Engineering Plastics Market Outlook:

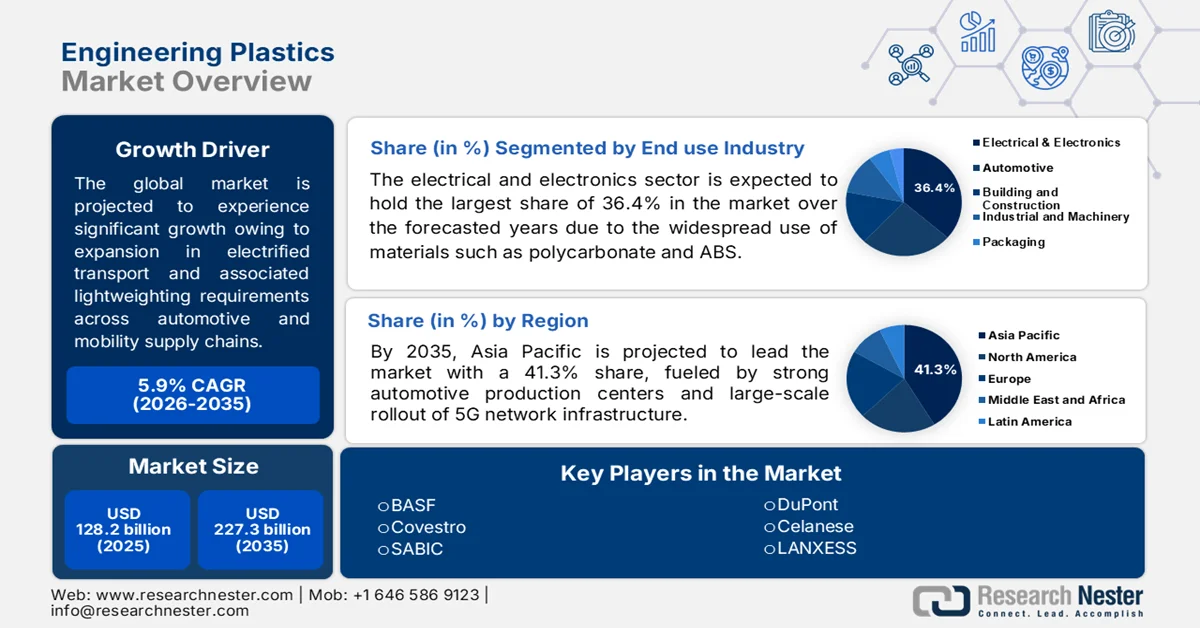

Engineering Plastics Market size was valued at USD 128.2 billion in 2025 and is expected to reach USD 227.3 billion by 2035. Growing at a CAGR of 5.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of engineering plastics is evaluated at USD 135.7 billion.

The global engineering plastics market is projected for solid growth in the next decade owing to the sustained expansion in terms of electrified transport and associated lightweighting requirements across automotive and mobility supply chains. Government energy agencies across different countries consistently report rising penetration of electric vehicles, which structurally increases demand for polymer systems to be used in battery housings, connectors, insulation, and structural components. In April 2024, BASF reported that it supplied high-performance engineering plastics, i.e., Ultramid B3EG7 and Ultramid A3EG6 EQ, for RML Group’s immersion-cooled 800V hybrid hypercar battery system, where they are used in the housing and cell holders. These materials provide high mechanical strength, crash resistance, and excellent thermal stability, which makes them suitable for extreme automotive battery conditions.

Furthermore, the market reflects rising interest in sustainable and recyclable material solutions, which encourages innovation in bio-based and circular engineering plastics. Also, rapid industrialization, expanding manufacturing activities, and continuous technological developments are expected to create new growth opportunities, positioning the market for sustained long-term expansion. In February 2023, Repsol announced that it is expanding its circular economy strategy with a total of USD 28.5 million investment in its Puertollano Industrial Complex in Spain, where it is adding a new recycled plastics production line under its Reciclex range. The new unit will have a capacity of 25,000 tons per year, nearly doubling the site’s current recycled plastics output, and it will process HDPE and LDPE plastics with recycled content ranging from 10% to 80%.

