Endpoint Detection and Response Market Outlook:

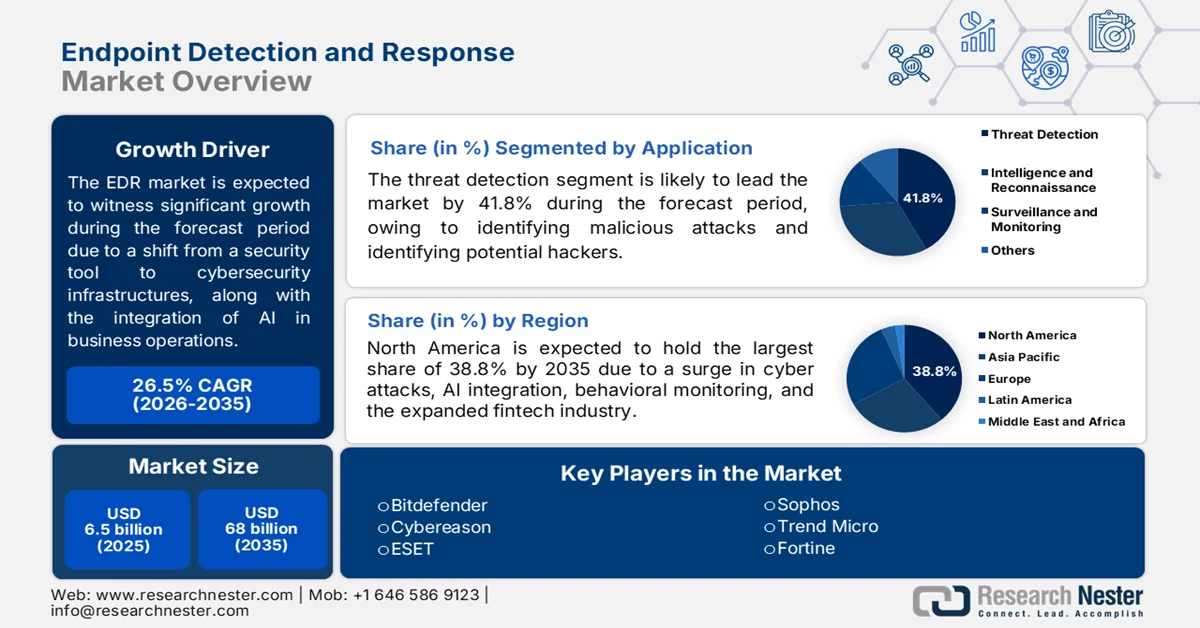

Endpoint Detection and Response Market size was valued at USD 6.5 billion in 2025 and is expected to cross USD 68 billion by the end of 2035, expanding at more than 26.5% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of endpoint detection and response is estimated at USD 8.2 billion.

The global endpoint detection and response market is readily undergoing a fundamental transformation from a niche endpoint security tool into the central part of modernized enterprise cybersecurity architectures. The growth is underpinned by the dissolution of conventional networks due to hybrid work culture, the maturation of artificial intelligence (AI)-based analytics, and the commercialization of ransomware-as-a-service. According to an article published by OECD in September 2025, in terms of the digital government index (DGI), 70% of countries utilized AI to optimize internal governmental processes, while just 33% utilized it to boost policy design and implementation. Therefore, the AI incorporation is gradually increasing in the government sector, thus bolstering the market demand. Besides, the continuous supply of computer storage devices is also responsible for uplifting the market demand globally.

