Carbon Fiber Composite Materials Market Outlook:

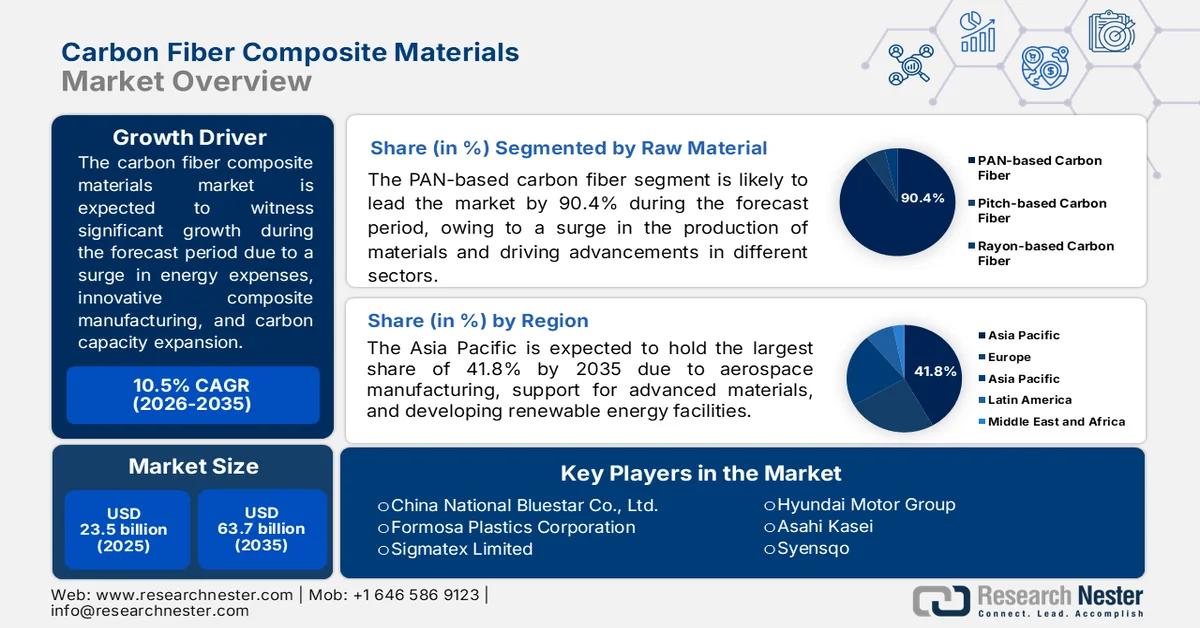

Carbon Fiber Composite Materials Market size was valued at USD 23.5 billion in 2025 and is projected to reach USD 63.7 billion by the end of 2035, registering around 10.5% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of carbon fiber composite materials is evaluated at USD 25.9 billion.

The worldwide carbon fiber composite materials market is being increasingly reshaped due to geopolitical realignment, the tariff framework, sourcing strategies, energy cost inflation, regulatory dynamics, waste reduction, advanced composite manufacturing, and carbon material capacity expansion. According to official statistics published by Resources, Conservation and Recycling in June 2025, there has been an increase in the global requirement for carbon fiber by 168.0% as of 2023, along with a predicted additional growth by 144.0% by the end of 2030. This particular growth has been reflected across different sectors, with an increased demand in the wind energy industry by 167.0%, which is further expected to surge to 113.0% by 2030. Therefore, this continuous growth is positively fueling the activated carbon supply chain across different regions, which in turn, is bolstering the market growth.

