores the continued reliance on glass in pharmaceutical packaging, deliberately supporting growth in the glass packaging market.

Challenges

- High transportation & handling costs: Glass packaging is considered to be heavier and more fragile when compared to plastic or aluminum, which exacerbates the transportation expenses. Shipping requires proper handling and protective packaging in order to prevent any type of breakage, which adds to operational complexity. On the other hand, this fragility also raises insurance premiums, whereas for global distribution, these costs multiply, making glass less competitive in terms of long-distance supply chains. Retailers and manufacturers who are operating in the glass packaging market need to make investments in training staff for safe handling and using durable packaging solutions. Therefore, the existence of these logistical challenges ultimately limits the adoption of glass for high-volume, cost-sensitive consumer goods.

- Energy-intensive production: The glass production process is a highly energy-intensive process, which is influenced by the need for high-temperature furnaces to melt raw materials such as silica sand, soda ash, and limestone. This process consumes high amounts of electricity and fuel, which contributes to high operational costs and a considerable carbon footprint. Besides, energy price fluctuations can negatively affect profitability, particularly for manufacturers who depend on fossil fuels. The existence of modern furnaces and recycling practices, such as using cullet, can reduce energy requirements, but initial investment in these technologies is high. In addition, high energy consumption also attracts scrutiny from regulators and eco-conscious consumers, making sustainable energy management a critical challenge in the glass packaging market.

Glass Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 68.1 billion |

|

Forecast Year Market Size (2035) |

USD 106.5 billion |

|

Regional Scope |

|

Glass Packaging Market Segmentation:

Product Type Segment Analysis

In the product type segment, the bottles sub-segment is expected to attain the largest revenue share of 55.6% in the glass packaging market during the forecast duration. The bottles for beverages and food are widely generated and recycled materials in municipal waste streams, reflecting strong ongoing consumption and recycling infrastructure in major markets. In April 2025, New Zealand-based glass manufacturer, Visy, achieved a landmark 70% recycled glass content in locally made bottles and jars. It is producing more than 700 million containers annually for wineries and food companies. Hence, from a strategic perspective, such instances by the company reflect the prominence of leading manufacturers, which can drive both market dominance in the bottles sub-segment. In addition, such moves support sustainability leadership by leveraging high recycled content and large-scale production to reinforce circular economy practices in major markets.

End use Segment Analysis

Food and beverage subtype is anticipated to garner a considerable revenue share of the glass packaging market by the conclusion of 2035. The growth of the segment is largely driven by the ever-increasing demand for packaged beverages and processed foods. In July 2024, Ardagh Glass Packaging-North America announced the expansion of its craft beverage bottle portfolio with new 12oz bottles in emerald green, flint, and amber glass. The product is designed and manufactured in the U.S., and these bottles are 100% recyclable and endlessly reusable without loss of quality. Therefore, these consistent efforts from leading pioneers indicate that glass packaging market leaders are strategically leveraging product innovation and domestic manufacturing to capture a significant consumer base. At the same time, their focus on sustainability and recyclability is solidifying long-term growth in this segment.

Glass Type Segment Analysis

Under the glass type segment, type 1 borosilicate is predicted to grow with a lucrative revenue share in the glass packaging market during the discussed timeframe. The sub-segment’s growth is mainly propelled by the increasing adoption of specialty glass types that offer enhanced strength, clarity, and chemical resistance. In addition, the regulatory standards and consumer preferences are encouraging the shift toward these advanced glass materials. In August, 2025, SCHOTT became the first in India to locally produce high-precision syringes and glass tubing at its Gujarat facility. This expansion supports the surging demand for GLP-1-based injectables such as semaglutide, which is vital for diabetes and weight management. The move strengthens the country’s pharmaceutical self-reliance under the Make in India initiative, positioning SCHOTT as the largest producer of syringes and borosilicate cartridge tubing, hence denoting a wider segment scope.

Our in-depth analysis of the global glass packaging market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

End use |

|

|

Glass Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Glass Packaging Market - Regional Analysis

APAC Market Insights

The Asia Pacific glass packaging market is predicted to garner the largest revenue share of 40.5% by the conclusion of the forecast duration. The region’s dominance is largely driven by high demand for packaged goods, including food, beverages, and pharmaceuticals. Meanwhile, accelerating urbanization is shifting consumer preferences toward premium and sustainable packaging solutions, attracting more investments in this sector. In April 2024, the report published by the government of Australia stated that glass packaging played a significant role in Australia’s 2021–22 packaging landscape. It accounted for almost 16.4% of the total packaging placed on the glass packaging market, with a strong recovery rate of 18.4% of all post-consumer packaging collected. It also underscores that glass has excellent recycling potential, with 100% of it deemed recyclable, hence highlighting glass as one of the most sustainable packaging materials in the region.

