Feed Acidifiers Market Outlook:

Feed Acidifiers Market size was valued at USD 3.1 billion in 2025 and is projected to reach USD 5.4 billion by the end of 2035, rising at a CAGR of 5.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of feed acidifiers is assessed at USD 3.2 billion.

The global demand for the feed acidifiers market is closely related to the livestock production expansion, feed efficiency improvement programs, and antimicrobial reduction policies implemented by the public authorities. The global livestock output continues to rise as governments prioritize food security and protein availability. According to the FAO December 2022 data, the global meat production reached 362.4 million tons in 2022, while the poultry production accounted for 141 million tons, making it the fastest-growing animal protein segment. Rising poultry and swine output directly increases the demand for the feed additives that support digestive efficiency and gut health. Moreover, the meat production is expected to rise and is supported by the intensification of commercial farming systems and higher feed utilization rates.

Further, the government supported livestock productivity programs, and the feed safety regulations are driving the demand for the market. As per the NLM study published in January 2024, the U.S. has produced nearly 20,000 metric tons of chicken, maintaining its position as the world’s largest poultry producer. Moreover, the large-scale poultry operations require high-efficiency feed formulations to maintain the feed conversion ratios and reduce the bacterial contamination risks. On the other hand, the global expansion of aquaculture is contributing to a higher feed additive consumption. Feed acidifiers play a functional role in maintaining feed stability and microbial balance in aquatic feed systems where water exposure increases contamination risks. Combined with rising feed demand driven by livestock expansion and regulatory shifts toward antimicrobial stewardship, these policy frameworks are creating sustained procurement demand for feed acidifier ingredients across global feed manufacturing operations.

Key Feed Acidifiers Market Insights Summary:

Regional Highlights:

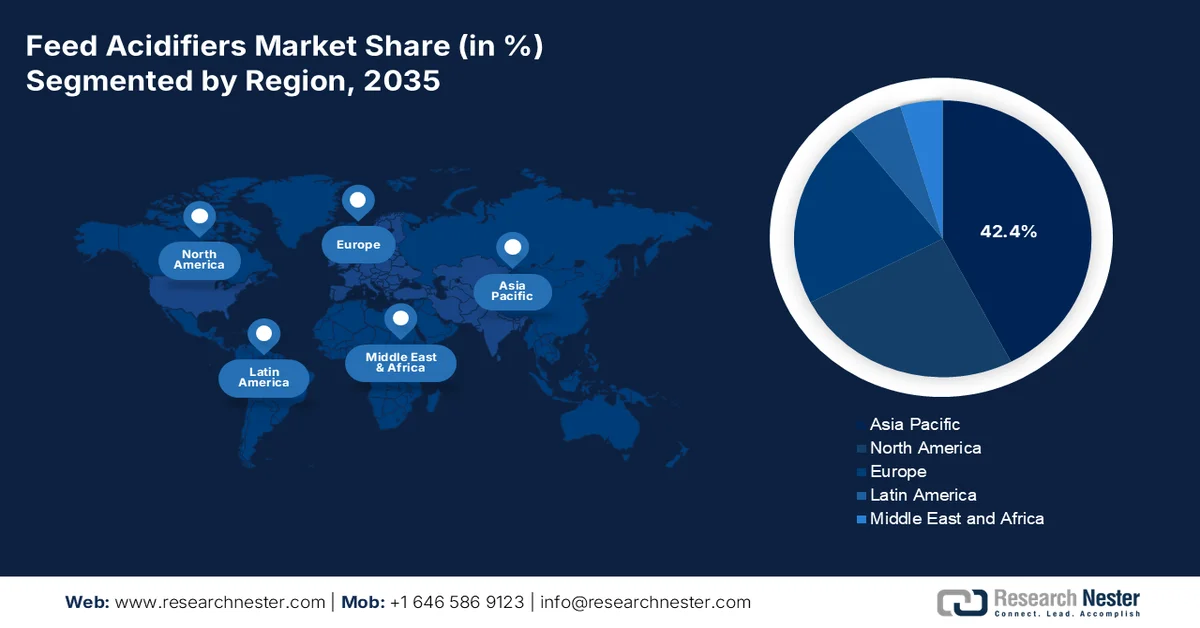

- Asia Pacific feed acidifiers market is projected to command a 42.4% share by 2035, propelled by rapid expansion of commercial livestock production to meet rising protein demand