2024 Activated Carbon Export and Import Global Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

650.0 million |

- |

|

U.S. |

543.0 million |

292.0 million |

|

India |

403.0 million |

- |

|

Germany |

- |

262.0 million |

|

South Korea |

- |

183.0 million |

|

Global Trade Valuation |

3.4 billion |

|

|

Global Trade Share |

0.01% |

|

|

Export Product |

0.4% |

|

Source: OEC

Furthermore, the artificial intelligence (AI)-based smart manufacturing systems, the proliferation of closed-loop take-back systems, and the thermoplastic adoption in high-rate aerospace production are a few trends that are responsible for driving the market globally. As stated in an article published by NLM in May 2025, GE’s exceptional factory approach has integrated AI, machine learning, and Internet of Things-based sensors for monitoring the overall manufacturing process of turbine blades and aircraft components and successfully achieved nearly 20.0% optimization in production efficiency. Based on this, the global shipment valuation of carbon fibers, particularly for non-electrical applications, is worth USD 2.1 billion as of 2024, as stated by the OEC. Besides, as per the February 2023 Composites Part B: Engineering article, the worldwide carbon fiber reinforced polymer matrix composites (CFRPs) volume demand was almost 181.0 kt, which further doubled to 285.0 kt as of 2025, thus ensuring market demand.

2024 Carbon Fiber for Non-Electrical Uses Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

U.S. |

438.0 million |

369.0 million |

|

Japan |

391.0 million |

- |

|

France |

236.0 million |

- |

|

Germany |

- |

300.0 million |

|

China |

- |

223.0 million |

|

Global Trade Share |

0.009% |

|

|

Product Complexity |

0.8 |

|

Source: OEC

Key Carbon Fiber Composite Materials Market Insights Summary:

Regional Highlights:

- Asia pacific region in the carbon fiber composite materials market is anticipated to command a 41.8% revenue share by 2035, fueled by rapid industrialization, expanding aerospace manufacturing programs, government backing for advanced materials, and growing renewable energy infrastructure

- Europe is projected to emerge as the fastest-growing region throughout 2026–2035, impelled by stringent automotive emission regulations, accelerating offshore wind installations, environmental sustainability targets, and advancements in battery efficiency

Segment Insights:

- The carbon fiber composite materials market PAN-based carbon fiber segment is expected to command a 90.4% share by 2035, propelled by rising demand for lightweight materials with superior tensile strength and stiffness across aerospace, defense, automotive, and sports equipment applications

- During 2026–2035, the polymer matrix composites sub-segment is poised to secure the second-largest share in the market, stimulated by increasing adoption of high-strength-to-weight engineering materials that enable substantial vehicle weight reduction in automotive and aerospace applications

Key Growth Trends:

- Upscaling hydrogen storage facility

- Wind turbine decommissioning wave

Major Challenges:

- The recycling and circular economy deadlock

- Qualification deadlock for non-aerospace applications

Key Players: Toray Industries, Inc., Teijin Limited, Mitsubishi Chemical Group Corporation, Hexcel Corporation, SGL Carbon, Solvay S.A., DowAksa Advanced Composites Holdings, Hyosung Advanced Materials Corporation, Taekwang Industrial Co., Ltd., Kureha Corporation, Osaka Gas Chemicals Co., Ltd., UMATEX Group, Zhongfu Shenying Carbon Fiber Co., Ltd., Jilin Chemical Fiber Group Co., Ltd., Jiangsu Hengshen Co., Ltd., China National Bluestar (Group) Co., Ltd., Formosa Plastics Corporation, Sigmatex Limited, Cytec Industries, Mitsubishi Chemical Carbon Fiber and Composites, Hyundai Motor Group, Asahi Kasei, Syensqo.

Global Carbon Fiber Composite Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 23.5 billion

- 2026 Market Size: USD 25.9 billion

- Projected Market Size: USD 63.7 billion by 2035

- Growth Forecasts: 10.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.8% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, South Korea, Vietnam, Australia, Thailand