In China, the glass packaging market is a global powerhouse, fueled by a massive manufacturing infrastructure and the beverage and pharmaceutical industries. As domestic consumers are seeking high-end cosmetics and craft spirits, manufacturers are focused on lightweight designs to meet both aesthetic demands. Based on the country’s government data, published in January 2026, its new action plan aims to enhance solid waste management as part of its green transition. The plan is highly focused on increasing the recycling of materials such as plastics, metals, and glass, and improving waste reduction at the source. The article highlights that by 2030, China has set a target to recycle 510 million tons of major renewable resources annually, with a greater emphasis on integrating waste into a circular economy, hence suitable for bolstering the country’s market growth.

The expanding pharmaceutical sector and a rising consumer preference for premium packaging are responsible for uplifting the glass packaging market in India. As the world’s leading supplier of generic medicines and vaccines, the country is heavily dependent on glass vials and ampoules to maintain product integrity for high-value exports. Simultaneously, the alcoholic beverage industry remains a core pillar of demand, in which craft breweries and distilleries choose glass for its capability to preserve flavor. In July 2025, Sakhi Neer eco-friendly glass water bottling facility was inaugurated at the Gujarat Secretariat, which marks a major step in reducing single-use plastic. Besides, it is managed by the MAA Narmada Ekta Mahila Mandal and powered by technology from a Vadodara-based youth startup. The initiative will replace plastic bottles with reusable glass ones, hence positively impacting glass packaging market growth.

India Glass Bottles Trade 2024: Exports, Imports, Top Markets & Key Insights

|

Metric |

Value |

Notes |

|

Exports |

USD 465 million |

173 / 1,220 (India’s product ranking) |

|

Top Export Destination |

U.S. |

USD 152 million |

|

Fastest Growing Export Market |

U.S. |

+USD 32.3 million (2023–2024) |

|

Share of India in Global Exports |

3.24% |

10 / 186 (global ranking) |

|

Imports |

USD 113 million |

427 / 1,211 (India’s product ranking) |

|

Top Import Origin |

China |

USD 66.4 million |

|

Fastest Growing Import Origin |

China |

+USD 9.67 million (2023–2024) |

|

Share of India in Global Imports |

0.79% |

25 / 221 (global ranking) |

|

Main Export Destinations |

U.S., France, Nepal, Spain, UAE |

USD 152 million, 34.3 million, 26.1 million, 24.1 million, 24 million |

|

Main Import Origins |

China, Sri Lanka, Italy, Oman, Germany |

USD 66.4 million, 12.6 million, 6.1 million, 4.8 million, 4.7 million |

Source: Observatory of Economic Complexity

North America Market Insights

The North America glass packaging market is anticipated to grow at the fastest rate during the stipulated timeframe. The region’s prominence in this field is largely driven by the high consumption of alcoholic beverages. In addition, the swift adoption of advanced technologies for innovative glass packaging is also a key factor that is contributing to this growth. In 2024, 60.5% of people ages 12 and older, which is approximately 169.9 million people, reported drinking alcohol in the past year, according to the official statistics published by the National Institute on Alcohol Abuse and Alcoholism in August 2025. In the case of adults 18 and older, 65.2%, that is around 145.3 million, had consumed alcohol in the past year. Among youth ages 12 to 17, 11.4% about 3.0 million, reported drinking in the past year, hence denoting a lucrative growth opportunity for the region’s market to grow at an extensive pace.

The import and manufacturing trends are reshaping the growth dynamics of the U.S. glass packaging market. The surge in beer, wine, and spirits container shipments, coupled with increasing investments in advanced glass production technologies, is efficiently strengthening the market’s capacity. In April 2024, the Glass Packaging Institute reported that, as of February 2024, beer dominates U.S. glass container shipments, accounting for almost 47% of the market, which was followed by food at 24%, non-alcoholic beverages at 10%, and wine at 8%. Spirits represent 6% of shipments, with ready-to-drink beverages at 5%. On the other hand, glass bottle imports into the U.S. have increased by 6.8% year-to-date, which totals 68 million more containers, and China and Mexico are the largest importers. In addition, imported 750ml wine/spirit bottles witnessed a 60% increase in early 2024 when compared to the same period in 2023, hence suitable for bolstering overall glass packaging market growth.