Global Polycarbonate Export Rankings by Country in 2024: Shipment Value and Volume

|

Exporter |

Trade Value (1000 USD) |

Quantity (Kg) |

|

Korea, Rep. |

1,764,897.54 |

692,931,000 |

|

China |

1,112,844.45 |

487,064,000 |

|

U.S. |

1,012,036.97 |

325,506,000 |

|

Thailand |

872,828.54 |

425,949,000 |

|

Other Asia, nes |

572,339.41 |

244,764,000 |

|

Netherlands |

557,662.97 |

164,088,000 |

|

Japan |

539,640.26 |

112,198,000 |

|

Europe |

416,366.16 |

126,266,000 |

Source: WITS

Key Engineering Plastics Market Insights Summary:

Regional Highlights:

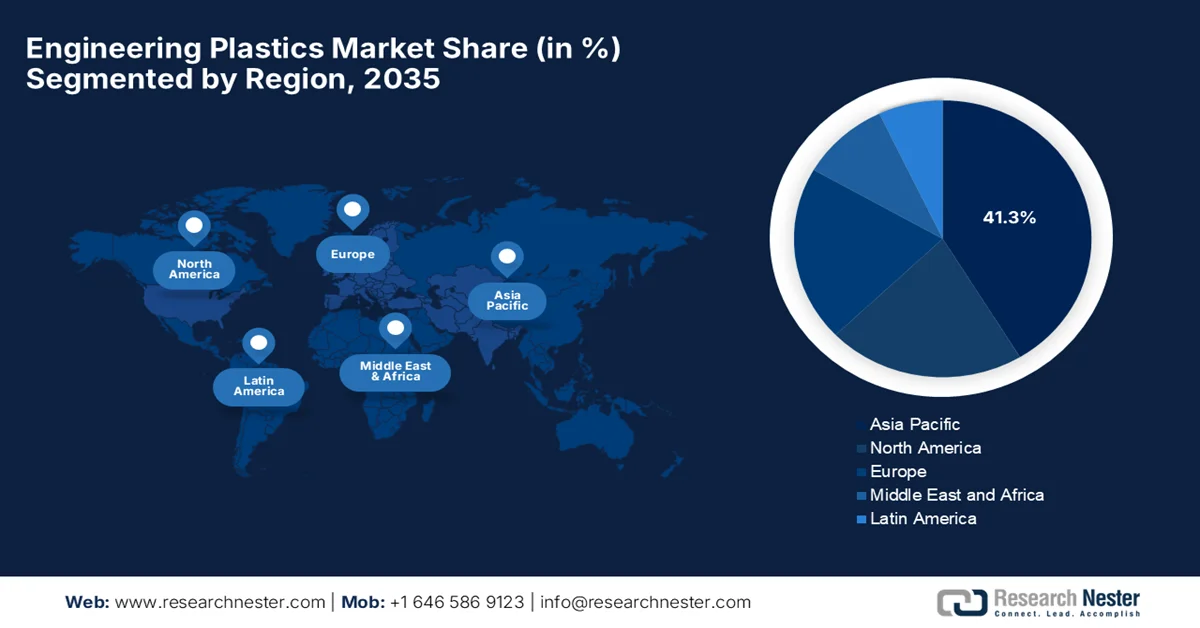

- The engineering plastics market in Asia Pacific is anticipated to command 41.3% share by 2035, bolstered by massive automotive manufacturing hubs, expanding 5G telecommunication networks, semiconductor packaging, and consumer electronics

- North America is poised to register considerable growth during 2026-2035, fueled by the structural shift toward domestic manufacturing and advanced technology sectors

- The engineering plastics market in the U.S. accounts for 81.5% of the share in North America, which is driven by the strong automotive, electrical & electronics, and industrial manufacturing demand in the country

Segment Insights:

- The electrical and electronics segment is projected to account for 36.4% share by 2035 in the engineering plastics market, reinforced by the widespread use of polycarbonate and ABS for their excellent insulation and flame resistance

- The styrene copolymers segment is expected to secure a significant revenue share during 2026-2035, propelled by its high toughness, excellent moldability, and superior surface finish

Key Growth Trends:

- Automotive lightweighting and EV adoption

- Surging medical device demand

Major Challenges:

- Volatility in raw material prices

- Environmental regulations and sustainability pressure

Key Players: BASF, Covestro, SABIC, DuPont, Celanese, LANXESS, Mitsubishi Chemical Group, Toray Industries, Solvay, Polyplastics Co., Ltd., Asahi Kasei, LG Chem, EMS-Chemie.