- North America is anticipated to witness the fastest growth at a CAGR of 6.8% during 2026–2035, fueled by stringent regulations limiting antibiotic use in livestock

Segment Insights:

- In the feed acidifiers market, indirect sales segment is expected to capture 72.3% share by 2035, driven by the fragmented livestock industry relying on distributor-led rural supply networks

- The dry sub-segment is forecasted to dominate the form segment over 2026–2035, owing to its superior stability, ease of handling, and cost-effectiveness in feed milling

Key Growth Trends:

- Antimicrobial stewardship policies

- Growth in aquaculture production

Major Challenges:

- Fluctuation in raw material pricing

- Competition from alternative feed additive technologies

Key Players: Kemin Industries, Inc. (U.S.), ADM (U.S.), Perstorp Holding AB (Sweden), Corbion N.V. (Netherlands), BASF SE (Germany), Biomin (Austria), Alltech, Inc. (U.S.), Novus International, Inc. (U.S.), Selko (part of Trouw Nutrition) (Netherlands), Pancosma (Switzerland), Nutrex N.V. (Belgium), Impextraco N.V. (Belgium), Vitalac (France), Bioergex Salatas Bros SA (Greece), SOMA Inc. (South Korea), Nuacid (Ireland), Cargill (U.S.), EW Nutrition (Germany), Fonterra (New Zealand), Sri Aqua Formulations (India).

Global Feed Acidifiers Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.1 billion

- 2026 Market Size: USD 3.2 billion

- Projected Market Size: USD 5.4 billion by 2035

- Growth Forecasts: 5.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.4% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Brazil, India

- Emerging Countries: Vietnam, Thailand, Indonesia, Mexico, Philippines

Last updated on : 24 March, 2026

Feed Acidifiers Market - Growth Drivers and Challenges

Growth Drivers

- Antimicrobial stewardship policies: The government regulations restricting the use of antibiotic growth promoters in animal feed are a primary driver supporting the adoption of feed acidifiers. Moreover, the public health authorities increasingly prioritize antimicrobial resistance mitigation via stricter feed additive regulations. The European Union has banned the use of antibiotic growth promoters, and regulatory enforcement remains strong via monitoring frameworks. According to the EMA November 2022 data, the antimicrobial sales for the food processing animals in Europe declined by over 47%, reflecting the regulatory pressure to reduce antibiotic dependence. This helps the livestock producers to adopt non-antibiotic feed additives to maintain productivity and animal health. Feed acidifiers are widely used as an alternative strategy to reduce pathogenic bacteria in the digestive tract while maintaining feed efficiency. The continued expansion of antimicrobial stewardship programs across Europe and other developed markets is expected to sustain long-term demand for acidifier-based feed solutions across the poultry and swine industries.

- Growth in aquaculture production: Government initiatives to expand aquaculture output are creating a new demand for the feed acidifiers used in the aquatic feed formulations. Aquaculture has become a vital component of the global food supply strategies. According to the FAO June 2024 data, the global aquaculture production reached 130.9 million tons, accounting for over 51% of the aquatic animal food consumed worldwide. Many governments are investing heavily in aquaculture infrastructure and feed development to reduce the reliance on wild fisheries. Aquaculture feed systems require microbial stability due to exposure to water and environmental contamination risks. Feed acidifiers is market therefore widely used to stabilize feed quality and improve nutrient digestibility in aquatic species.

- Rising feed production: Government policies are aiding the feed grain production and the livestock farming, and are contributing to the compound feed manufacturing volumes, which are indirectly boosting the demand for the feed additives. The IFIF June 2023 data reports that the global compound feed production exceeds 1 billion, reflecting the large-scale livestock operations requiring the nutritionally optimized feed formulations. Moreover, the government continues to support the feed grain production via agricultural subsidies and food security initiatives. As feed manufacturing expands, the feed producers integrate additives such as organic acids to improve feed conversion efficiency and maintain microbial stability. The scale of global feed production supported by public agricultural policies, therefore, represents a significant structural driver for the market.

