Gastrointestinal Bleeding Treatment Market Outlook:

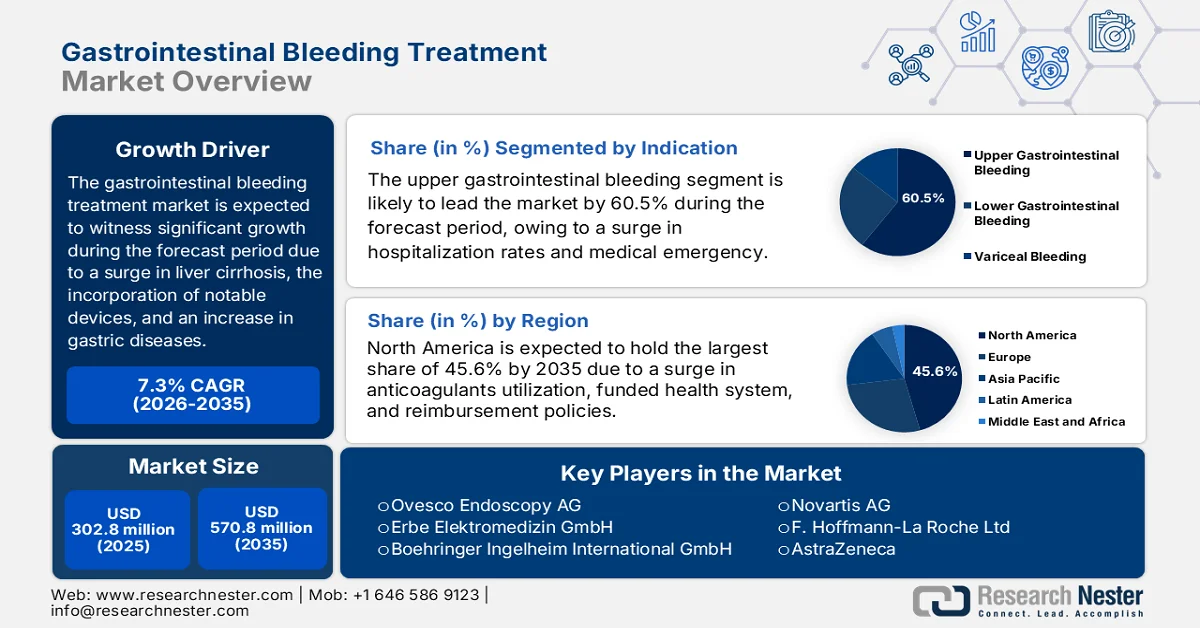

Gastrointestinal Bleeding Treatment Market size was valued at USD 302.8 million in 2025 and is projected to reach USD 570.8 million by the end of 2035, registering a CAGR of 7.3% during the forecast period, i.e., 2026-2035. In 2026, the industry size of gastrointestinal bleeding treatment is assessed at USD 324.9 million.

The worldwide gastrointestinal bleeding treatment market is continuously being shaped by different foundational factors, such as a rise in the burden of liver cirrhosis, the comprehensive utilization of direct oral anticoagulants, a surge in healthcare facilities, and the rapid adoption of novel devices. According to official statistics published by NLM in July 2025, the global liver cirrhosis incidence significantly reached 58.4 million, denoting a rise from 36.9 million. This incidence is highly fueled by non-alcoholic fatty liver disease (NAFLD), which also increased from 24.8 million to 48.3 million. In addition, there has also been an increase in liver cirrhosis-related deaths from 10.2 million to 14 million, accounting for 2% of overall deaths. Besides, the disease incidence is extremely prevalent in the U.S., based on which there is a huge demand for the gastrointestinal bleeding treatment market.

