Feed Processing Market Outlook:

Feed Processing Market size was valued at USD 25.2 billion in 2025 and is anticipated to reach USD 39.9 billion by the end of 2035, rising at a CAGR of 4.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of feed processing is assessed at USD 26.4 billion.

Feed processing is a vital component of the global livestock value chain, aided by the demand for animal protein and formalized feed safety oversight. According to the FAO 2023 data, the global meat production reached 362.6 million tons in 2022, while the milk production was 944 million tons, reflecting the sustained pressure on compound feed output to support the productivity and feed efficiency. Moreover, in the major livestock-producing countries, the feed milling operations are increasingly concentrated in regions with dense animal populations to minimize logistics costs. For instance, in Southeast Asia, there is a significant investment in feed milling capacity to support the growing poultry and aquaculture sectors, with the feed import dependency shifting toward value-added processing inputs such as vitamins and amino acids rather than complete feeds.

Besides, the regulatory compliance, the feed safety frameworks are also shaping the capital allocation within the feed processing ecosystem. The Food Safety Modernization Act under the U.S. FDA enforces operational protocols for animal food facilities, requiring feed manufacturers to implement hazard analysis and risk-based preventive controls. Similar regulatory policies are seen in Europe, providing scientific oversight on feed additives and risk assessment across EU member states, reinforcing traceability and hazard control standards. Further, sustainability and resource efficiency are becoming measurable priorities. According to the FAO 2026 report, the livestock supply chain accounts for nearly 14.5% of the global anthropogenic greenhouse gas emissions, boosting the feed manufacturers to improve the feed conversion ratios and optimize ingredient utilization. These policies and production dynamics sustain a steady industrial demand for modern feed processing capacity, automation upgrades, and compliance-driven facility modernization across developed and emerging feed processing markets.

Key Feed Processing Market Insights Summary:

Regional Highlights:

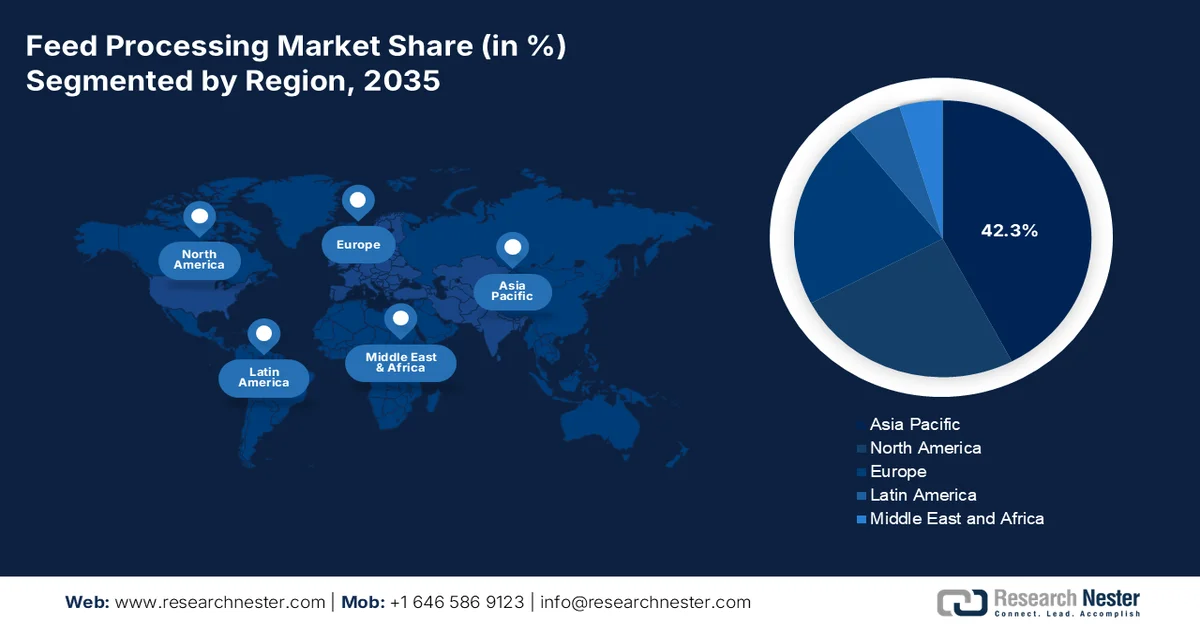

- Asia Pacific is projected to capture 42.3% share of the feed processing market by 2035, propelled by rising population-driven protein demand and government investments in industrialized feed milling capacity.

