Electrical Insulation Materials Market Outlook:

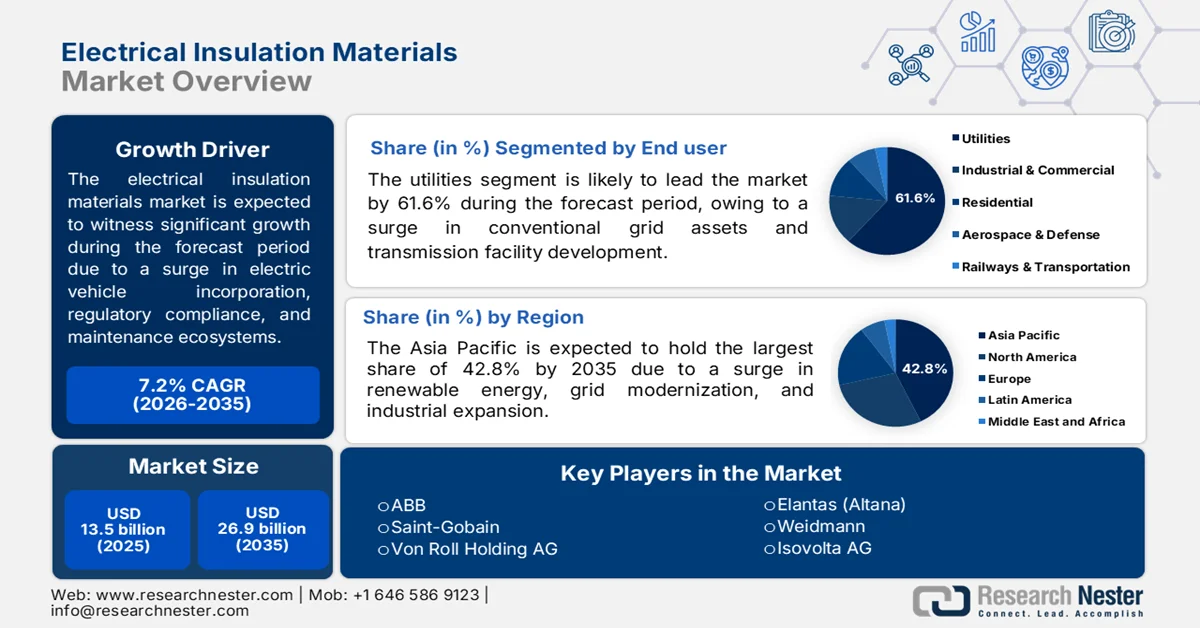

Electrical Insulation Materials Market size was valued at USD 13.5 billion in 2025 and is expected to reach USD 26.9 billion by the end of 2035, gradually mounting at a 7.2% CAGR during the forecast period, i.e., 2026-2035 In 2026, the industry size of electrical insulation materials is assessed at USD 14.4 billion.

The worldwide electrical insulation materials market is growing beyond traditional industrial forces, including grid modernization, electric vehicle adoption, regulatory compliance, demographic transition, a rise in predictive maintenance ecosystems, and underwriting standards. According to official statistics published by the Energy Transitions Commission in September 2024, in terms of net-zero scenarios, the overall length of grids is expected to grow by more than 50% by the end of 2050, demonstrating a USD 22.5 trillion investment. Besides, the International Energy Agency (IEA) demonstrated that in a grid-delay scenario, nations might miss the 58 Gt CO2 of cumulative emissions savings by the end of the same year. This is readily equivalent to worldwide power industrial carbon dioxide emissions from the past 4 years and nearly 430% of the remaining carbon budget for a 1.5 degrees Celsius scenario, thus fueling the market growth globally.