Last updated on : 13 May, 2026

Carbon Fiber Composite Materials Market - Growth Drivers and Challenges

Growth Drivers

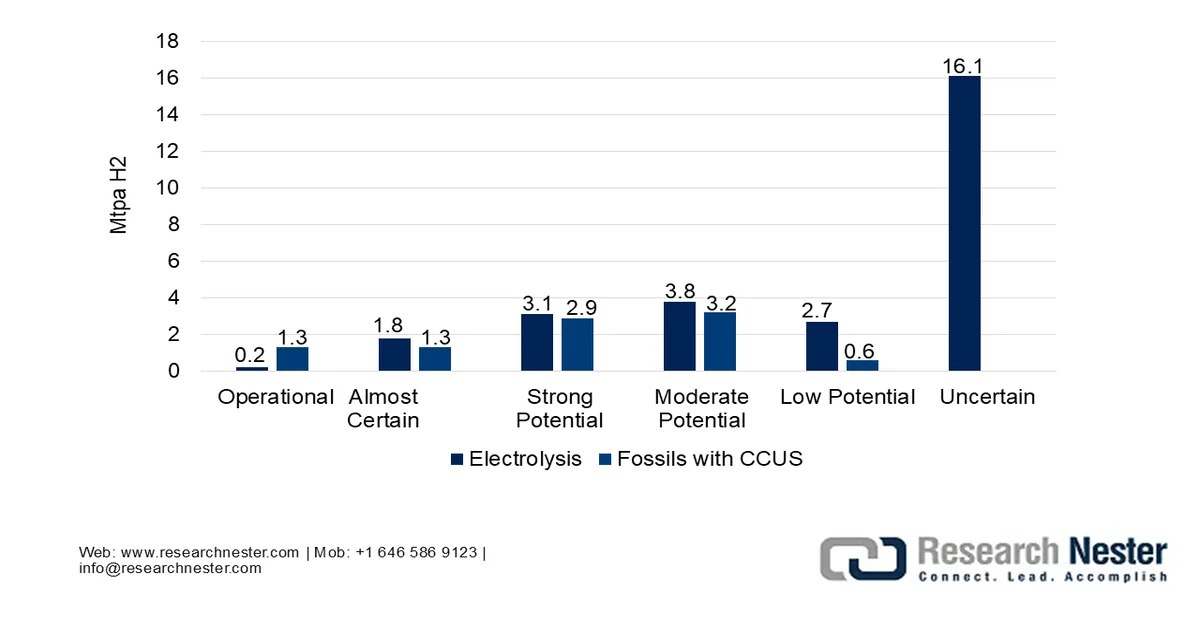

- Upscaling hydrogen storage facility: The worldwide push for hydrogen as a clean energy carrier is enhancing the unprecedented need for the carbon fiber composite materials market globally. According to official statistics published by the IEA Organization in 2025, there has been an increase in the demand for hydrogen to nearly 100 million tons as of 2024. Additionally, this demonstrated a surge by 2.0% from 2023 and is eventually in line with the total energy demand growth. Besides, the hydrogen demand from the newest applications accounted for less than 1.0% of the total, and is entirely concentrated in biofuels production. Meanwhile, the hydrogen supply is also dominated by fossil fuels, utilizing 290.0 billion cubic meters of natural gas and 90.0 million tons of coal equivalent as of 2024, thus fueling the market exposure.

Low-Emissions Hydrogen Production by Technology, 2030

Source: IEA Organization

- Wind turbine decommissioning wave: This is one of the significant drivers of the market, deliberately originating from the wind energy industry. As stated in an article published by the World Wind Energy Association (WWEA) in April 2026, there has been an expansion in worldwide wind capacity by 1,346 gigawatt, with an addition of 169.0 gigawatt as of 2025, demonstrating 35.0% more than 2024. Moreover, the wind power generation accounts for 3,000 TWh, which is more than 11.0% of the global demand. Besides, the yearly growth rate has surged from 11.9% to 14.3%, with China readily installing 130.0 gigawatt, which is 49.0% more than in 2024, and 77.0% from the global industry, thereby denoting an optimistic outlook for the market’s growth and expansion.

Total Cumulative Wind Capacity Installation, 2016-2025

|

Year |

Installation Capacity (MW) |

|

2016 |

485,549 |

|

2017 |

537,732 |

|

2018 |

589,511 |

|

2019 |

651,001 |

|

2020 |

744,745 |

|

2021 |

844,790 |

|

2022 |

930,793 |

|

2023 |

1,051,789 |

|

2024 |

1,177,164 |

|

2025 |

1,346,916 |

Source: World Wind Energy Association

- Electric vehicle lightweighting mandates: The automotive industry’s shift to electric platforms has significantly intensified lightweighting demands beyond conventional materials satisfaction, which is also fueling the carbon fiber composites market globally. As per an article published by the UNEP in 2026, the worldwide light-duty vehicle fleet, including both light commercial vehicles and passenger cars, is rapidly growing from 1.0 billion vehicles at present to an expected 2.0 billion or 2.5 billion by the end of 2050. This particular growth is poised to lead to a nearly 3-fold increase in energy utilization and carbon dioxide emissions globally. In this regard, by gaining a 60.0% share of battery electric and plug-in hybrid vehicles on the road, with saving more than 60.0 billion tons of carbon dioxide by the end of the same year.

