High Performance Plastics Market Outlook:

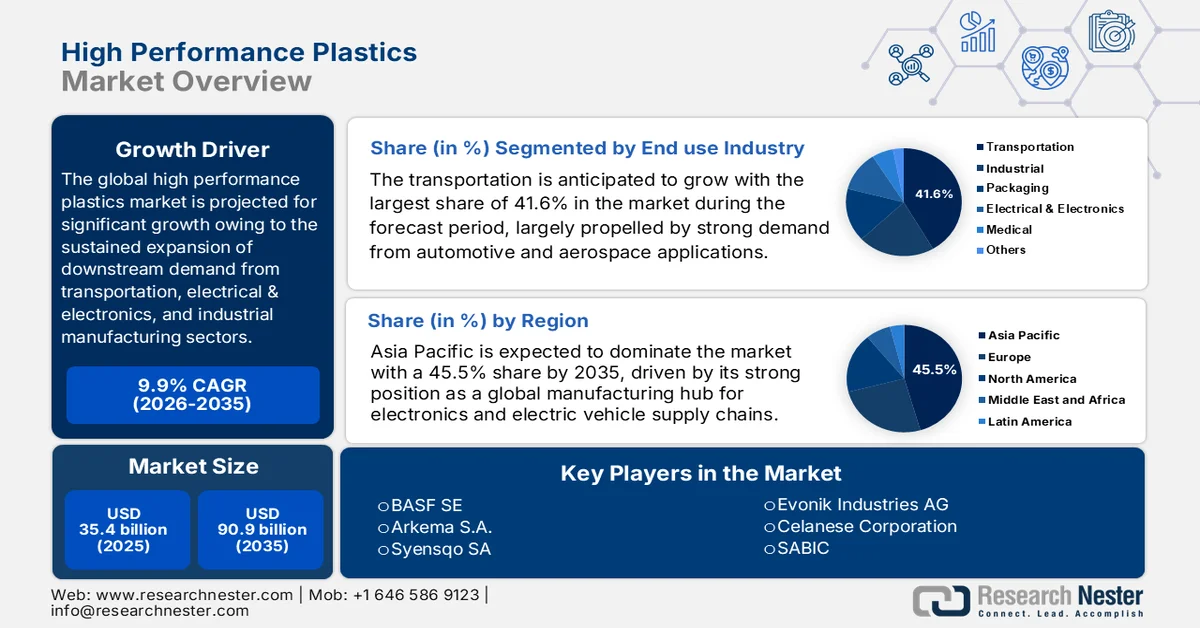

High Performance Plastics Market size was valued at USD 35.4 billion in 2025 and is predicted to reach USD 90.9 billion by the end of 2035, expanding at around 9.9% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of high performance plastics is assessed at USD 38.9 billion.

The global high performance plastics market is positioned for extensive growth over the years ahead, owing to the sustained expansion of downstream demand from transportation, electrical & electronics, and industrial manufacturing sectors. This is also supported by structural economic growth and increasing material substitution toward high-strength, lightweight polymers. In this context, the study by the Plastics Industry Association in 2025 revealed that the U.S. plastics industry demonstrated steady resilience in 2024, with manufacturing output and shipments supported by sustained downstream demand across industrial sectors. The article mentions that industry shipments reached USD 551 billion in 2024, whereas the total supplier-related shipments to the plastics sector stood at about USD 754 billion, reflecting strong upstream integration across raw materials and conversion industries. Plastic products accounted for nearly 75% of personal consumption usage in 2024, thus elevating the growth potential of the market.

Furthermore, the market benefits from trade activities that directly reshape supply stability, pricing, and global competitiveness. Strong exports expand market reach, whereas imports secure critical raw materials, thereby driving continued innovation in automotive, aerospace, and electronics. In this context, World Integrated Trade Solution reported that India’s imports of fluoro-polymers (excluding polytetrafluoroethylene) reached a substantial USD 89.15 million in 2023, which also reported a total import volume of 3,717,360 kg, indicating strong dependence on select global suppliers for high-performance polymer grades. Besides, the report outlined that China was the largest supplier with USD 27.65 million, followed by the U.S. with a total of USD 23.85 million and Japan with USD 17.94 million, reflecting concentrated sourcing from technologically advanced chemical manufacturing hubs.

