Environmental Monitoring Market Outlook:

Environmental Monitoring Market size was valued at USD 30.2 billion in 2025 and is projected to reach USD 68.1 billion by the end of 2035, rising at a CAGR of 8.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of environmental monitoring is evaluated at USD 32.7 billion.

The environmental monitoring has become a central operational requirement across the industrial manufacturing, energy, agriculture, water management, and urban infrastructure, as governments expand regulatory oversight of air, water, and soil quality. In the U.S. EPA operates extensive national monitoring programs that require continuous measurement of pollutants such as particulate matter, ozone, nitrogen dioxide, and sulfur dioxide via an air quality system network. According to the EPA, October 2025 data, there are more than 4,000 monitoring stations across the country that report real-time air pollution data used for regulatory enforcement and environmental planning. The public spending also reflects the scale of the monitoring infrastructure. Moreover, the U.S. federal budget allocated over USD 10.994 billion to the EPA, supporting the environmental compliance programs, including air and water monitoring networks and environmental data systems, enabling a positive growth in the environmental monitoring market.

Further, the environmental capacity is also expanding globally as the government strengthens the environmental reporting requirements and climate resilience programs. According to the WHO April 2022 data, nearly 99% of the global population lives in areas exceeding the WHO air quality guidelines limits, which has stimulated national investments in monitoring infrastructure and public data platforms. The European Environment Information and Observation Network depicts that over 3,500 air quality monitoring Is installed in more than 100 countries. Furthermore, the governments are increasingly integrating digital sensor networks, satellite observations, and automated sampling platforms to improve compliance monitoring and environmental risk detection across the industrial corridors and urban centers. These developments indicate a growth that requires consistent environmental measurement and reporting across the sectors, including energy generation, transport management, and agriculture.

Key Environmental Monitoring Market Insights Summary:

Regional Highlights:

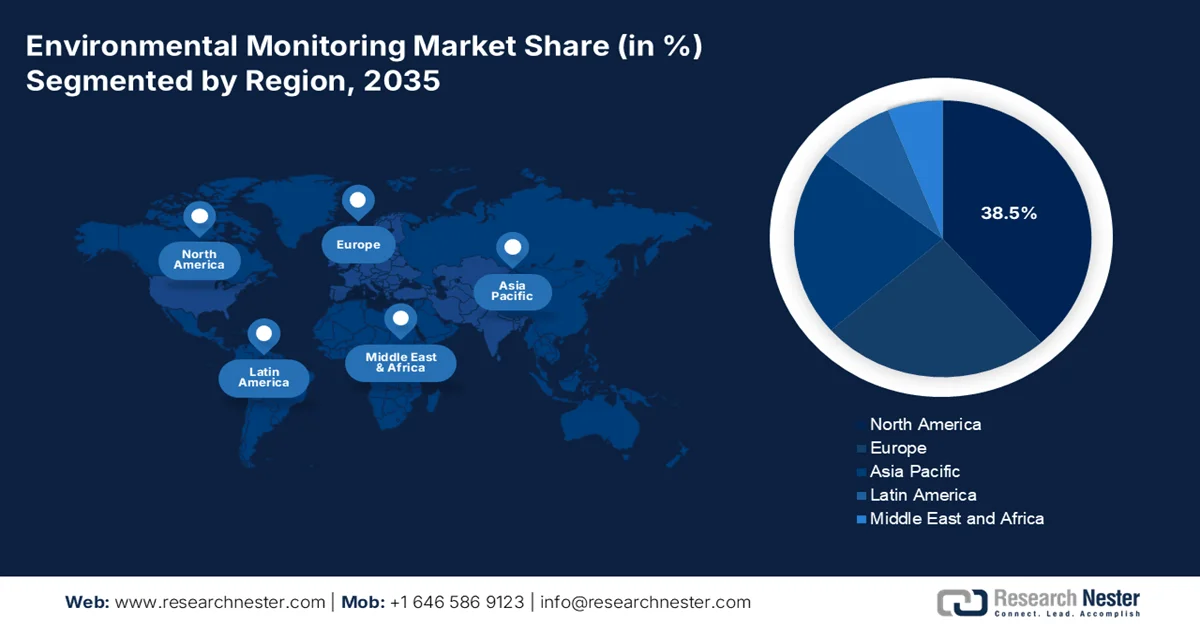

- North America environmental monitoring market is anticipated to command a 38.5% revenue share by 2035, attributed to stringent regulatory frameworks and substantial federal infrastructure investments.