Challenges

- The recycling and circular economy deadlock: Sustainability mandates are accelerating globally, yet the carbon fiber composite materials market remains functionally non-recyclable under conventional industrial infrastructure. Unlike thermoplastics that can be remelted or aluminum that retains value after reclamation, thermoset-based carbon fiber components end their lives in landfills or incinerators, a liability growing untenable as wind turbine blades and retired aircraft enter the waste stream. The technical challenge is severe: epoxy matrices are permanently cross-linked, and reclaiming fiber requires pyrolysis or solvolysis, which degrades mechanical properties and consumes significant energy. Economically, reclaimed chopped fiber commands only a fraction of virgin material pricing, making recycling operations commercially unviable without subsidies.

- Qualification deadlock for non-aerospace applications: While the aerospace industry relishes mature material databases and certified design allowables, industrial sectors lack equivalent design confidence in the carbon fiber composite materials market. Besides, automotive engineers, for instance, require millions of fatigue cycles, crash simulation models, and repairability protocols, none of which exist in publicly validated form for high-volume carbon fiber architectures. Moreover, every new industrial application effectively requires bespoke qualification, a process that consumes years and millions in testing. This standardization deficit creates perverse outcomes, with automakers either over-engineering using aerospace-grade material or under-engineering with generic grades.

Carbon Fiber Composite Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.5% |

|

Base Year Market Size (2025) |

USD 23.5 billion |

|

Forecast Year Market Size (2035) |

USD 63.7 billion |

|

Regional Scope |

|

Carbon Fiber Composite Materials Market Segmentation:

Raw Material Segment Analysis

Based on the raw material, the PAN-based carbon fiber segment is anticipated to grab the largest share of 90.4% in the carbon fiber composite materials market by the end of 2035. The segment’s upliftment is primarily attributed to its necessity for producing materials with outstanding tensile strength, low weight, and high stiffness, highly driven by innovations in defense, automotive, high-performance sports equipment, and aerospace industries. According to official statistics published by the Composites Part B: Engineering in February 2023, the yearly growth rate of CFRPs has been almost 12.5% since the past 20 years. In the aerospace sector, the Airbus A350 and the Boeing 787 made an expanded utilization of CFRPs within the airframe, which is more than 50 wt%, thereby bolstering the segment’s growth globally.

Matrix Material Segment Analysis

During the forecast period, the polymer matrix composites sub-segment, part of the matrix material segment, is projected to grab the second-largest share in the carbon fiber composite materials market. The sub-segment’s growth is effectively driven by its crucial role as engineering materials that offer exceptionally high-strength-to-weight and stiffness-to-weight ratios, along with permitting weight reduction in automotive and aerospace applications. As stated in an article published by NLM in August 2025, carbon fiber composites effectively weigh 25.0% of steel and almost 70.0% less than aluminum-based materials. In addition, multi-layer composites tend to absorb more energy than traditional steels, ensuring 60.0% reduction in the weight of front-end vehicle components. Therefore, based on this, polymer-based carbon fiber composites are increasingly implemented by the automotive sector, owing to their capability to diminish vehicle weight, thus boosting the sub-segment’s demand.

Tow Size Segment Analysis

The large tow (>48K) sub-segment, which is part of the tow size segment, is expected to account for the third-largest share in the market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by prioritizing volume, cost-efficiency, and processability over absolute mechanical performance. This fundamental positioning enables its dominance in high-throughput industries where material cost per kilogram outweighs marginal gains in tensile strength. The manufacturing advantage stems from the Zoltek-style precursor conversion: wider tow bands reduce the energy and floor space required per fiber unit, allowing producers to achieve economic scales unreachable with aerospace-grade offerings. However, this cost advantage introduces trade-offs, which make it suitable for driving the market growth.