Liver Cirrhosis Incidence Analysis in the U.S., 2024

|

Components |

Prevalence |

|

Adults aged more than 18 years |

4.5 million |

|

Diagnosis Percentage |

1.8% |

|

Number of deaths |

52,274 |

|

Deaths per 100,000 population |

15.4 |

|

Cause of death rank |

9 |

Source: CDC Government

Furthermore, the artificial intelligence (AI)-assisted bleeding detection, tele-endoscopy and remote proctoring for bleeding management, along with a shift toward same-day discharge following endoscopic hemostasis, are a few trends for bolstering the gastrointestinal bleeding treatment market worldwide. As stated in an article published by NLM in May 2025, based on esophageal epithelial tumors, just 0.4% of patients readily undergo endoscopy, which are further characterized by the triad of wart-based exophytic growth, surface vessel crossing, and projections. Besides, gastrointestinal stromal tumor (GIST) is considered one of the most common mesenchymal tumors, with cases ranging from 1% to 3%, thus driving the increased demand for endoscopy treatment. Moreover, based on the August 2023 NLM article, this utilization has led to a payer’s pricing of USD 30 in terms of out-of-pocket difference, and USD 18 billion yearly for prescription and medical drug expenses, particularly for dyspepsia, thus driving the market expansion.

Key Gastrointestinal Bleeding Treatment Market Insights Summary:

Regional Highlights:

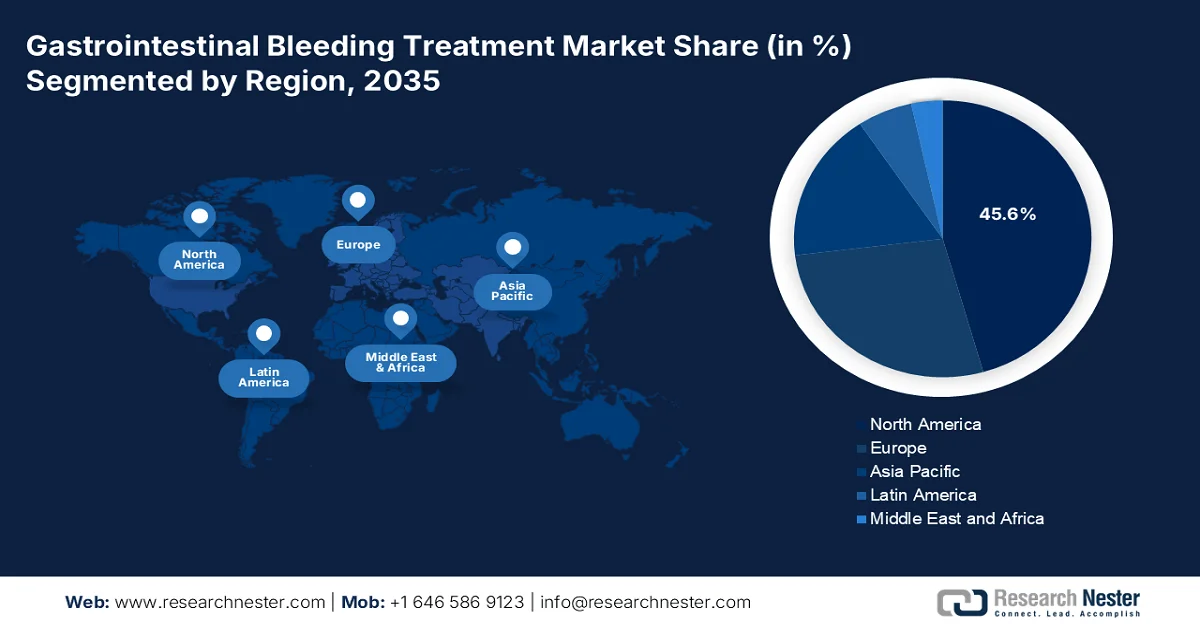

- By 2035, North America is projected to dominate the gastrointestinal bleeding treatment market with a 45.6% share, stimulated by aging population and increased anticoagulant utilization

- Across 2026–2035, Asia Pacific is poised to register the fastest growth energized by rapid healthcare infrastructure expansion and rising disease awareness

Segment Insights:

- By 2035, upper gastrointestinal bleeding (UGIB) is anticipated to capture a 60.5% share in the gastrointestinal bleeding treatment market, propelled by its high incidence and associated hospitalization risks

- Over the forecast period 2026–2035, hospitals are expected to hold the second-largest share, reinforced by their capability to manage complex GI bleeding cases with advanced multidisciplinary care

Key Growth Trends:

- Rising prevalence of diverticular bleeding

- Expansion in direct-to-consumer health awareness campaigns

Major Challenges:

- Reimbursement compression and value-based pricing pressures

- Delayed diagnosis and under-treatment in outpatient settings

Key Players: Boston Scientific Corporation (U.S.), Olympus Corporation (Japan), Cook Medical (U.S.), CONMED Corporation (U.S.), Medtronic (U.S.), Abbott (U.S.), Cardinal Health (U.S.), STERIS PLC (U.S.), U.S. Medical Innovations, LLC (U.S.), Ovesco Endoscopy AG (Germany), Erbe Elektromedizin GmbH (Germany), Boehringer Ingelheim International GmbH (Germany), Octapharma AG (Switzerland), Novartis AG (Switzerland), F. Hoffmann-La Roche Ltd (Switzerland), AstraZeneca (UK), Takeda Pharmaceutical Company Limited (Japan), CSL (Australia), NEXT BIOMEDICAL (South Korea), Sun Pharmaceutical Industries Ltd. (India), Astellas Pharma Inc. (Japan), Eisai Co., Ltd. (Japan), Aurobindo Pharma Limited (India), Hyloris Pharmaceuticals SA (Belgium).

Global Gastrointestinal Bleeding Treatment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 302.8 million

- 2026 Market Size: USD 324.9 million

- Projected Market Size: USD 570.8 million by 2035

- Growth Forecasts: 7.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Indonesia, Mexico

Last updated on : 23 April, 2026

Gastrointestinal Bleeding Treatment Market - Growth Drivers and Challenges

Growth Drivers

- Rising prevalence of diverticular bleeding: Diverticular disorder has emerged as one of the drivers for the gastrointestinal bleeding treatment market. This disorder structurally weakens colonic wall layers in combination with pulsion forces from enhanced intraluminal pressure. According to official statistics published by the NCBI in April 2023, the disease prevalence significantly affects 5% to 45% of individuals in the West. In addition, there has been an increase in the prevalence based on age, accounting for 20% of patients affected at the age of 40 years and 60% affected at 60 years. Besides, an estimated 95% of the global patient population in the West with diverticulosis are impacted with diverticular disease in the sigmoid colon, thereby proliferating the market demand.

- Expansion in direct-to-consumer health awareness campaigns: This is one of the most notable growth drivers of the gastrointestinal bleeding treatment market regarding health awareness by identifying bleeding symptoms. As stated in an article published by the CDC Government in October 2024, the health campaign, Active People, Healthy Nation, is readily focused on moving 15 million adults from being inactive to participating in moderate-based activity regularly. Simultaneously, the campaign also ensures that 10 million adults engage in some physical activities to meet the minimum aerobic physical activity guideline, while 2 million young people tend to meet the minimum guideline. Therefore, the focus on increased physical activities plays a huge role in enhancing the gastrointestinal bleeding treatment market requirement globally.

- Increase in interventional radiology: The upliftment of the gastrointestinal bleeding treatment market is significantly amplified by the extended role of interventional radiology as a suitable backup to poor endoscopic hemostasis. As per an article published by the Radiology Society of North America (RSNA) in August 2024, the U.S. Department of Energy’s National Nuclear Security Administration (NNSA) generously awarded the organization a USD 2 million grant for more than 5 years to support global accessibility to radiology. This is focused on providing and optimizing patient care across low- to middle-resourced countries. Moreover, the NNSA also granted USD 1 million to the organization for over 3 years in developing connections in overall America and addressing radiology treatment services, which is boosting the market exposure.

Challenges

- Reimbursement compression and value-based pricing pressures: Healthcare payers globally are strongly transitioning from fee-for-service to value-based reimbursement models, creating a difficult environment for manufacturers of the gastrointestinal bleeding treatment market. Hemostatic products, particularly single-use endoscopic clips, injection needles, and powder delivery catheters, are increasingly scrutinized by hospital procurement committees, which demand demonstrable reductions in rebleeding rates, length of stay, or intensive care unit transfers. Besides, payers in mature markets are bundling endoscopic procedure payments, meaning that adding a premium-priced hemostatic device directly reduces hospital margins unless the device clearly prevents costly readmissions.