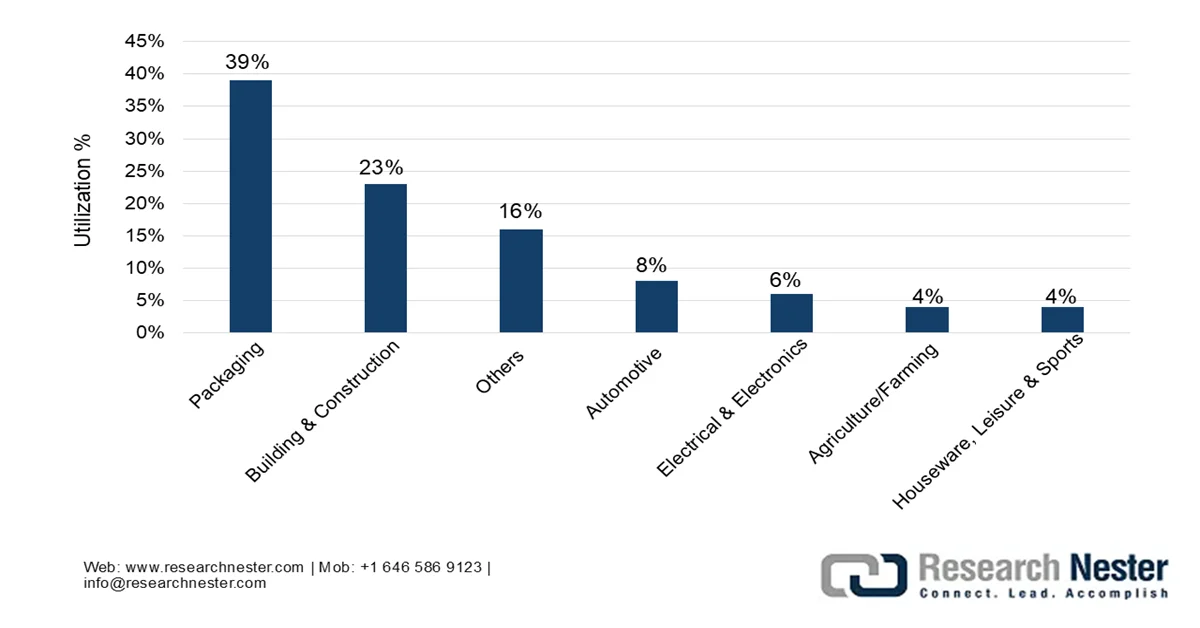

Furthermore, the workforce demographic transition in utilities, increased focus on insurance-based material specifications, and second-life polymer feedstocks from unrelated industries are a few trends that are also bolstering the market worldwide. According to official statistics published by NLM in June 2024, every year, more than 300 million tons of plastics are increasingly manufactured worldwide for consumers. In addition, the largest industry utilizing plastics is packaging, which accounts for roughly 40% of the overall plastic consumption globally, owing to the aspects of durability, lightweight, and an effective method of preservation. Besides, approximately 90.6% of plastics are usually based on fossil fuels, and other forms, such as mechanically recycled plastics, cater to 8.9%. Moreover, the increased plastic utilization by different industries has resulted in optimizing the polymer sustainability, which has readily emerged as a paramount objective for the overall market.

Plastic Utilization Across Different Industries for Polymer Sustainability, 2024

Source: NLM

Key Electrical Insulation Materials Market Insights Summary:

Regional Highlights:

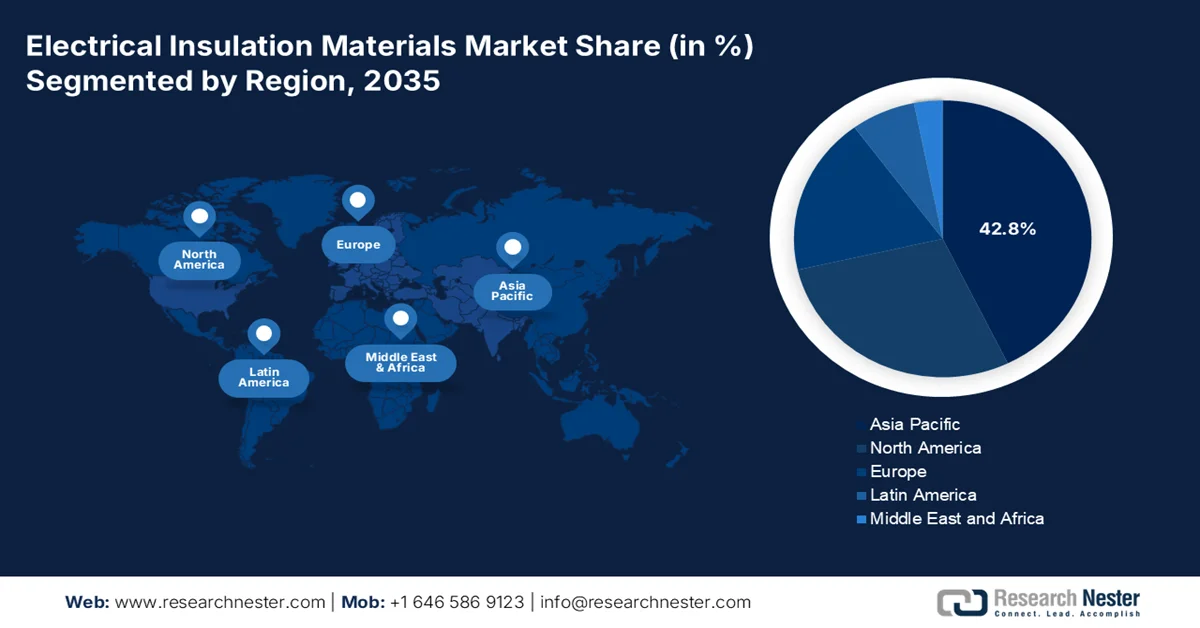

- The electrical insulation materials market in Asia Pacific is projected to command a 42.8% share by 2035, bolstered by accelerating renewable energy investments, rapid industrialization, grid modernization initiatives, and strong manufacturing capabilities

- Europe is anticipated to register the fastest growth in the market throughout 2026–2035, stimulated by renewable energy integration strategies, stringent environmental regulations, and expanding cross-border electrification projects

Segment Insights:

- The utilities segment is expected to secure a 61.6% share of the electrical insulation materials market by 2035, propelled by continuous upgrades of aging grid infrastructure and expanding transmission network investments

- The wires and cables sub-segment is anticipated to capture the second-largest share in the market during 2026–2035, catalyzed by surging demand for data transmission infrastructure and the expanding deployment of global subsea fiber-optic cable networks

Key Growth Trends:

- Data center liquid immersion cooling insulation

- Space-driven solar power transition

Major Challenges:

- Stringent and diverging regulatory compliance standards

- Technological obsolescence of legacy insulation systems

Key Players: DuPont, 3M, Hitachi, Nitto Denko, Toray, Siemens, ABB, Saint-Gobain, Von Roll Holding AG, Elantas, Weidmann, Isovolta AG, Krempel, Tesa SE, Röchling Group, Dr. Dietrich Müller GmbH, ITW Formex, Avery Dennison, Mica Manufacturing Co. Pvt. Ltd., Sichuan EM Technology, Clariant, TopBuild Corp., BASF.

Global Electrical Insulation Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.5 billion

- 2026 Market Size: USD 14.4 billion

- Projected Market Size: USD 26.9 billion by 2035

- Growth Forecasts: 7.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.8% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: South Korea, Vietnam, Brazil, Saudi Arabia, Indonesia

Last updated on : 13 May, 2026

Electrical Insulation Materials Market - Growth Drivers and Challenges

Growth Drivers

- Data center liquid immersion cooling insulation: The transition from air-cooled to liquid-immersed cooling across high-performance data centers has created specialized and new requirements for electrical insulation materials. Based on government estimates published by Congress in January 2026, the yearly energy utilization across data centers in the U.S. as of 2023 was approximately 176 TWh, which is roughly 4.4% of the domestic electricity consumption. Additionally, it has been predicted that the data center energy consumption can double or triple by the end of 2028, further contributing to almost 12% of domestic electricity utilization. Besides, a 100- megawatt domestic data center has the ability to consume water, which is equivalent to 2,600 households, ultimately leading to direct water consumption through different cooling approaches, thus bolstering the electrical insulation materials market globally.

- Space-driven solar power transition: Space-based solar power projects are increasingly driving specialized insulation requirements for severe environment power transmission, which is positively impacting the market. As stated in an article published by the Department of Energy in April 2026, laser solar satellites deliberately account for low startup expenses between USD 500 million and USD 1 billion. Meanwhile, microwave solar satellites comprise uninterrupted and steady transmission of power through clouds, rain, and other atmospheric conditions. Additionally, these offer 1 GW of upward energy to a terrestrial receiver, which is considered to be suitable for powering a large-scale location, thereby making it suitable for the market’s expansion.