Global Computer Storage Devices Import and Export Analysis, 2024

|

Countries/Components |

Export (USD Billion) |

Import (USD Billion) |

|

Thailand |

16.5 |

- |

|

China |

10.4 |

9.8 |

|

U.S. |

4.8 |

9.5 |

|

Hong Kong |

- |

5.8 |

|

Global Trade Value |

60.2 |

|

|

Global Trade Share |

0.2% |

|

|

Product Complexity |

0.89 |

|

|

Export Growth |

17.3% |

|

Source: OEC

Furthermore, the transition from standalone EDR to extended detection and response (XDR) platforms, which is followed by the generative AI revolutionizing threat investigation, and the proliferation of EDR-based toolkits and tamper-proof engineering, are a few trends that are also responsible for driving the endpoint detection and response (EDR) market. As stated in an article published by Array in December 2025, based on a survey, 50% of global organizations readily performed official risk evaluations with the utilization of generative AI during software development. Meanwhile, less than 30% adopted generative AI for conducting security evaluations, especially during the initial phases. Therefore, this particular gap underscores the requirement for a strong and structured framework for addressing security at each operational stage for promoting a proactive cybersecurity culture.

Key Endpoint Detection and Response Market Insights Summary:

Regional Highlights:

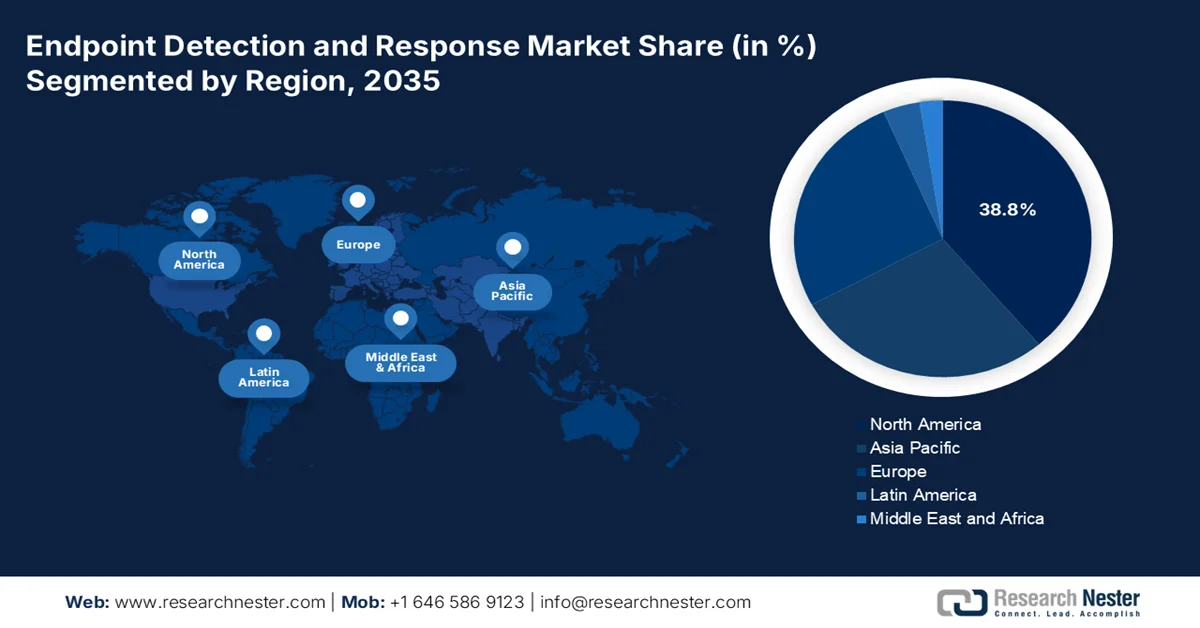

- Endpoint detection and response market North America is projected to account for 38.8% of the market share by 2035, underpinned by cybersecurity mandates, rising ransomware attacks, AI-powered threat detection platforms, and the expansion of fintech and natural resources industries

- Europe is expected to secure 26.4% of the market share by 2035, accelerated by strict regulatory policies, increasing adoption of threat detection technologies, and growing demand for hybrid-scalable and cloud-first solutions

- The endpoint detection and response (EDR) market in Japan caters to 6.3% of the regional share, owing to the support provision by its innovative technological landscape, along with a robust focus on cybersecurity

Segment Insights:

- Endpoint detection and response market The Threat Detection segment is anticipated to capture 41.8% of the market share by 2035, propelled by the increasing need to identify malicious cyberattacks before they cause severe damage

