Pipe Insulation Market Outlook:

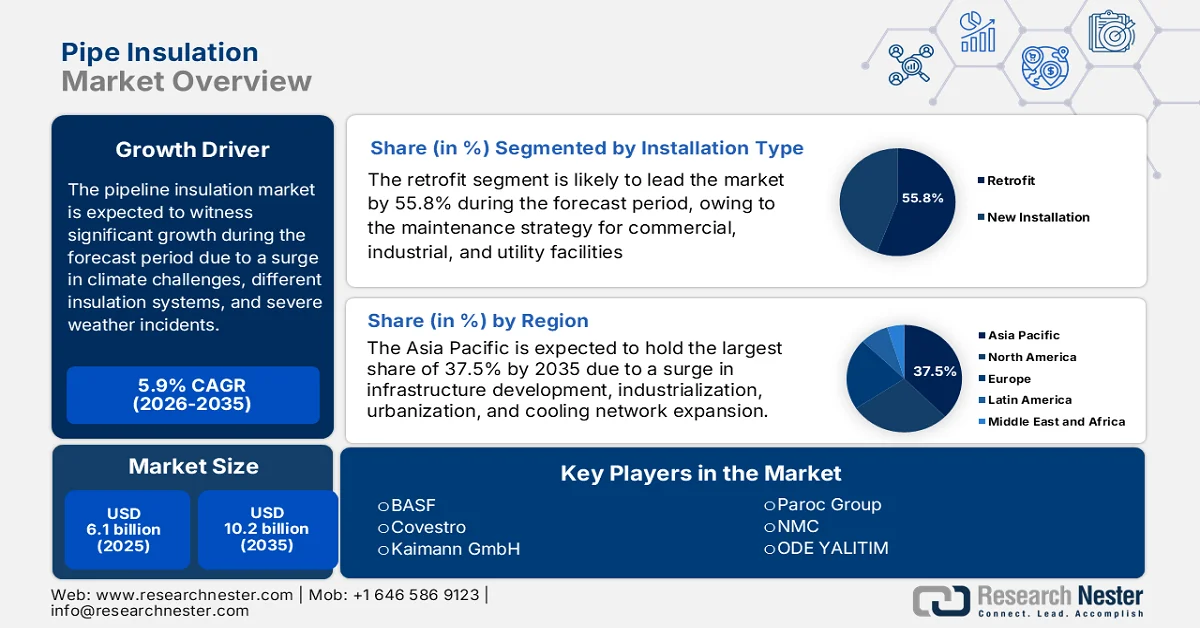

Pipe Insulation Market size was valued at over USD 6.1 billion in 2025 and is expected to reach USD 10.2 billion by the end of 2035, growing at a CAGR of 5.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of pipe insulation is estimated at USD 6.4 billion.

The worldwide pipe insulation market is significantly expanding, owing to interconnected factors, including an increase in extreme weather incidents, climate-based risks, labor market dynamics for product development, modular insulation systems, and the presence of consolidation in the industrial and construction sectors. According to official statistics published by the NIA Organization in January 2024, the global demand for insulation is predicted to rise by 1.5% every year to USD 59.2 billion by the end of 2026, along with an increase in the volume demand offset by reduced expenses. In addition, the volume demand for modular insulation is also predicted to grow by 2.7% per year and reach 29.6 million metric tons by the end of the same year. This growth is highly driven by increased manufacturing activities, suitable efforts in Europe, along with a rise in the production of HVAC equipment, which is uplifting the market growth.

Furthermore, the digital integration, the adoption of smart insulation systems, and the presence of low-carbon and bio-based insulation materials are certain trends that are fueling the pipe insulation market demand globally. As per an article published by NLM in May 2025, the aspect of implementing a combination of low-carbon expenses among 23.7% emitters has the capability of diminishing international carbon footprints by 10.4 gigatons of equivalent carbon dioxide, which is 40.1% of the household consumption-specific emissions. Besides, the low-carbon consumption pattern modifications are deliberately related to services and mobility that effectively contributed to 10.2% and 11.8% of emission reductions. Moreover, a rebound effect from re-spending income savings from lifestyle modifications offsets the projected carbon savings by 6.5% to 45.8%, thereby denoting an optimistic outlook for the market expansion.