U.S. Countervailing Duty Rates on China Glass Wine Bottle Imports: Company-Wise Breakdown 2024

|

Company |

Final Countervailable Subsidy Rate (% ad valorem) |

|

Shandong Changyu Glass Co., Ltd. |

21.31 |

|

Boliva International Limited |

212.58 |

|

Bright Glassware |

212.58 |

|

Shandong Dingxin Electronic |

212.58 |

|

Wenden Wensheng Glass Co., Ltd. |

212.58 |

|

Wuixi Hua Zhong Glass Co., Ltd. |

212.58 |

|

Xiamen Jane Jonson Co., Ltd. |

212.58 |

|

Yamamura Glass Qinhuangdao |

212.58 |

|

Yantai Prime Packaging Co., Ltd. |

212.58 |

|

Zibo Regal Glass Products Co., Ltd. |

212.58 |

|

All others |

21.31 |

Source: USITC

Canada glass packaging market has gained immense exposure, which is propelled by provincial sustainability mandates and a growing consumer shift from single-use plastics. The country is witnessing the notable expansion of the cosmetic and food sector, where brand owners are willing to pay a premium for glass to align with eco-conscious narratives and high-end positioning. Based on the government data published in February 2023, food packaging materials in Canada are regulated under Division 23 of the Food and Drugs Act, which prohibits harmful substances from migrating into food. It stated that manufacturers may voluntarily submit materials for premarket assessment, and favorable evaluations result in letters of no objection that confirm chemical safety but are not legal approvals. These letters remain valid indefinitely unless the material’s composition or use changes, though Health Canada can rescind them if risks emerge, hence reflecting the prominence of sustainability trends in the country’s market.

Europe Market Insights

Europe glass packaging market is predicted to retain its position as the second-largest stakeholder in the global dynamics. The region benefits from the world's most advanced recycling infrastructure and the luxury cosmetics sector. Stricter environmental mandates are forcing a rapid shift toward the adoption of decarbonized production, leading manufacturers to invest heavily in hydrogen-powered furnaces and electric melting technologies. In June 2023, as per the European Container Glass Federation article, close the glass loop initiative reported that the EU glass packaging collection rate reached 80.1% in 2021, showing steady progress toward its 90% target by 2030. Most collected glass is effectively recycled, wherein 91% reused to make new bottles and jars. Besides, the article underscored that Portugal, with a 54.4% rate, has significant potential and is taking steps through its Vidro+ program to improve glass recycling, hence suitable for boosting the market’s expansion.

The advanced technological infrastructure and rising recycling capacity are propelling the growth of the glass packaging market in Germany. The market is undergoing a massive energy transition, with manufacturers aggressively adopting hybrid electric and hydrogen-compatible melting to meet stringent national carbon-neutrality targets. In August 2024, the country’s government reported that glass recycling in Germany is extremely efficient, as waste glass can be melted and reused indefinitely to produce new bottles and jars. In 2022, about 2.5 million tons of glass packaging were recycled, thereby achieving a recovery rate of almost 84.6%, though still short of the 90% target that was set by the Packaging Act. This particular law requires dual systems to ensure at least 90% of collected glass is reused or recycled on a yearly basis, wherein consumers play a key role by properly disposing of glass in recycling containers.

The UK glass packaging market is mainly driven by its focus on circularity and decarbonisation. The market is undergoing a technological shift, with the presence of major manufacturers such as Encirc and Beatson Clark, which are trialling ultra-low-carbon furnaces powered by hydrogen and biofuels to meet the government's net-zero targets. In January 2025, the country's government announced that it would introduce a deposit return scheme across England, Scotland, and Northern Ireland, with the main goal of reducing waste and increasing recycling of single-use drinks containers. Under the scheme, consumers will pay a small deposit on bottles and cans, which is refunded when they return the items to collection points such as supermarkets. With around 25 billion containers used annually and 6.5 billion wasted, the initiative aims to cut litter, protect wildlife, and reduce pollution, including microplastics, thus denoting a positive outlook for the glass packaging market’s expansion and exposure.