- Desert solar farm corrosion mitigation: The aspect of utility-scale solar installations in arid, dust-prone environments, such as the Atacama Desert and Arabian Peninsula, faces a distinct insulation challenge. This includes abrasive dust infiltration combined with condensation-driven corrosion. Besides, unlike coastal or temperate installations, desert solar farms experience high daytime temperatures, low humidity, and sudden dew incidents at night, and condensation that results in accumulated dust, forming a conductive sludge that tracks across insulator surfaces and accelerates tracking and erosion. Moreover, standard hydrophobic silicone rubber insulators, effective in polluted industrial areas, degrade faster under this abrasive-condensation cycle because dust particles embed in the rubber surface, retaining moisture.

Challenges

- Stringent and diverging regulatory compliance standards: Manufacturers must simultaneously satisfy multiple, often contradictory, fire safety, environmental, and electrical performance regulations across different geographies. A material approved for utilization in Europe rail infrastructure may fail North America flame‑spread or smoke‑toxicity tests, forcing companies to maintain separate product portfolios and certification processes. The ongoing global transition away from halogenated flame retardants and certain per‑and polyfluoroalkyl substances adds another layer of complexity, as substitute materials require extensive requalification by original equipment manufacturers. Besides, regulatory bodies update their standards asynchronously, leaving manufacturers in a perpetual state of catching up rather than leading innovation, thus negatively impacting the electrical insulation materials market.

- Technological obsolescence of legacy insulation systems: A significant portion of existing electrical infrastructure, from power transformers to industrial motors, still relies on decades‑old insulation technologies that are ill‑suited for modern operating conditions. Moreover, as grids integrate intermittent renewables and EVs introduce ultra‑high‑voltage charging cycles, legacy materials, such as conventional kraft paper, oil‑impregnated systems, and standard thermoplastics, degrade faster than their original design life, raising the risk of premature failure and unplanned downtime. Therefore, retrofitting this installed base is technically complex and economically unattractive for asset owners, who prefer cheaper, immediate repairs over complete redesigns. However, continuing with outdated insulation increases maintenance frequency and reduces overall system reliability, which is causing a hindrance in the market.

Electrical Insulation Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.2% |

|

Base Year Market Size (2025) |

USD 13.5 billion |

|

Forecast Year Market Size (2035) |

USD 26.9 billion |

|

Regional Scope |

|

Electrical Insulation Materials Market Segmentation:

End user Segment Analysis

Among end user, the utilities segment is anticipated to capture the largest share, at 61.6%, in the electrical insulation materials market by the end of 2035. The segment’s upliftment is primarily driven by the continuous operation of aging grid assets and the simultaneous build‑out of new transmission infrastructure. Power companies rely on insulation to maintain separation between conductive components in transformers, switchgears, circuit breakers, and underground cables, where even minor material degradation can trigger cascading failures. The operational environment for utilities has grown more demanding as renewable energy sources introduce variable power flows and higher transient voltages, placing additional stress on insulation systems originally designed for stable, one‑way electricity delivery.

Application Segment Analysis

The wires and cables sub-segment, part of the application segment, is projected to account for the second-highest share in the market during the forecast period. The sub-segment’s growth is effectively fueled by its importance as a crucial backbone of modernized infrastructure that enables the distribution, transmission, and generation of data and electricity across transportation, industrial, and residential industries. Besides, data is considered the centralized resource in digital societies, with military communication, private calls, and business transactions highly dependent on the Internet. As per an article published by Technological Forecasting and Social Change in June 2025, fiber-optic subsea data cables presently offer almost 99% of intercontinental data traffic. In addition, more than 550 active subsea data cables form a suitable network for global telecommunication, thereby driving the sub-segment’s growth globally.

