Fishing Equipment Market Outlook:

Fishing Equipment Market size was valued at USD 21.7 billion in 2025 and is projected to reach USD 31.8 billion by the end of 2035, rising at a CAGR of 3.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of fishing equipment is evaluated at USD 22.5 billion.

The global fishing equipment market trends are supported by the sustained participation in recreational fishing, stable license issuance, and public investment in fisheries management and habitat conservation. According to the Take Me Fishing July 2022 report, nearly 52.4 million U.S. people aged 6 and above have participated in fishing in 2022, representing one of the largest outdoor recreation cohorts in the country. Moreover, the U.S. Fish and Wildlife Service 2022 report depicts that the anglers have spent more than USD 99.4 billion on fishing, underscoring the scale of direct product demand. Additionally, the technology adoption in the fishing equipment continues to shape equipment requirements, with the recreational anglers utilizing some form of angling technology, increasing demand for integrated electronic components within traditional fishing gear categories.

Besides, the FAO 2024 data shows that the fisheries and aquaculture production reached 223.2 million tonnes, worth a record USD 472 billion, and providing an estimated 20.7 kg of aquatic animal foods per capita. This production scale reinforces the importance of reliable harvesting and handling equipment across both the capture fishers and aquaculture operations. It also reflects continued institutional focus on food security, export competitiveness, and suitable resource management in coastal and inland economies. As regulatory oversight and traceability requirements strengthen, demand for compliant, durable, and efficiency-oriented fishing equipment is expected to remain structurally supported across commercial supply chains. The data support the steady long-term growth in the fishing equipment market, mainly across commercial and institutional procurement segments.

Key Fishing Equipment Market Insights Summary:

Regional Highlights:

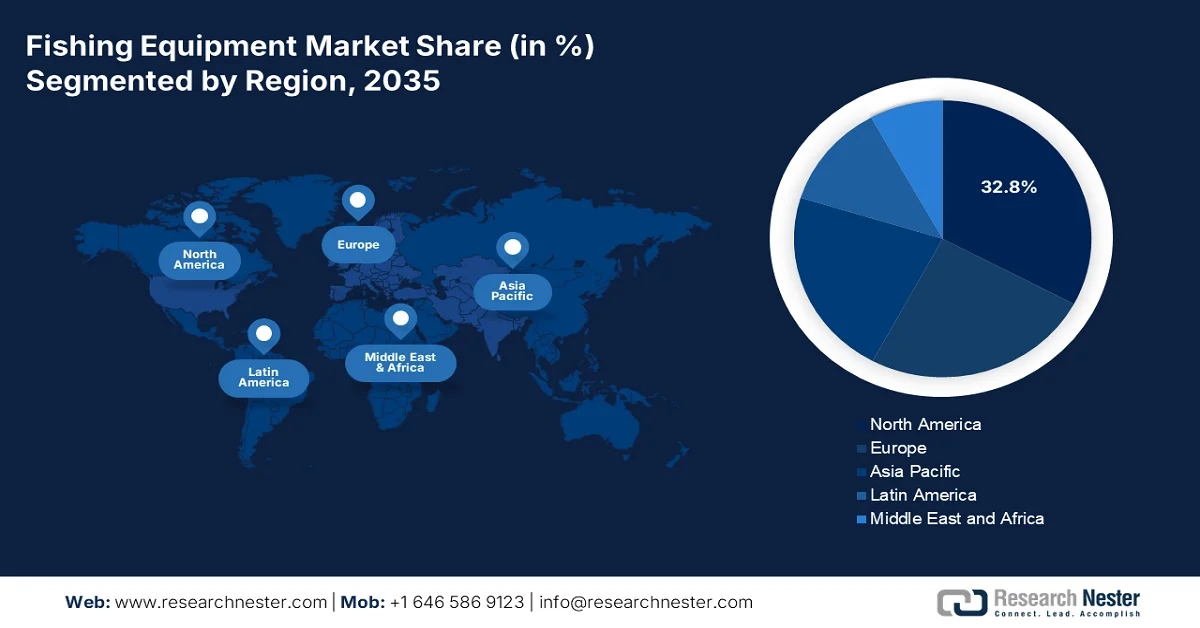

- North America fishing equipment market is projected to command a 32.8% revenue share by 2035, propelled by high recreational participation rates, government-backed fish stocking programs, and increasing adoption of premium and technology-integrated gear.