- Delayed diagnosis and under-treatment in outpatient settings: A significant but often overlooked roadblock stems not from device availability but from the patient journey itself. Based on this, gastrointestinal bleeding is frequently intermittent or occult, leading to delayed presentation, misdiagnosis, or treatment in suboptimal outpatient settings. Moreover, patients experiencing melena or hematochezia may initially consult primary care physicians rather than gastroenterologists, resulting in proton pump inhibitor prescriptions without timely endoscopic evaluation. This delay allows lesions to worsen or rebleed, ultimately requiring more complex and costly interventions later. Besides, ambulatory surgical centers and small community clinics often lack on-site hemostatic device inventory or after-hours endoscopy capacity, forcing patient referral to larger hospitals, which in turn is negatively impacting the gastrointestinal bleeding treatment market.

Gastrointestinal Bleeding Treatment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.3% |

|

Base Year Market Size (2025) |

USD 302.8 million |

|

Forecast Year Market Size (2035) |

USD 570.8 million |

|

Regional Scope |

|

Gastrointestinal Bleeding Treatment Market Segmentation:

Indication Segment Analysis

The upper gastrointestinal bleeding (UGIB) sub-segment, part of the indication segment, is anticipated to capture the largest share of 60.5% in the gastrointestinal bleeding treatment market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its crucial role as a severe medical emergency, frequently leading to increased hospitalization rates and an effective mortality risk. According to official statistics published by the NIH in August 2024, this particular bleeding usually occurs in 80 1o 150 out of 100,000 people every year, with an approximate mortality rate between 2% and 10%. Additionally, this bleeding type is usually chronic or acute, along with being overt or obscure and brisk or slow, highly depending on the blood loss chronicity, bleeding rate, and underlying etiology, thus fueling the sub-segment’s expansion across different regions.

End user Segment Analysis

During the forecast period, the hospitals sub-segment, which is part of the end user segment, is projected to account for the second-largest share in the gastrointestinal bleeding treatment market. The sub-segment’s growth is highly driven by the aspect of being uniquely equipped to handle the full spectrum of GI bleeding severity, from hemodynamically unstable variceal hemorrhages requiring intensive care unit monitoring to obscure lower GI bleeding necessitating advanced endoscopic or interventional radiology backup. This centrality stems from the multidisciplinary nature of hospital-based care, where gastroenterologists, interventional radiologists, acute care surgeons, and transfusion medicine specialists coordinate in real time. Unlike ambulatory surgical centers or outpatient clinics, hospitals maintain 24/7 access to emergency endoscopy suites, on-call specialist coverage, blood banks, and surgical theaters, thereby proliferating the sub-segment’s exposure.

Route of Administration Segment Analysis

Based on the route of administration, the intravenous segment is expected to garner the third-largest share in the gastrointestinal bleeding treatment market by the end of the stipulated timeline. The segment’s development is effectively fueled by its importance in clinical care, which is increasingly utilized for restoring fluids, serving as an alternative route for nutrition, and administering medications or blood products when the gastrointestinal tract does not adequately function. As per an article published by NLM in July 2023, this particular administration is extremely common, and an estimated 25 million people receive intravenous fluid therapy globally. Besides, based on a clinical study conducted at the University of Sree Chitra in Trivandrum, it was demonstrated that the flow rate was adjusted in 43.3% of occasions and 50% of situations, thus fueling the segment’s growth.

Our in-depth analysis of the gastrointestinal bleeding treatment market includes the following segments:

|

Segment |

Subsegments |

|

Indication |

|

|

End user |

|

|

Route of Administration |

|

|

Treatment Type |

|

|

Product Type |

|

|

Drug Class |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Gastrointestinal Bleeding Treatment Market - Regional Analysis

North America Market Insights

North America in the gastrointestinal bleeding treatment market is anticipated to garner the highest share of 45.6% by the end of 2035. The market’s upliftment in the region is primarily driven by the aging population, widespread utilization of anticoagulants, innovative endoscopic facilities, suitable reimbursement frameworks, and the presence of a funded health system. According to official statistics published by NLM in November 2022, a clinical study was conducted on 436,864 patients in the U.S. impacted by nonvalvular atrial fibrillation (AF) with increased stroke incidence. In this study, it was observed that there was an increase in anticoagulation rates from 56.3% to 64.7%, owing to the enhanced utilization of direct oral anticoagulants from 4.7% to 47.9%, while indicating a decrease in warfarin use from 52.4% to 17.7%, thereby bolstering the market demand in the overall region.