Global Engineering Plastics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 128.2 billion

- 2026 Market Size: USD 135.7 billion

- Projected Market Size: USD 227.3 billion by 2035

- Growth Forecasts: 5.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.3% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Thailand, Indonesia, Malaysia

Last updated on : 7 July, 2026

Engineering Plastics Market - Growth Drivers and Challenges

Growth Drivers

- Automotive lightweighting and EV adoption: There has been an accelerating transition toward electric vehicles, which drives market growth as automakers are looking to reduce vehicle weight to extend battery range. Also, these engineering plastics efficiently replace heavy metal components in powertrains, battery enclosures, and structural parts. In this context, the International Energy Agency in 2026 revealed that electric car sales surpassed almost 20 million globally in 2025, growing about 20% year-on-year, and reached a substantial 25% share of total new car sales, which is one in four new cars sold worldwide was electric. Battery electric vehicles dominated this growth, accounting for around 65% of total EV sales. China was the largest market, contributing more than half of global EV sales growth and more than 13 million units, whereas Europe saw strong expansion with 30%, and the U.S. was stable with just under 10% EV share. Overall, EVs currently represent about 5% of the global car stock and thus heighten demand for engineering plastics.

- Surging medical device demand: The healthcare sector is mostly dependent on certain engineered plastics to manufacture advanced devices, surgical instruments, and diagnostic equipment. These specialized polymers provide the required rates of biocompatibility, chemical resistance, and the ability to withstand rigorous sterilization processes. In this context, in August 2023, DuPont announced the acquisition of Spectrum Plastics Group with the main goal of strengthening its position in advanced healthcare and medical device components. This acquisition expands DuPont’s capabilities in high-growth medical applications such as structural heart, electrophysiology, surgical robotics, and cardiovascular devices, thus elevating the growth potential of the market.

Challenges

- Volatility in raw material prices: One of the main burdens for the market is the volatility in terms of raw materials, especially petrochemical feedstocks such as naphtha, benzene, and propylene. Most of the engineering plastics are derived from fossil-based sources, due to which fluctuations in crude oil prices directly impact production costs as well as profit margins. Manufacturers also face struggles in order to maintain stable pricing strategies, especially in long-term supply contracts with automotive and electronics OEMs, and this unpredictability also affects investment planning and capacity expansion decisions. In addition, any type of sudden spikes in input costs can reduce competitiveness against alternative materials such as metals and composites, especially in cost-sensitive applications. Therefore, this causes limitations to large-scale adoption, thereby making raw material dependency a major structural challenge.

- Environmental regulations and sustainability pressure: This is yet another major burden for the market due to stringent environmental regulations and sustainability expectations from governments, consumers, and end use industries. Some policies target plastic waste reduction, recycling mandates, and carbon emission limits, compelling manufacturers to redesign materials and production processes. These engineered plastics possess limited recyclability due to complex polymer structures and additives. On the other hand, compliance with continuously evolving regulations such as extended producer responsibility schemes increases operational complexity and cost. Companies are making heavy investments in recyclable, bio-based, and circular economy solutions, but scaling these technologies is challenging.

Engineering Plastics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

5.9% |

|

Base Year Market Size (2025) |

USD 128.2 billion |

|

Forecast Year Market Size (2035) |

USD 227.3 billion |

|

Regional Scope |

|

Engineering Plastics Market Segmentation:

End use Industry Segment Analysis

Under the end use industry segment, the electrical and electronics sector is expected to hold the largest share of 36.4% in the engineering plastics market over the forecasted years. The segment’s dominating position is efficiently driven by the widespread use of materials such as polycarbonate and ABS due to their excellent insulation and flame resistance. Growth is further supported by device miniaturization, expanding 5G infrastructure, and increasing adoption of smart technologies, all of which require compact and high-performance materials. For instance, in October 2023, VVDN Technologies announced the inauguration of a new SMT (surface-mount technology) production line in India to manufacture 4G and 5G connectivity modules and data cards for Telit Cinterion. This new SMT line strengthens local Design and Make in India capabilities, enabling end-to-end production of advanced IoT and telecom hardware and thus rising demand for engineering plastics.