- North America is anticipated to register the fastest expansion in the market during 2026–2035, attributed to technological modernization, replacement of aging processing equipment, and growing adoption of automated energy-efficient systems.

Segment Insights:

- In the feed processing market, the Merchant/Commercial Sales sub-segment under the Trade segment is estimated to secure a 75.3% share by 2035, impelled by the large-scale presence of specialized feed manufacturers supplying external livestock producers.

- Within the Trade segment, Direct Sales are expected to remain prominent across the forecast period 2026–2035, supported by the need for customized capital-intensive feed processing machinery and strong manufacturer–mill operator collaborations.

Key Growth Trends:

- Investment in aquaculture infrastructure

- Grain production and feedstock investments

Major Challenges:

- Rising raw material price volatility

- Sustainability and traceability mandate

Key Players: Andritz AG (Austria), Bühler AG (Switzerland), CPM (California Pellet Mill) (U.S.), Muyang Group (China), SKIOLD (Denmark), Clextral (France), GEA Group AG (Germany), La Meccanica (Italy), Henan Vanmay Industry Co., Ltd. (China), ABC Machinery (China), Alvan Blanch Development Company Limited (UK), Henan Longchang Machinery Manufacturing Co., Ltd. (China), VICTOR Milling (India), Henan Dowin International Trade Co., Ltd (China), Jiangsu Degao Machinery Co., Ltd (China), Royal De Heus (Netherlands), CJ Feed & Care (South Korea), Louis Dreyfus Company (Netherlands), De Heus India (India), Fortifi Food Processing Solutions (Italy).

Global Feed Processing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 25.2 billion

- 2026 Market Size: USD 26.4 billion

- Projected Market Size: USD 39.9 billion by 2035

- Growth Forecasts: 4.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Brazil, Netherlands

- Emerging Countries: India, Vietnam, Indonesia, Thailand, Mexico

Last updated on : 12 March, 2026

Feed Processing Market - Growth Drivers and Challenges

Growth Drivers

- Investment in aquaculture infrastructure: National governments are investing heavily in aquaculture expansion to meet the rising protein demand and reduce import dependence. This directly fuels the demand for the extruders and aquatic feed processing lines, propelling the growth of the feed processing market. According to the PIB February 2026 data, the Department of Fisheries allocated nearly USD 2.18 billion under the Pradhan Mantri Matsya Sampada Yojana for the development of fisheries and aquaculture infrastructure modernization, including the feed mills. This initiative aims to double the fish production, requiring significant feed processing capacity. For equipment suppliers, these government-funded programs create predictable, multi-year demand cycles for floating feed extruders and drying systems.

- Grain production and feedstock investments: Feed processing demand is closely aligned with the government-supported grain output. According to the USDA 2025-2026 data, the global corn production reached 1.23 billion metric tons, with a major share allocated to feed use. On the other hand, the People’s Republic of China data in December 2023 reported that the national grain output rose by 1.3% YoY, reinforcing the domestic feed grain availability. Governments are prioritizing the feedstock security via input subsidies, irrigation investments, and storage infrastructure, stabilizing raw material supply for feed processors. Stable grain availability reduces price volatility and enables feed mills to operate at higher utilization rates. Public investments in warehousing, transport, and buffer stocks, therefore, directly sustain large-scale market capacity and modernization initiatives.

Corn Production (2024 to 2025)

|

Country |

Capacity (million metric tons) |

|

Brazil |

131.0 |

|

Argentina |

53.0 |

|

Ukraine |

29.0 |

|

Mexico |

25.7 |

|

South Africa |

16.5 |

Source: USDA 2025-2026

- Government subsidized feed for livestock reserves: Several nations maintain livestock reserves to ensure food security, with the governments directly subsidizing feed processing for these reserves. China’s Ministry of Agriculture and Rural Affairs manages the national hog and dairy reserves, with the provincial governments required to maintain minimum feed inventories. Moreover, the governments are allocating significant budgets for feed processing subsidies to rebuild the breeding herds. These programs create consistent government-funded demand for the processed feed, often with specific quality specifications requiring advanced milling and mixing equipment. Securing contracts for the strategic reserve feeding programs provides a stable baseload volumes that insulate the operations from the commercial feed processing market volatility, justifying investments in the production lines.

Challenges

- Rising raw material price volatility: Beyond availability, the sheer unpredictability of the ingredients' cost is the major barrier. The feed costs account for high production expenses and are driven by factors from the biofuel policy to speculative trading. For new market players operating on thin margins and without advanced hedging strategies, such volatility is a big challenge in the feed processing market. A sudden rise in corn or soybean meal prices can reduce the profitability instantly, while established players use futures and options to lock in prices and maintain budget accuracy within a narrow band.

