Alarm Monitoring Market Outlook:

Alarm Monitoring Market size was valued at USD 65.4 billion in 2025 and is projected to reach USD 121.1 billion by the end of 2035, rising at a CAGR of 6.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of alarm monitoring is assessed at USD 69.2 billion.

The alarm monitoring market is expanding due to the increasing public and private investments in the security infrastructure and the growing demand for continuous surveillance across the commercial, industrial, and residential environments. The government-backed public safety initiatives and emergency communication systems have significantly contributed to the adoption of the centralized monitoring platforms. For example, the U.S. GAO September 2024 data shows that more than 240 million 911 calls are made annually, highlighting the scale of the emergency communication systems that rely on the monitored alarm and dispatch networks for response coordination. Additionally, the governments are emphasizing the importance of integrated monitoring systems in crime prevention strategies, noting that electronic alarm and surveillance integration has supported the reduction in property crimes in several monitored jurisdictions.

Moreover, the growth in the market is also influenced by the investments in the smart infrastructure, emergency preparedness, and disaster response networks. According to the U.S. Department of Homeland Security data in April 2024, there are 16 critical infrastructure sectors, including energy, transportation, healthcare, and communication, that require continuous monitoring systems to ensure operational security and rapid incident response. Similarly, the Integrated Public Alert and Warning System is expanded to deliver nationwide emergency alerts, demonstrating the rising reliance on centralized monitoring platforms for public safety coordination. Further, the false alarms represent a significant operational concern. As per the data from the NSPA June 2024 report, nearly 94% of the fire alarm responses are not associated with the actual fires, underscoring the need for advanced monitoring and verification technologies. These operational challenges have prompted organizations to deploy the monitored alarm systems integrated with the verification tools, remote diagnostics, and automated dispatch protocols.

Key Alarm Monitoring Market Insights Summary:

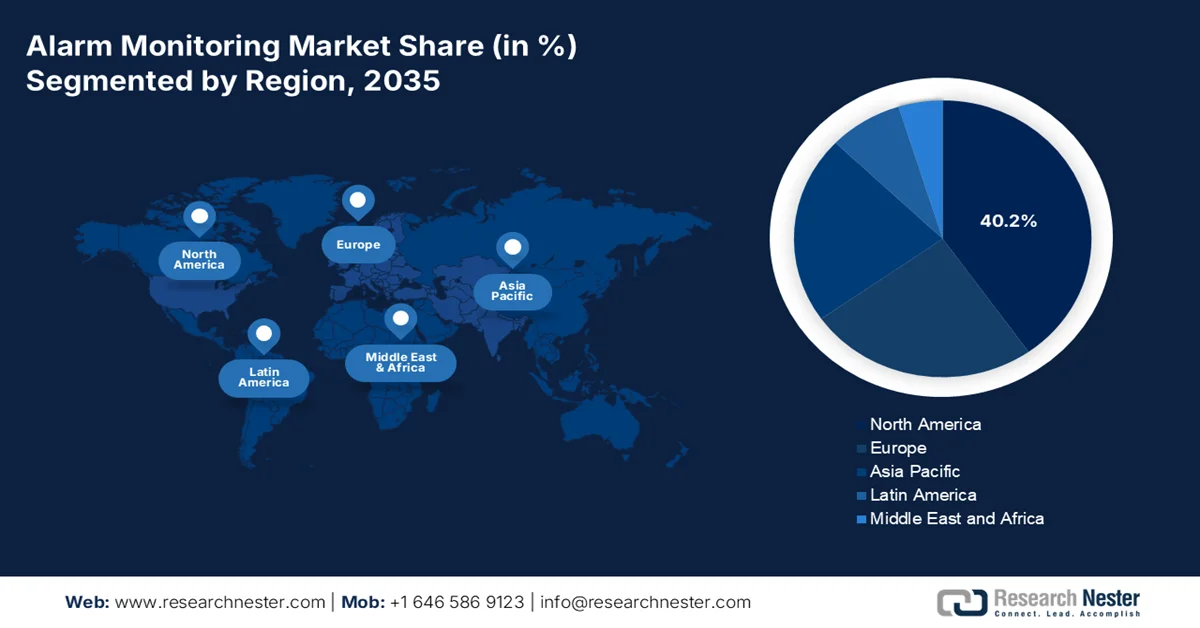

Regional Highlights:

- North America is forecast to secure a dominant 40.2% revenue share by 2035, underpinned by high security awareness, mature residential subscription models, and stringent commercial building regulations

- Asia Pacific is anticipated to register the fastest growth in the alarm monitoring market with a CAGR of 6.8% during 2026–2035, fueled by rapid urbanization and expanding government investments in smart city infrastructure

Segment Insights:

- In the alarm monitoring market, the wireless/cellular monitoring sub-segment under the communication segment is projected to account for a dominant 58.5% share by 2035, propelled by the need for always-on connectivity that cannot be physically severed by intruders and offers superior bandwidth for video verification

- The interactive services sub-segment within the service type segment is anticipated to secure the largest share by 2035, stimulated by rising consumer demand for real-time mobile access, convenience, and enhanced video-based verification capabilities

Key Growth Trends:

- Expansion of government critical infrastructure protection programs

- Government initiatives to reduce the property loss

Major Challenges:

- High initial infrastructure and technology investment

- Cybersecurity risks in connected alarm systems

Key Players: ADT Inc., Resideo Technologies, Inc., Johnson Controls International plc, Bosch Sicherheitssysteme GmbH, Honeywell International Inc., Securitas AB, Allegion plc, Assa Abloy AB, DSC Digital Security Controls Ltd., Napco Security Technologies, Inc., Secom Co., Ltd., Chubb Fire & Security Ltd., Telus Corporation, Vivint Smart Home, Inc., Axis Communications AB, Chubb Fire & Security Pty Ltd, Agilent Technologies Inc., Amthal Group Companies, Alarm.com, Everon, Hikvision.

Global Alarm Monitoring Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size:USD 65.4 billion

- 2026 Market Size: USD 69.2 billion

- Projected Market Size: USD 121.1 billion by 2035

- Growth Forecasts: 6.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries:United States, Germany, United Kingdom, Japan, China

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 12 March, 2026

Alarm Monitoring Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of government critical infrastructure protection programs: Government investments in the critical infrastructure protection are significantly shaping the demand for the alarm monitoring market across energy, transportation, healthcare, and other facilities. The federal spending on infrastructure security has increased via initiatives such as the Infrastructure Investment and Jobs Act, which allocated USD 1.2 trillion for national infrastructure modernization, including cybersecurity and physical security upgrades across public facilities, based on the PHMSA February 2023 data. These programs boost the agencies and operators to deploy the integrated alarm monitoring systems connected to emergency dispatch centers. For example, the transportation hubs and public utilities funded via federal security grants are required to deploy monitored alarm and surveillance infrastructure to ensure operational continuity and rapid response to incidents.

- Government initiatives to reduce the property loss: Government law enforcement agencies support the electronic alarm monitoring market for crime prevention strategies. According to the U.S. BJS June 2025 data, the total burglaries registered in 2023 were 1,746,980, with a majority targeting residential and small commercial properties. Moreover, many municipalities encourage verified alarm monitoring systems that enable faster law enforcement response and reduce property losses. Several cities in the U.S. and Europe have adopted policies that prioritize the police response to monitored and verified alarms to minimize false dispatches. These policies create incentives for businesses to implement professional alarm monitoring services rather than standalone alarms. Further, businesses are increasingly adopting monitored alarm systems as part of their risk management and compliance strategies.