- Asia Pacific is projected to witness the fastest expansion during 2026–2035 with a CAGR of 7.8%, fueled by rapid industrialization, urbanization, and escalating government responses to deteriorating air and water quality.

Segment Insights:

- Under the connectivity segment, the wireless monitoring systems sub-segment in the environmental monitoring market is projected to account for a 65.4% share by 2035, propelled by the need for real time wide area data acquisition.

- Within the sampling method, the continuous monitoring segment is anticipated to lead by 2035, stimulated by its ability to provide uninterrupted real-time compliance data..

Key Growth Trends:

- Public spending on water quality monitoring

- Climate monitoring and national adaptation programs

Major Challenges:

- High R&D costs

- High customer switching costs

Key Players: Thermo Fisher Scientific Inc., Danaher Corporation, Agilent Technologies, Inc., PerkinElmer, Inc., Teledyne Technologies Incorporated, Emerson Electric Co., Honeywell International Inc., Merck KGaA, Siemens AG, Shimadzu Corporation, Horiba, Ltd.

Global Environmental Monitoring Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 30.2 billion

- 2026 Market Size: USD 32.7 billion

- Projected Market Size: USD 68.1 billion by 2035

- Growth Forecasts: 8.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Singapore, United Arab Emirates

Last updated on : 12 March, 2026

Environmental Monitoring Market - Growth Drivers and Challenges

Growth Drivers

- Public spending on water quality monitoring: Water contamination risks and stricter discharge regulations are increasing the investments in water monitoring infrastructure. Governments are expanding river groundwater and drinking water surveillance networks to detect pollutants such as heavy metals pathogens and industrial chemicals. The June 2021 data shows that USGS operates over 13,500 real time streamflow and water monitoring stations used for water resource management and contamination tracking. According to the EPA October 2024 data, the Bipartisan Infrastructure Law allocated USD 50 billion for water infrastructure improvements including monitoring and testing for drinking water safety and contamination risks. These initiatives require analytical instruments automated sensors and data systems for continuous monitoring enabling the growth of environmental monitoring market.

- Climate monitoring and national adaptation programs: Climate change monitoring programs are creating a sustained demand for environmental data collection systems. The governments are deploying atmospheric, oceanic, and land monitoring infrastructure to support climate modeling and policy planning. As per the Budget of the U.S. government data published in March 2023, the National Oceanic and Atmospheric Administration received USD 7 billion for climate-related funding supporting climate observation systems, including weather stations, satellite monitoring platforms, and ocean sensors. These systems track temperature, precipitation, atmospheric gases, and extreme weather events. These investments are expected to drive the environmental monitoring market and fuel the procurement of environmental sensors, remote monitoring equipment, and environmental data management platforms.

- Industrial emission compliance: Industrial sectors are expanding the environmental monitoring adoption to comply with the stricter emission regulations. The governments are enforcing the air, water, and soil pollution monitoring requirements for industries, including the power generation, oil and gas, chemicals, and mining. In the U.S., the Clean Air Act requires industrial facilities to monitor the emissions of the regulated pollutants with the reported via EPA compliance systems. According to the EPA, December 2025 data from the EPA Enforcement and Compliance History Online data show that over 100,000 regulated facilities report environmental compliance data annually. On the other hand, in Europe, the Industrial Emissions Directive requires continuous emission monitoring systems across the major industrial plants. These are creating a sustained environmental monitoring market demand.

Challenges

- High R&D costs: The environmental monitoring market is shifting rapidly toward IoT enabled real time and AI-integrated systems, demanding continuous and expensive innovation, which can be a major hurdle for companies with limited R&D budgets. New entrants must compete with the top players who are already integrating their instruments with cloud-based analytics and AI. Top players are actively investing in making their instruments compatible with the AI engines to help customers interpret the massive amounts of data generated, while also focusing on automation to give lab technicians more scientific hours.