Type Segment Analysis

The styrene copolymers segment is projected to lead the engineering plastics market, capturing a significant revenue share during the discussed timeframe. This segment’s growth is attributed to its high toughness, excellent moldability, and superior surface finish. They are extensively used in consumer electronics, automotive interiors, and household appliances due to their cost efficiency and versatility. In June 2024, Trinseo announced the launch of new ABS and SAN resins under its MAGNUM™ ECO+, MAGNUM™ CR, and TYRIL™ CR brands that incorporate up to 60% chemically recycled styrene using a mass-balance approach. The company also notes that these materials are designed as drop-in replacements, which means they can be processed using existing equipment and tooling without any changes in manufacturing conditions.

Parameter Segment Analysis

Based on the parameter, the high-performance segment is anticipated to showcase lucrative growth opportunities in the engineering plastics market over the forecasted years. The segment’s growth is largely driven by increasing demand from extreme operating environments where standard plastics fail, particularly in terms of aerospace, oil & gas, and high-end industrial machinery. Strong growth in electrification systems, especially high-voltage EV components and power electronics, is also expanding usage. In addition, stricter safety, fire-resistance, and regulatory compliance requirements are accelerating the adoption of advanced high-performance engineering plastics. Furthermore, rapid innovation in polymer chemistry and the rising substitution of metals in critical load-bearing applications deliberately support segment expansion.

Our in-depth analysis of the engineering plastics market includes the following segments:

|

Segment |

Subsegments |

|

End use Industry |

|

|

Type |

|

|

Parameter |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Engineering Plastics Market - Regional Analysis

APAC Market Insights

Asia Pacific engineering plastics market is anticipated to garner the highest share of 41.3% during the forecast period. The region’s upliftment is mainly attributable to massive automotive manufacturing hubs, expansions in regional 5G telecommunication networks, semiconductor packaging, and consumer electronics. In addition, local investments in terms of massive local investments in chemical production facilities, such as mega-scale specialty resin complexes, and shifting supply networks toward intra-ASEAN sourcing are strengthening domestic feedstock availability. Based on government data published in September 2023, GlobalFoundries has opened a USD 4 billion semiconductor fabrication plant expansion in Singapore, adding significant new manufacturing capacity. The new 23,000 sqm facility will increase GlobalFoundries’ Singapore output by about 450,000 additional 300mm wafers per year. Hence, such instances efficiently boost demand for engineering plastics in the region.

The country’s undisputed global dominance in electric vehicle production is responsibly positioning China's market for sustained growth. On the supply side, major domestic chemical giants are building mega-scale integrated production complexes that shift away from their reliance on foreign resin imports toward domestic self-reliance in specialty compounding. For instance, in November 2023, BASF and Sinopec announced the inauguration of an expanded Verbund chemical production site in Nanjing, China, through their joint venture BASF-YPC to meet rising demand from China’s industrial sectors. The expansion includes new downstream plants and a tert-butyl acrylate unit, which is the first use of this advanced technology outside Germany, making it suitable for standard market growth.

In India, the market is being thoroughly supported by the government’s intensifying focus on domestic manufacturing with substantial funding grants. Simultaneously, the country’s expanding electronics manufacturing sector and widespread telecommunications infrastructure rollouts are creating strong demand for flame-retardant, high-temperature resins used in connectors and appliance components. As stated by the Press Information Bureau (PIB) in April 2025, India is strengthening its polymer manufacturing ecosystem through the Government’s Plastic Parks Scheme, under which 10 plastic parks have been approved across multiple states with central assistance of up to 50% of project cost. Hence, the initiative supports innovation, domestic manufacturing capacity, and the long-term growth of the engineering plastics value chain in the upcoming years.