India Fluoro-Polymers Import Statistics 2023 by Country: Trade Value, Volume & Key Supplier Analysis

|

Partner Country |

Trade Value (USD ‘000) |

Quantity (Kg) |

|

China |

27,653.34 |

1,415,660 |

|

U.S. |

23,852.49 |

770,157 |

|

Japan |

17,943.12 |

591,501 |

|

Singapore |

5,424.99 |

535,371 |

|

Netherlands |

4,147.83 |

113,917 |

|

Italy |

3,577.72 |

100,468 |

|

Germany |

2,596.13 |

76,516 |

|

France |

1,291.90 |

42,918 |

|

Korea, Rep. |

853.85 |

4,079 |

Source: WITS

Key High Performance Plastics Market Insights Summary:

Regional Highlights:

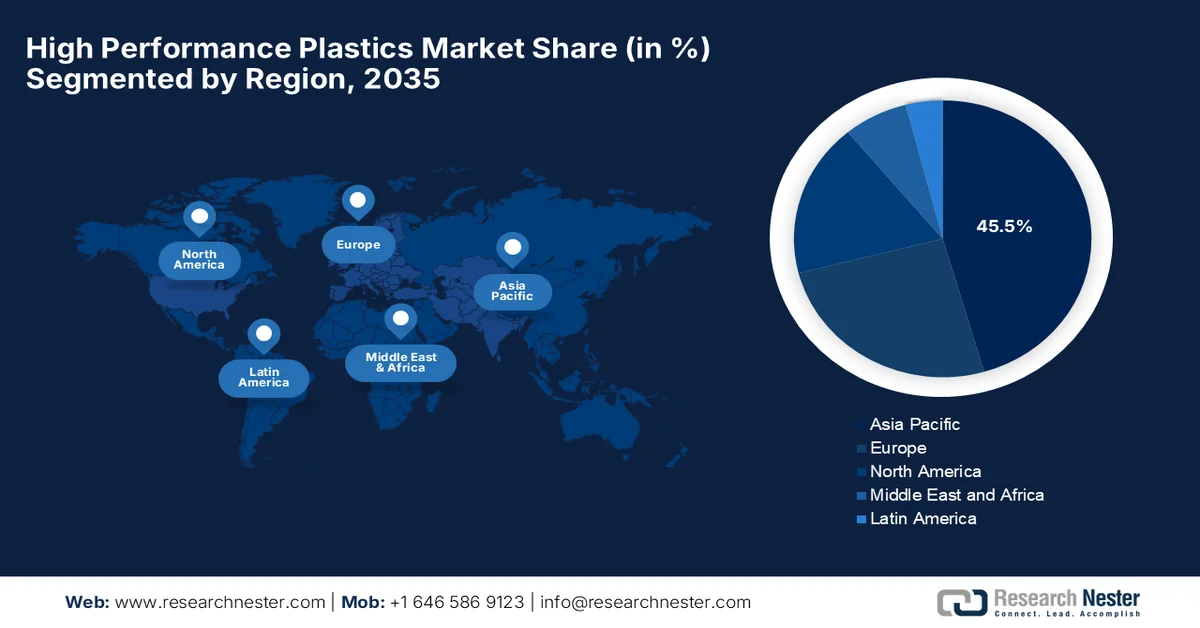

- The Asia Pacific high performance plastics market is forecast to account for 45.5% of global revenue by 2035, underpinned by its role as a major manufacturing hub for global electronics and electric vehicle supply chains

- Europe is expected to retain a prominent share of the market through 2035, bolstered by strong engineering excellence and sustainability innovation

Segment Insights:

- During the 2026–2035 period, the transportation segment is projected to capture 41.6% share of the high performance plastics market, reinforced by robust adoption across automotive and aerospace applications

- Fluoropolymer is anticipated to secure a considerable revenue share in the market by 2035, supported by expanding utilization across transportation, electronics, medical devices, and energy applications

Key Growth Trends:

- Aerospace & aviation demand

- Medical technology innovation

Major Challenges:

- Processing complexity and technical barriers

- Performance vs cost trade-off in mass adoption

Key Players: BASF SE, Arkema S.A., Syensqo SA, Evonik Industries AG, Celanese Corporation, SABIC, DuPont de Nemours, Inc., Victrex plc, Daikin Industries, Ltd., Solvay S.A., Toray Industries, Inc., Daher, LIST, Cetim, AniForm Engineering, DGAC, Mitsubishi Chemical Group Corporation.