Key Pipe Insulation Market Insights Summary:

Regional Highlights:

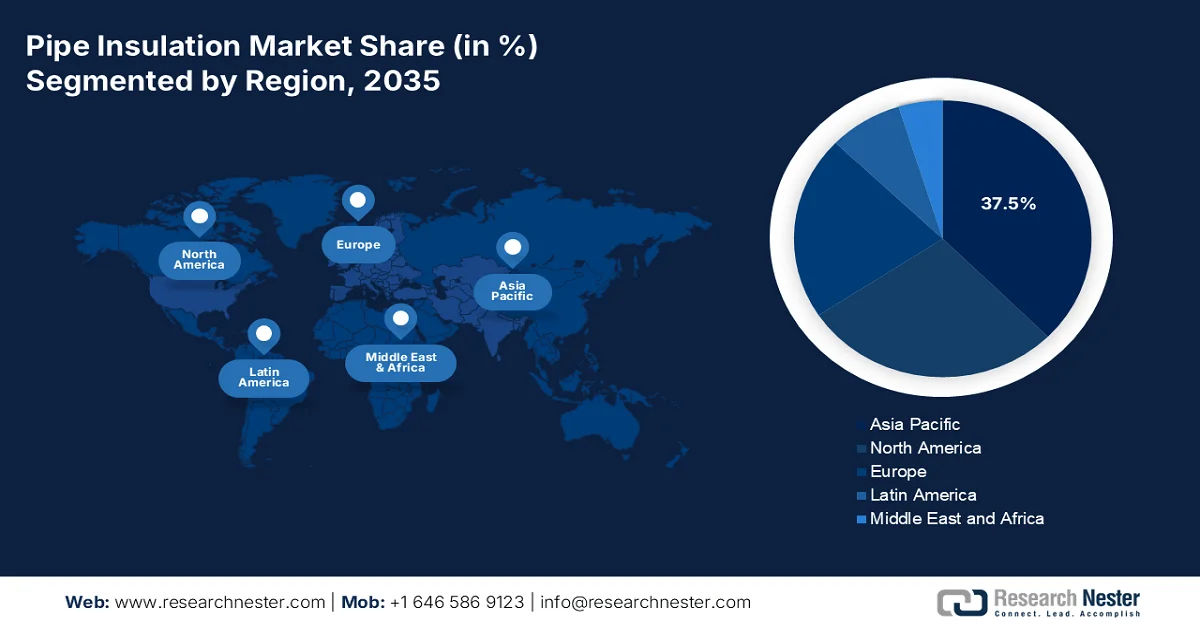

- Asia Pacific pipe insulation market is projected to command a 37.5% share by 2035, bolstered by rapid urbanization, industrial expansion, and rising adoption of energy-efficient district cooling systems.

- Europe is anticipated to witness the fastest growth through 2035, fueled by decarbonization initiatives and expansion of district heating infrastructure.

Segment Insights:

- The retrofit segment in the pipe insulation market is expected to capture a 55.8% share by 2035, supported by increasing upgrades and maintenance activities across utility and industrial applications.

- The industrial segment is poised to secure the second-largest share by 2035, reinforced by its critical role across oil and gas, chemical processing, and power generation sectors.

Key Growth Trends:

- Expansion in LNG infrastructure

- Focus on corrosion under insulation prevention

Major Challenges

- Volatility in raw material prices

- Stringent and evolving regulatory compliance requirements

Key Players: Owens Corning (U.S.), Johns Manville (U.S.), Knauf Insulation (U.S.), ITW (Illinois Tool Works) (U.S.), Armacell (Germany), Rockwool (Denmark), Kingspan (Ireland), K-flex (Italy), Saint-Gobain (France), BASF (Germany), Covestro (Germany), Kaimann GmbH (Germany), Paroc Group (Finland), NMC (Belgium), ODE YALITIM (Turkey), Wincell (China), Huamei (China), Dyplast Products (U.S.), Aeroflex USA, Inc (U.S.), PERMA-PIPE International Holdings, Inc (U.S.), STATS Group (UK), EPOMS Sdn Bhd (Malaysia), Tenaris (Luxembourg), Oatey Co. (U.S.).