- The BFSI segment is forecast to hold 31.5% of the market share by 2035, reinforced by the growing need to prevent financial fraud, safeguard sensitive data, and ensure stringent regulatory compliance

Key Growth Trends:

- Accelerating the microservice adoption

- Democratizing enterprise-based EDR for SMEs

Major Challenges:

- Integration complexity with legacy OT environments

- Difficulty quantifying ROI and business value

Key Players: CrowdStrike (U.S.), Microsoft (U.S.), Palo Alto Networks (U.S.), SentinelOne (U.S.), Sophos (UK), Trend Micro (Japan), Fortinet (U.S.), Check Point (Israel), Bitdefender (Romania), Cybereason (U.S.), ESET (Slovakia), Ent (San Francisco, U.S.), WatchGuard Technologies (U.S.), Acronis (Switzerland), Ericsson (Sweden).

Global Endpoint Detection and Response Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.5 billion

- 2026 Market Size: USD 8.2 billion

- Projected Market Size: USD 68 billion by 2035

- Growth Forecasts: 26.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, South Korea, Singapore, Indonesia, Vietnam

Last updated on : 26 June, 2026

Endpoint Detection and Response Market - Growth Drivers and Challenges

Growth Drivers

- Accelerating the microservice adoption: The cloud-native EDR, along with cloud workload protection, is considered the rapid segment for benefiting the adoption, which is driving the endpoint detection and response market globally. According to an article published by the Open Access Government in April 2023, cloud computing is gradually rising, with worldwide end user expenditure on public cloud services reaching more than USD 590 billion as of 2025, indicating a 20.7% year-on-year (YoY) increase. In this regard, large-scale enterprises migrated almost 60% of their digital infrastructure to the cloud in the same year, which included both public and private hosting setups, thereby making it suitable for driving the market’s exposure.

- Democratizing enterprise-based EDR for SMEs: An increase in cyber threats has resulted in an upsurge in the demand for EDR services and solutions, which has enabled small and medium-sized enterprises (SMEs) to adopt security solutions. Besides, SMEs collaborated with governments to combat cybersecurity barriers and challenges, especially in Wales. As per the November 2023 International Journal of Information Management Data Insights article, the 2022 Cyber UK conference resulted in the launch of the National Cybersecurity Centre's (NCSC) flagship for combating cybersecurity issues in the UK. This comprised an investment of USD 12.5 million (£9.5 million) for the Innovation Hub in South Wales. The purpose of this investment was to assist domestic SMEs in increasing cyber defenses under the guidance of administrative bodies, such as Business Wales, thus proliferating the endpoint detection and response (EDR) market’s growth.

Challenges

- Integration complexity with legacy OT environments: The chemical industry and broader industrial sectors rely heavily on legacy operational technology systems that were never built with cybersecurity in mind. Many chemical plants operate aging programmable logic controllers, distributed control systems, and human-machine interfaces running decades-old software versions that cannot support modern endpoint agents. Installing EDR software on these critical systems risks destabilizing production processes, causing unintended shutdowns, or interfering with real-time operational requirements. Consequently, these OT environments often remain unmonitored, creating significant blind spots that adversaries actively target, thereby negatively impacting the endpoint detection and response (EDR) market growth.

- Difficulty quantifying ROI and business value: The endpoint detection and response market is fundamentally preventative and reactive investments where success is measured by the absence of successful attacks, a scenario that provides no direct revenue generation and makes ROI calculation exceptionally challenging for security leaders. Organizations struggle to justify substantial licensing, staffing, and infrastructure costs when the primary outcome is risk reduction rather than tangible business growth or operational efficiency gains. Moreover, budget decisions often default to reactive prioritization following high-profile incidents, rather than proactive strategic investment. The intangible nature of security value creates friction with finance teams demanding clear financial justification.