- Asia Pacific is anticipated to expand at a CAGR of 6.8% during 2026–2035, fueled by expanding recreational fishing engagement, strong manufacturing capabilities in China, Japan, and South Korea, and rising investments in aquaculture modernization.

Segment Insights:

- In the fishing equipment market, the recreational anglers sub-segment is expected to secure a 70.3% share by 2035, driven by the universal appeal of leisure and sport fishing.

- The graphite/carbon fiber sub-segment within the material category is poised to maintain its leading position through 2035, impelled by growing demand for lightweight, high-sensitivity rods that enhance angling precision and endurance.

Key Growth Trends:

- Public investment in fisheries management and stock sustainability

- Aquaculture expansion programs and infrastructure support

Major Challenges:

- Tariff uncertainty and supply chain disruption

- Price sensitivity and premium product adoption barriers

Key Players: Newell Brands (U.S.), Globeride (Daiwa) (Japan), Shimano Inc. (Japan), Pure Fishing (U.S.), Rapala VMC Corporation (Finland/Europe), Zebco Brands (U.S.), Dongmi Fishing (South Korea), Gamakatsu (Japan), St. Croix Rods (U.S.), Okuma Fishing Tackle (Taiwan), Abu Garcia (Sweden), Leeda (UK), Jarvis Walker Pty Ltd (Australia), Silstar (South Korea), Mikado Fishing Tackle (India), Daiwa (India), Cox Enterprises (U.S.), Archer Limited (Norway), Daiwa (Malaysia), Fox International Group (UK).

Global Fishing Equipment Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 21.7 billion

- 2026 Market Size: USD 22.5 billion

- Projected Market Size: USD 31.8 billion by 2035

- Growth Forecasts: 3.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Indonesia, Vietnam

Last updated on : 3 March, 2026

Fishing Equipment Market - Growth Drivers and Challenges

Growth Drivers

- Public investment in fisheries management and stock sustainability: Government budget allocations for the fisheries science stock assessments and enforcement directly sustain commercial and recreational fishing activity, thereby supporting the demand for the fishing equipment market. In the U.S., the report from the NOAA Fisheries in November 2023 reported that USD 1.09 billion was allocated in 2023 funding for stock monitoring, habitat conservation, and regulatory enforcement programs that underpin harvesting activity. These programs maintain allowable catch levels and long-term fleet participation, directly influencing the procurement of nets, lines, trawling systems, and onboard handling gear. Similarly, Europe also allocates funds to support sustainable fisheries and fleet modernization across EU member states. Such public capital flows reduce the operational uncertainty and enable vessel upgrades, driving structured replacement cycles in commercial fishing equipment markets.

- Aquaculture expansion programs and infrastructure support: National aquaculture development strategies are expanding the demand for cages, feeding systems, monitoring tools, and water management equipment. Aquaculture is a primary contributor to global aquatic animal production growth, reflecting a sustained public sector support. Further, the commercial aquaculture expansion is promoted under the national aquaculture development plan, reinforcing the domestic production capacity. Moreover, the PIB August 2025 data has reported that nearly USD 2.20 billion is allocated under Pradhan Mantri Matsya Sampada Yojana to enhance fisheries infrastructure, hatcheries, of farm level fishing and handling equipment, while encouraging private capital participation, strengthening upstream manufacturing demand in the fishing equipment market.