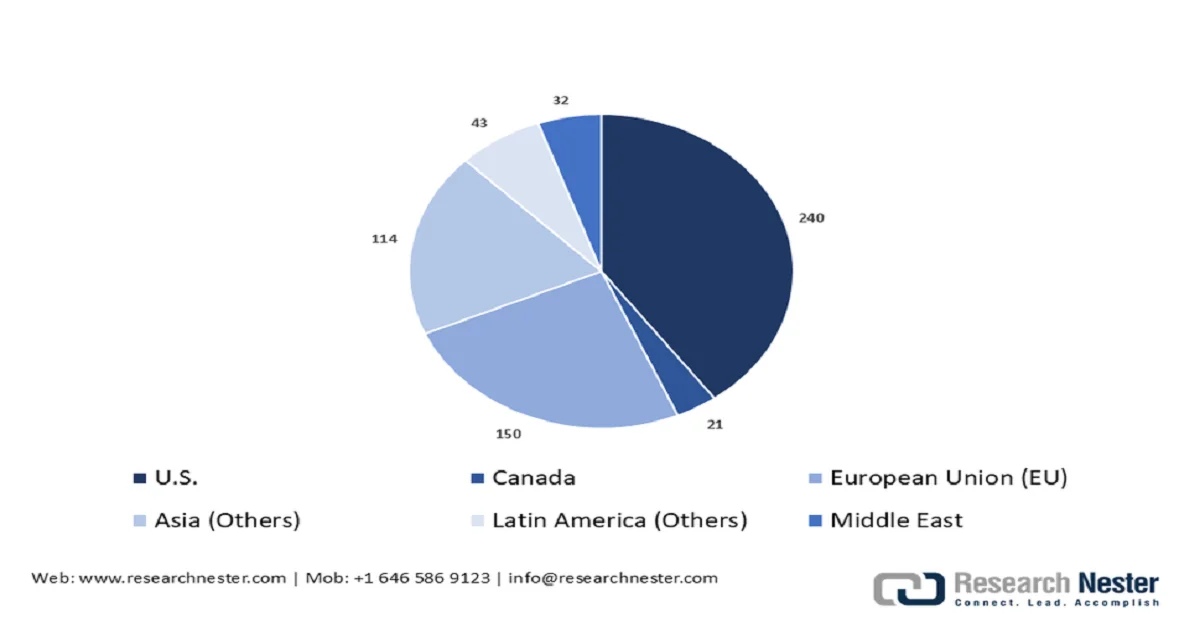

Global Compound Feed Production, 2023

Source: IFIF June 2023

Challenges

- Fluctuation in raw material pricing: The feed acidifiers market relies on the organic acids sourced from the complex agricultural and chemical supply chains, making them highly vulnerable to price instability. The climate conditions, energy costs, and geopolitical development can trigger significant price fluctuations that make cost control extremely difficult, mainly for the new entrants with limited purchasing power. This volatility was intensified when the rapid implementation of the tariffs changed the global trade flows, directly affecting the organic acid supplies from the key producing regions.

- Competition from alternative feed additive technologies: The market competes against a growing array of alternative additives, including probiotics, prebiotics, enzymes, phytogenics, and herbal products that may offer cost advantages or specific suitability. The large integrated producers often use mixtures or switch to alternatives to optimize the costs, limiting the acidifiers' market share. This substitution threat is mainly acute for new entrants offering an undifferentiated single acid product. Further, the top players are developing proprietary blends and enzyme-activated formulations that create technological trenches.

Feed Acidifiers Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.7% |

|

Base Year Market Size (2025) |

USD 3.1 billion |

|

Forecast Year Market Size (2035) |

USD 5.4 billion |

|

Regional Scope |

|

Feed Acidifiers Market Segmentation:

Distribution Channel Segment Analysis

Under the distribution channel segment, the indirect sales are dominating and are poised to hold the share value of 72.3% by the end of 2035 in the feed acidifiers market. This dominance is driven by the fragmented nature of the livestock industry, where thousands of small to mid-sized farms rely on the local agricultural supply stores for their nutritional inputs. Distributors provide critical value by consolidating products from multiple manufacturers, offering technical advice, and managing complex logistics and inventory customized to regional farming practices. Moreover, the distributors strengthen market penetration by leveraging established rural retail networks and long-standing relationships with the feed mills and livestock producers. Their ability to provide the localized product availability and technical extension services further accelerates the adoption of the feed acidifiers across diverse farming systems.