Our in-depth analysis of the carbon fiber composite materials market includes the following segments:

|

Segment |

Subsegments |

|

Raw Material |

|

|

Matrix Material |

|

|

|

|

Product Form |

|

|

Manufacturing Technology |

|

|

End user Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Carbon Fiber Composite Materials Market - Regional Analysis

APAC Market Insights

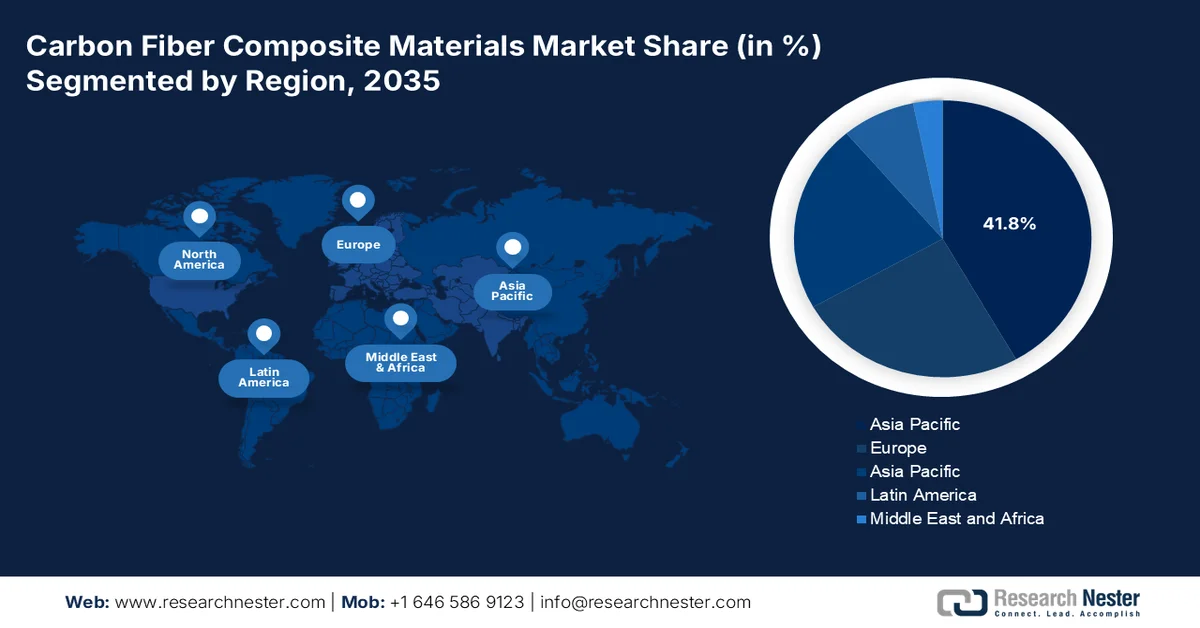

The Asia Pacific in the carbon fiber composite materials market is anticipated to account for the highest share of 41.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to rapid industrialization, an expansion in domestic aerospace manufacturing programs, strong government support for innovative materials, and the development of renewable energy facilities. According to official statistics published by the IEA Organization in 2026, the share of modernized renewables in finalized energy consumption in the region totaled 13.0% as of 2022, along with more than 135.0% in trends analysis. Based on this, New Zealand accounted for 30.4%, which is followed by 22.7% in Vietnam, 18.4% in India, 16.2% in Thailand, 14.0% Indonesia, and 13.5% in Australia. Therefore, with the presence of renewable facilities across countries, the market is witnessing increasing growth in the overall region.