Global Pipe Insulation Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.1 billion

- 2026 Market Size: USD 6.4 billion

- Projected Market Size: USD 10.2 billion by 2035

- Growth Forecasts: 5.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (37.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 25 March, 2026

Pipe Insulation Market - Growth Drivers and Challenges

Growth Drivers

- Expansion in LNG infrastructure: The unprecedented worldwide expansion of liquefied natural gas (LNG) terminal infrastructure is readily propelling the pipe insulation market. According to official statistics published by the IEA Organization in January 2026, there has been an increase in the international LNG supply by nearly 7% as of 2025, with almost three-quarters of the upliftment. Additionally, the investment momentum in the global LNG supply remained deliberately strong as of 2025, with over 90 billion cubic meters every year of LNG liquefaction capacity successfully reaching a finalized investment decision. In this regard, the U.S. catered to the latest investment wave, constituting for more than 80 bcm of accepted yearly capacity, thus denoting a huge growth opportunity for the pipe insulation market development.

- Focus on corrosion under insulation prevention: The existence of a strict regulatory framework for addressing corrosion under insulation has significantly emerged as the most crucial growth driver for the pipe insulation market. As stated in an article published by America Coating Association in 2026, the chemical transformation, as part of the EonCoat formulation, constitutes 100% solids, along with non-toxic, water-based, non-flammable, odourless, and comprises zero volatile organic compounds. This can readily be applied at temperatures ranging between 40 and 120 degrees Fahrenheit, along with humidities accounting for 30% to 95%, at a minimum thickness of 20 mils. Therefore, with the implementation of this particular formulation, the market is gradually gaining exposure.

- Modernization in urban underground infrastructure: The transformative factor that is reshaping the pipe insulation market is the unprecedented worldwide push towards urban underground infrastructure modernization, along with the increased adoption of trenchless installation technologies. As stated in an article published by Engineering in February 2025, the construction of underground spaces in buildings is considered one of the largest carbon emitters within the overall urban underground space (UUS), significantly releasing a considerable 547.2 metric tons. Besides, the geothermal carbon sequestration, which is a significant element of the UUS system, offered an impressive and unexpected contribution, effectively sequestering 70 metric tons of carbon, thus proliferating the market development.

Challenges

- Volatility in raw material prices: The pipe insulation market is highly susceptible to fluctuations in raw material costs, creating significant challenges for manufacturers in terms of pricing stability, profit margin management, and supply chain reliability. The primary materials used in pipe insulation production, including fiberglass, mineral wool, elastomeric foams, polyurethane, and aerogels, are derived from energy-intensive manufacturing processes and petrochemical feedstocks that experience substantial price volatility driven by global energy markets, geopolitical events, and supply-demand imbalances. This volatility introduces considerable uncertainty into production planning and financial forecasting, forcing manufacturers to constantly reassess their cost structures and pricing strategies in response to rapidly changing input costs.

- Stringent and evolving regulatory compliance requirements: Manufacturers and installers in the pipe insulation market need to navigate an increasingly complex and stringent regulatory landscape that governs material composition, fire safety standards, environmental impact, and installation practices. Compliance with these multifaceted regulations requires substantial investments in research and development, testing and certification, and ongoing monitoring of regulatory changes across multiple jurisdictions. The challenge is compounded for global manufacturers, intended to satisfy varying requirements in each market they serve, from Europe-based directives on construction products and chemical safety to North America-based building codes and fire testing standards, thus causing a hindrance in the pipe insulation market growth.