Form Segment Analysis

Within the form segment, the dry sub-segment is leading and is projected to hold the largest share value during the assessed period in the market. The dominance is due to its superior stability, ease of handling, and cost-effectiveness in the feed milling. Dry acidifiers offer a longer shelf life compared to liquids, are simpler to transport and store, and can be homogenously mixed into the compound feeds without specialized liquid application equipment. This makes it a preferred choice for the large-scale integrated feed manufacturers who prioritize operational efficiency and feed consistency. According to the KVIC March 2023 data, the cost of the dry fodder is USD 0.024 per kg. Furthermore, dry formulations enhance dosing accuracy and ensure uniform acidifier distribution in compound feed production.

Composition Segment Analysis

Blended component acidifiers are projected to command the largest share value in the market by the end of 2035, as synergistic mixtures of organic acids, inorganic acids, and salts offer superior efficacy over single-component products. These blends are scientifically formulated to target different sections of the animal’s gastrointestinal tract, providing a broader spectrum of pathogen control and more consistent pH regulation. A blend might contain fast-acting formic acid in the stomach and slow-release butyric acid in the intestine. The European Food Safety Authority, Scientific Opinion on the safety and efficacy of feed additives, confirmed that properly formulated acidifier blends demonstrate enhanced biological activity without increasing toxicological risks. The EFSA report emphasized that blends allow for lower inclusion rates of individual acids while achieving greater overall efficacy, aligning with industry goals for sustainable, high-performance animal nutrition and reducing the environmental load of feed additives.

Our in-depth analysis of the feed acidifiers market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Form |

|

|

Livestock |

|

|

Composition |

|

|

Function |

|

|

Formulation |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Feed Acidifiers Market - Regional Analysis

APAC Market Insights

Asia Pacific dominates the global feed acidifiers market and is projected to hold the regional share value of 42.4% by the end of 2035. The market is driven by the rapid expansion of commercial livestock production to meet the rising protein demand. Unlike the Western market, where regulation is the primary driver, the APAC growth is fueled by the production scale and food safety requirements for the export market. China remains the world’s largest pork producer, while Vietnam and Thailand have expanded the poultry integration to supply global markets. A key trend is the intensive production system that requires acidifiers for pathogen control and feed preservation in humid tropical climates. Government initiatives to modernize agriculture, such as India's National Livestock Mission and China's Five-Year Plans for agricultural modernization, include support for veterinary health infrastructure.

The transformation of poultry from backyard farming to commercial integration is driving the market in India. As per the Agri Export report 2022, the Department of Animal Husbandry and Dairying under India's Ministry of Fisheries, Animal Husbandry and Dairying reported that the livestock sector contributes 4.35% to the national GDP. The National Action Plan on Antimicrobial Resistance, coordinated by the Ministry of Health, includes strategies to reduce antibiotic use in food animals, creating regulatory impetus for acidifier adoption. Moreover, the export-driven quality requirements for Indian seafood and poultry are the key trends for the market growth. Further, India's poultry feed production reached approximately 9 million metric tons, creating substantial addressable volume for acidifier suppliers targeting organized commercial farms.

High feed import dependence and strict regulatory oversight on the feed safety and animal health are shaping the feed acidifiers market in Japan. The country relies on compound feed to sustain its poultry, swine, and aquaculture sectors, which require additives to maintain digestive stability and feed hygiene. According to the IFIF June 2023 data, Japan produced 24 million tons of compound animal feed, reflecting the scale of the feed manufacturing supporting the commercial livestock operations. Poultry production is a major demand driver, as the Government of Canada reported that Japan produced around 2.4 million tons of chicken meat, requiring efficient feed formulations to maintain productivity in intensive farming systems. These factors collectively support the steady integration of feed acidifiers across Japan’s livestock and aquaculture feed industries.

North America Market Insights

North America is projected to be the fastest-growing market, anticipated to expand at a CAGR of 6.8% during the forecast period, 2026 to 2035. The market in North America is driven by the stringent regulatory frameworks governing antibiotic use in livestock, mainly in the U.S., and the FDA’s guidance for industry promoting antibiotics. This regulatory environment pushes producers to adopt acidifiers for disease prevention and gut health management. The key trend is the consolidation of poultry and swine operations, leading to centralized purchasing decisions and demand for the scientifically validated, consistent formulations. The producers are actively seeking blended acidifier solutions that offer synergistic effects against pathogens like Salmonella and E. coli, rather than single-component products.