Modern Renewables Share in Final Energy Consumption in the Asia Pacific, 2012-2022

|

Year |

Share % |

|

2012 |

7 |

|

2013 |

8 |

|

2014 |

8 |

|

2015 |

9 |

|

2016 |

9 |

|

2017 |

10 |

|

2018 |

10 |

|

2019 |

11 |

|

2020 |

12 |

|

2021 |

12 |

|

2022 |

13 |

Source: IEA Organization

The carbon fiber composite materials market in China is growing significantly, owing to strong industrial policies, prioritizing innovative composites for renewable energy, automotive, and aerospace industries, an expansion in domestic capacities, substantial government funding, and rapid expansion in the commercial aviation industry. As stated in an article published by the State Council in January 2026, the Civil Aviation Administration of China (CAAC) declared that the industry effectively achieved an overall transportation turnover of 164.0 billion ton-kilometers as of 2025, demonstrating a 10.5% year-on-year (YoY) increase. Based on this, the passenger traffic reached 770 million in the same year, indicating a 5.5% rise from 2024, while mail and cargo volume hit 10.1 million tons, depicting a surge by 13.3% YoY, thereby enhancing the demand for the market in the country.

The aspects of strengthening and modernizing defense capabilities, an increase in procurement expenditure on aircraft and equipment, the transition to electrified and lighter automobiles, and the presence of an effective supply chain are a few factors that are responsible for uplifting the market in Japan. Besides, the carbon fiber composite materials industry in the country was worth USD 1.5 billion as of 2025. Based on this, the industry is projected to reach USD 1.6 billion by the end of 2026, followed by USD 2.5 billion by 2035, along with a 7.2% growth rate. Moreover, based on government estimates published by the ITA in November 2025, 4,421,494 new passenger vehicles were readily sold in the country as of 2024. Besides, the auto manufacturing accounted for 2.9% of the country’s gross domestic product (GDP), along with 13.9% of its manufacturing GDP, thereby enhancing the market demand.

New Vehicle Sales Analysis in Japan, 2021-2024

|

Vehicle Type (In Units) |

2021 |

2022 |

2023 |

2024 |

|

Total new vehicle sales |

4,448,340 |

4,201,320 |

4,779,086 |

4,421,494 |

|

Passenger Cars |

3,675,698 |

3,448,296 |

3,992,727 |

3,725,200 |

|

Trucks |

765,762 |

747,543 |

777,949 |

686,197 |

|

Buses |

6,880 |

5,480 |

8,410 |

10,097 |

|

Key car sales |

1,652,522 |

1,638,136 |

1,744,919 |

1,557,868 |

|

Hybrid vehicle sales |

1,441,487 |

1,467,683 |

1,868,625 |

2,040,181 |

|

Electric vehicle sales |

21,693 |

58,813 |

88,535 |

59,736 |

Source: ITA

Europe Market Insights

Europe in the carbon fiber composite materials market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by strict regional emission regulations for automotive applications, rapid expansion in offshore wind energy facilities, environmental targets, innovative material solutions, and enhancements in battery performance. According to official statistics published by WindEurope in February 2025, the region installed 16.4 GW of new wind power capacity as of 2024, and 84.0% of this latest wind capacity developed was onshore. Besides, 2.6 GW of the latest offshore wind power capacity has been connected to the regional grid. Moreover, the region presently comprises 285.0 GW of wind power capacity, of which 248 GW is onshore, and the remaining 37 GW is offshore, thus proliferating the market development.

Yearly Onshore and Offshore Wind Power Capacity Installation in Europe, 2015-2024

|

Year |

Onshore (GW) |

Offshore (GW) |

|

2015 |

10.8 |

3.0 |

|

2016 |

13.3 |

1.5 |

|

2017 |

13.0 |

3.2 |

|

2018 |

9.6 |

2.7 |

|

2019 |

11.8 |

3.7 |

|

2020 |

11.3 |

2.9 |

|

2021 |

14.4 |

2.9 |

|

2022 |

16.4 |

2.5 |

|

2023 |

14.7 |

3.7 |

|

2024 |

13.8 |

2.6 |

Source: WindEurope

The carbon fiber composite materials market in Germany is gaining increased traction, owing to the unparalleled automotive engineering expertise, robust industrial base, the Industrie 4.0 strategy to foster manufacturing advancement, integrating carbon fiber-reinforced polymers, and support provision for lightweight materials. As stated in an article published by the ITA in August 2025, almost 70.0% of domestic advanced manufacturing firms purchase mostly within the overall region. Besides, 77.0% of domestic advanced manufacturing organizations are expecting growth in the industry in the upcoming 2 years. Moreover, in June 2025, the Federal Ministry of Finance proclaimed that the domestic cabinet has unveiled a law to accelerate depreciation of 30.0% for investments in machinery and equipment, thereby denoting a huge growth opportunity in the country.