Pipe Insulation Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.9% |

|

Base Year Market Size (2025) |

USD 6.1 billion |

|

Forecast Year Market Size (2035) |

USD 10.2 billion |

|

Regional Scope |

|

Pipe Insulation Market Segmentation:

Installation Type Segment Analysis

The retrofit segment in the pipe insulation market is anticipated to garner the largest share of 55.8% by the end of 2035. The segment’s upliftment is primarily attributed to the upgraded and maintenance strategy for providing suitable advantages for utility, commercial, and industrial applications. According to the official statistics published by the MDPI in February 2026, the aspect of hydrogen blending into natural gas grids is eventually possible in achieving conventional levels of almost 20% by volume. This particular activity constitutes direct implications for pipeline operations, since natural gas is estimated to be three times more energy-intensive than hydrogen. This denotes that 100% hydrogen tends to drop at constant pressure, leading to 15% to 20% low energy transmission capacity and further demanding high flow velocities, which is positively uplifting the segment growth.

End use Industry Segment Analysis

During the forecast period, the industrial segment, which is part of the end use industry, is projected to hold the second-largest share in the pipe insulation market. The segment’s growth is highly fueled by encompassing critical industries such as oil and gas, chemical processing, power generation, and petrochemical manufacturing. Within this segment, pipe insulation serves as a non-negotiable technical requirement rather than an optional building component, driven by the imperative to maintain precise process temperatures, ensure operational safety, and optimize energy efficiency across complex piping networks. Besides, the oil and gas industry, a dominant sub-segment, relies heavily on insulated piping systems for upstream exploration in harsh environments, midstream transportation through extensive pipeline networks, and downstream refining processes where thermal insulation prevents heat loss, maintains flow efficiency, and prevents costly issues such as wax formation or hydrate blockages in cold climates.

Material Type Segment Analysis

The inorganic segment, part of the material type, is expected to account for the third-largest share in the pipe insulation market by the end of the stipulated timeline. The segment’s development is highly propelled by its high-temperature stability, durability, corrosion resistance, and fire resistance. Additionally, this segment includes fiberglass, mineral wool, calcium silicate, cellular glass, and aerogels, each distinguished by its inherent resistance to high temperatures, fire, moisture, and chemical degradation. Besides, fiberglass dominates this segment as the most widely utilized inorganic insulation material, prized for its exceptional thermal performance, cost-effectiveness, and versatility across both commercial and industrial applications, with glass fibers typically comprising sand combined with recycled glass content.

Our in-depth analysis of the pipe insulation market includes the following segments:

|

Segment |

Subsegments |

|

|

|

End use Industry |

|

|

Material Type |

|

|

Product Form |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Pipe Insulation Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the pipe insulation market is anticipated to garner the highest share of 37.5% by the end of 2035. The market’s upliftment in the region is primarily attributed to unprecedented urbanization, increased industrialization, huge infrastructure development across emerging economies, expansion of district cooling and heating networks, and the proliferation of green building mandates. According to official statistics published by the DBDH Organization in August 2024, direct cooling systems are well-suited for urban areas and cities with increased cooling demand in the region, with benefits including almost 50% low energy consumption and nearly 30% reduced installed cooling capacity. In addition, the system also caters to combating the urban heat island effect, along with high availability and long-term lifespan, which is positively impacting the market growth.

The pipe insulation market in China is growing significantly, owing to huge infrastructure investment, strong energy efficiency mandates, the enhancement of the industrial chemical sector, the government’s commitment to diminishing carbon intensity, high-performance thermal insulation across industrial, commercial, and residential projects, and suitable modernization in north provinces. As stated in an article published by NLM in March 2025, the carbon emissions and energy consumption of the construction industry and other industries in the country accounted for 36% of the worldwide energy consumption. Moreover, despite the technological advancements in developing thermal management, the proportion of energy consumption is continuously increasing and is eventually breaking through 40%, thus denoting a huge growth opportunity for the market in the country.

The aspects of infrastructure development, increased urbanization, the government’s robust push toward energy efficiency under the domestic Smart Cities Mission, expansion in petrochemical industries and chemical processing, and extension in urban centers are certain factors that are bolstering the pipe insulation market in India. As per an article published by the India Investment Grid in October 2025, the petrochemical sector in the country is presently on a trajectory path to effectively reach an outstanding 35 million tons by the end of 2027 and 2028. In addition, major petrochemical production amounted to 9,319,000 metric tons, along with constituting a 3.7% growth rate. Besides, there has been a surge in petrochemical exports by an outstanding 106% as of 2022, deliberately underscoring the country’s expansion on the global petrochemical industry.