The gastrointestinal bleeding treatment market in the U.S. is growing significantly, owing to the implementation of AI-based endoscopy, an expansion in outpatient management, federal coverage policies, an extension in Medicare beneficiaries, and a reinforcement of public health priorities. As stated in an article published by NLM in September 2025, over 1.3rd of outpatient facilities, which is 37%, along with an estimated 2/3rd or 66% of outpatient physicians, were readily affiliated with 637 health systems and 593 corporate owners as of 2023. Besides, health systems in the country were enumerated with almost 1 acute care hospital and more than 50 physicians. In addition, these health systems comprise integrated systems, church-based systems, and investor-driven hospital chains, thereby making it suitable for fueling the gastrointestinal bleeding treatment market growth in the overall country.

Outpatient Trends Analysis in the U.S., 2020-2023

|

Ownership Type |

2020 |

2021 |

2022 |

2023 |

Change (2020-2023) |

|

|

Total Number |

% |

|||||

|

Overall |

272,554 |

280,325 |

283,138 |

279,446 |

- |

- |

|

Independent/Other |

|

|

|

|

|

|

|

Total Number |

182,295 |

184,345 |

182,458 |

176,263 |

6,032 |

3.8 |

|

Share % |

66.9 |

65.8 |

64.4 |

63.1 |

- |

- |

|

Health Systems |

|

|

|

|

|

|

|

Total Number |

65,262 |

67,460 |

69,612 |

70,432 |

5,170 |

1.3% |

|

Share % |

23.9 |

24.1 |

24.6 |

25.2 |

- |

- |

|

Corporate Owners |

|

|

|

|

|

|

|

Total Number |

24,997 |

28,520 |

31,068 |

32,751 |

7,754 |

2.5% |

|

Share % |

9.2 |

10.2 |

11.0 |

11.7 |

- |

- |

Source: NLM

The provincial variability, centralized procurement, a robust emphasis on equitable accessibility, an increase in hospitalization rates, the adoption of hub-and-spoke tele-endoscopy networks, suitable resource allocation, real-time monitoring, and federal government funding are certain factors that are driving the gastrointestinal bleeding treatment market in Canada. Based on government estimates published by the ITA in November 2023, the medical device industry in the country was valued at USD 6.8 billion as of 2022, which is further projected to grow by 5.4% every year by the end of 2028. Besides, the overall healthcare expenditure in the country also totaled a roughly USD 242.3 billion or USD 6,270.7 per population. Moreover, the increased focus on healthcare and medical expenditure per person in terms of provinces is also uplifting the market in the country.

Health and Medical Per Person Spending Analysis in Canada, 2022

|

Territory/Province |

Spending Per Person (Public and Private) |

Change From 2021 |

|

Alberta |

USD 8,545 |

3.5% |

|

British Columbia |

USD 8,790 |

2.4% |

|

Manitoba |

USD 8,417 |

1.0% |

|

New Brunswick |

USD 8,010 |

0.9% |

|

Newfoundland and Labrador |

USD 9,894 |

1.5% |

|

Northwest Territories |

USD 21,946 |

2.3% |

|

Nunavut |

USD 21,978 |

8.3% |

|

Nova Scotia |

USD 9,563 |

5.0% |

|

Ontario |

USD 8,213 |

0.3% |

|

Prince Edward Island |

USD 8,531 |

2.3% |

|

Quebec |

USD 8,701 |

1.8% |

|

Saskatchewan |

USD 8,954 |

No change |

|

Yukon |

USD 15,884 |

1.2% |

|

Canada |

USD 8,563 |

0.3% |

Source: ITA

APAC Market Insights

The Asia Pacific in the gastrointestinal bleeding treatment market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by rapid healthcare infrastructure expansion, a rise in medical tourism, an increase in the awareness of gastrointestinal diseases across densely populated countries, government-based health insurance, and technological detection systems. According to official statistics published by NLM in February 2023, a meager proportion, which is an estimated 4% to 7% of the overall GDP, has been generously invested in the health industry across the majority of domestic countries. Besides, based on the November 2024 OECD article, there has been the provision of healthcare spending and resources across 27 regional nations, thereby positively impacting the gastrointestinal bleeding treatment market development.