Number of Burglary/Trespassing

|

Types of Crime |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Burglary/trespassing |

2,178,400 |

1,741,250 |

1,800,350 |

1,919,930 |

1,746,980 |

|

Burglary |

1,484,730 |

1,210,640 |

1,142,900 |

1,324,030 |

1,202,830 |

|

Trespassing |

693,670 |

530,610 |

657,440 ‡ |

595,910 |

544,140 |

Source: U.S. BJS June 2025

- Smart city and urban safety programs: Government-led smart city initiatives are expanding the urban security infrastructure and increasing demand for the integrated alarm monitoring market. the government led smart city challenge and related urban innovation programs promote cities to deploy connected infrastructure, including smart surveillance, emergency communication systems, and monitored security networks. Further, many governments in Europe and Asia are funding smart urban infrastructure to improve safety, transportation efficiency, and emergency response coordination. Smart city programs integrated surveillance cameras, environmental sensors, and alarm systems into the centralized monitoring platforms operated by the municipal authorities. These platforms enable real-time detection of incidents such as fires, intrusions, or infrastructure failures.

Challenges

- High initial infrastructure and technology investment: Entering the alarm monitoring market requires a heavy investment in the monitoring centers, cloud infrastructure, AI analytics, and cybersecurity systems. Companies must build redundant data centers, 24/7 monitoring operations, and reliable communication networks. Top players invest heavily in the digital transformation and monitoring infrastructure to support the smart security services. Though the market is expected to grow, the infrastructure cost remains a key barrier for new entrants. Smaller suppliers struggle to compete with the established players that already operate the large monitoring networks and nationwide service coverage.

- Cybersecurity risks in connected alarm systems: Modern alarm monitoring relies heavily on IoT devices, cloud platforms, and remote connectivity, making systems vulnerable to cyberattacks. Moreover, the security breaches could allow hackers to disable the alarms or access user data. For instance, vulnerabilities discovered in Ring home security cameras raised concerns about smart security device hacking and privacy risks. Moreover, the breach cost is exceeding billions, highlighting the financial risk for companies managing sensitive security infrastructure. New players in the alarm monitoring market must invest heavily in encryption, secure device authentication, and threat monitoring.

Alarm Monitoring Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.4% |

|

Base Year Market Size (2025) |

USD 65.4 billion |

|

Forecast Year Market Size (2035) |

USD 121.1 billion |

|

Regional Scope |

|

Alarm Monitoring Market Segmentation:

Communication Segment Analysis

Under the communication segment, the wireless/cellular monitoring sub-segment is leading and is expected to hold the largest share value of 58.5% by the end of 2035. The segment is driven by the need for always-on connectivity that cannot be physically severed by intruders and offers superior bandwidth for video verification. The cellular paths ensure that alarm signals reach central stations instantly, even during power outages or internet disruptions, providing the highest level of security assurance. The expansion of 5G and LTE-M networks designed for IoT devices has further stimulated this adoption, enabling a longer battery life for the sensors and more reliable data transmission. According to a report from the OEC Commons, September 2023 data, nearly 16.1% of the burglaries occurred during daylight hours, highlighting the critical need for remotely monitored, reliable cellular systems that can alert homeowners instantly, regardless of time or location.

Service Type Segment Analysis

In the service type segment, the interactive services sub-segment is expected to hold the largest share value in the alarm monitoring market by the end of 2035. Unlike the traditional services that only notify a call center, interactive services empower users with real-time mobile access to their security systems. This includes live video streaming, remote locking and unlocking, and smart home automation integration such as adjusting thermostats or lights based on security events. The primary driver is consumer demand for convenience and control, coupled with the need for video verification to reduce false dispatches. By allowing users and monitoring centers to visually confirm, alarm response accuracy improves dramatically. As per the NLM December 2023 study, by implementing the intelligent escalation algorithms and delaying non-critical alerts in the clinical interventions, 68% of the alarm notification is reduced, validating efficiency and growing dominance of this service model.