- Sustainability and traceability mandate: New regulations require companies to show that the supply chains are deforestation-free, with traceability down to specific plots of land. Meeting this requires implementing digital traceability platforms and securing certified ingredients that often command premium prices. This represents a transformation of the supply chain that is costly and complex. New players are lacking the scale to absorb these compliance costs or the supplier relationships to guarantee certified sourcing, and may find themselves immediately excluded from the feed processing market, stopping their growth before it begins.

Feed Processing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

4.7% |

|

Base Year Market Size (2025) |

USD 25.2 billion |

|

Forecast Year Market Size (2035) |

USD 39.9 billion |

|

Regional Scope |

|

Feed Processing Market Segmentation:

Trade Segment Analysis

Under the trade segment, the merchant/commercial sales sub-segment dominates the feed processing market and is poised to hold the share value of 75.3% by the end of 2035. The dominance is due to the fact that feed production is conducted by large-scale specialized companies that sell feed externally to livestock producers rather than consuming it internally. As per the CFAES December 2023 data, the U.S. boasted nearly 5,800 commercial feed mills licensed by the FDA producing a million tons of feed and feed ingredients annually for the merchant market. This vast network of third-party manufacturers underscores the dominance of the commercial trade segment, as integrated farming operations represent a smaller fraction of total production volume, primarily serving specific poultry or swine integrators.

Distribution Channel Segment Analysis

The direct sales are dominating the segment in the feed processing market as capital-intensive machinery, such as extruders, pellet mills ad automated batching systems require high levels of customization, technical negotiation, and after-sales service. Top manufacturers engage directly with the commercial feed millers and integrators to design bespoke production lines, ensuring the equipment meets specific capacity and formulation requirements. The preference for direct sales is validated by the scale of investment in the sector. The report from the OEC 2024, Italy alone has exported over USD 110 million worth of machinery for preparing animal feeding stuff, with the majority of these high-value capital goods being procured via direct manufacturer-distributor agreements rather than retail intermediaries, highlighting the B2B nature.

End user Segment Analysis

Commercial feed manufacturers are the primary end users in the feed processing market, accounting for the largest share of the equipment purchases. These entities range from the multinational corporations to large regional cooperatives, all requiring high-throughput processing lines to produce consistent, nutritionally balanced feed at scale. Moreover, the commercial manufacturers must adhere to the stringent regulatory standards for feed safety and quality, driving the demand for advanced conditioning, pelleting, and coating technologies. Besides the animal food facilities, which include commercial manufacturers operating under the food safety modernization act represents the core customer base for the feed processing equipment suppliers, as these facilities are legally mandated to implement preventive controls that require advanced processing and monitoring machinery.

Our in-depth analysis of the feed processing market includes the following segments:

|

Segment |

Subsegments |

|

Trade |

|

|

Equipment Type |

|

|

Application |

|

|

Form |

|

|

Mode of Operation |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Feed Processing Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating and is poised to hold the largest regional revenue share of 42.3% by the end of 2035. The market is driven by the rising population and subsequent protein transition, which necessitates industrialized feed production. Governments across the region are prioritizing food security, leading to investments in domestic feed milling capacity to reduce the reliance on imported meat and fish. The major trend is the modernization of diversified small-scale mills into large automated processing facilities driven by both economic efficiency and stringent food safety standards being implemented by national authorities. For instance, China enforces strict feed quality regulations, pushing processors to upgrade to advanced grinding, mixing, and pelleting lines with the integrated traceability system. Furthermore, the government-backed aquaculture expansion is fueling the demand for the feed processing market in Asia Pacific.

Government initiatives to boost livestock productivity and aquaculture exports are driving the demand for the feed processing market in India. In February 2026, the HAFED’s 150-tonne-per-day cattle feed plant at Rohtak, along with its additional facility in Saktakhera, demonstrates state-backed cooperative participation in the organized feed manufacturing in Haryana. The modernization of legacy 100 TPD infrastructure with the upgraded processing technology reflects capacity enhancement aligned with the rising livestock productivity requirements. Moreover, the data from the DAHD March 2026 shows that the Government of India has approved a revised outlay of USD 3.16 billion under the Animal Husbandry Infrastructure Development Fund (AHIDF) up to 2025 to 2026, which explicitly includes financial support for the establishment of animal feed plants alongside dairy and meat processing infrastructure. This shows an uplift in the market growth.