The gastrointestinal bleeding treatment market in China is gaining increased traction, owing to rapid health and medical modernization, an escalation in device acceptance duration, an increase in patient diagnosis, a surge in the elderly population, and the presence of increased hospital infrastructures. As stated in an article published by the State Council Information Office in November 2023, over 7,100 healthcare centers readily meet the domestically suggested standards, and more than 3,800 community-based hospitals have been developed across the country. Based on this, over 5,000 medical students were increasingly recruited to operate across rural locations. Moreover, the country has focused on basic public health services, which has boosted per capita governmental subsidy to USD 12.1 as of 2023, thereby fueling the market development.

The aspects of generous health and medical coverage services, suitable funding allocation for state and central health schemes, the increased prevalence of alcohol-based liver disease and viral hepatitis, and the introduction of a national training program for conducting rural endoscopists are a few trends that are responsible for driving the gastrointestinal bleeding treatment market in India. As per an article published by the Global Journal of Medical Students Organization in 2024, 90% of liver-based diseases in the country are related to poor lifestyles, and 50% of total patients are diagnosed with this disorder, which is followed by an emergency hospital admission. Besides, in terms of viral hepatitis, Hepatitis A was demonstrated to range between 2.1% to 52.5%, while Hepatitis B accounted from 0.8% to 21.4% of the overall population. Meanwhile, Hepatitis C was indicated to range from o.5% to 53.7%, thus enhancing the market development in the nation.

Europe Market Insights

Europe in the gastrointestinal bleeding treatment market is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by the aging demographic, established universal healthcare systems, accessibility to emergency endoscopy, robust regulatory harmonization, medical spending, and cross-border real-world evidence generation. According to official statistics published by Eurostat in October 2024, the healthcare expenditure in the region was worth USD 2 billion as of 2023, which was equivalent to 10% of the gross domestic product (GDP). Besides, Germany accounts for 11.7%, which is followed by 11.5% for France, as well as 11.2% for both Sweden and Austria, all catered to the highest healthcare spending, which is positively impacting the gastrointestinal bleeding treatment market growth.

The gastrointestinal bleeding treatment market in Germany is gaining increased exposure, owing to the presence of a statutory health insurance system, the decentralized hospital landscape, the implementation of advanced clauses for permitting additional reimbursement facilities, multiple medical device manufacturers, and export-based medical technologies. As stated in an article published by ITA in August 2025, the medical device industry in the country is one of the largest globally, significantly accounting for approximately USD 44 billion in yearly revenue, which made up 26.5% of the regional economy. Besides, with USD 172 billion generated through international sales, the healthcare sector readily contributed 8.1% of the country’s overall exports as of 2023. Additionally, in the same year, healthcare-based imports were valued at USD 188.5 billion, which is responsible for fueling the market exposure in the country.

German Medical Device Industry Analysis, 2022-2025

|

Components |

2022 |

2023 |

2024 |

2025 |

|

Total Exports |

USD 27.1 billion |

USD 30.0 billion |

USD 31.0 billion |

USD 36.4 billion |

|

Total Imports |

USD 24.0 billion |

USD 25.3 billion |

USD 26.0 billion |

USD 27.5 billion |

|

Imports from the U.S. |

USD 5.2 billion |

USD 5.6 billion |

USD 6.0 billion |

USD 6.4 billion |

|

Exchange Rates |

1.05 |

1.08 |

1.08 |

1.07 |

Source: ITA

The existence of a centralized data facility, proactive pharmacovigilance systems, an increase in healthcare resource utilization, suitable reimbursement decisions, generous investments in the medical industry, and reference networks for chronic digestive disease facilities are responsible for bolstering the gastrointestinal bleeding treatment market in France. As per an article published by NLM in October 2022, acute gastroenteritis is regarded as a common illness in the country, with an approximate 21 million incidences occurring yearly. Besides, in terms of health data sources, the syndromic surveillance system (SurSaUD) collects regular data, such as demographic and administrative information for more than 700 emergency departments, which accounts for 92.3% of national emergency department attendances, thereby denoting an optimistic outlook for the gastrointestinal bleeding treatment market growth.