Component Segment Analysis

Hardware sub segment is leading in the component segment in the alarm monitoring market. The segment is driven by the physical devices that are essential for detection and deterrence, including control panels, motion sensors, glass break detectors, and surveillance cameras. The sustained dominance of hardware is driven by the continuous technological advancements, such as the development of high definition cameras with the edge based AI analytics and long life sensors batteries. As new construction projects and retrofits demand advanced security infrastructures, the volume of installed devices continues to climb. Further, the push for smart cities and commercial building automation requires dense networks of physical sensors to collect data. Moreover, the adoption of intrusion detection hardware in critical infrastructure sectors underscores the hardware's vital role in national security resilience.

Our in-depth analysis of the alarm monitoring market includes the following segments:

|

Segment |

Subsegments |

|

System Type |

|

|

Communication |

|

|

Service Type |

|

|

End user |

|

|

Component |

|

|

Vertical |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Alarm Monitoring Market - Regional Analysis

North America Market Insights

North America is dominating and is expected to hold the regional revenue share of 40.2% by the end of 2035 in the alarm monitoring market. The market is driven by high security awareness, mature residential subscription models, and stringent commercial building regulations. The market is defined by a shift from traditional intrusion detection to interactive services integrating video verification and home automation. The key drivers include the municipal false alarm reduction ordinances directing the verified response, which pushes the adoption of advanced systems. The aging population fuels the demand for medical alert systems integrated with the monitoring platforms. Moreover, the commercial growth sector is underpinned by the regulatory compliance requirements from agencies such as the OSHA and insurance mandates. further the U.S. accounts for the vast majority of regional revenue, supported by a dense network of central monitoring stations and high broadband penetration.

The federal investments in public safety infrastructure emergency response modernization and building safety compliance across the commercial and public facilities are influencing the alarm monitoring market in U.S. According to the NFPA November 2025 data fire departments responded to about 1.38 million fire incidents in 2024 with a significant share occurring in the residential and commercial structures reinforcing demand for the monitored fire and safety alarm systems in buildings that require rapid response coordination. On the other hand, the total motor vehicle theft in 2023 was 808,830, as per the BJS November 2025 report, requiring alarm monitoring for the vehicles. Moreover, the U.S. Department of Homeland Security's February 2021 report reported USD 1.87 billion allocated through preparedness grant programs to strengthen security and emergency response capabilities for critical infrastructure and public facilities, supporting wider deployment of integrated monitoring and alert systems.

The increasing property crime surveillance needs and rising fire incident management across residential and commercial infrastructure are driving the alarm monitoring market in Canada. According to Statistics Canada, February 2023 data, property crimes account for about 18% of reported criminal incidents, creating sustained demand for intrusion detection and monitored security systems. Moreover, the Government of Canada's August 2022 data reported that although the Non-violent Crime Severity Index declined by 3%, largely due to a 10% decrease in breaking and a 4% drop in theft under USD 5,000, businesses continue to invest in monitored alarm systems to prevent financial losses and improve security compliance. On the other hand, the Government of Canada's July 2023 data depicts that the fire incident reporting program shows that fire departments across seven reporting jurisdictions responded to more than 39,000 fires in 2021, marking the second consecutive annual increase and therefore enabling a strong market growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to grow at a CAGR of 6.8%. The alarm monitoring market in APAC is driven by the rapid urbanization and significant government investments in the smart city infrastructure. The region’s diversity encompasses mature markets such as Japan, with advanced aging in place technologies and high-growth markets such as China and India, where rising crime awareness and insurance requirements fuel the adoption. A key regional trend is the integration of alarm monitoring with the national public safety networks, mainly in China and India. Moreover, the government spending on critical infrastructure protection, including transportation hubs and power grids, creates sustained demand for commercial monitoring services.