Global High Performance Plastics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 35.4 billion

- 2026 Market Size: USD 38.9 billion

- Projected Market Size: USD 90.9 billion by 2035

- Growth Forecasts: 9.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (45.5% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Brazil, Saudi Arabia, Mexico

Last updated on : 26 June, 2026

High Performance Plastics Market - Growth Drivers and Challenges

Growth Drivers

- Aerospace & aviation demand: The aerospace and aviation industry is a major boosting factor for high performance plastics market, owing to the extensive need for lightweight and heat-resistant materials. These plastics reduce aircraft weight, improve fuel efficiency, and enhance safety. In January 2023, Airbus reported that the Airbus A350 is designed using around 70% advanced materials, which include a high share of carbon-fiber composites, and it significantly reduces aircraft weight and improves fuel efficiency. This lightweight structure, combined with advanced aerodynamics and efficient engines, enables the aircraft to achieve about 25% lower fuel burn and operating costs when compared to previous-generation widebody jets.

- Medical technology innovation: The extensive advancements in terms of medical devices and surgical techniques efficiently fuel the demand for biocompatible, sterilizable polymers in the emerging healthcare applications. High-performance plastics such as medical-grade PEEK and polysulfones are widely used to manufacture orthopedic implants, surgical instruments, and diagnostic equipment components. For instance, in April 2024, Evonik reported that its VESTAKEEP® i4 3DF PEEK filament enabled the first U.S. surgeries using Curieva’s world’s first 3D printed spinal implants for commercial use. The implants were manufactured using Curiteva’s proprietary additive manufacturing system and are designed to enhance osseointegration, radiolucency, and biomechanical compatibility with human bone, thus positively benefiting the high performance plastics market’s growth.

Challenges

- Processing complexity and technical barriers: The high performance plastics require certain advanced processing technologies and highly controlled manufacturing environments, which is a major challenge for both producers and end users. Most of the materials present high melting temperatures, narrow processing windows, and specialized molding or extrusion requirements. Therefore, improper processing can lead to defects and increased material waste, thereby affecting production efficiency and product quality. Manufacturers operating in the market need specialized equipment and skilled personnel to process these advanced polymers successfully. Furthermore, integrating high-performance plastics into existing production lines may require additional capital investment and technical knowledge, ultimately causing a hindrance to widespread adoption.

- Performance vs cost trade-off in mass adoption: Another important challenge that has skewed the growth of market is the trade-off between superior performance and high cost, which limits mass adoption of high-performance plastics. These materials offer superior mechanical strength and chemical stability, but their cost is still higher than that of engineering plastics or metals in many applications. As a result, industries are opting for these high-performance plastics for niche or critical applications rather than large-scale substitution. Apart from this, in the case of price-sensitive sectors, decision-makers might showcase a preference for cheaper alternatives even if they provide slightly lower performance. Hence, this is causing restrictions on market penetration, especially in developing regions.

High Performance Plastics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.9% |

|

Base Year Market Size (2025) |

USD 35.4 billion |

|

Forecast Year Market Size (2035) |

USD 90.9 billion |

|

Regional Scope |

|

High Performance Plastics Market Segmentation:

End use Industry Segment Analysis

The transportation in the end use industry is anticipated to grow with the largest share of 41.6% in the high performance plastics market during the forecast period. The segment’s dominance is largely propelled by strong demand from automotive and aerospace applications. High-performance plastics are extensively used in vehicle manufacturing for components such as insulation systems, under-the-hood parts, seals, and structural elements. In March 2026, SABIC announced the launch of ULTEM™ SU3102P reactive oligomer, which is a toughening agent for aerospace thermoset composites. This new polyetherimide oligomer enables loadings up to 50% by weight, thereby delivering a 140% better toughness-stiffness balance versus rPES, thus indicating a wider segment scope.