- Regulatory compliance and monitoring requirements: Stricter catch documentation, vessel monitoring, and traceability mandates are shaping the fishing equipment market specification. The electronic monitoring and reporting in several federally managed fisheries, influencing the onboard technology upgrades, are required by the NAOO. Moreover, the European Commission’s fisheries control regulation similarly strengthens the traceability and digital reporting obligation. Compliance-driven investments encourage integration of monitoring compatible gear and digital tracking systems within the fishing operations. These regulatory frameworks elevate procurement standards, encouraging the replacement of legacy systems with compliant alternatives and supporting market growth in higher-value equipment.

Challenges

- Tariff uncertainty and supply chain disruption: Global trade tensions and tariff implementations have created significant uncertainty for fishing equipment market manufacturers. The industry observers noted that the tariffs had become the primary concern for exhibitors, with companies struggling to answer the questions regarding the costs. Very few fishing products are made exclusively from domestic material sources, leaving manufacturers exposed to international trade policy shifts.

- Price sensitivity and premium product adoption barriers: Despite the growing interest in the advanced fishing technologies, significant price sensitivity constrains market expansion. Many consumers report price sensitivity as a primary constraint in the fishing equipment market, and the fishing communities rely on traditional equipment due to the cost limitations. These pricing pressures are intensified by competition from ultra-low-cost online platforms that avoid regulatory compliance costs.

Fishing Equipment Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

3.9% |

|

Base Year Market Size (2025) |

USD 21.7 billion |

|

Forecast Year Market Size (2035) |

USD 31.8 billion |

|

Regional Scope |

|

Fishing Equipment Market Segmentation:

End user Segment Analysis

Within the end user segment, the recreational anglers sub-segment is leading and is expected to hold the share value of 70.3% by the end of 2035 in the fishing equipment market. The segment is driven by the universal appeal of leisure and sport fishing. Apart from the commercial operations, which are focused on yielding recreational participants, continuously invest in upgrading roads, reels, electronics, and specialized apparel to enhance their personal experience and success rates. This demographic is highly responsive to lifestyle marketing and product innovation, from portable fish finders to ergonomic reel designs. According to the USGS October 2024 data, angling technologies are used by 80%. This data represents the segment's deep reliance on innovation to improve the catch rates and satisfaction on the water.

Material Segment Analysis

Under the material segment, the graphite/carbon Fiber has emerged as the leading material sub-segment in rod manufacturing due to its unparalleled strength to weight ration and sensitivity. Anglers increasingly demand rods that can transmit the slightest underwater vibrations while remaining lightweight enough to prevent fatigue during the long casting sessions. The material’s versatility allows the manufacturers to engineer specific actions from the fast tipping for jigging to parabolic bends for fighting large game fish, catering to highly specialized techniques. According to the Take Me Fishing June 2024 data, many traditional fishing rods were composed of fiberglass and are now replaced by graphite or carbon fiber. The choices of fishing rods can be staggering.

Fishing Environment Segment Analysis

Freshwater fishing remains the dominant environment globally due to its geographic accessibility and lower barriers to entry compared to saltwater angling. Millions of lakes, rivers, and reservoirs provide convenient fishing opportunities near population centers, requiring less specialized, expensive equipment than deep-sea excursions. This environment encompasses hugely popular disciplines such as bass fishing and trout angling, which have robust cultures of tournaments and club participation that drive repeat equipment purchases. Conservation efforts and state-managed stocking programs ensure the sustainable fish populations, maintaining the viability of the sport. According to the Department of Environmental Conservation, February 2026 data, in New York, there are many world-class fishing opportunities for a wide variety of sportfish within 7,500 lakes and ponds, 70,000 miles of rivers and streams, and hundreds of miles of coastline.

Our in-depth analysis of the fishing equipment market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Fishing Environment |

|

|

Distribution Channel |

|

|

End user |

|

|

Price Point |

|

|

Mechanism |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Fishing Equipment Market - Regional Analysis

North America Market Insights

The fishing equipment market in North America is dominating and is expected to hold the regional revenue share of 32.8% by 2035. The market is primarily driven by the high recreational participation rates. The government spending via infrastructure programs and fish stocking initiatives supports sustained demand. The key trends include technology adoption, a shift towards the premium specialized gear, and the growth of online retail channels. The state and provincial fish stocking programs ensure accessible fishing opportunities. Moreover, the export growth of advanced composite rods indicates strong manufacturing capability. Further, the stable consumer base is the key that the equipment manufacturers can reliably target for long-term planning and investment.