Key Gastrointestinal Bleeding Treatment Market Players:

- Boston Scientific Corporation (U.S.)

- Olympus Corporation (Japan)

- Cook Medical (U.S.)

- CONMED Corporation (U.S.)

- Medtronic (U.S.)

- Abbott (U.S.)

- Cardinal Health (U.S.)

- STERIS PLC (U.S.)

- U.S. Medical Innovations, LLC (U.S.)

- Ovesco Endoscopy AG (Germany)

- Erbe Elektromedizin GmbH (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Octapharma AG (Switzerland)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd (Switzerland)

- AstraZeneca (UK)

- Takeda Pharmaceutical Company Limited (Japan)

- CSL (Australia)

- NEXT BIOMEDICAL (South Korea)

- Sun Pharmaceutical Industries Ltd. (India)

- Astellas Pharma Inc. (Japan)

- Eisai Co., Ltd. (Japan)

- Aurobindo Pharma Limited (India)

- Hyloris Pharmaceuticals SA (Belgium)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Boston Scientific Corporation has established a strong presence in gastrointestinal bleeding treatment through its comprehensive portfolio of endoscopic hemostatic devices, including resolution clips and hemostatic sprays. The company continuously innovates it’s through-the-scope and over-the-scope clip systems to address the full spectrum of bleeding lesions encountered during routine endoscopy.

- Olympus Corporation leverages its leadership in endoscopic imaging systems to offer integrated solutions for diagnosing and treating gastrointestinal bleeding in a single procedural session. The company's hemostatic devices, including a range of metal clips and injection needles, are designed to work seamlessly with its proprietary endoscopy platforms for enhanced procedural efficiency.

- Cook Medical has maintained a specialized focus on gastrointestinal bleeding intervention with its well-regarded hemostasis accessories, including injection needles and multi-band ligators for variceal bleeding. The company emphasizes durable, reliable products that cater to both standard and complex bleeding scenarios encountered across hospital endoscopy units.

- CONMED Corporation addresses the gastrointestinal bleeding market primarily through its endoscopic surgical instruments, including hemostatic forceps and clip delivery systems. The company focuses on ergonomic design and precision engineering to reduce operator fatigue during prolonged endoscopic hemostasis procedures.

- Medtronic has strengthened its gastrointestinal bleeding portfolio through strategic distribution partnerships, notably bringing advanced hemostatic powder technologies to broad commercial networks. The company integrates these hemostatic solutions into its broader gastrointestinal franchise, positioning them alongside its established endoscopy and surgical offerings for comprehensive bleed management.

Here is a list of key players operating in the global gastrointestinal bleeding treatment market:

The gastrointestinal bleeding treatment market is highly consolidated, with U.S.-based medical device giants and European pharmaceutical leaders holding dominant positions. Key players are aggressively pursuing new product development and geographic expansion to strengthen their foothold. For instance, South Korea's NEXT BIOMEDICAL has secured FDA approval for its Nexpowder device in lower GI bleeding, distributing across 29 Europe-based countries and 45 U.S. states through Medtronic. Besides, in January 2025, Astellas Pharma Inc. indicated that China's National Medical Products Administration (NMPA) has approved VYLOY™ by combining it with fluoropyrimidine- and platinum-containing chemotherapy. This is suitable for aiding patients with gastric bleeding, thereby enhancing the gastrointestinal bleeding treatment industry globally.

Corporate Landscape of the Market:

Recent Developments

- In June 2025, Eisai Co., Ltd. introduced Pariet® S, which is a pharmaceutical-based guidance and is increasingly effective in alleviating critical heartburn and stomach pain caused by gastric acid reflux, which is readily available at drugstores and pharmacies throughout Japan.

- In March 2025, Aurobindo Pharma Limited successfully gained the finalized acceptance from the U.S. FDA for its very own abbreviated new drug application for Pantoprazole Sodium, which is suitable for delayed-release oral suspension, significantly associated with gastroesophageal reflux disease (GERD).

- In February 2025, Hyloris Pharmaceuticals SA entered into an outstanding licensing agreement and created a ready-to-use formulation for intravenous administration of pantoprazole, which is a molecule utilized to aid gastric acrid-based conditions.

- Report ID: 8528

- Published Date: Apr 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.