Key Glass Packaging Market Players:

- Owens‑Illinois Inc. (U.S.)

- WestPack LLC (U.S.)

- Anchor Glass Container Corporation (U.S.)

- Ardagh Group S.A. (Luxembourg)

- Verallia S.A. (France)

- Gerresheimer AG (Germany)

- HEINZ‑GLAS GmbH & Co. KGaA (Germany)

- Vetropack Holding AG (Switzerland)

- Bormioli Rocco S.p.A. (Italy)

- Vidrala S.A. (Spain)

- Ba Glass B.V. (Netherlands)

- Beatson Clark (UK)

- Nihon Yamamura Glass Co., Ltd. (Japan)

- Toyo Seikan Group Holdings, Ltd. (Japan)

- Koa Glass Co., Ltd. (Japan)

- Amcor Plc (Australia)

- Corning Inc. (U.S.)

- BA Glass (Poland)

- CANPACK Group (Poland)

- Piramal Glass Pvt. Ltd. (India)

- Hindustan National Glass & Industries Ltd. (India)

- PGP Glass Private Limited (India)

- Borun Glass Works Ltd. (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Owens-Illinois Inc. is one of the largest and most established players in the global glass packaging market. The company is based in the U.S., and it specializes in manufacturing glass containers for the food, beverage, and pharmaceutical industries.

- Ardagh Group S.A. is identified as a leading global producer of glass and metal packaging solutions. The company is highly focused on sustainability, with innovative packaging designs, recyclability, and the use of post-consumer recycled glass.

- Verallia S.A. is one of the world’s largest manufacturers of glass packaging, which is supplying to major food and beverage brands. The company’s core focus is on providing high-quality glass containers that meet the needs of customers in the wine, spirits, food, and soft drink categories.

- Gerresheimer AG is a key player in the production of glass packaging, with a focus on the pharmaceutical and cosmetic sectors. The company efficiently produces a range of glass containers for pharmaceutical products, i.e., vials, ampoules, and injection systems, along with glass packaging for personal care products.

- Nihon Yamamura Glass Co., Ltd., based in Japan, is a prominent player and specializes in manufacturing glass containers for a wide range of industries. The company benefits from its extensive manufacturing base in Japan and a growing international presence.

Below is the list of some prominent players operating in the global glass packaging market:

The global glass packaging market is highly competitive, which hosts a combination of long‑established multinationals and regionally strong manufacturers. Industry leaders such as Owens‑Illinois, Ardagh Group, and Verallia are focused on expansive production networks and sustainability initiatives, such as lightweight glass designs and high recycled content. Strategic partnerships, technological innovation in eco‑design, and expansion into emerging markets are the major strategies adopted by the leading players to drive growth and exposure of the sector. For instance, in November 2023, CANPACK Group and BA Glass announced a definitive agreement for the transfer of CP Glass operations in Poland. This Orzesze plant will be integrated into BA Glass’s existing facilities in Sieraków and Jedlice, thereby strengthening its footprint in the country.

Corporate Landscape of the Glass Packaging Market:

Recent Developments

- In February 2026, Ardagh Glass Packaging announced the launch of two newly designed 8-oz ring-neck bottles. Manufactured in flint glass with lug or continuous thread finishes, these bottles are 100% recyclable and endlessly reusable.

- In February 2026, Gerresheimer showcased its sustainable glass packaging solutions at BIOFACH in Nuremberg. The portfolio includes flint and amber glass designs with high recycled content, lightweight structures, and refillable options to reduce carbon footprints.

- In September 2025, Verallia inaugurated an oxy-combustion furnace at its Campo Bom plant in Brazil, consisting of Air Liquide’s HeatOx technology. This USD 118 million investment enhances production capacity to 820 tons of glass per day, reducing carbon emissions by up to 20%.

- In March, 2025, PGP Glass commissioned a new furnace at its Kosamba, Gujarat plant, boosting production of cosmetic container glass. It is built with support from HORN and its subsidiaries, and the facility has a daily capacity of 120 tons of flint glass for pharmaceuticals, cosmetics, and perfumery.

- In July 2023, Corning announced the launch of Viridian Vials, which are designed to combine performance with sustainability in pharmaceutical packaging. These vials use 20% less glass material when compared to conventional ones, cutting manufacturing and transport emissions.

- Report ID: 4645

- Published Date: Mar 31, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.