Incident Response Market Outlook:

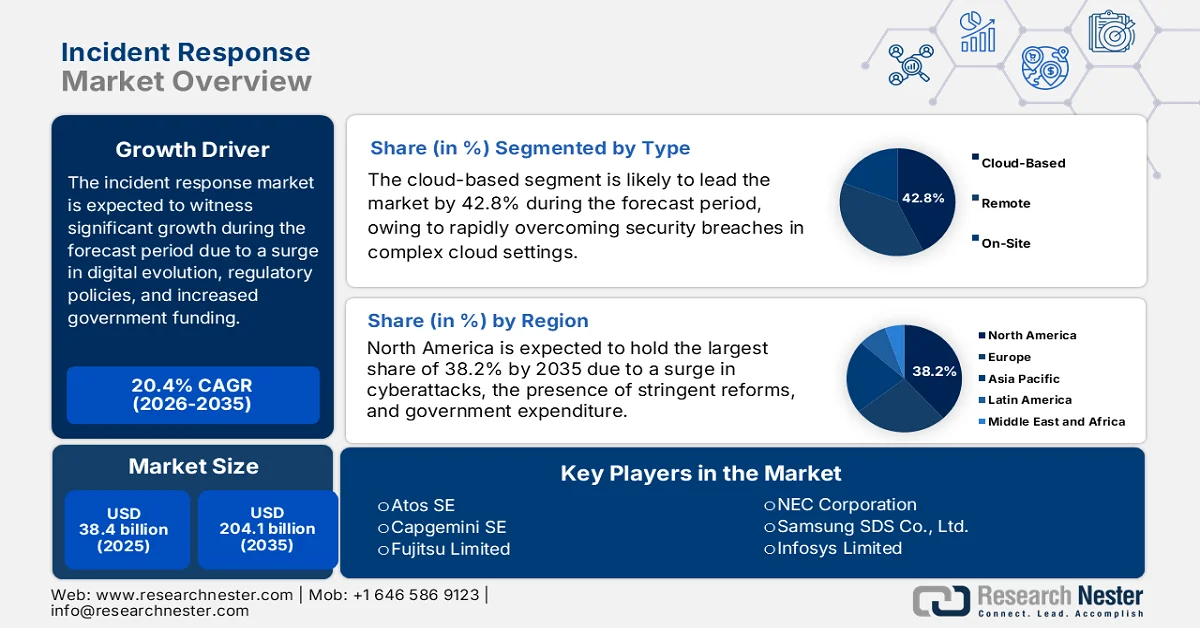

Incident Response Market size was over USD 38.4 billion in 2025 and is estimated to reach USD 204.1 billion by the end of 2035, expanding at a CAGR of 20.4% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of incident response is evaluated at USD 46.2 billion.

The international incident response market is rapidly evolving, owing to the convergence of digital transformation, the existence of regulatory mandates, enterprise adoption, increased government investments, and the presence of heightened cyber risks. According to official statistics published by the World Bank Organization in 2026, almost 1/3rd of the international population, or 2.6 billion people, remained offline as of 2023. In addition, over 90% of people across high-income nations utilized the internet as of 2022, while just 1 in 4 in low-income nations utilized the internet. Therefore, the worldwide community is recommended to assist in creating nations to catch up and escalating the digital adoption. This has eventually resulted in a huge growth opportunity for the market globally.

Furthermore, the integration of incident response with zero trust architectures, a rise in incident response-as-a-service (IRaaS), cross-sector collaboration platforms, and the gamification of cybersecurity training are a few trends that are bolstering the incident response market globally. As stated in a data report published by the Internet Crime Report in 2024, the organization has received an estimated 2,000 complaints every month, and since the past 5 years, there has been an average of 2,000 complaints every day. Besides, fraud demonstrated the bulk of reported losses as of 2024, along with ransomware emerging as the most pervasive risk to severe infrastructure, with complaints rising by 9% since 2023. Moreover, people aged more than 60 years suffered the most losses and submitted the majority of complaints, thereby enhancing the market’s demand across different nations.