Feed grain availability and substitution dynamics are shaping the feed processing market in China. According to the USDA October 2024 data, China’s total feed reached 286.5 million metric tons, indicating a continued large-scale industrial feed production. Moreover, the corn production reached 293 MMT, reinforcing corn’s dominance in the feed formulations due to the competitive pricing. Besides, the wheat production is projected to increase; however, wheat feed usage is expected to reduce as improved corn quality limits substitution. Rice production is forecast to decline slightly due to flooding, with reduced feed utilization. Collectively, stable domestic grain output, moderated import volumes, and corn-centric feed formulations support a sustained demand for large-scale grinding, batching, and pelleting infrastructure within China’s feed processing industry.

North America Market Insights

The North America is projected to emerge as the fastest growing region during the assessed period, 2026 to 2035, in the feed processing market. The market is driven by consolidation, technological upgrading, and stringent regulatory compliance. The U.S. and Canada together represent a mature, high-volume market focused on operational efficiency and food safety. The primary driver is the replacement of aging equipment with automated energy-efficient systems to reduce labor costs and meet regulatory standards. A key trend in the feed processing market in North America is the integration of data analytics for predictive maintenance and yield optimization, reducing the downtime in high-throughput mills serving poultry and swine integrators. The market is also seeing increased demand for equipment capable of processing alternative ingredients, such as insect meal and canola coproducts, driven by sustainability goals.

The sustained livestock output and grain availability, reinforced by federal agricultural oversight, are boosting the demand for the feed processing market in U.S. According to the USDA's June 2025 data, U.S. broiler production has expanded by 17.3% in 2024, reflecting stable demand for compound poultry feed. On the other had the U.S. corn production totaled 432.34 million metric tons with a significant share allocated to animal feed use, ensuring raw material availability for industrial feed mills based on the USDA 2025 to 2026 data. Further, the regulatory oversight under the Food Safety Modernization Act (FSMA), administered by the U.S. Food and Drug Administration, continues to govern over 20,000 animal food facilities nationwide, reinforcing compliance-driven capital investment in batching, conditioning, and pelleting systems as per the Georgetown Environmental Law December 2023 data. Overall, these data show a steady industrial demand for automated, high-capacity feed processing infrastructure across poultry, cattle, and swine segments.

The stable livestock output and grain production capacity are shaping the feed processing market in Canada. According to the Government of Canada, February 2025 data, total cattle and calves inventory stood at 10.9 million, reinforcing baseline demand for processed ruminant feed. Moreover, the chicken production in Canada generated USD 3.9 billion, reflecting sustained compound feed requirements under the country’s supply management framework, based on the Government of Canada August 2025 data. On the trade side, Canada has exported USD 61.1 million worth of machinery for preparing animal feed in 2024. Combined livestock scale, grain availability, and federal regulatory controls sustain steady demand for industrial feed processing systems across poultry, cattle, and swine segments in Canada.

Export Data of Machinery for Preparing Animal Feed (2024)

|

Country |

Value (USD) |

|

U.S. |

56.9M |

|

Japan |

710K |

|

Australia |

1.46M |

|

China |

201K |

Source: OEC 2024

Europe Market Insights

Europe is actively expanding the growth in the feed processing market through advanced technology and strict regulatory policies. The growth is driven by modernization, sustainability mandates, and import substitution. The European Green Deal and the Farm to Fork Strategy are the primary catalysts pushing the processors to reduce their environmental footprints via energy-efficient equipment and alternative protein processing lines. The regulatory compliance with the EU feed hygiene regulations and contaminants directives necessitates the investment in advanced cleaning, grinding, and thermal treatment systems. A key trend in the feed processing market in Europe is the consolidation with larger cooperatives acquiring smaller mills to achieve economies of scale in adopting digital monitoring and automation.

The concentrated livestock sector and stringent environmental regulations are fueling the growth of the feed processing market in Germany. According to the OEC 2024 data, Germany has exported USD 131 million worth of machinery for preparing animal feed, indicating its position as a key equipment supplier. Moreover, the advancements, such as the investment of USD 58.15 million on a pulse processing facility inaugurated by BENEO in April 2025, reinforce the domestic processing capacity for feed ingredients, mainly plant-based protein inputs such as faba beans. On the other hand, the innovation such as Ceva’s automated broiler sex separation system support the productivity optimization in poultry production, indirectly strengthening the demand for the standardized high-quality feed output, indicating a positive growth in the market.