The stable participation rates and increasing technology integration are fueling the fishing equipment market in U.S. According to the U.S. Fish and Wildlife Service in April 2025 data, nearly 39.9 million U.S people aged 16 and older participated in recreational fishing, spending USD 394 billion on fishing and other outdoor activities. Besides, the U.S. Geological Survey's October 2024 data reveals that most of the recreational anglers utilize angling technologies, driving demand for fish finders, GPS units, and smartphone-connected devices. The U.S. Fish and Wildlife Service data in January 2024 shows that the National Fish Hatchery System stocks 100 million fish annually across 70 hatcheries, maintaining fish populations across 45 million freshwater acres. These data show an uplift in the fishing equipment market in the U.S.

U.S. Fish and Aquatic Conservation Program Infrastructure and Operational Network

|

Program / Facility |

Number |

Primary Function |

|

National Fish Hatcheries |

71 |

Raise and stock over 100 million fish annually to support recreational fishing, tribal subsistence fisheries, and recovery of imperiled species. |

|

Fish Technology Centers |

7 |

Address technical challenges in hatchery operations and aquatic resource management. |

|

Fish Health Centers |

6 |

Prevent the spread of aquatic diseases and protect the health of wild and hatchery fish populations. |

|

Historic National Fish Hatchery & National Fish and Aquatic Conservation Archives |

1 |

Preserve historical records, conservation data, and legacy assets related to national fish and aquatic programs. |

|

Aquatic Animal Drug Approval Partnership (AADAP) |

1 (National Program) |

Secures U.S. FDA approval for medications required in fish culture operations and supports protection of fishery resources. |

Source: U.S. Fish and Wildlife Service January 2024

Canada’s market growth is structurally supported by the high participation levels and strong provincial and federal fisheries management programs. According to the Ontario December 2025 data, approximately 1.3 million people are licensed to hunt and fish, with anglers spending about USD 1.74 billion annually on recreational fishing. Moreover, 1.15 million anglers is spent in 15.6 million fishing days, generating sustained consumables and equipment-related expenditures. Besides the provincial hatchery programs, further reinforcement of participation is provided, with roughly 8 million fish stocked annually across 1,200 lakes, directly supporting catch rates and equipment replacement cycles. On the other hand, the Government of Canada's January 2023 report indicates that Canada’s 243,000-kilometre coastline and 5.5 million square kilometres of ocean territory underpin commercial and recreational fishing infrastructure demand. These data create stable procurement conditions for the fishing equipment market in Canada, particularly across rods, tackle, bait systems, and monitoring electronics.

APAC Market Insights

The Asia Pacific is a significant player and is the fastest growing, poised to register a CAGR of 6.8% between 2026 and 2035. The growth is defined by the expanding population, increasing recreational fishing participation, and strong manufacturing capabilities in China, Japan, and South Korea. China dominates as both a manufacturing hub and a growing consumer market, supported by the government initiatives promoting leisure activities. On the other hand, India is rapidly expanding with a young population and increasing disposable incomes drive the entry-level equipment demand. Moreover, the government investments in aquaculture infrastructure across the region drive demand for specialized feeding, monitoring, and harvesting equipment. Key trends in the fishing equipment market in the Asia Pacific include technology adoption in premium segments, growth of domestic manufacturing capabilities, and expansion of e-commerce distribution channels reaching previously underserved populations.

Strong aquaculture growth and policy-driven modernization are the key trends shaping the fishing equipment market in China. According to the USDA March 2025 data, China is the world’s largest seafood producer with total production reaching 74.1 million metric tons in 2024, which is a rise of 4.1% from 71.2 MMT in 2023. Aquaculture is the primary growth engine, rising to 60.8 MMT in 2024, reflecting a continued expansion of farming efficiency and the recovery of production areas after regulatory tightening. Government initiatives are accelerating deep-sea aquaculture development, further supporting industry chain modernization, technological innovation, and marine spatial optimization. This adoption is reinforcing a steady demand for advanced aquaculture equipment and marine technologies.