Endpoint Detection and Response Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

26.5% |

|

Base Year Market Size (2025) |

USD 6.5 billion |

|

Forecast Year Market Size (2035) |

USD 68 billion |

|

Regional Scope |

|

Endpoint Detection and Response Market Segmentation:

Application Segment Analysis

Based on the application, the threat detection segment is anticipated to garner the highest share of 41.8% in the endpoint detection and response market by the end of 2035. The segment’s upliftment is highly driven by the aspect of the process for identifying malicious attacks in the computer network before causing severe harm. Additionally, it is essential for recognizing hackers and combating them from locking files, stealing data, and shutting down businesses. According to the January 2023 PIB Government report, CERT-In, which is India’s ultimate defender against cyber threats, administered more than 2.9 million cyber incidents, issued 1,530 alerts, along with 390 vulnerability notes, and 65 advisories. Besides, carrying on with such activities, there is a huge demand for monitoring devices. Based on this, in May 2026, Omdia’s shipment of desktop monitors significantly reached 133.4 million tons as of 2025, increasing by 4.3% YoY growth, thereby boosting the market demand.

End user Segment Analysis

During the forecast period, the BFSI segment under end user is projected to grab the second-largest share of 31.5% in the endpoint detection and response (EDR) market. The segment’s growth is primarily attributed to the importance of EDR as a crucial cybersecurity tool for continuously withstanding data theft, preventing huge financial fraud, and ensuring stringent regulatory compliance. As stated in a data report published by the International Monetary Fund (IMF) in March 2026, across 20 sectors in the BFSI industry in 162 countries, financial-based cyber incidents readily accounted for almost 10%, and eventually concentrated in securities and banking segments. Besides, cyber-specific fraud tripled and continues to remain underestimated, owing to data barriers and underreporting across different jurisdictions, thus driving the market’s demand.

Point of Sale Segment Analysis

The workstations sub-segment, which is part of the point of sale segment, is expected to account for the third-largest share of 29.4% in the endpoint detection and response (EDR) market by the end of the stipulated timeline. The sub-segment’s development is effectively propelled by the aspect of remaining as the frontline battlefields for enterprise cybersecurity despite the growing shift toward cloud and mobile ecosystems. These fixed, high-performance machines are predominantly used by knowledge workers, security analysts, system administrators, and developers who require robust computing power for daily operations. From a security perspective, workstations are attractive attack surfaces because they host privileged credentials, handle unencrypted data in transit, and serve as gateways to critical servers and cloud consoles.

Our in-depth analysis of the endpoint detection and response market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

End user |

|

|

Point of Sale |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Endpoint Detection and Response Market - Regional Analysis

North America Market Insights

The North America endpoint detection and response market is anticipated to account for the highest share of 38.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to the presence of cybersecurity mandates, an increase in ransomware attacks, the integration of AI-based platforms for automated threat detection and behavioral monitoring, along with expansion in the fintech and natural resources industries. According to the Center for Strategic and International Studies article, in March 2026, Stryker witnessed a cyberattack on its Microsoft computer systems, leading to comprehensive disruption to shipping, production, and order processing. Likewise, in the same month, Telus, a telecommunications firm in Canada, reported a cybersecurity case, which involved unauthorized accessibility to its systems. Regarding this, the ShinyHunters hacking group was responsible and stole almost 700 terabytes of data, thus enhancing the market’s demand to overcome such incidents in the region.

The endpoint detection and response (EDR) market in the U.S. is growing significantly, owing to the proliferation of connected devices across different production centers, a rise in smart manufacturing, the convergence of operational technology with IT networks, and the demand for securing diversified endpoints. In terms of smart manufacturing, in November 2024, the National Institute of Standards and Technology’s Manufacturing Extension Partnership (NIST MEP) signed a memorandum of understanding with the Clean Energy Smart Manufacturing Innovation Institute (CESMII). The purpose was to strengthen the competitiveness of manufacturers in the country and assist small and medium-sized manufacturers in implementing smart manufacturing technologies. Therefore, with the increased adoption of such technologies, there is a huge demand for EDR systems to combat cyberattacks and ensure standard security services.