Regulatory divergence and a national focus on food security are fueling the feed processing market in the UK. According to the Government of the UK, June 2025 data, 60% of livestock holdings in the UK incorporate ration formulation or professional nutritional guidance when determining feeding strategies for cattle and sheep, with 47% of holdings applying such support at least periodically, indicating structured feed planning and increased reliance on standardized compound feed solutions. This level demands precision batching, mixing, and quality-controlled feed processing systems. Additionally, the Cold Chain Federation August 2023 data represents nearly 300 members operating more than 450 storage facilities and over 30,000 vehicles across the UK, underscoring the scale of temperature-controlled logistics infrastructure relevant for specialty and performance feed products. These data show an active rise in the market growth.

Key Feed Processing Market Players:

- Andritz AG (Austria)

- Bühler AG (Switzerland)

- CPM (California Pellet Mill) (U.S.)

- Muyang Group (China)

- SKIOLD (Denmark)

- Clextral (France)

- GEA Group AG (Germany)

- La Meccanica (Italy)

- Henan Vanmay Industry Co., Ltd. (China)

- ABC Machinery (China)

- Alvan Blanch Development Company Limited (UK)

- Henan Longchang Machinery Manufacturing Co., Ltd. (China)

- VICTOR Milling (India)

- Henan Dowin International Trade Co., Ltd (China)

- Jiangsu Degao Machinery Co., Ltd (China)

- Royal De Heus (Netherlands)

- CJ Feed & Care (South Korea)

- Louis Dreyfus Company (Netherlands)

- De Heus India (India)

- Fortifi Food Processing Solutions (Italy)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Andritz AG is a prominent international technology group that has made significant advancements in the feed processing market by providing complete production lines and innovative systems for animal feed and aquafeed. The company has integrated its extensive experience in mechanical and thermal processing to develop advanced mills that ensure high efficiency and product quality.

- Buhler AG, a Swiss technology leader, has significantly shaped the competitive landscape of the feed processing solutions that prioritize sustainability, food safety, and digital transformation. The company has adopted strategic initiatives centered around its nutritional solutions framework, integrating advanced grinding, mixing, and pelleting technologies with its proprietary digital services platform. In 2024, the company made a turnover of USD 2.56 billion.

- CPM is a cornerstone of the global feed processing market, renowned for its robust and high-performance pelleting equipment that has set industry standards for decades. The company has made technological advancements by expanding its portfolio beyond the traditional pellet mills to include comprehensive process solutions via its subsidiaries. In 2024, the company made a revenue of USD 41.1 million.

- Muyang Group has penetrated the global feed processing market by offering comprehensive engineering solutions and high-quality equipment that cater to the specific needs of diverse geographies. The company has advanced its market position via strategic initiatives focused on total solutions contracting, providing everything from machines to turnkey feed mill projects.

- SKIOLD has established itself as a key innovator in Europe and the global feed processing market by specializing in the optimization of feed mills for efficiency and grain-to-meat traceability. The company has made significant advancements by integrating its core competencies in the grinding, dosing, and mixing with the robust digital management systems.

Here is a list of key players operating in the global feed processing market:

The global feed processing market is highly competitive and fragmented, defined by the presence of established multinational corporations and specialized regional players. The key strategic initiatives among the market leaders include a strong focus on technological innovation, mainly the integration of IoT and data analytics to create smart, automated feed mills that enhance efficiency and traceability. There is also a significant push towards sustainability with companies developing energy-efficient equipment and processes to reduce the carbon footprint of animal protein production. Mergers and acquisitions remain a prevalent strategy for market consolidation and geographic expansion, while partnerships with the feed manufacturers allow for the co-development of customized solutions. For example, in October 2025, Royal De Heus expands its Asia footprint with the acquisition of CJ Feed & Care. The competitive dynamics are shifting as companies from Asia, mainly in China and India, increase their global footprint via cost-effective manufacturing and strategic alliances.

Corporate Landscape of the Feed processing market:

Recent Developments

- In November 2025, Louis Dreyfus Company inaugurated its new specialty feed protein production line in Tianjin, as part of the Group’s strategic plans to expand its activities further downstream in the value chain and diversify its offering with value-added products, including specialty feed ingredients, as part of its Food & Feed Solutions business.

- In September 2025, De Heus India, part of De Heus Animal Nutrition, opens a new animal feed factory in Rajpura, Punjab. The factory, built with an investment of around 17 mln USD, is one of the largest and most advanced in India, carrying an installed capacity of 180 kMT with the potential to expand to 240 kMT.

- In March 2024, Fortifi Food Processing Solutions announced the launch a unified platform of global leading brands and products within food processing equipment and automation solutions. Operating in more than 15 countries spanning five continents, Fortifi provides a broad range of solutions across the food industry, including applications in protein, dairy, and fruits and vegetables.

- Report ID: 8434

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.