Type Segment Analysis

Fluoropolymer, which is under the type segment, is expected to grow with a considerable revenue share in the market during the discussed timeframe. Their exceptional chemical resistance, thermal stability, and non-reactive nature make them suitable for a wide range of demanding applications. They are used across industries such as transportation, electronics, medical devices, and energy, which also includes applications, i.e., wire insulation, lithium-ion battery components, biomedical implants, and protective coatings. In this context, Solvay and Agru in August 2023 signed a supply agreement for Solef® PVDF fluoropolymer with the main goal of securing a reliable material for ultra-pure semiconductor water piping systems. Besides, this collaboration combines Solvay’s high-purity fluoropolymer resins along with Agru’s engineering knowledge to deliver cleaner, more durable piping solutions.

Our in-depth analysis of the high performance plastics includes the following segments:

|

Segment |

Subsegments |

|

End use Industry |

|

|

Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

High Performance Plastics Market - Regional Analysis

APAC Market Insights

The Asia Pacific high performance plastics market is anticipated to dominate with a total share of 45.5% during the forecast period. The region’s dominance is mainly propelled by a central manufacturing hub for global electronics and electric vehicle supply chains. The regional industrialization, rising domestic consumption, and extensive infrastructure development across major manufacturing powerhouses also propel the demand for advanced polymers. In August 2023, BASF inaugurated a new Electronic Materials R&D Center at Ansan, South Korea, thereby relocating from Suwon to enhance efficiency and innovation. Hence, this expansion strengthens Ansan as a hub for engineering plastics and electronics R&D, and it complements BASF’s EPIC Korea and CECC centers. Such expansion strategies from the leading market players will position the region for unprecedented growth by the end of 2035.

The nation’s transition from a massive volume-based manufacturer into an advanced, high-value industrial powerhouse is propelling the upliftment of high performance plastics market in China. The country leads in terms of electric vehicle production, due to which the dependence on high-temperature specialty polymers such as PEEK and polyphenylene increases. Apart from this, the country's aggressive domestic push for semiconductor self-sufficiency and widespread 5G telecommunication infrastructure created an unprecedented demand for dimensionally stable liquid crystal polymers and ultra-pure fluoropolymers. Based on the government data published in November 2025, China’s new materials industry reached a scale of USD 1.2 trillion in 2024, which is a a 13.8% year-on-year growth. This progress is driven by innovations in PLA bioplastics, boehmite for EV battery safety, and AI-integrated frontier materials, and thus positively contributing to high performance plastics industry.

India market is poised for exponential growth owing to the emergence of the Make in India manufacturing initiative. In addition, the country’s booming electronics manufacturing and expanding telecommunications network deployment fuel a continuous demand for advanced resins with superior dielectric properties and high thermal stability. In December 2025, the article published by India Brand Equity Foundation revealed that the country’s plastic industry, which was valued at USD 26.61 billion in 2025, is projected to grow to USD 44.59 billion by 2030 at a CAGR of 10.9%, and it will be employing more than 5 million people across 30,000 processing units. The export value reached almost USD 5.8 billion in FY25, and India supplies plastics to more than 200 countries, which is led by the U.S. and UAE, hence suitable for bolstering the overall market’s growth.

India Polyamide Exports 2023: Country-wise Trade Shipment Value and Quantity Analysis