India Acrylonitrile-Butadiene-Styrene (ABS) Copolymer Exports by Country in 2023 - Trade Value and Quantity

|

Partner Country |

Trade Value (1000 USD) |

Quantity (Kg) |

|

World |

990.52 |

379,979 |

|

UAE |

234.92 |

100,418 |

|

Mexico |

166.15 |

55,200 |

|

China |

148.53 |

69,323 |

|

U.S. |

93.82 |

10,484 |

|

Nepal |

92.97 |

48,379 |

|

Italy |

65.07 |

11,235 |

|

Bangladesh |

35.11 |

30,075 |

|

Argentina |

26.02 |

13,200 |

Source: WITS

India Polycarbonate Exports by Country in 2023 - Trade Value and Quantity Breakdown

|

Partner Country |

Trade Value (1000 USD) |

Quantity (Kg) |

|

World |

5,464.48 |

2,863,140 |

|

Korea, Rep. |

2,027.94 |

1,223,250 |

|

Italy |

793.76 |

530,735 |

|

Nepal |

292.14 |

165,550 |

|

China |

275.48 |

137,209 |

|

Belgium |

273.88 |

132,506 |

|

Other Asia, nes |

272.03 |

210,056 |

|

France |

224.63 |

32,431 |

|

Sri Lanka |

164.33 |

57,650 |

|

UAE |

121.92 |

36,546 |

|

Germany |

119.26 |

13,989 |

Source: WITS

North America Market Insights

The North America engineering plastics market is projected to witness considerable growth from 2026 to 2035. The region’s market is largely driven by a structural shift toward domestic manufacturing and advanced technology sectors. Also, the market benefits from a world-leading medical device industry, and expanding aerospace manufacturing sectors require highly specialized, biocompatible, and ultra-high-strength resins. In February 2026, Celanese Corporation inaugurated an expanded Michigan Technology Center in Troy, Michigan, to accelerate innovation in engineered materials and strengthen customer collaboration across North America. This expansion includes relocating the Santoprene® TPV piloting operation from Houston to create a centralized hub for extrusion, foaming technologies, and advanced materials development.

The reshoring of advanced manufacturing and strict federal clean energy initiatives are the main factors powering the market in the U.S. The domestic corporations focus on carbon-neutrality targets, due to which the market is witnessing surging investment in advanced chemical recycling infrastructure to scale the domestic supply of high-purity resins. As of the May 2026 data from the U.S. Department of Energy, advanced recycling is considered to be a key technology to complement mechanical recycling by converting difficult-to-recycle plastics into virgin-equivalent feedstocks. It also mentioned that these technologies support the recycling of engineering plastics, including polyamides, and help reduce landfill waste, conserve raw materials, and advance circular economy goals. Thus, such initiatives are supporting the expansion of domestic supplies of high-purity resins and thereby reducing reliance on virgin raw materials.

Canada market is structured around a strong industrial pivot toward advanced manufacturing, clean technology, and strict federal environmental mandates. Simultaneously on the supply side, the country leverages its mature chemical infrastructure and abundant natural gas feedstocks to support domestic compounding operations. For instance, in March 2024, NOVA Chemicals announced the launch of the Centre of Excellence for Plastics Circularity in Canada in order to accelerate innovation in sustainable plastics through collaboration among industry, academia, and government. This particular initiative is highly focused on advancing research in mechanical recycling, advanced recycling, and microplastics, while developing scalable technologies that support a circular plastics economy.

Europe Market Insights

The Europe engineering plastics market is growing at a significant rate, propelled mainly by the most stringent environmental mandates and a strong corporate encouragement toward circular economies. The region also benefits from highly advanced medical technology, aerospace, and precision industrial sectors, which sustain a constant demand for ultra-high-strength, bio-compatible, and flame-retardant resins. The European Commission deliberately promotes a circular economy to replace the linear take-make-dispose model with systems that reuse and recycle materials. The upcoming Circular Economy Act, by the end of 2026, will create a single EU market for secondary raw materials and increase access to high-quality recycled inputs, and it targets doubling the EU circularity rate from 12% to 24% by 2030. Also, with suitable policies, it collectively strengthens recycling, product sustainability, and material efficiency across industries.