The industrial decarbonization, chemical safety and cybersecurity strategies, as well as government incentives and funding, are certain factors that are responsible for fueling the endpoint detection and response (EDR) market in Canada. As per an article published by the Government of Canada in April 2026, Budget 2023 generously allocated USD 5 million for more than 3 years, and established the Canadian Program for Cyber Security Certification (CPCSC). This program is readily led by Public Services and Procurement Canada and National Defense, suitable for mandating cybersecurity standards for defense contractors to guard sensitive data and information, along with maintaining interoperability with allies. Besides, in March 2026, the Government of Canada invested USD 3.6 million in the defense industry for the Université du Québec en Outaouais (UQO), which is focused on enhancing business integration into national and global supply chains.

Europe Market Insights

Europe in the endpoint detection and response market is expected to emerge as the fastest-growing region, with a share of 26.4% during the forecast period. The market’s development is highly propelled by strict regulatory policies, standard compliance with frameworks, the increased adoption of threat detection technologies by organizations, and the demand for hybrid-scalable and cloud-first solutions. According to an article published by the European Commission in June 2026, the Cybersecurity Act expanded the EU Agency for Cybersecurity (ENISA) and established a cybersecurity certification framework for products and services. Additionally, in January 2026, the Commission proposed the newest Cybersecurity Act for strengthening the regional cybersecurity capabilities and resilience, thereby indicating a huge growth opportunity for the market.

The endpoint detection and response (EDR) market in Germany is gaining increased traction, owing to its emergence as the powerhouse of chemicals, automotive, and manufacturing, along with a massive industrial base for expanding the endpoint landscape and ensuring suitable digital transformation. As stated in an article published by GovTec Intelligence Hub in July 2025, the aspect of gaining Denmark’s level of administrative digitalization has the ability to increase Germany’s real gross domestic product (GDP) per capita by 2.7%. Based on this, the country is poised to design its very own digital public infrastructure (DPI) for directly integrating with regional ecosystems, including cross-border data spaces and eIDAS 2.0 digital wallets, as well as assist in establishing standard rules for reflecting regional values, thus demonstrating an optimistic outlook for the market development.

The government-based digitalization, an expansion in investments for technological processes, the rapid adoption of connected manufacturing technologies, and innovation in advanced manufacturing technologies are a few trends that are responsible for boosting the endpoint detection and response market in France. As per the 2024 European Parliament data report, the country significantly accounted for 12.4% of regional net greenhouse gas emissions as of 2023. Besides, emissions from industries under the regional emission trading system reduced by 52.3% and from effort-sharing industries by 24.1%. Therefore, to focus on the aim of achieving 55% reduction in net emissions, the country intends to consider diminishing emissions by 5% every year by the end of 2030. This particular action readily drives digitalization and ensures expansion in the latest endpoints as suitable tools for gaining complete emission reduction.

APAC Market Insights

The Asia Pacific in the endpoint detection and response (EDR) market is projected to witness a considerable share of 28.3% by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by healthcare modernization, digital banking, and government digitalization, especially across Southeast Asia, South Korea, Japan, China, and India. According to a report published by AMRO ASIA in 2025, increased mobile penetration has bolstered the adoption of digital payments, with Bakong reaching 30 million users as of 2024, along with an increase in the number of KHQR-registered merchants to 4.5 million. Besides, there was a surge in digital transactions by 67.7% between 2022 and 2024, rising to USD 181.8 billion (KHR 728.9 trillion), thereby enhancing the market demand for identifying and overcoming cyberattacks.

The endpoint detection and response market in China is gaining increased exposure, owing to the largest digital and industrial economy, massive manufacturing sector, rapid smart city approaches, the existence of policies for optimizing digitalization and safety mandates, and the creation of deployment opportunities. As stated in an article published by the China Organization in November 2025, the country’s overall transaction valuation in digital payments successfully reached an estimated USD 10 trillion as of 025, which is further predicted to be worth USD 13.5 trillion by the end of 2030. In terms of digitalization in Beijing, more than 5 billion real-time transactions were undertaken in 2022, and over 80 million enterprises and corporations adopted digital payment systems. Therefore, all these developments led to near-ubiquitous digitalization across the national economy, thus positively driving the market growth.