Key Incident Response Market Insights Summary:

Regional Highlights:

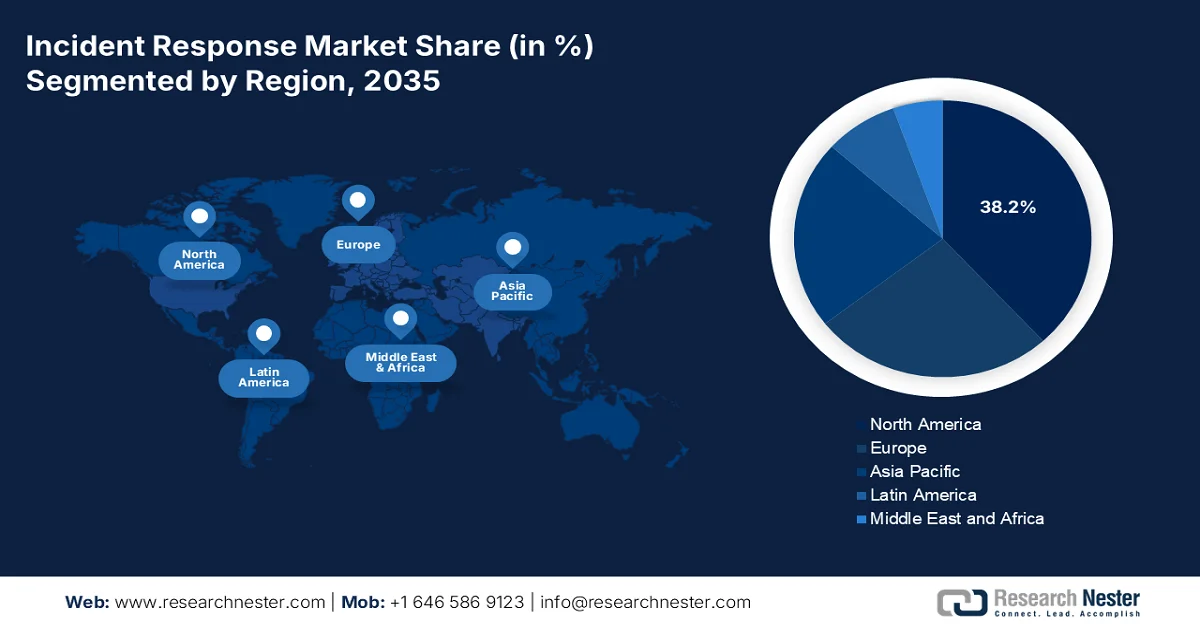

- North America is projected to capture the largest revenue share of 38.2% by 2035 in the incident response market, attributed to the rising frequency of cyberattacks, stringent compliance frameworks, and substantial governmental spending.

- Asia Pacific is anticipated to register the fastest growth in the market over 2026-2035, propelled by accelerating digitalization, expanding cloud adoption, and increasing ICT expenditure across emerging economies.

Segment Insights:

- The cloud-based segment is forecasted to account for a dominant 42.8% share by 2035 in the incident response market, driven by its critical role in rapidly identifying, remediating, and containing security breaches within complex and scalable cloud environments.

- The critical incidents segment is expected to secure the second-highest share during 2026–2035, fueled by the rising occurrence of severe operational disruptions and high-impact cyberattacks necessitating immediate response strategies.

Key Growth Trends:

- Explosion of edge and IoT devices

- Expansion in AI-driven threat hunting

Major Challenges:

- Escalating complexity of cyber threats

- Shortage of skilled cybersecurity professionals

Key Players: IBM Corporation (U.S.), Cisco Systems, Inc. (U.S.), Palo Alto Networks, Inc. (U.S.), Accenture plc (Ireland), Deloitte Touche Tohmatsu Limited (UK), KPMG International (Netherlands), EY (UK), McAfee, LLC (U.S.), FireEye, Inc. (U.S.), CrowdStrike Holdings, Inc. (U.S.), Check Point Software Technologies Ltd. (Israel), BAE Systems plc (UK), Atos SE (France), Capgemini SE (France), Fujitsu Limited (Japan), NEC Corporation (Japan), Samsung SDS Co., Ltd. (South Korea), Infosys Limited (India), Wipro Limited (India), Telekom Malaysia Berhad (Malaysia).