The increase in investment in innovative manufacturing technologies, a robust aerospace industry centering around the Bristol composites facility, suitable government support for research and development in composite materials, the Zero Innovation Portfolio, and the increased focus on reducing carbon emissions are a few trends that are developing the carbon fiber composite materials market in the UK. Based on government estimates published by the ITA in January 2026, the domestic civil aerospace turnover was worth roughly USD 38.0 billion, of which USD 25.0 billion was exported as of 2023. Besides, the domestic defense industry’s turnover was valued at an estimated USD 35.0 billion, of which USD 12.0 billion is exported. Meanwhile, the country’s space industry’s overall turnover was worth USD 22.0 billion, with USD 7.0 billion is exported, thus enhancing the market development in the nation.

North America Market Insights

North America in the carbon fiber composite materials market is projected to witness suitable growth by the end of the stipulated timeline. The market’s growth in the region is effectively driven by the presence of the unparalleled defense and aerospace industry, an expansion in clean energy strategies, a mature industrial base, an increase in workforce in innovative manufacturing, and strong governmental support for lightweight materials. According to official statistics published by the Department of Energy in April 2026, the Biden-Harris Administration’s Investing in America agenda notified more than USD 230.0 billion as energy manufacturing investment, along with over 920 expanded energy manufacturing facilities, and 200,000 potential new clean energy employment opportunities. Besides, as per the April 2026 World Resources Institute article, data centers in the U.S. are projected to consume 9.0% to 17.0% of electricity by the end of 2030, thus boosting the market exposure.

Industries in the U.S. Driving Energy Demand, 2025-2030

|

Industry Type Category |

Growth |

|

Data Centers |

90.0 GW (55.0%) |

|

Industrial/Manufacturing |

30.0 GW (20.0%) |

|

Oil & Gas/Mining |

10.0 GW (5.0%) |

|

Other |

30.0 GW (20.0%) |

Source: World Resources Institute

The carbon fiber composite materials market in the U.S. is gaining increased exposure, owing to a suitable growth in satellite and space hardware manufacturing, along with the increased focus on low-cost coal-based carbon fiber development. As stated in an article published by the Center for Security and Emerging Technology (CSET) in February 2025, the country effectively conducts more than 50.0% of launches, with 5 of every 6 domestic launches originating from a single provider, namely SpaceX. In addition, with 81 launches, the provider accounts for over 149 global launches. Meanwhile, based on the July 2025 Space Foundation Organization article, the U.S. government space budget for the global space economy amounted to USD 77.7 billion. Therefore, with an increase in domestic launches and generous investment provision, the market is growing in the country.

The existence of government-funded zero-emission vehicle programs, as well as the import-based demand for high-performance composites, are a few factors that are responsible for expanding the carbon fiber composite materials market in Canada. As per an article published by the Government of Canada in August 2025, zero-emission vehicles, including battery-electric and plug-in hybrid electric vehicles, are continuing to enhance their shares in new vehicle purchases in the country and successfully reached 15.0% of overall motor vehicle registrations as of 2024. In addition, there has been an increase in overall vehicle sales by 8.0% as of 2024, in comparison to 2023. Besides, these vehicles are significantly responsible for 60.0% of the net increase in overall vehicle registrations, and accounted for 1 in 7 new vehicle purchases, thereby making it suitable for driving the market growth.

Key Carbon Fiber Composite Materials Market Players:

- Toray Industries, Inc. (Japan)

- Teijin Limited (Japan)

- Mitsubishi Chemical Group Corporation (Japan)

- Hexcel Corporation (U.S.)