China Aquaculture Area (Unit: hectares)

|

Year |

Ocean |

Freshwater |

Total |

|

2020 |

1,995,550 |

5,040,556 |

7,036,106 |

|

2021 |

2,025,510 |

4,983,870 |

7,009,380 |

|

2022 |

2,074,420 |

5,033,084 |

7,107,504 |

|

2023 |

2,214,870 |

5,409,730 |

7,624,600 |

|

2023-2022 change |

+6.77% |

+7.48% |

+7.28% |

|

2022-2021 change |

+2.4% |

+0.99% |

+1.4% |

|

2021-2020 change |

+1.5% |

-1.12% |

-0.38% |

|

2020-2019 change |

+0.17% - |

1.48% |

-1.02% |

Source: USDA March 2025

Active resource availability, inland aquaculture expansion, and government-backed development programs are driving the fishing equipment market in India. As per the PIB February 2026 data, the coastline of over 11,099 km and extensive inland water resources, the sector supports nearly three crore livelihoods and plays a vital role in the rural economic stability. Moreover, the report from the Government of India 2023 data shows that the fish production reached 197 lakh tonnes in 2024 to 2025, reflecting a decade of expansion. Besides, the inland fisheries now contribute over 75% of the total production, highlighting the ongoing shift from capture-based fishing to culture-based aquaculture, which has improved output stability and productivity. India produced 17.5 million metric tonnes, accounting for roughly 9% of global fish production, reinforcing its position as one of the world’s leading producers. This shows a positive impact on the market growth.

Europe Market Insights

The fising equipment market in Europe is expanding significantly and is defined by the mature recreational fishing participation across Western Europe and increasing adoption of specialized gear technologies. Moreover the government initiatives promoting sustainable fishing practices directly influence equipment demand patterns. Besides the key importing countries supplying to China, Japan, Belgium Netherlands, and Malaysia, indicating diversified global supply chains. Germany's fishing apparel equipment market benefits from growing recreational fishing activities and increasing awareness about the specialized gear benefits. Further, the government policies across the region focus on balancing the economic opportunities with environmental conservation via sustainable fishing equipment regulations.

Strong angler participation, manufacturing expertise and government support for the fisheries management are fueling demand for the fishing equipment market in Germany. According to the BMLEH July 2025 data, the Germany fishing fleet lands 200,000 tonnes of fish annually, accounting for USD 237.9 million, operating via roughly 1,300 vessels, of which about 1,000 are small-scale coastal boats under 12 meters creating steady replacement demand for small-vessel gear and onboard handling equipment. Besides the inland and recreational segments, mandatory licensing reinforces the regulated purchasing behavior. Moreover, the permit-based fishing, equipment restrictions, and active association-led restocking programs collectively sustain recurring demand across rods, lines, terminal tackle, and compliant gear systems in Germany’s structured fishing market.

The structural consolidation within the fleet and regulatory driven sustainability controls are shaping the fishing equipment market in UK. As per the UK Sea Fisheries Statistics 2022 data, England accounts for 48% of total UK vessels and Scotland 37%, the Scottish fleet represents 61% of total fleet capacity due to its larger and more powerful vessels with the average length of 13 metres compared to just over 11 metres in England. On the other hand, the vessels under 10 metres represent a 79% of the fleet but contribute just 8% of capacity, supporting steady but lower value demand in small scale gear. The 20% increase in cod landings in 2022, resulting in 53% rise in the landed value, signals improved short term revenue conditions for certain segments supporting the reinvestment in compliant and selective gear amid quota controls and sustainability regulations therefore, these data show a positive impact on the market growth.

Key Fishing Equipment Market Players:

- Newell Brands (U.S.)