Global Incident Response Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 38.4 billion

- 2026 Market Size: USD 46.2 billion

- Projected Market Size: USD 204.1 billion by 2035

- Growth Forecasts: 20.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.2% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, South Korea, Singapore, Australia, Canada

Last updated on : 19 February, 2026

Incident Response Market - Growth Drivers and Challenges

Growth Drivers

- Explosion of edge and IoT devices: The proliferation of edge computing and the Internet of Things (IoT) has created the newest vulnerabilities, significantly fueling the demand for incident response solutions that are tailored to decentralized environments. According to official statistics published by the OECD in October 2023, semiconductor components of IoT devices have been continuously growing and are estimated to account for between 5% and 7% of the international semiconductor industry. Besides, IoT-specific patent applications surged by nearly 20% every year and further accounted for more than 11% of overall patenting activity internationally. Moreover, venture capital investment across IoT firms also boosted, significantly reaching USD 8 billion, thereby enhancing the incident response market’s growth.

- Expansion in AI-driven threat hunting: The aspect of artificial intelligence (AI)-based predictive analytics is readily ensuring proactive detection of anomalies, thus making the incident response market extremely efficient and diminishing mean-time-to-respond (MTTR). As per an article published by the 2025 AI Index Report, researchers have unveiled the latest benchmarks in AI, such as SWE, GPQA, and MMMU, with an increase in performance from 18.8% to 48.9% and 67.3% points. Besides, as of 2023, the U.S. Food and Drug Administration (FDA) successfully approved 223 AI-driven medical devices, denoting a rise from only 6 devices. Therefore, this continuous increase in AI utilization has resulted in threats, based on which there is a huge demand for the market internationally.

- Increase of government-backed digital approaches: Countries are generously funding national cybersecurity programs to readily protect critical infrastructure, directly bolstering the demand for incident response market services. As per a data report published by MEITY in January 2025, through governmental support, the digital economy in India accounted for 11.7% of the national income between 2022 and 2023 and further increased to 13.4% between 2024 and 2025. In addition, the country’s digital economy between 2022 and 2023 has been equivalent to INR 28.9 lakh crore (approximately USD 368 billion) in GVA and INR 31.6 lakh crore, which is estimated to be USD 402 billion in gross domestic product (GDP), thereby enhancing the market’s demand.

Challenges

- Escalating complexity of cyber threats: The incident response market faces a major challenge in keeping pace with increasingly sophisticated cyberattacks. Threat actors are leveraging advanced techniques such as AI-driven malware, polymorphic ransomware, and supply chain attacks that bypass traditional detection systems. This complexity requires organizations to invest heavily in advanced analytics, threat intelligence, and automation. However, many enterprises lack the skilled workforce and budget to deploy such solutions effectively. The rapid evolution of attack vectors also means that incident response frameworks must be continuously updated, creating operational strain.

- Shortage of skilled cybersecurity professionals: A critical roadblock for the incident response market is the global shortage of skilled cybersecurity professionals. According to industry associations, different cybersecurity roles remain unfilled worldwide, with incident response expertise being among the most in-demand. This talent gap limits organizations’ ability to build robust response teams capable of handling complex breaches. Besides, skilled professionals are required not only for detection and containment but also for forensic analysis, compliance reporting, and recovery planning. The shortage is particularly acute in emerging markets, where digital transformation is accelerating but cybersecurity education and training lag behind.

Incident Response Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

20.4% |

|

Base Year Market Size (2025) |

USD 38.4 billion |

|

Forecast Year Market Size (2035) |

USD 204.1 billion |

|

Regional Scope |

|

Incident Response Market Segmentation:

Type Segment Analysis

The cloud-based segment, which is part of the type, is anticipated to garner the highest share of 42.8% in the incident response market by the end of 2035. The segment’s upliftment is highly driven by its importance for rapidly remediating, identifying, and containing security breaches within complex, scalable, and dynamic cloud environments. According to official statistics published by the National Center for Science and Engineering Statistics in August 2022, the Broadband Equity, Access, and Deployment Program generously authorized USD 42.4 billion for digitalized infrastructure investment, readily prioritizing underserved and unserved regions. Therefore, based on this, cloud-based services have been introduced to diminish experimentation expenses through digitalization, thus creating an optimistic outlook for the segment’s growth and expansion.