|

Partner |

Trade Value (1000 USD) |

Quantity (Kg) |

|

World |

29,747.19 |

9,643,880 |

|

Japan |

7,604.59 |

3,035,290 |

|

Malaysia |

3,614.25 |

797,175 |

|

Philippines |

3,243.46 |

449,500 |

|

U.S. |

3,192.18 |

1,165,850 |

|

Italy |

2,130.85 |

975,864 |

|

Thailand |

1,671.09 |

572,725 |

|

South Africa |

1,464.23 |

507,055 |

|

Singapore |

1,428.57 |

260,750 |

|

Germany |

720.47 |

232,249 |

|

UAE |

640.21 |

314,428 |

|

Vietnam |

627.02 |

207,900 |

|

China |

538.00 |

113,439 |

Source: WITS

Europe Market Insights

The Europe market has acquired a prominent position in the global landscape owing to the strong emphasis on engineering excellence and sustainability innovation. The region’s well-established aerospace and defense manufacturing industries utilize carbon-reinforced polymers and polyimides to engineer next-generation aircraft with minimized structural weight and lower fuel burn. For instance, in October 2025, Syensqo introduced a proprietary chemical recycling technology that enables infinite circularity of sulfone polymers such as PSU, PPSU, and PESU. This particular process depolymerizes post-industrial scrap and post-consumer parts into purified monomers, and it allows these materials to be reused without performance loss in new polymer products.

The premium automotive industry and highly organized mechanical engineering sector are driving high performance plastics market in Germany. The country’s luxury and electric vehicle manufacturers adopt advanced polymers such as PEEK and polyphenylene sulfide to insulate complex electrical powertrains and meet stringent regional environmental mandates. A strong industrial demand is being witnessed in the country’s advanced machinery and Industry 4.0 sectors, which depend on chemically resistant specialty resins. In November 2023, the POLYLINE project achieved a milestone at BMW’s Additive Manufacturing Campus in Munich by implementing the first-ever automated AM production line for polymer parts at scale. In partnership with DyeMansion, EOS, and Grenzebach, BMW demonstrated a fully digitalized, end-to-end process chain that boosts productivity and ensures consistent quality, thus heightening demand for high performance plastics in the country.

In the UK, the high performance plastics market is growing on account of pioneering research and development networks. The nation’s renowned life sciences and medical technology industries drive steady demand for bio-inert, highly sterilizable specialty resins used in advanced orthopedic implants, diagnostic equipment, and surgical instruments. As of April 2026, data from the UK Research and Innovation, the EPSRC manufacturing research hub for a sustainable future in engineering plastics, which is led by the University of Warwick, is pioneering circular economy solutions for durable polymer products. It readily tackles recycling challenges in engineering plastics used in transport, electronics, and construction, and the Hub focuses on advanced reuse, repair, remanufacturing, and digital tools such as product passports and twins.

North America Market Insights

North America market is growing at a considerable rate owing to a mature industrial base and a high concentration of technologically advanced end use industries. The region’s massive aerospace and defense manufacturing sectors serve as primary drivers of sustained demand, and it encourages more players to make investments in this sector. In this context, as stated by the Plastic Makers Organization in September 2025, the U.S. plastics industry was reported to generate more than USD 1.1 trillion in economic output, supporting nearly 5 million jobs. The sector possesses more than 11,600 facilities and 670,000 direct employees, thereby producing USD 380 billion in resins and products. Apart from this, the sector also invested almost USD 17.5 billion in new facilities and equipment, whereas plastics drive growth in key industries such as automotive, healthcare, and construction, while contributing USD 64 billion in exports.

The ongoing revitalization of the domestic semiconductor industry and 5G network infrastructure is responsibly boosting the U.S. high performance plastics market. In addition, the country’s market benefits from the accelerating electric vehicle transition and a highly advanced medical device sector that heavily integrates heat-resistant, biocompatible, and sterilizable specialty resins into automotive battery housings and orthopedic implants. For instance, in March, 2024, the Biden-Harris Administration and Intel announced a preliminary agreement for a total of USD 8.5 billion in direct CHIPS Act funding, along with eligibility for USD 11 billion in federal loans and a 25% investment tax credit on more than USD 100 billion in planned U.S. investments. These funds will deliberately accelerate Intel’s semiconductor projects in Arizona, New Mexico, Ohio, and Oregon, strengthening the demand for high performance plastics in the country.

In Canada, the market is progressing at a noteworthy rate, owing to the rising focus on natural resource development and aerospace innovation. The country’s market dynamics are also being reshaped by the massive oil, gas, and mining sectors, which require chemically resistant fluoropolymers to withstand extreme operating conditions. Based on the government data published in November 2023, Canada introduced its first significant project, which is supported by investment tax credits, and it allows Dow to construct the first-ever net-zero emissions ethylene cracker and derivatives facility in Fort Saskatchewan, Alberta. The total investment of USD 8.5 billion will cut about 1 million metric tons of CO2e annually through carbon capture and clean hydrogen technologies. Hence, such instances strengthen the domestic production of advanced polymer feedstocks used in oil & gas, mining, and aerospace applications.