Material Type Segment Analysis

By the end of the stipulated timeline, the thermoplastics segment, part of the material type, is expected to garner the third-highest share in the market. The segment’s development is highly attributed to its importance in modernizing manufacturing, owing to its ability to be reshaped and remelted, providing increased recyclability, versatility, and cost-efficiency. As per a data report published by the International Institute for Sustainable Development in July 2025, an increase in thermoplastics has been predicted by an estimated 70%, from almost 350 million to 590 million tons by the end of 2050. Besides, thermoplastics comprise the category of plastics from which the majority of plastic products, such as single-use plastics, are made with polyethylene terephthalate, polyvinyl chloride, polystyrene, polypropylene, high-density polyethylene, and low-density polyethylene, thus proliferating the segment’s upliftment.

Our in-depth analysis of the electrical insulation materials market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Application |

|

|

Material Type |

|

|

Product Form |

|

|

Functionality |

|

|

Voltage Level |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Electrical Insulation Materials Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the electrical insulation materials market is anticipated to grab the largest share of 42.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to the unparalleled industrial expansion, renewable energy deployment, grid modernization, and the presence of manufacturing powerhouses. According to official statistics published by the ADB Organization in April 2025, there has been a growth of clean energy investment in the region by over 900%, which reached USD 729.4 billion as of 2023, further comprising nearly 45% of worldwide investment. Besides, China catered to a majority of this investment by collaborating with India and 7 other countries, wherein renewables surpassed 75% of the newest national energy capacity addition in 2022. Therefore, with all these developments, the market is gradually expanding in the overall region.

The electrical insulation materials market in China is growing significantly, owing to the existence of the largest manufacturing base for electrical equipment, robust renewable energy targets, readily prioritizing chemical and petrochemical industries, and the production of sustainable aviation fuel and green methanol. As stated in an article published by the State Council Information Office in September 2025, the country has aimed to achieve an average yearly increase of more than 5% in the added value of the chemical and petrochemical sectors by the end of 2026. This objective comprises a rebound in economic returns that marked an upsurge in technological, scientific, and industrial advancement, along with measurable reductions in both carbon emissions and pollution, thereby positively impacting the market upliftment in the country.

The aspects of revitalizing the semiconductor industry based on government strategies, the presence of an advanced electronics ecosystem, and the domestic supply dynamics for industrial equipment, automobiles, and electronics are certain factors that are proliferating the electrical insulation materials market in Japan. Besides, the domestic electrical insulation materials industry was worth USD 16.4 billion as of 2025, which is projected to be valued at USD 17.8 billion by the end of 2026. Additionally, the industry is poised to reach USD 36.7 billion, along with an 8.4% growth rate by the end of 2035. Moreover, as per the November 2025 ITA article, the semiconductor industry in the country significantly reached USD 51 billion in 2025, owing to steady growth and increased investments in memory and logic integrated circuits, thus bolstering the market exposure.

Japan Semiconductor Industrial Size Analysis, 2022-2025

|

Year |

Market Size (USD Billion) |

Year-on-Year Growth |

Exchange Rate |

|

2022 |

48.1 |

10.2% |

131.4 |

|

2023 |

48.7 |

-2.9% |

140.4 |

|

2024 |

47.4 |

1.4% |

150.5 |

|

2025 |

51.8 |

9.4% |

148.9 |

Source: ITA

Europe Market Insights

Europe in the electrical insulation materials market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by modernization approaches for renewable energy integration, strict environmental regulations across countries, the zero-pollution objective, and an increase in cross-border projects. According to official data published by the Europe Commission in 2026, the zero-pollution vision for 2050 is focused on improving air quality to lower the number of premature deaths caused by air pollution by 55%. This is followed by optimizing water quality by reducing plastic and waste litter at sea by 50% and microplastics in the environment by 30%. The objective also focuses on enhancing soil quality by lowering nutrient losses and chemical pesticide utilization by 50%, thereby making it suitable for boosting the market development in the region.

The market in Germany is gaining increased traction, owing to the presence of the sophisticated chemical industry, the manufacturing facility for power equipment, industrial automation, and automotive, along with strong federal policy and the grid modernization program. As stated in an article published by the Green Carbon in March 2024, the German Nova Institute demonstrated the production of 373 million tons of plastic from fossil raw materials, while the Plastics Europe industry association noted 391 million tons of plastic production. Meanwhile, the Organization of Economic Cooperation and Development predicted roughly 600 million tons of plastic to be produced by the end of 2060. Therefore, with this increase in the production process, there is a huge growth opportunity for the market in the overall country.