- High customer switching costs: Customers mainly in the industrial and laboratory settings face high switching costs, making it difficult for new vendors to displace competitors. These costs are not just financial but also operational, involving requalification of methods, staff retraining, and integration with existing laboratory information management systems. A new entrant offering only a standalone instrument struggles to compete with such comprehensive, integrated offerings in the environmental monitoring market.

Environmental Monitoring Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.5% |

|

Base Year Market Size (2025) |

USD 30.2 billion |

|

Forecast Year Market Size (2035) |

USD 68.1 billion |

|

Regional Scope |

|

Environmental Monitoring Market Segmentation:

Connectivity Segment Analysis

Under the connectivity segment, the wireless monitoring systems sub-segment is expected to hold the largest share value of 65.4% by the end of 2035 in the environmental monitoring market. The segment is driven by the need for the real time wide area data acquisition. By transitioning from manual data logging to interconnected sensor networks, environmental agencies and industries can now monitor conditions with granular spatial and temporal resolution. The expansion of the low-power wide-area networks and 5G infrastructure allows thousands of sensors to stream data on air quality and water levels to centralized platforms instantaneously. This shift reduces the latency between a pollution event and the response, enabling smarter urban planning and industrial compliance. further the availability of portable air sensors indicates the environmental monitoring market shift toward accessible connected devices for community-based monitoring.

Sampling Method Segment Analysis

Within the sampling method, the continuous monitoring is leading the segment in the environmental monitoring market by the end of 2035. The dominance is due to its ability to provide uninterrupted real-time compliance data. Unlike the portable or passive methods that offer snapshots, fixed monitoring stations utilize advanced analyzers to track pollutant fluctuations, which is essential for industrial facilities operating under strict emission caps. These systems are critical for detecting fugitive leaks and ensuring that the regulatory thresholds are not exceeded during operational peaks. According to the UPCCCE April 2024 data, 2500 industries that installed continuous emission monitoring systems reflect a significant shift toward automated round-the-clock environmental governance.

Pollutants Target Segment Analysis

The chemical pollutants sub-segment is leading the pollutant target segment in the environmental monitoring market. This dominance is fueled by the urgent need to detect both the legacy contaminants and the emerging threat such as the PFAS in drinking water and VOC emissions in urban industrial zones. The precision required to measure these toxins at parts per trillion levels drives the continuous investment in advanced instrumentation, such as gas chromatographs and mass spectrometers. Moreover, the critical nature of this monitoring is underscored by the recent federal initiatives. According to the Project Censored August 2025 data, the White House announced that nearly USD 9 billion is being allocated via the Bipartisan Infrastructure Law specifically to address the PFAS and other emerging chemical contaminants in water systems nationwide.

Our in-depth analysis of the environmental monitoring market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Sampling Method |

|

|

Components |

|

|

Application |

|

|

End user |

|

|

Pollutants Target |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Environmental Monitoring Market - Regional Analysis

North America Market Insights

North America is dominating and is expected to hold the largest regional revenue share of 38.5% in the environmental monitoring market by the end of 2035. The market is driven by the stringent regulatory frameworks and substantial federal infrastructure investments. The U.S. dominates the regional demand via EPA enforcement of Clear Air Act. The key drivers include the aging monitoring infrastructure replacement, community air monitoring expansion under the environmental justice initiatives and greenhouse gas verification requirements. The market benefits from well-established laboratory networks, continuous emission monitoring systems installations at industrial facilities, and integrated water quality surveillance programs. Further, this leadership is reinforced by the rapid deployment of PFAS monitoring funding under the Bipartisan Infrastructure Law, ensuring sustained procurement cycles for the next decade.

The rising federal investments in pollution control, climate programs, and water safety regulations are expanding the environmental monitoring market in the U.S. According to the EPA, October 2025 data, USD 325 million is funded for 21 environmental and climate justice projects via the Community Change Grants Program. On the other hand, the Bipartisan Infrastructure Law allocated USD 9 billion specifically to address PFAS contamination and emerging contaminants in drinking water, as per the EPA April 2024 data. Moreover, the EPA also introduced the first national enforceable drinking water standards for PFAS chemicals, affecting around 66,000 public water systems, with an estimated 6% to 10% of systems needing monitoring and remediation actions. These regulatory developments are increasing demand for environmental monitoring, and the long-term monitoring programs, such as CASTNET and national air quality monitoring systems, continue to support ongoing investments in environmental data infrastructure across the U.S.