The shift toward specialized high-performance resins and advanced mass-balance compounding to combat severe macroeconomic and energy cost pressures is driving the upliftment of Germany market. Meanwhile, the massive chemical sector has faced overall production headwinds and high natural gas costs, whereas domestic resin innovators such as BASF, Covestro, and LANXESS are pivoting toward absolute sustainability and technical differentiation. Climate Policy Database states that the Buildings Energy Act (GEG) regulates energy efficiency in buildings and the use of renewable energy in heating, replacing earlier energy and construction laws. Recent updates, which are from 2022 to 2024, tightened efficiency rules and introduced a 65% renewable energy requirement for new heating systems, thus elevating demand for engineering plastics.

The UK market is highly influenced by post-Brexit industrial incentives, localized tax pressures, and strict domestic sustainability shifts. The country’s market is witnessing sharp cost re-engineering by compounders who face an increased Plastic Packaging Tax rate and tightening restrictions on per- and polyfluoroalkyl substances. Based on government data published in January 2025, the Department for Environment, Food & Rural Affairs has announced a Deposit Return Scheme for plastic bottles and cans in England and Northern Ireland with a collective goal to reduce litter and improve recycling rates. From October 2027, consumers will pay a deposit when buying drinks and get it back when returning empty containers to collection points, thus making it suitable for bolstering the country’s market growth.

Key Engineering Plastics Market Players:

- BASF (Germany)

- Covestro (Germany)

- SABIC (Saudi Arabia)

- DuPont (U.S.)

- Celanese (U.S.)

- LANXESS (Germany)

- Mitsubishi Chemical Group (Japan)

- Toray Industries (Japan)

- Solvay (Belgium)

- Polyplastics Co., Ltd. (Japan)

- Asahi Kasei (Japan)

- LG Chem (South Korea)

- EMS-Chemie (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Covestro is a leading materials manufacturer, and it has a strong focus on high-performance polymer solutions, particularly polycarbonates under the Makrolon® brand. The company is a pivotal leader in engineering plastics, which are used in automotive, electronics, healthcare, and construction applications.

- SABIC is a major global player in engineering thermoplastics that offers a wide portfolio including LNP™ compounds, NORYL™ resins, and specialty polycarbonates. Besides, the company supplies high-performance materials to automotive, aerospace, electrical, and consumer goods industries.

- DuPont is a central player in this field, and it focuses on high-performance applications across different sectors. The company differentiates itself through deep material science expertise, strong application engineering support, and a legacy of innovation in high-performance polymers.

- Celanese is a leading engineered materials company that has a strong presence in engineering thermoplastics such as Hostaform® (POM) and Celanex® (PBT). In addition, the firm benefits from its strong compounding capabilities, application development expertise, and strategic acquisitions that have expanded its engineering materials portfolio.

Here is a list of key players operating in the global market:

The engineering plastics market represents a moderately consolidated landscape at the global level, which hosts a small group of multinational chemical companies dominating high-performance resin production. Competition in this field is primarily propelled by material innovation, heat and chemical resistance performance, and solutions which are suitable for automotive, electrical & electronics, and industrial applications. Large market pioneers maintain strong global supply networks along with polymer portfolios, whereas regional manufacturers compete in terms of specialized or cost-sensitive solutions. For instance, in February 2025, Sirmax Group and Autotech announced the expansion of their Palwal plant in India, thereby increasing annual capacity to 30,000 tons with four new extrusion lines, upgraded labs, and automated warehousing. Besides, this facility has been modernized to better serve the rising demand for high-performance thermoplastic and polypropylene-based compounds in both the domestic and international markets.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, BASF introduced Ultramid® A3XZC3 ESD, which is a carbon-fiber-reinforced, flame-retardant engineering plastic used in the backplate of MSA’s M1 self-contained breathing apparatus. This material combines high mechanical strength, impact resistance, and reduced surface resistivity.

- In October 2025, Mitsui Chemicals and Polyplastics entered into a marketing partnership under which Polyplastics will exclusively manage customer relations, business development, and technical support for Mitsui Chemicals’ ARLEN® and AURUM® engineering plastics. Under this collaboration, Mitsui Chemicals will continue to oversee R&D, manufacturing, logistics, and product supply.

- Report ID: 8653

- Published Date: Jul 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.