The large scale livestock production system and increasing regulatory focus on the feed safety and antimicrobial stewardship are driving the growth of the feed acidifiers market in the U.S. The poultry and swine sectors represent a major consumption base for the compound feed additives, which are used to maintain gut health and improve feed efficiency. According to the USDA June 2025 data, broilers hold the majority share in the poultry sector with USD 45.4 billion, reflecting the scale of intensive poultry production that depends heavily on optimized feed formulations. Moreover, the USDA January 2025 data states that the U.S. is the second largest exporter of pork meat, increasing the demand for feed additives that support animal performance and pathogen control in commercial farming systems. The data show an active upliftment in the U.S. market

Large livestock sector, strong feed grain production, and regulatory oversight on the feed safety and antimicrobial use are driving the market in Canada. The country maintains a significant commercial animal production industry that relies heavily on nutritionally optimized feed. According to the Government of Canada, September 2025 data, the country produced around 2.34 million tons of pork, with pork representing one of Canada’s largest livestock export commodities. The poultry sector is also a key driver of feed additive demand. Statistics Canada's August 2025 data recorded approximately 15.3 million tons of corn production, a major ingredient used in compound livestock feed. On the other hand, the livestock feed under the Feeds Regulations to ensure feed safety and proper additive usage, promotes producers to adopt feed management solutions that reduce pathogen risk and improve feed efficiency. The strict federal feed safety regulations continue to support the integration of acid-based feed additives across Canada’s poultry, swine, and ruminant production systems.

Europe Market Insights

The feed acidifiers market in Europe is expanding significantly and is driven by the European Union’s long-standing regulatory framework against antibiotic growth promoters. This regulatory head start has created a mature market where the acidifiers are standard practice in livestock production. The key drivers include the European Green Deal and the Farm to Fork Strategy, which set ambitious targets to reduce antimicrobial sales, intensifying the demand for alternatives. Another significant trend is the shift toward precision livestock farming, where the acidifiers are integrated into the automated feeding systems for the consistent delivery. Producers are also demanding multi-functional blends that combine the acidifiers with the essential oils or probiotics for synergistic gut health benefits. The market is characterized by strong quality and safety standards.

The feed acidifiers market in UK is supported by the country’s well-established livestock and feed manufacturing sectors, alongside regulatory emphasis on feed hygiene and antimicrobial stewardship. Poultry production is one of the largest drivers of feed consumption, requiring nutritionally balanced feed formulations to support digestive health and microbial control. According to the Government of the UK’s February 2026 data, the country has produced 181.9 thousand tonnes of poultry meat. This data reflects the scale of intensive poultry farming and its reliance on compound feed systems. Regulatory oversight further demands safe feed additives due to the strict requirements for feed safety and hygiene under the EU feed regulations to prevent contamination and maintain animal health standards. These factors support the continued integration of the feed acidifiers within the commercial feed formulations across the UK livestock sector.

UK Poultry Production, 2026

|

Category |

Indicator |

January 2026 |

Change vs Jan 2025 |

|

Chick Placements |

Commercial Layer Chick Placings |

3.4 million chicks |

↓ 5.4% |

|

Chick Placements |

Broiler Chick Placings |

99.8 million chicks |

↑ 0.1% |

|

Chick Placements |

Turkey Poult Placings |

0.6 million chicks |

↑ 25% |

|

Slaughter Statistics |

Broiler Slaughterings |

96.6 million birds |

↓ 2.6% |

|

Slaughter Statistics |

Turkey Slaughterings |

0.5 million birds |

↑ 0.3% |

|

Production |

Total Poultry Meat Production |

181.9 thousand tonnes |

↑ 1.3% |

Source: Government of the UK, February 2026

The strong compound feed manufacturing industry and strict regulatory framework governing feed safety and antimicrobial usage are shaping the market in Germany. According to the European Parliament's February 2023 data, the EU member states produced 150.2 million tons of compound feed, and Germany produced nearly 16% of the overall production, reflecting the scale of the feed production supporting the intensive livestock systems. Poultry and pork production are key demand drivers for feed additives that help maintain gut health and improve the feed conversion efficiency. As per the report from the German Meat July 2025 data, Germany produced 4.3 million tonnes of pork. Moreover, Germany also remains one of Europe’s largest pork producers. These data support a steady adoption of feed acidifiers across Germany’s poultry and swine feed industries.