Europe Market Insights

Europe in the pipe insulation market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is primarily propelled by commoditized building materials, the decarbonization agenda, a rapid expansion in the fourth-generation district heating networks, and aging industrial infrastructure. According to official statistics published by the IEA Organization in July 2023, the region effectively provided USD 464 million in April 2023 as support for the Czech green district heating scheme. Simultaneously, in March 2023, the Energy Security Bill in the UK unveiled heat networks regulations to ensure heat zoning. Regarding this, the Climate Change Committee has estimated that almost 18% of heat consumption in the country, which is poised to be supplied through heat networks by the end of 2050, thus fueling the market development.

The pipe insulation market in Germany is gaining increased traction, owing to the convergence of strict energy-efficient regulations, expanded district heating infrastructure, and upscaling of the industrial chemical sector. As per an article published by the Institute for Market Integration and Economic Policy in June 2023, the chemical industry in the country accounts for the third-largest industrial sector, with a direct gross value added of USD 38.2 billion and an overall gross value added of USD 81.0 billion. Therefore, this further caters to 3.6% of manufacturing as well as 2.3% of the domestic gross value added. Moreover, the industry also provides suitable employment opportunities for 1.7 million citizens in the country, with an employment multiplier of 3.6. Therefore, with such developments in the industry, the market is gradually expanding in the overall country.

The unique combination of climate targets, early adoption of smart infrastructure technologies, substantial resources for industrial decarbonization, massive transformation toward green hydrogen production, carbon capture infrastructure, bio-based chemicals, and suitable industrial developments are fueling the pipe insulation market in the Netherlands. As stated in an article published by the Green Hydrogen Organization in 2026, the 2022-2025 National Strategy has developed the need for green hydrogen and regional infrastructure, which has scaled the installed electrolyzer capacity to 500 MW as of 2025. Likewise, between 2026 and 2030, the massive upscaling of electrolyzer capacity is projected to reach 4 GW by the end of 2030, along with denoting an expansion of infrastructure and storage, thereby making it suitable for driving the market in the overall country.

North America Market Insights

North America in the pipe insulation market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by industrial decarbonization mandates, large-scale infrastructure modernization, strict energy regulations, and significant transformations across power generation, oil and gas, and chemical sectors. According to official statistics published by the Energy Innovation Organization in October 2022, industrial facilities in the U.S. utilize low-temperature heat of almost 165 degrees Celsius in different manufacturing processes, accounting for an estimated 35% of industrial process heat demand. Besides, low-temperature industrial heating produced 171 million metric tons of carbon dioxide, which caters to 3.5% of overall domestic energy-based carbon dioxide emissions. This is significantly equivalent to the yearly emission from 37 million gasoline-specific cars, along with 22 million homes or 430 natural gas-fired power facilities, which is positively impacting the market growth.

The pipe insulation market in the U.S. is gaining increased exposure, owing to the escalating energy expenses and operational savings imperative, strict energy efficiency regulations and building codes, federal programs and public and private partnerships, expansion of energy and industrial infrastructure, along with the growing awareness of sustainability goals and environmental impact. Based on government estimates published by the EIA in August 2024, the energy expenditure as of 2022 in the country increased from 22% to over USD 1.7 trillion. This resulted in increased petroleum prices for transportation as well as natural gas expenses. Moreover, the domestic inflation-based energy expenditures per capita totaled USD 5,200, with Alaska accounting for the highest per-capita energy spending at USD 13,100, which is further followed by USD 11,200 in Wyoming, thus driving the market expansion.

The presence of clean economy investment tax credits, federal decarbonization mandates and net-zero targets, major industrial project investments, expansion of district energy systems and green building initiatives, as well as critical minerals strategy and manufacturing support, are factors boosting the pipe insulation market in Canada. As stated in an article published by the Government of Canada in March 2026, the country’s greenhouse gas emissions accounted for 694 metric tons of carbon dioxide, denoting a decrease of 65 metric tons, which is 8.5%. Besides, the emissions intensity for the total domestic economy has been continuously declining since 2023 by 45%. This particular decline is highly attributed to factors, including an increase in efficiency, modernization in industrial processes, structural modifications in the economy, and fuel switching, which is positively impacting the market growth.