The increasing urban security requirements, rising property-related crime incidents and government initiatives to modernize public safety infrastructure are driving the growth of the alarm monitoring market in India. According to the Ministry of Home Affairs 2022-2023, India recorded 36,63,360 cognizable crimes, with theft and burglary forming a significant share of property-related offences, encouraging households, retail establishments, and commercial facilities to install monitored intrusion alarm systems. Moreover, strengthening the urban surveillance and emergency response infrastructure via the Safe City Programme supports the deployment of integrated command and control centers, surveillance networks, and alarm-based alert systems across major cities. These data show a positive uplift in the alarm monitoring market growth.

The government investments in public security infrastructure, smart city development, and increasing surveillance of residential and commercial facilities are driving the alarm monitoring market in China. According to the UNDP 2023 report, the country’s urbanization rate reached about 66.2% in 2023, reflecting the rapid expansion of urban residential complexes commercial buildings, and industrial facilities that require integrated security and alarm monitoring systems. Further, the public security expenditure is also supporting the deployment of monitoring technologies, emergency response systems, and urban security networks across cities and transportation hubs. These government-led safety initiatives and expanding urban infrastructure are encouraging organizations and property developers to deploy integrated alarm monitoring platforms connected to centralized command and emergency response systems across major cities in China.

Europe Market Insights

The alarm monitoring market in Europe is expanding rapidly and is defined by the stringent regulatory frameworks, increasing urbanization, and a strong focus on integrating security with healthcare services. The region benefits from harmonized standards under the European Committee for Standardization, which facilitate cross border equipment certificates and service interoperability. The key drivers include the European Commission’s Security Union Strategy, which promotes critical infrastructure protection and public space security. The aging population fuels the demand for medical alert systems integrated with the monitoring platforms. Data protection regulations shape the system's design, requiring manufacturers to implement privacy by design features. Moreover, the municipalities are adopting verified response policies and driving the demand for video-verified alarm systems.

The strong regulatory requirements for building safety, increasing property crime surveillance, and government investment in emergency response infrastructure are shaping the alarm monitoring market in Germany. According to the OSAC February 2025 data, Germany recorded over 1.9 million theft-related offences, including burglary and commercial property theft, prompting businesses and residential property owners to deploy monitored intrusion alarm systems to reduce financial losses and improve security compliance. Moreover, the fire services require rapid detection and alarm notification systems to support emergency response. These government-led safety and disaster management initiatives encourage integration of building alarm systems with centralized monitoring platforms, supporting steady adoption of professional alarm monitoring services across commercial facilities, industrial plants, and public infrastructure in Germany.

The alarm monitoring market in the UK is driven by property crime prevention initiatives, fire safety regulations, and government investments in emergency communication systems. According to the UK Office for National Statistics, September 2024 data, shoplifting offences increased by 23%, boosting the adoption of monitored intrusion alarm systems among households and businesses. Moreover, fire safety compliance is another important factor influencing the market. The Government of the UK's March 2025 data reports that fire and rescue services attended over 142,494 fire-related incidents, leading to strict enforcement of fire detection and alarm system requirements in commercial buildings, multi-residential housing, and public facilities. These data show that the integration of building alarm systems is supporting the adoption of professional alarm monitoring services throughout the UK.

Crime Statistics in England and Wales

|

Crime Category |

Year Ending September 2023 |

Year Ending September 2024 |

Change |

|

Offences involving firearms |

6,499 |

5,372 |

↓ 17% |

|

Robbery offences |

78,865 |

82,347 |

↑ 4% |

|

Shoplifting offences |

402,220 |

492,914 |

↑ 23% |

Source: UK Office for National Statistics, September 2024

Key Alarm Monitoring Market Players:

- ADT Inc. (U.S.)

- Resideo Technologies, Inc. (U.S.)

- Johnson Controls International plc (Ireland)

- Bosch Sicherheitssysteme GmbH (Germany)

- Honeywell International Inc. (U.S.)

- Securitas AB (Sweden)

- Allegion plc (Ireland)

- Assa Abloy AB (Sweden)

- DSC (Digital Security Controls) Ltd. (Canada)

- Napco Security Technologies, Inc. (U.S.)