Major U.S. Environmental Monitoring Programs

|

Program |

Managing Organization |

Monitoring Focus |

Key Data Collected |

|

Clean Air Status and Trends Network (CASTNET) |

U.S. Environmental Protection Agency (EPA) Office of Air and Radiation |

Long-term monitoring of air pollutant concentrations and atmospheric deposition |

Ozone, sulfur dioxide, nitrogen compounds, particulate pollutants, dry deposition data |

|

Long-Term Monitoring (LTM) Program |

U.S. Environmental Protection Agency (EPA) |

Monitoring chemical changes in surface water affected by air pollution and acid deposition |

Surface water chemistry in lakes and streams, sulfate, nitrate, and acidity levels |

|

National Atmospheric Deposition Program (NADP) |

Cooperative program involving federal, state, tribal agencies, universities, and NGOs |

Monitoring wet atmospheric deposition across North America |

Sulfur, nitrogen, mercury, and precipitation chemistry |

|

Air Quality System (AQS) |

U.S. Environmental Protection Agency (EPA) |

National repository for ambient air quality monitoring data |

Air pollutant measurements from regulatory monitoring stations |

Source: EPA August 2025

The air quality surveillance programs and pollutant monitoring initiatives are shaping the demand for the environmental monitoring market in Canada. The National Air Pollution Surveillance Program measures air pollutant concentrations across the country via a large network of monitoring stations used to track the particulate matter and nitrogen dioxide levels. According to the Government of Canada, February 2026 data, the annual average peak PM2.5 concentrations in 2023 were recorded at 204 monitoring stations across Canada. Moreover, in these stations, 120 recorded concentrations above the standard of 27 micrograms per cubic meter mainly in provinces such as Alberta, Ontario, Quebec, and British Columbia, which are major industrial and urban regions. These monitoring networks generate continuous environmental datasets used for regulatory compliance, pollution control policies, and public health protection, supporting demand for air quality sensors, pollutant analyzers, and environmental data systems across Canada.

APAC Market Insights

The APAC is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to grow at a CAGR of 7.8%. This growth is driven by the rapid industrialization, urbanization, and escalating government responses to deteriorating air and water quality. China’s comprehensive ecological redline policy mandates monitoring across certain territory, while India’s National Clean Air Programme targets non-attainment cities for air quality improvement. The Asian Development Bank 2026 data depict that USD 41.9 billion is committed towards environmental sustainability. Further, the transboundary pollution concerns, particularly regarding haze and marine debris, are driving regional cooperation and standardized monitoring protocols.

The environmental monitoring market in India is expanding due to the air quality programs, pollution control regulations, and government investments in environmental surveillance infrastructure. According to CSPS December 2023 data, the monitoring network covers over 473 cities and towns with more than 1,296 monitoring stations measuring pollutants such as particulate matter, sulfur dioxide, nitrogen dioxide, and ozone. Further, the National Ambient Air Quality Monitoring Programme was allocated USD 7.7 million, with USD 7.0 million utilized for operation and maintenance of monitoring stations, expansion of PM2.5 monitoring, and establishment of new manual monitoring sites. Moreover, USD 0.46 million was dedicated to the operation and maintenance of Continuous Ambient Air Quality Monitoring stations, with 14 stations currently managed by the Central Pollution Control Board. These data show a rising demand for the monitoring technologies in India.