Key Pipe Insulation Market Players:

- Owens Corning (U.S.)

- Johns Manville (U.S.)

- Knauf Insulation (U.S.)

- ITW (Illinois Tool Works) (U.S.)

- Armacell (Germany)

- Rockwool (Denmark)

- Kingspan (Ireland)

- K-flex (Italy)

- Saint-Gobain (France)

- BASF (Germany)

- Covestro (Germany)

- Kaimann GmbH (Germany)

- Paroc Group (Finland)

- NMC (Belgium)

- ODE YALITIM (Turkey)

- Wincell (China)

- Huamei (China)

- Dyplast Products (U.S.)

- Aeroflex USA, Inc (U.S.)

- PERMA-PIPE International Holdings, Inc (U.S.)

- STATS Group (UK)

- EPOMS Sdn Bhd (Malaysia)

- Tenaris (Luxembourg)

- Oatey Co. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Owens Corning is a prominent player in the fiberglass pipe insulation sector, leveraging its strong brand recognition and extensive distribution network to serve both commercial and industrial applications. The company focuses on developing innovative insulation solutions that enhance energy efficiency and meet evolving building code requirements across North America.

- Johns Manville is a leading manufacturer of fiberglass and mineral wool pipe insulation, known for its commitment to product quality and technical expertise. The company strategically emphasizes sustainable manufacturing practices and provides comprehensive insulation systems designed for demanding industrial and mechanical specifications.

- Knauf Insulation has established a strong presence in the pipe insulation market through its focus on sustainability and circular economy principles. The company invests significantly in advanced manufacturing technologies to produce high-performance insulation materials that address both thermal efficiency and acoustic control requirements.

- ITW (Illinois Tool Works) offers specialized pipe insulation solutions that integrate with its broader portfolio of construction products and fastening systems. The company's decentralized operational structure enables it to maintain close customer relationships and respond effectively to regional market demands for mechanical insulation.

- Armacell is a global leader in flexible foam insulation for mechanical equipment, renowned for its innovative elastomeric products that provide superior condensation control and energy savings. The company maintains a strong focus on developing sustainable insulation technologies and has established manufacturing facilities across multiple continents to serve diverse industrial and HVAC applications.

Here is a list of key players operating in the global market:

The global pipe insulation market is moderately consolidated, with the top five manufacturers, including Owens Corning, Armacell, Johns Manville, Rockwool, and Knauf Insulation, accounting for the majority of the global market share. Besides, leading players are pursuing strategic initiatives focused on product innovation and sustainability, with major investments in eco-friendly materials and manufacturing processes to comply with increasingly stringent global energy efficiency regulations. Companies are expanding their geographic footprint through strategic acquisitions and facility expansions, particularly in the high-growth Asia Pacific. For instance, in January 2023, Perma-Pipe International Holdings, Inc. effectively entered into a joint venture with Gulf Insulation Group in Saudi Arabia for providing pre-insulated piping systems, internal and external fusion bonded epoxy, piping fabrication, and external fusion bonded epoxy, as well as three-layer coating services, thus fueling the pipe insulation industry.

Corporate Landscape of the Pipe Insulation Market:

Recent Developments

- In April 2025, STATS Group and EPOMS Sdn Bhd successfully secured a 3-year pipeline isolation contract, further including 1 year option, with a major Malaysia-based oil and gas operator for covering offshore and onshore pipelines located in Sabah, Sarawak, and Peninsular Malaysia.

- In November 2023, Tenaris significantly acquired Mattr’s pipe coating business unit for USD 182.6 million, which includes an approximate working capital and an additional USD 16.9 million in cash, along with achieving regulatory approvals in Norway and Mexico.

- In August 2023, Oatey Co. acquired Lansas B.V.for expanding its footprint in Europe-based waterworks industry by incorporating Lansas’ outstanding employees, innovative technologies, and the manufacturing facility.

- Report ID: 8471

- Published Date: Mar 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Pipe Insulation Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.