Incident Severity Segment Analysis

The critical incidents segment in the incident response market is projected to hold the second-highest share during the forecast period. The segment’s growth is highly fueled by the existence of major disruptions, including severe operational failures or cyberattacks. These are paramount in incident response for reducing reputational and financial damage, protecting employee well-being, and ensuring business continuity. As per an article published by the Center for Strategic & International Studies in 2026, Medusa, the ransomware company, reported being responsible for a data breach for SimonMed Imaging, during which hackers exfiltrated data belonging to an estimated 1.2 million patients in October 2025. Additionally, in the same year, hackers uploaded 23 million customer records belonging to different companies, such as Vietnam Airlines, thereby enhancing the market’s demand globally.

Component Segment Analysis

By the end of the stipulated timeline, the services sub-segment under the component is expected to account for the third-highest share in the incident response market. The sub-segment’s development is highly propelled by the rising demand for managed security services, consulting, and training. Organizations increasingly outsource incident response functions to specialized providers due to the shortage of skilled cybersecurity professionals and the escalating complexity of cyber threats. Managed services offer continuous monitoring, rapid detection, and automated response capabilities, reducing mean-time-to-respond (MTTR) and ensuring compliance with regulatory frameworks such as GDPR, HIPAA, and NIST. Consulting services play a critical role in assisting enterprises in designing tailored response strategies, conducting forensic investigations, and aligning with industry-specific compliance mandates.

Our in-depth analysis of the incident response market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Incident Severity |

|

|

Component |

|

|

Response Time |

|

|

Deployment Model |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Incident Response Market - Regional Analysis

North America Market Insights

North America in the incident response market is anticipated to garner the largest share of 38.2% by the end of 2035. The market’s upliftment in the region is highly attributed to an increase in cyberattack frequency, the presence of strict compliance, such as FFIEC, NIST, and HIPAA, along with the provision of generous governmental spending. According to official statistics published by the America Hospital Association in October 2025, 364 hacking cases have been recorded by the U.S. Department of Health and Human Services Office for Civil Rights. This has readily affected more than 33 million of the regional population, resulting in the market’s increased demand. Besides, by the end of 2024, 259 million people’s protected health information (PHI) has been reported to be hacked, of which 192.7 million people’s healthcare records have been stolen during the UnitedHealth Group/Change Healthcare ransomware attack, thus boosting the market’s growth in the region.

The incident response market in the U.S. is growing significantly, owing to the presence of regulatory mandates, federal investments, broadband expansion, as well as cybersecurity enforcement. As per an article published by NLM in January 2023, the U.S. federal government generously authorized USD 87 billion in funding for broadband accessibility and adoption. This particular fund includes USD 65 billion from the Infrastructure Investment and Jobs Act to effectively address the digitalization divide, with USD 20.4 billion for funding digital equity policies from the America Rescue Plan. In addition, USD 1.6 billion has been allocated from the Consolidated Appropriations Act for significantly connecting minority communities, general broadband infrastructure deployment, and connectivity in tribal lands, thereby proliferating the incident response market’s growth.

The aspects of 5G expansion, the presence of digital transformation programs that enhance cybersecurity readiness, regulatory frameworks, along with promoting professional standards and ICT resilience are factors that are bolstering the incident response market in Canada. Based on government estimates published by the Government of Canada in December 2024, the Minister of Families, Children and Social Development, on behalf of the Minister of Innovation, Science and Industry, declared an investment of USD 45 million in a USD 66 million project, deliberately led by the Centre of Excellence in Next Generation Networks (CENGN). Therefore, this particular investment, which is made through the Strategic Innovation Fund (SIF) is expected to support the establishment of an unusual 5G testbed to create 5G-based applications, thus driving the market’s growth.

APAC Market Insights

The Asia Pacific incident response market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by rapid digitalization, an upsurge in cloud adoption, an increase in ICT expenditure, and the presence of METI-based ICT resilience programs. According to an official data report published by the UNESCAP Organization in 2023, a 1% surge in cloud penetration has yielded 0.7% average gross domestic product (GDP) increase in the overall region. Additionally, the cloud computing contribution to the economies of Vietnam, South Korea, Singapore, the Philippines, New Zealand, Malaysia, Japan, Indonesia, India, and Australia has ranged from 0.2% to 2.2% of the GDP as of 2023. Therefore, with this continuous increase in cloud adoption, there is a huge growth opportunity for the market in the region.