The unprecedented growth momentum, the ambitious energy transition through wind and solar generation, readily prioritizing grid modernization, an expansion in tourism infrastructure, increased focus on regionally funded research initiatives, and energy transition policies are a few trends that are responsible for driving the electrical insulation materials market in Greece. As per an article published by the ITA in May 2024, power produced by hydroelectric and renewable facilities accounts for 57% of the country’s energy mix, demonstrating an 8.5% surge from 2022. Besides, the domestic government submitted the national plan for energy and climate to the Europe Commission as of 2023, which has set ambitious renewable targets that are to be achieved by the end of 2030, thereby denoting an optimistic outlook for the market’s development and expansion.

North America Market Insights

North America in the electrical insulation materials market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is significantly fueled by the modernization of aging power grids, an increase in the electrification of transportation, and an expansion in renewable energy infrastructure across Canada and the U.S. According to official statistics published by the Center for Sustainable Systems in 2026, 82% of energy in the U.S. derives from fossil fuels, which is followed by 8.7% from nuclear, and 9.1% from renewable sources. In addition, solar and wind are the fastest-growing renewable sources, contributing less than 3% of overall energy utilization in the country. Besides, the country comprises approximately 463,400 TWh of renewable energy technical potential, which is more than 100 times the electricity, thus driving the market growth in the region.

Renewable Energy Utilization in the U.S., 2013-2023

|

Year |

Biomass (Quads) |

Hydroelectricity (Quads) |

Wind (Quads) |

Solar (Quads) |

Geothermal (Quads) |

|

2013 |

4.8, 73.8% |

0.9, 13.9% |

0.5, 8.7% |

0.1, 1.8% |

0.1, 1.8% |

|

2014 |

5.0, 73.8% |

0.8, 13.0% |

0.6, 9.1% |

0.1, 2.4% |

0.1, 1.7% |

|

2015 |

5.0, 73.4% |

0.8, 12.4% |

0.6, 9.5% |

0.2, 2.9% |

0.1, 1.7% |

|

2016 |

5.0, 71.1% |

0.9, 12.8% |

0.7, 10.9% |

0.2, 3.5% |

0.1, 1.7% |

|

2017 |

5.0, 68.3% |

1.0, 13.9% |

0.8, 11.8% |

0.3, 4.5% |

0.1, 1.6% |

|

2018 |

5.1, 67.7% |

1.0, 13.2% |

0.9, 12.3% |

0.3, 5.1% |

0.1, 1.6% |

|

2019 |

5.0, 66.6% |

0.9, 12.9% |

1.0, 13.3% |

0.4, 5.7% |

0.1, 1.5% |

|

2020 |

4.5, 62.3% |

0.9, 13.3% |

1.1, 15.8% |

0.5, 7.0% |

0.1, 1.6% |

|

2021 |

4.7, 62.1% |

0.8, 11.2% |

1.2, 16.9% |

0.6, 8.2% |

0.1, 1.5% |

|

2022 |

4.8, 60.0% |

0.8, 10.7% |

1.4, 18.3% |

0.7, 9.4% |

0.1, 1.5% |

|

2023 |

4.9, 60.4% |

0.8, 9.8% |

1.4, 17.6% |

0.8, 10.6% |

0.1, 1.5% |

Source: Center for Sustainable Systems

The electrical insulation materials market in the U.S. is gaining increased exposure, owing to federal grid modernization funding, an increase in commercial fleet electrification, and the occurrence of extreme weather incidents. As stated in an article published by the Department of Energy in March 2026, the Office of Electricity (OE) proclaimed an estimated USD 1.9 billion funding opportunity to accelerate the upgradation of the country’s power grid. This particular investment is poised to cater to the rise in electricity demand as well as resource adequacy requirements, while diminishing electricity expenses for regional businesses and households. Based on this, different projects have been selected through the Speed to Power through Accelerated Reconductoring and other Key Advanced Transmission Technology Upgrades (SPARK), thus proliferating the market growth.