Air Quality Monitoring Stations in India under Automatic and Manual

|

State |

Real Time Under (CAAQMS) |

Manual Under (NAMP) |

||

|

No. of Cities |

No. of Stations |

No. of Cities |

No. of Stations |

|

|

Andhra Pradesh |

7 |

8 |

15 |

72 |

|

Arunachal Pradesh |

1 |

1 |

2 |

2 |

|

Assam |

3 |

5 |

13 |

31 |

|

Bihar |

25 |

35 |

7 |

8 |

|

Chhattisgarh |

4 |

10 |

5 |

17 |

|

Goa |

0 |

0 |

18 |

18 |

|

Gujarat |

6 |

17 |

7 |

24 |

|

Haryana |

24 |

30 |

3 |

5 |

|

Himachal Pradesh |

1 |

1 |

14 |

25 |

|

Jharkhand |

1 |

1 |

7 |

10 |

|

Karnataka |

24 |

34 |

18 |

30 |

|

Kerala |

8 |

9 |

12 |

29 |

|

Madhya Pradesh |

15 |

19 |

15 |

42 |

|

Maharashtra |

11 |

41 |

27 |

80 |

|

Manipur |

1 |

2 |

1 |

1 |

|

Meghalaya |

1 |

2 |

7 |

11 |

|

Mizoram |

1 |

1 |

8 |

19 |

|

Nagaland |

1 |

1 |

2 |

10 |

|

Odisha |

10 |

10 |

16 |

38 |

|

Punjab |

8 |

8 |

38 |

52 |

|

Rajasthan |

8 |

10 |

8 |

39 |

|

Sikkim |

1 |

1 |

8 |

9 |

|

Tamil Nadu |

13 |

22 |

16 |

55 |

|

Telangana |

3 |

14 |

11 |

25 |

|

Tripura |

1 |

2 |

1 |

2 |

|

Uttar Pradesh |

20 |

57 |

27 |

84 |

|

Uttarakhand |

1 |

1 |

6 |

12 |

|

West Bengal |

6 |

14 |

44 |

83 |

|

Andaman & Nicobar (UT) |

0 |

0 |

2 |

3 |

|

Chandigarh (UT) |

1 |

3 |

1 |

5 |

|

DNH and Daman & Diu (UT) |

0 |

0 |

4 |

6 |

|

Delhi (UT) |

1 |

40 |

1 |

10 |

|

Jammu & Kashmir (UT) |

1 |

1 |

18 |

31 |

|

Lakshadweep (UT) |

0 |

0 |

1 |

1 |

|

Pondicherry (UT) |

1 |

1 |

2 |

6 |

|

Andaman & Nicobar (UT) |

0 |

0 |

2 |

3 |

|

Chandigarh (UT) |

1 |

3 |

1 |

5 |

|

DNH and Daman & Diu (UT) |

0 |

0 |

4 |

6 |

|

Delhi (UT) |

1 |

40 |

1 |

10 |

|

Jammu & Kashmir (UT) |

1 |

1 |

18 |

31 |

|

Lakshadweep (UT) |

0 |

0 |

1 |

1 |

Source: CSPS December 2023

The stringent environmental regulations, national air quality surveillance programs, and government investments in pollution control technologies are driving the environmental monitoring market in Japan. According to the NLM June 2025 data, the national monitoring system includes more than 1,900 air pollution monitoring stations measuring pollutants across urban and industrial regions. Moreover, the Green Space 2021 data depicts that the national average PM2.5 concentration recorded at 5.8 µg/m³ in 2021, reflecting the improvements from previous years due to emission control policies and technological upgrades. In addition to air monitoring, Japan also operates nationwide water and marine environmental monitoring programs to track pollutants and protect coastal ecosystems, supporting broader environmental data collection and regulatory compliance efforts.

Europe Market Insights

The Europe represent an expanding environmental monitoring market and is driven by the European Green Deal and Zero Pollution Action Plan. The market operates within a framework of directives governing air quality, water purity, industrial emissions, and chemical safety, all of which require verified monitoring data for compliance demonstration. The national environmental agencies across the continent coordinate via the European Environmental Agency, creating a standardized approach to monitor the methodology and data reporting. Industrial facilities operating under the Industrial Emissions Directive must install and maintain continuous monitoring systems, while urban areas face specific obligations related to ambient air quality standards. Further, the market is characterized by both harmonized technical requirements and national variations in procurement and enforcement intensity.

The environmental monitoring market in Germany is supported by the strict environmental regulations, national air quality surveillance systems, and the continuous investment in pollution control infrastructure. The German Environment Agency coordinates nationwide environmental monitoring programs that track air pollutants, water quality, and environmental indicators used for regulatory enforcement and policy planning. According to the Unweltbundesamt August 2025 report, Germany operates over 400 air quality monitoring stations that measure pollutants. Moreover, the NLM study in January 2025 depicts that the monitoring results indicated that nitrogen dioxide annual average concentrations exceeded the EU limit value of 40 µg/m³ at several traffic-related monitoring sites, highlighting the need for continued monitoring and pollution mitigation measures. These data show a positive growth demand in the German environmental monitoring market.