Key High Performance Plastics Market Players:

- BASF SE (Germany)

- Arkema S. A. (France)

- Syensqo SA (Belgium)

- Evonik Industries AG (Germany)

- Celanese Corporation (U.S.)

- SABIC (Saudi Arabia)

- DuPont de Nemours, Inc. (U.S.)

- Victrex plc (UK)

- Daikin Industries, Ltd. (Japan)

- Solvay S.A. (Belgium)

- Toray Industries, Inc. (Japan)

- Daher (France)

- LIST (Luxembourg)

- Cetim (France)

- AniForm Engineering (Netherlands)

- DGAC (France)

- Mitsubishi Chemical Group Corporation (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF SE is a leading supplier of high-performance plastics, which operates through its Performance Materials division. The company’s portfolio of materials is extensively used in automotive, electronics, and industrial applications. BASF is highly focused on electrification and sustainable material solutions, supported by investments in circular economy initiatives.

- Arkema S.A. is also a foundational player in this sector, which offers advanced materials such as Kynar® PVDF, Rilsan® polyamides, Pebax® elastomers, and Kepstan® PEKK. The firm is primarily focused on high-growth sectors, which include electric vehicles, renewable energy, healthcare, and semiconductors.

- Syensqo SA supplies specialty polymers which includes KetaSpire® PEEK, Ryton® PPS, Amodel® PPA, and Solef® PVDF. The company focuses mainly on PVDF capacity expansion and development of circular polymer technologies, which have allowed it to maintain this leading position.

- Evonik Industries AG leverages prominence in high-performance polymers such as VESTAKEEP® PEEK, VESTAMID® polyamides, and TROGAMID® transparent polyamides. The company’s targeted applications include medical, automotive, additive manufacturing, and electronics.

- Celanese Corporation offers a broad portfolio of engineered materials, which includes Hostaform® POM, Fortron® PPS, Vectra® LCP, and Celanex® PBT. The firm is highly focused on metal replacement, electrification, and high-performance applications, supported by continuous portfolio expansion.

Here is a list of key players operating in the global market:

The high performance plastics market has been witnessing intense competition amongst the worldwide specialty chemical and advanced materials manufacturers who are focused on innovation, product differentiation, and application-specific solutions. The sector’s leading pioneers are making investments in R&D to enhance the thermal, mechanical, and chemical properties of high-performance polymers for use in different applications. Strategic initiatives opted by the market participants include capacity expansions, particularly for PEEK, PPS, and PVDF materials, as well as partnerships with automotive and battery manufacturers. For instance, in January 2025, Toray Industries announced the establishment of a new high-performance plastic compound production site in Guangdong Province, China. This facility is a part of Toray Resins (Foshan) Co., Ltd., and it will strengthen supply stability and meet rising demand in automotive, electronics, and solar applications.

Corporate Landscape of the Market:

Recent Developments

- In April 2026, BASF announced the expansion of its HALS and NOR® HALS capacities, showcasing its leadership in plastic additive solutions. The advanced NOR HALS technology is particularly important for China’s fast-growing plasticulture sector, ensuring multi-season agricultural films with improved sustainability.

- In January 2026, Daher won the JEC Composites Innovation Award - Aerospace (Parts) for its highly loaded thermoplastic wing rib, which was developed with partners including Victrex, LIST, Cetim, AniForm Engineering, and DGAC. This rib is made with VICTREX LMPAEK™ composites, and it delivers a 22% weight reduction when compared to aluminum.

- In May 2025, Syensqo signed new multi-year Solef® PVDF contracts with leading automotive OEMs and battery makers, solidifying its role in the fast-growing EV battery market. Solef® PVDF is a high-performance thermoplastic fluoropolymer that enhances lithium-ion batteries.

- Report ID: 8637

- Published Date: Jun 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.