The presence of distinct national priorities centering on renewable energy extension and electrification mandates, an expansion in transmission facilities, government strategies, the growing need for an electricity network, and the Pan-Canada Framework on Clean Growth and Climate Change are certain trends that are fueling the market in Canada. As per an article published by Natural Resources Canada in August 2025, the country’s clean energy gross domestic product (GDP) is expected to reach USD 107 billion, which is highly driven by USD 58 billion in yearly investments by the end of 2030 and over 600,000 employment opportunities. Besides, between 140 and 190 GW of additional clean electricity generating capacity are predicted to be required by the end of 2050, thus creating a huge growth opportunity for the market.

Key Electrical Insulation Materials Market Players:

- DuPont (U.S.)

- 3M (U.S.)

- Hitachi (Japan)

- Nitto Denko (Japan)

- Toray (Japan)

- Siemens (Germany)

- ABB (Switzerland)

- Saint-Gobain (France)

- Von Roll Holding AG (Switzerland)

- Elantas (Altana) (Germany)

- Weidmann (Switzerland)

- Isovolta AG (Austria)

- Krempel (Germany)

- Tesa SE (Germany)

- Röchling Group (Germany)

- Dr. Dietrich Müller GmbH (Germany)

- ITW Formex (U.S.)

- Avery Dennison (U.S.)

- Mica Manufacturing Co. Pvt. Ltd. (India)

- Sichuan EM Technology (China)

- Clariant (Switzerland)

- TopBuild Corp. (U.S.)

- BASF (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- DuPont is recognized as a cornerstone innovator in high-performance polymer insulation, particularly through its Nomex and Kapton brands, which set industry benchmarks for thermal and dielectric strength. The company continuously focuses on developing next-generation materials that address the stringent demands of electric vehicle motors and high-voltage transformers.

- 3M leverages its deep expertise in fluoropolymer and ceramic-filled technologies to produce flexible insulation solutions for demanding aerospace and industrial cable applications. The company emphasizes reliability and long-term aging performance, making its tapes and embedded materials a preferred specification for critical infrastructure projects.

- Hitachi integrates its insulation materials division with its broader power systems' expertise, focusing on advanced epoxy resins and coil insulation for heavy-duty rotating machinery. The company prioritizes compatibility with high-efficiency transformer designs to support grid modernization and renewable energy integration.

- Nitto Denko specializes in thin-film and adhesive-based insulation products, maintaining a strong focus on ultra-thin electrical tapes for compact consumer electronics and automotive sensors. The company invests heavily in thermal dissipation technologies to ensure insulation integrity in densely packed electronic control units.

- Toray applies its advanced polymer engineering capabilities to produce high-grade polypropylene and polyester films for power capacitor and flexible laminate applications. The company focuses on achieving exceptional electrical purity and dimensional stability to meet the rigorous standards of signal transmission and energy storage systems.

Here is a list of key players operating in the global market:

The electrical insulation materials market is characterized by a mature, fragmented, and competitive landscape dominated by diversified chemical and industrial conglomerates alongside specialized insulation manufacturers. The first tier of competition includes U.S.-based giants, including DuPont and 3M, Europe powerhouses such as Siemens and ABB, and Japan-specific leaders, including Hitachi and Nitto Denko. These players leverage extensive R&D capabilities, global distribution networks, and strong brand recognition to maintain their market positions. Besides, in August 2025, Hitachi Energy expanded its India-based transformer insulation production by aiming to double its capacity for pressboards. Based on this expansion, the factory in Mysore is projected to emerge as an ultra-low carbon pressboard production facility by the end of 2027, with the absence of fossil fuel utilization for processing heat generation, thus boosting the electrical insulation materials industry globally.

Corporate Landscape of the Market:

Recent Developments

- In October 2025, Clariant completed its USD 127.7 million investment in the Daya Bay facility, with the second production line fully operational, which further strengthened its ability to cater to the growing demand for increased sustainable flame-retardant solutions, particularly in Asia and other nations.

- In October 2025, TopBuild Corp. successfully acquired Specialty Products and Insulation for USD 1 billion, which was suitable in positioning the combined organization by providing consumers with advanced and high-quality solutions.

- In May 2024, BASF significantly opted for a sustainable glass fiber in its Ultramid® A&B portfolio by setting up the ambitious objective of diminishing its Scope 3.1 emissions by 15% by the end of 2030 and achieving net zero by the end of 2050.

- Report ID: 8560

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.