- Secom Co., Ltd. (Japan)

- Chubb Fire & Security Ltd. (UK)

- Telus Corporation (Canada)

- Vivint Smart Home, Inc. (U.S.)

- Axis Communications AB (Sweden)

- Chubb Fire & Security Pty Ltd (Australia)

- Agilent Technologies Inc. (U.S.)

- Amthal Group Companies (UK)

- Alarm.com (U.S.)

- Everon (U.S.)

- Hikvision (China)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ADT Inc holds a dominant position in the alarm monitoring market and has transitioned from traditional intrusion detection to a comprehensive ecosystem of smart home protection. By integrating the professional monitoring with the mobile app, which controls video surveillance and smart automation, the company ensures continuous protection for residential and business customers. In 2024, the company made a revenue of USD 4,293,477 in monitoring and related service segments.

- Resideo Technologies Inc is a key player in the global alarm monitoring market, primarily known for its expansive portfolio of security and life safety products under the brands such as First Alert and ADEMCO. As a major manufacturer of hardware, such as control panels and sensors, their influence extends deeply into the monitoring ecosystems via their Resideo Pro platform. In 2024, the company made a revenue of USD 6,761, based on the company’s annual report.

- Johnson Controls International plc is a global powerhouse in the building solutions sector with a formidable presence in the alarm monitoring market via its open platform technology. The company manufacturers industry leading brands such as DSC and Bentel, which are widely used in intrusion detection systems worldwide. Their strategic advancements focus on integrating security with broader building intelligence.

- Bosch Sicherheitssysteme GmbH, a division of the Bosch Group, is renowned for engineering precision and innovation within the global alarm monitoring market. They specialize in intelligent intrusion detection systems, fire alarms, and evacuation solutions that prioritize the reliability and reduction of nuisance alarms. A significant advancement from Bosch is their integration of remote monitoring via mobile applications and cloud platforms.

- Honeywell International Inc is a titan in the industrial and safety sectors, wielding massive influence over the commercial and residential alarm monitoring market. They provide extensive hardware and software solutions that cover everything from fire alarms and intrusion detection to mass notification systems. Their strategic initiatives involve leveraging the IoT to transform traditional alarm systems into connected and data-driven assets.

Here is a list of key players operating in the global alarm monitoring market:

The global alarm monitoring market is defined by intense competition and is driven by the convergence of traditional security services with the smart home and IoT technologies. The key players are shifting from offering simple intrusion detection to providing comprehensive interactive solutions. For example, in September 2025, Agilent Technologies Inc. announced the launch of its new Insight Series Alarm Resolution Systems, designed to enhance the safety and streamline operations at airport security checkpoints worldwide. The major initiatives include integrating artificial intelligence for advanced video analytics and false alarm reduction, expanding into home automation and energy management, and developing robust mobile applications for remote control. Consolidation remains a key trend with the large players acquiring the regional specialists to expand their geographic footprint and service portfolios. Companies are also heavily investing in cybersecurity measures to protect user data and system integrity, differentiating themselves in a crowded marketplace.

Corporate Landscape of the Alarm Monitoring Market:

Recent Developments

- In February 2026, Amthal Group Companies unveiled a new wireless intruder alarm system named AirShield, developed in collaboration with Dahua Technology. This addition broadens Amthal’s portfolio of professionally installed security solutions specifically aimed at residential properties.

- In December 2025, Alarm.com and Everon, LLC, a leading security integrator and premier provider of commercial security, video, fire, and life safety solutions, announced a strategic partnership to deliver a unified console for Everon customers to manage integrated intrusion protection, access control, remote video monitoring, and business management solutions.

- In March 2024, Hikvision launched the AX HOME series wireless alarm system designed to meet the needs of homeowners. The AX HOME Series builds on Hikvision's commitment to deliver cutting-edge, reliable alarm systems that are both cost-effective and user-friendly.

- Report ID: 8437

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.