The aspects of growing awareness of vulnerabilities in the supply chain, an upsurge in digital transformation, government-specific cybersecurity approaches, and the integration of IoT and digital solutions are certain factors that are responsible for boosting the endpoint detection and response (EDR) market in Japan. As per a data report published by Cyber Japan in December 2025, a North Korea-based cyberattack group, referred to as TraderTraitor, stole cryptocurrency that was worth roughly USD 298 million (48.2 billion yen) from a domestic cryptocurrency business as of May 2024. Likewise, there was a ransomware attack at the Port of Nagoya in 2023, followed by an attack on the National Center of Incident Readiness and Strategy for Cybersecurity (NISC) in the same year, and cyberattacks against the Japan Aerospace Exploration Agency (JAXA) between 2021 and 2024. Therefore, all these incidents denote a huge demand for the market in the country to combat cyber risks.

Key Endpoint Detection and Response Market Players:

- CrowdStrike (U.S.)

- Microsoft (U.S.)

- Palo Alto Networks (U.S.)

- SentinelOne (U.S.)

- Sophos (UK)

- Trend Micro (Japan)

- Fortinet (U.S.)

- Check Point (Israel)

- Bitdefender (Romania)

- Cybereason (U.S.)

- ESET (Slovakia)

- Ent (San Francisco)

- WatchGuard® Technologies (U.S.)

- Acronis (Switzerland)

- Ericsson (Sweden)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- CrowdStrike is a dominant force in the endpoint detection and response (EDR) market, built from the ground up as a cloud-native platform that delivers lightweight, high-performance endpoint protection. The company is widely recognized for its elite threat intelligence team and its ability to stop breaches through real-time behavioral analysis.

- Microsoft leverages its pervasive enterprise ecosystem to offer deeply integrated EDR capabilities through Microsoft Defender for Endpoint. The company's strength lies in its seamless native integration with Windows, Azure, and Microsoft 365, making it the default choice for organizations already committed to the Microsoft security stack.

- Palo Alto Networks competes with its Cortex XDR platform, which extends beyond traditional endpoint detection to unify telemetry from networks, cloud workloads, and third-party data sources. The company differentiates itself by appealing to mature security operations teams that require deep investigative capabilities and extensive customization.

- SentinelOne is known for its autonomous, AI-driven Singularity XDR platform that emphasizes self-healing capabilities and automated incident response. The company positions itself as an innovator in endpoint security, offering unified protection across enterprise endpoints, cloud workloads, and containerized environments.

- Sophos delivers accessible, highly manageable EDR and XDR solutions tailored for mid-market enterprises and managed service providers. The company differentiates itself through its integrated approach to endpoint protection, extended detection and response, and its ability to augment lean security teams with managed threat hunting services.

Here is a list of key players operating in the global market:

The endpoint detection and response market is characterized by a consolidated group of established cybersecurity giants and a few highly specialized innovators, with intense competition centered on AI-native architectures and platform integration. A few dominant players, including CrowdStrike, Microsoft, and Palo Alto Networks, hold significant market share globally, leveraging their robust cloud-native platforms and broad threat intelligence networks. These leaders compete intensely with vendors, such as SentinelOne and Sophos, who differentiate themselves through dedicated forensics, autonomous response capabilities, and recognition in independent evaluations. Besides, in February 2026, Ericsson expanded its telecom cybersecurity by providing an agentless EDR, developed for mission-critical systems and telco networks, thereby positively contributing towards the EDR industry’s growth.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, Ent, which is an intent-based workspace security organization, effectively emerged from stealth with USD 100 million in seed financing, suitable for approaching the cybersecurity development.

- In October 2025, WatchGuard® Technologies launched the endpoint security prime, which is the latest package for redefining the standard for ensuring endpoint protection, readily available in North America.

- In June 2024, Acronis unveiled Acronis Advanced Security + XDR, which is the newest addition to its security solution portfolio, easy to manage, maintain, and deploy, further expanding the EDR provision.

- Report ID: 8638

- Published Date: Jun 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.