- Globeride (Daiwa) (Japan)

- Shimano Inc. (Japan)

- Pure Fishing (U.S.)

- Rapala VMC Corporation (Finland/Europe)

- Zebco Brands (U.S.)

- Dongmi Fishing (South Korea)

- Gamakatsu (Japan)

- St. Croix Rods (U.S.)

- Okuma Fishing Tackle (Taiwan)

- Abu Garcia (Sweden)

- Leeda (UK)

- Jarvis Walker Pty Ltd (Australia)

- Silstar (South Korea)

- Mikado Fishing Tackle (India)

- Daiwa (India)

- Cox Enterprises (U.S.)

- Archer Limited (Norway)

- Daiwa (Malaysia)

- Fox International Group (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Newell Brands holds the top position in the global fishing equipment market via its prestigious subsidiary. Leveraging a vast distribution network that spans mass retailers and specialized tackle shops, the company ensures its rods, reels, and fishing kits are accessible to beginners and hobbyists worldwide. In 2024, the company made a net sales of USD 7,582 million.

- Globeride, operating under the renowned Daiwa brand, is a dominant player in the global fishing equipment market, celebrated for its cutting-edge technological advancements. The company has positioned itself at the premium end of the market, pioneering innovations such as the Airity reel technology and advanced Zaion rod materials.

- Shimano Inc stands as a titan in the global fishing equipment market, leveraging its precision engineering heritage from Japan to produce world-class reels and rods. The company’s strategic focus relies on continuous technological innovation, strengthened by its advanced Hagane gear technology and cooler billet handle design, which set industry standards for durability and performance. In 2025, the company made a net sales of USD 3016.23 million.

- Pure Fishing employs a powerful multi-brand strategy to dominate the fishing equipment market. strategic initiatives focus on cross-brand innovation, such as combining Berkley’s soft bait technology with Abu Garcia’s reel design. This approach, coupled with a massive global distribution network, enables Pure Fishing to maintain an active presence and drive market trends.

- Rapala VMC corporation, originating from Finland, has carved a legendary niche in the global Fishing equipment market, beginning with its iconic hand-tuned balsa wood lures. The company’s strategic initiatives have successfully expanded its brand beyond lures via a series of key acquisitions, incorporating leading hook manufacturers such as VMC and terminal tackle brands.

Here is a list of key players operating in the global market:

The global fishing equipment market is defined by a highly competitive and fragmented landscape, with the key players differentiating themselves via product innovation, brand loyalty, and strategic expansion into the emerging markets. The leading companies are actively investing in research and development to produce high-performance gear using advanced materials such as carbon fiber and nanotechnology. Moreover, the strategic initiatives include mergers and acquisitions to expand the market. For example, in October 2025, Cox Enterprises announced the acquisition of Loop Tackle, which produces elite fly-fishing equipment and the conservation of wild fish populations. Further, the strong push towards sustainability with the manufacturers developing eco-friendly products and supporting the conservation efforts to appeal to the environmentally conscious modern angler. This dynamic environment pushes companies to evolve their offerings to maintain a competitive edge.

Corporate Landscape of the Fishing Equipment Market:

Recent Developments

- In December 2025, Cox Enterprises has announced the launch of Cox Outdoors, a new business segment dedicated to outdoor recreation and conservation. Cox Outdoors brings together two of Cox’s most recent investments, Loop Tackle, a company committed to producing expert fly-fishing equipment and protecting wild fish and wild places, and KUIU, a company focused on creating the world’s most innovative outdoor performance gear.

- In October 2024, Archer Limited announced that it has agreed to acquire Wellbore Fishing & Rental Tools, LLC (“WFR”). WFR is a U.S.-based well technology player focused on fishing operations in the oil and gas sector.

- In January 2024, Rapala VMC Corporation has announced that it has bought James Coble’s remaining 40 per cent shareholding of DQC International, the owner of the 13 Fishing rod and reel brand.

- Report ID: 8410

- Published Date: Mar 03, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.