Key Feed Acidifiers Market Players:

- Kemin Industries, Inc. (U.S.)

- ADM (U.S.)

- Perstorp Holding AB (Sweden)

- Corbion N.V. (Netherlands)

- BASF SE (Germany)

- Biomin (Austria)

- Alltech, Inc. (U.S.)

- Novus International, Inc. (U.S.)

- Selko (part of Trouw Nutrition) (Netherlands)

- Pancosma (Switzerland)

- Nutrex N.V. (Belgium)

- Impextraco N.V. (Belgium)

- Vitalac (France)

- Bioergex Salatas Bros SA (Greece)

- SOMA Inc. (South Korea)

- Nuacid (Ireland)

- Cargill (U.S.)

- EW Nutrition (Germany)

- Fonterra (New Zealand)

- Sri Aqua Formulations (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Kemin Industries, Inc. continues to strengthen its position in the feed acidifiers market via focused product innovation and the application of advanced encapsulation technologies. The company has launched an innovative feed additive for the U.S. swine market that uses a proprietary blend of encapsulated calcium formate and citric acid.

- ADM uses its vast global footprint and diversified portfolio to maintain a leading role in the market. Through its animal nutrition division, ADM provides a comprehensive range of feed acidifiers designed to improve gut health and feed efficiency across various livestock species, including poultry, swine, and aquaculture. In 2024, the company made a total revenue of USD 85,530.

- Perstorp Holding AB is executing a clear strategy to expand its footprint in the global feed acidifiers market with a particular focus on the high-growth APAC region. As a specialist in organic acid-based feed additives, the company develops esterified organic acids designed for targeted release in the digestive tract to optimize gut health and feed efficiency.

- Corbion N.V. distinguishes itself in the market by focusing on bio-based and sustainable ingredient solutions. As a leading player in the market, the company leverages its deep expertise in fermentation and biochemistry to produce high-purity lactic acid and other organic acids used in feed applications. According to the 2024 annual report, the company has made a growth of 5.2% in 2024.

- BASF SE leverages its position as a global chemical giant to maintain a stronghold in the market via extensive R&D capabilities and a comprehensive product portfolio. As one of the top key players identified in the market, the company focuses on developing high-quality organic acid-based formulations that optimize pH levels in livestock and inhibit pathogenic bacteria growth.

Here is a list of key players operating in the global market:

The global feed acidifiers market is defined by the intense competition driven by the phasing out of antibiotic growth promoters and the rising demand for sustainable animal nutrition. The competitive landscape features a mix of the large multinational corporations with broad portfolios and significant R&D capabilities, and regional players who succeed with specialized, locally customized formulations. The key strategic initiatives among top players include heavy investment in innovative technologies such as encapsulation for targeted release, the development of synergistic acid blends, and the strategic partnership to expand their portfolio. For example, in September 2024, Cargill acquired two U.S. feed mills, strengthening production and distribution capabilities to grow with customers. Further, the market leaders are differentiating themselves by offering technical support services that directly enhance the feed hygiene and animal health for their customers.

Corporate Landscape of the Feed Acidifiers Market:

Recent Developments

- In January 2025, EW Nutrition confirmed two names were added to key positions in its global team. From January 2025, Marie Gallissot and Nadia Yacoubi have joined the German-headquartered animal nutrition company.

- In December 2024, Perstorp Holding AB acquired 100% of the shares of OQ Chemicals Nederland B.V. from OQ Chemicals GmbH. The deal provides Sweden-based Perstorp with full ownership and control over all of the Dutch company’s production assets, related technology, and employees.

- In August 2024, Fonterra teamed up with Superbrewed Food, a natural ingredient manufacturer, to develop functional biomass protein from the Co-op’s lactose. The aim is to create more value from milk by converting lactose into high-quality, sustainable protein using Superbrewed's technology.

- Report ID: 8469

- Published Date: Mar 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.