- SGL Carbon (Germany)

- Solvay S.A. (Belgium)

- DowAksa Advanced Composites Holdings (Turkey)

- Hyosung Advanced Materials Corporation (South Korea)

- Taekwang Industrial Co., Ltd. (South Korea)

- Kureha Corporation (Japan)

- Osaka Gas Chemicals Co., Ltd. (Japan)

- UMATEX Group (Russia)

- Zhongfu Shenying Carbon Fiber Co., Ltd. (China)

- Jilin Chemical Fiber Group Co., Ltd. (China)

- Jiangsu Hengshen Co., Ltd. (China)

- China National Bluestar (Group) Co., Ltd. (China)

- Formosa Plastics Corporation (Taiwan)

- Sigmatex Limited (UK)

- Cytec Industries (now part of Solvay) (U.S.)

- Mitsubishi Chemical Carbon Fiber and Composites (U.S./Japan)

- Hyundai Motor Group (South Korea)

- Asahi Kasei (Japan)

- Syensqo (Belgium)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Toray Industries, Inc. stands as the most vertically integrated player in the carbon fiber market, controlling the value chain from raw polyacrylonitrile precursor through to finished prepregs and finished composite parts. The company has aggressively expanded its global manufacturing footprint across the U.S., Europe, and Asia to serve both aerospace anchor customers and emerging industrial applications such as pressure vessels and wind energy.

- Teijin Limited has strategically pivoted from a pure fiber supplier toward a solutions provider, focusing heavily on thermoplastic composite systems and automotive mass-production technologies. The company continues to invest in recycling infrastructure and rapid consolidation of its Tenax brand through targeted acquisitions of downstream fabricators.

- Mitsubishi Chemical Group Corporation differentiates itself through a dual focus on both PAN-based and specialized pitch-based carbon fibers, capturing niche applications requiring high thermal conductivity, such as semiconductor manufacturing equipment and space structures. The company has systematically expanded its large tow production capacity to compete aggressively in the industrial segment while maintaining a dedicated supply chain for Japanese aerospace programs.

- Hexcel Corporation maintains a concentrated focus on the premium end of the market, primarily supplying aerospace and defense platforms with certified, high-performance prepregs and structural reinforcements. The company has pursued long-term supply agreements with major airframers while simultaneously developing out-of-autoclave processing technologies to reduce manufacturing costs.

- SGL Carbon operates with a distinctly European industrial profile, leveraging its expertise in carbon fiber for automotive lightweighting and high-volume applications through joint ventures with major automakers. The company has restructured its portfolio away from commoditized fiber toward engineered solutions in hydrogen storage, wind energy, and battery components.

Here is a list of key players operating in the global market:

The global carbon fiber composite materials market remains highly consolidated, with Japan-based manufacturers, such as Toray, Teijin, and Mitsubishi, historically commanding the largest share of premium-grade production. However, the competitive dynamics are shifting as China-specific state-backed enterprises rapidly scale up capacity across both industrial and high-performance segments. Moreover, leading players are pursuing distinct strategic initiatives through vertical integration into precursor manufacturing and downstream prepregs, geographic expansion through local production facilities to mitigate tariff exposure. For instance, in September 2025, Asahi Kasei introduced its latest innovation in PFAS-free polyamide and recycling technology of continuous carbon fibers. These are suitable material solutions for automotive applications, lightweighting, and optimized connectivity, which is fueling the carbon fiber composite materials industry growth.

Corporate Landscape of the Market:

Recent Developments

- In October 2025, Hyundai Motor Group and Toray Industries, Inc. signed a strategic joint developmental agreement to collaborate on innovative materials and component advancements, intended to provide suitable standards in future mobility.

- In June 2025, Syensqo and Fairmat entered into a collaboration agreement for recycling carbon fiber prepreg waste and transforming it into valuable resources for manufacturing and creating new products in mobility, electronics, energy, and sports industries.

- In February 2025, Toray Industries, Inc. declared that 5 of its group organizations are expanding services in the composites industry by creating the latest value and a sustainable future through collaboration and technology implementation.

- Report ID: 8558

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.