The air quality surveillance programs, water quality regulations, and government investments in environmental protection are driving the environmental monitoring market in the UK. According to the Department for Environment, Food & Rural Affairs, September 2023 data, the AURN network operates more than 300 monitoring stations across the country, measuring pollutants with national air quality objectives. Moreover, the Government of the UK's April 2022 data depicts that the government announced a USD 6.6 billion investment in flood and coastal defense programs, which include environmental monitoring activities such as river monitoring, water quality assessments, and ecosystem management. These initiatives require continuous deployment of monitoring sensors supporting demand for environmental monitoring technologies in the UK.

Key Environmental Monitoring Market Players:

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- Agilent Technologies, Inc. (U.S.)

- PerkinElmer, Inc. (U.S.)

- Teledyne Technologies Incorporated (U.S.)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Merck KGaA (Germany)

- Siemens AG (Germany)

- Shimadzu Corporation (Japan)

- Horiba, Ltd. (Japan)

- Yokogawa Electric Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- ABB Ltd. (Switzerland)

- Spectris plc (UK)

- EcoTech Environmental Monitoring (Australia)

- ENVEA (France)

- APA Group (Australia)

- Veeva Systems (U.S.)

- PAI Partners (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Thermo Fisher Scientific Inc. is a leading player in the environmental monitoring market by providing comprehensive end-to-end solutions for air, water, and soil analysis. The company has advanced the market via the integration of its mass spectrometry and chromatography technologies with the automated data management software. In 2024, the company has made a revenue of USD 42.88 billion.

- Danaher Corporation has transformed the environmental monitoring market by leveraging its powerful Danaher Business System to drive continuous innovation in water quality and analysis. The corporation has advanced the sector via its operating companies by integrating smart connected sector into municipal and industrial water systems. In 2024, the company has made a total sale of USD 23,875.

- Agile Technologies Inc has made significant strides in the environmental monitoring market by focusing on the accuracy and reliability of laboratory testing for complex environmental contaminants. The company has advanced the field by introducing high-efficiency GC/MS and LC/MS systems designed specifically for environmental laboratories.

- PerkinElmer Inc has advanced the environmental monitoring market by pioneering solutions that address the global challenges related to food safety and industrial emissions. The company has made significant advancements by integrating its atomic spectroscopy and chromatography technologies into user-friendly platforms for detecting heavy metals and organic pollutants.

- Teledyne Technologies Incorporated has propelled the environmental monitoring market forward by specializing in advanced instrumentation for air quality emissions monitoring and oceanographic research. The company has advanced the market via its innovative gas analyzers and monitoring systems that utilize technologies such as cavity ring-down spectroscopy.

Here is a list of key players operating in the global environmental monitoring market:

The global environmental monitoring market is highly competitive and fragmented, and is defined by the presence of established multinational corporations and specialized regional players. The key strategic initiatives among these leaders include a strong focus on technological innovation, mainly the integration of IoT, AI, and advanced sensors for the real time data analytics and predictive monitoring. Moreover, the companies are actively pursuing mergers and acquisitions to expand their portfolios and geographic reach. For example, in May 2024, ENVEA announced the acquisition of the APAQ Group. Further, there is a significant push towards developing portable and user-friendly monitoring devices to cater to the growing demand from the various industries for regulatory compliance and workplace safety.

Corporate Landscape of the Environmental Monitoring Market:

Recent Developments

- In January 2026, Veeva Systems announced a new environmental monitoring solution to advance quality control for manufacturing operations. Veeva Environmental Monitoring, a cloud-native application unified with Veeva LIMS, will enable laboratories and manufacturing facilities to schedule, collect, and analyze environmental samples to ensure compliance with GMP and internal sterility standards.

- In September 2025, PAI Partners announced its agreement to acquire Orion, a leading Italian provider of environmental monitoring services, from Xenon Private Equity. The acquisition will be the first investment made through the PAI Mid-Market Fund II, PAI’s second fund dedicated to mid-market opportunities.

- In April 2025, ENVEA has launched a new, cutting-edge Optical Aerosol Spectrometer designed for real-time particulate matter (PM) monitoring, delivering ultra-precise data in any environment.

- Report ID: 8436

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.