Overall Cloud Economic Contribution in the Asia Pacific (2022)

|

Countries |

Cloud Contribution |

|

Singapore |

2.2% |

|

New Zealand |

2.1% |

|

Australia |

0.6% |

|

Japan |

0.6% |

|

Malaysia |

0.5% |

|

Korea |

0.4% |

|

Thailand |

0.4% |

|

Philippines |

0.3% |

|

Vietnam |

0.3% |

|

India |

0.2% |

|

Indonesia |

0.2% |

Source: UNESCAP Organization

The incident response market in China is gaining increased traction, owing to an increase in the enterprise adoption of innovative cybersecurity frameworks, the presence of regulatory mandates, and the provision of strong government-based ICT investments. As stated in an article published by the State Council Information Office in August 2022, the country has witnessed a rapid growth of internet users, with an increase to 1.0 billion from 564 million. Meanwhile, the internet utilization rate among the population also increased to 73% from 42.1%, leading to a huge demand for the market within the country. Besides, the country is regarded as the world’s largest and most innovative optical fiber broadband and mobile communications network, with the presence of 1.8 million 5G base stations, thereby making it suitable for bolstering the market’s exposure in the country.

The aspects of government expenditure, a surge in enterprise adoption, policy support, telecom expansion, regulatory compliance, and industrial collaboration are factors that are responsible for uplifting the incident response market in India. According to official statistics published by the IBEF Organization in November 2025, the country’s telecom industry is continuing to demonstrate robust momentum, with total revenue rising from USD 39.2 billion as of 2024 to USD 43.4 billion in 2025. In addition, the overall tele-density stood at 86.6%, deliberately reflecting the comprehensive reach of connectivity across the whole nation. Moreover, the overall telephone subscriber base has significantly reached 1.2 billion in September 2025, readily supported by wireless services, accounting for 1,182.3 million subscribers, thereby denoting an optimistic outlook for the market’s growth.

Europe Market Insights

Europe in the incident response market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the presence of GDPR compliance, regional cybersecurity policies, digital innovation facilities, robust ICT regulations, and governmental approaches. According to official statistics published by the ITA in January 2026, the Netherlands is well-known for its innovative digitalized infrastructure, which has made it rank second globally for online connectivity, with over 98% of households having a broadband connection. Additionally, the country comprises a well-established digitalized payment facility, with iDEAL as the ultimate Dutch payment solution, with 70% market share for online purchases. This has paved the way for increased cybercrimes, thus bolstering the market’s demand in the overall region.

The incident response market in the UK is gaining increased exposure, owing to government budget allocation, regulatory oversight, industrial collaboration, digital transformation, and regional support. As per a data report published by the Center for Data Innovation in November 2024, the AI industry in the country is presently valued at more than USD 21 billion, which is considered the third-largest AI industry in the world after the U.S. and China. Besides, the average number of employees for data-based organizations is nearly 1,500 in comparison to 700 for non-data-intensive firms. Furthermore, more than 80% of all jobs advertised in the country presently require digital skills, and this particular digital skills barrier costs the domestic economy as much as £63 billion within a year in lost GDP, thereby denoting a huge opportunity for the market’s growth in the country.

The aspects of generous government investment in modernizing the ICT industry, an increase in the enterprise adoption of innovative cybersecurity frameworks, and regulatory compliance are factors that are bolstering the incident response market in Germany. Based on government estimates published by the ITA in August 2025, 89% of the population readily supports healthcare digitalization, with developments including e-prescriptions, electronic patient records, and video consultations. Besides, 46% of domestic organizations are presently utilizing cloud computing technology to conduct business processes, along with an additional 11% on the verge of planning to adopt. Moreover, the country’s cybersecurity expenditure has reached over USD 10 billion as of 2023, thereby positively impacting the localized ICT industry, which in turn, is boosting the market’s exposure.

Germany ICT Industry Growth Analysis (2022-2025)

|

Components |

2022 (USD Billion) |

2023 (USD Billion) |

2024 (USD Billion) |

2025 (USD Billion) |

|

Overall Exports |

185.8 |

198.5 |

187.8 |

69.5 |

|

Overall Imports |

213.5 |

229.8 |

212.6 |

78.6 |

|

Imports from the U.S. |

5.5 |

6.0 |

5.6 |

2.3 |

Source: ITA

Key Incident Response Market Players:

- IBM Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- Palo Alto Networks, Inc. (U.S.)

- Accenture plc (Ireland)

- Deloitte Touche Tohmatsu Limited (UK)

- KPMG International (Netherlands)

- EY (UK)

- McAfee, LLC (U.S.)

- FireEye, Inc. (U.S.)

- CrowdStrike Holdings, Inc. (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- BAE Systems plc (UK)

- Atos SE (France)

- Capgemini SE (France)

- Fujitsu Limited (Japan)

- NEC Corporation (Japan)

- Samsung SDS Co., Ltd. (South Korea)

- Infosys Limited (India)

- Wipro Limited (India)

- Telekom Malaysia Berhad (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- IBM Corporation is one of the leading players in the incident response market, leveraging its IBM Security X-Force team to provide advanced threat intelligence and response services. The company integrates AI-driven analytics with cloud-native solutions to reduce response times and improve resilience. IBM’s partnerships with enterprises and governments strengthen its role in critical infrastructure protection.

- Cisco Systems, Inc. offers comprehensive incident response services through its Cisco Talos Intelligence Group, focusing on proactive threat detection and remediation. Its solutions integrate seamlessly with enterprise networks, enhancing visibility and control. Cisco’s emphasis on managed security services and compliance frameworks positions it as a trusted provider in the BFSI and government sectors.

- Palo Alto Networks, Inc. significantly drives innovation in automated incident response through its Cortex XDR and XSOAR platforms. The company emphasizes AI-powered detection, orchestration, and rapid containment of cyber threats. Its strong presence in cloud security and partnerships with global enterprises make it a dominant force in reducing mean-time-to-respond (MTTR).

- Accenture plc provides incident response services through its Accenture Security division, offering consulting, managed services, and digital forensics. The firm focuses on sector-specific solutions, particularly in BFSI and healthcare, where compliance and resilience are critical. Additionally, the company’s global reach and integration of AI-driven response frameworks enhance its competitive positioning.

- Deloitte Touche Tohmatsu Limited delivers incident response solutions through its Cyber Risk Services, emphasizing regulatory compliance and enterprise resilience. The company supports clients with forensic investigations, breach containment, and recovery strategies. Deloitte’s strong advisory role and collaboration with government agencies make it a key player in shaping cybersecurity policy and incident response frameworks.

Here is a list of key players operating in the global incident response market:

The international incident response market is highly competitive, with U.S. firms such as IBM, Cisco, and Palo Alto Networks leading the way with AI-driven detection and managed services. Europe-based players, including Atos and Capgemini, emphasize compliance with GDPR and regional cybersecurity mandates, while Japan-specific firms Fujitsu and NEC focus on integrated ICT resilience. Besides, South Korea’s Samsung SDS and India’s Infosys leverage cloud-native solutions for rapid response. Strategic initiatives include mergers, acquisitions, and partnerships with cloud providers, as well as investments in automation and threat intelligence. For instance, in February 2025, Morgan Lewis expanded cybersecurity services and bolstered its incident response and privacy practice by forming a standard partnership with international leaders, thereby uplifting the incident response industry globally.

Corporate Landscape of the Incident Response Market:

Recent Developments

- In November 2025, LevelBlue successfully completed its acquisition of Cybereason to bolster its international leadership in managed detection and response (MDR), cybersecurity consulting, and incident response, along with developing one of the sector’s most integrated and wide-ranging security platforms.

- In July 2025, KDDI and LAC commenced with the worldwide deployment of security solutions to effectively counter cyberattacks by combining expertise in security operations and monitoring, which are backed by Japan’s large-scale security operations facilities with an international business footprint.

- In December 2024, Tata Consultancy Services (TCS) unveiled the 2025 Cybersecurity Outlook by introducing supply chain resilience, cloud security, and generative AI, all of which are suitable for organizations to effectively navigate the threat landscape in upcoming years.

- Report ID: 8401

- Published Date: Feb 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.