Control Valve Market Outlook:

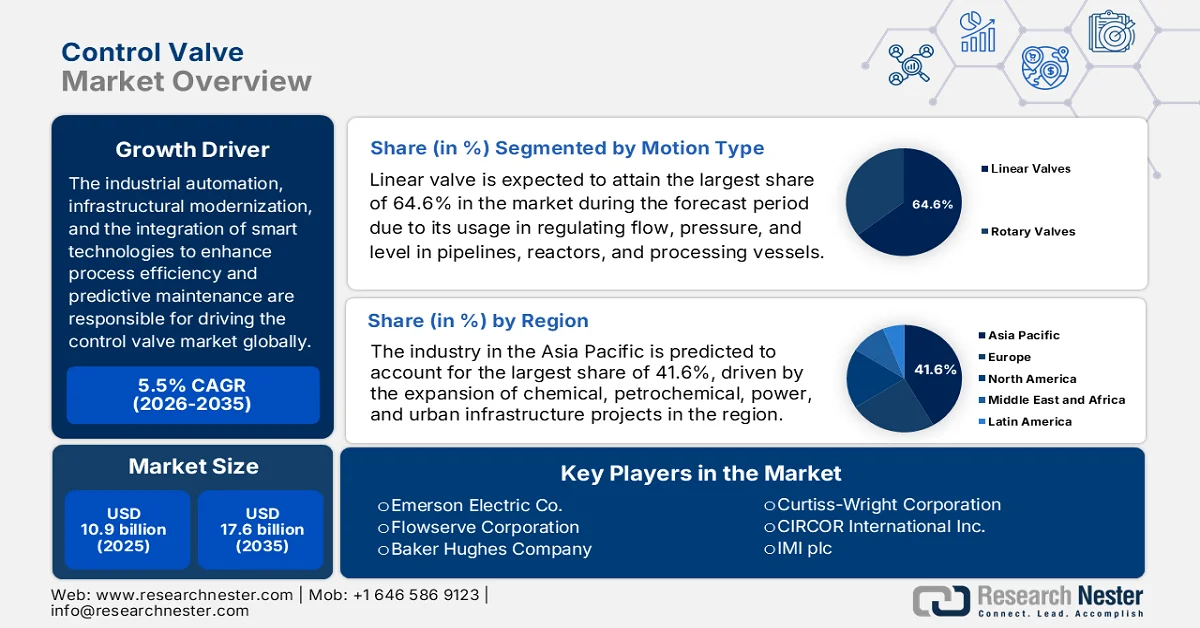

Control Valve Market size was valued at USD 10.9 billion in 2025 and is expected to grow to USD 17.6 billion by 2035, registering a CAGR of 5.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of control valve is assessed at USD 11.5 billion.

The rapid industrial automation, infrastructural modernization, and the integration of smart technologies to enhance process efficiency and predictive maintenance are the main growth catalysts for the control valve market globally. Demand is strong in the oil and gas, chemical processing, water treatment, and power generation sectors, which require precise flow, pressure, and temperature regulation for efficient operations. The control valve market depends on raw materials such as stainless steel, alloys, and specialized components. In February 2026, the World Steel Organization reported that global stainless steel melt shop production reached 64.2 million tons, which marks a 2.1% increase when compared to 2024. Asia led production with almost 55.3 million tons, up 2.7%, whereas Europe produced 5.7 million tons. In the U.S., the output rose 7.6% to 2.1 million tons, whereas other countries collectively produced 1.1 million tons, thus positively impacting the market’s growth.

Furthermore, the visible trends reshaping the future dynamics of the control valve market are a shift towards high-performance rotary valves and advanced digital actuators that offer improved accuracy and lower energy consumption under extreme process conditions. In this context, World Integrated Trade Solution (WITS) reported that in 2024, global exports of pressure‑reducing valves were led by Europe with a worth of USD 770.2 million, 15,208,300 kg, followed by Germany. At the same time, the U.S. exported a total of USD 478.8. Other noteworthy exporters in this category included Mexico, the UK, Korea, Japan, and India, reflecting a diverse set of manufacturing hubs supplying the global control valve market. Also, these figures indicate that Europe dominates in value, Asia contributes significantly in volume, reflecting cost‑competitive production and high demand in global pipelines. Moreover, the trade data emphasizes the tactical importance of cross‑border logistics and supply chain management for industrial valve components.

Top Global Pressure-Reducing Valve Exporters in 2024: Value and Volume by Country

|

Country/Region |

Export Value (USD 1000) |

Quantity (Kg) |

|

European Union |

770,236.43 |

15,208,300 |

|

Germany |

518,008.07 |

6,888,660 |

|

U.S. |

478,805.56 |

7,799,690 |

|

China |

395,315.70 |

28,755,700 |

|

Italy |

343,537.98 |

11,277,000 |

|

Mexico |

223,901.17 |

11,743,000 |

|

UK |

195,682.00 |

1,221,960 |

|

Korea, Rep. |

154,620.52 |

4,083,570 |

|

Japan |

138,718.63 |

2,083,880 |

|

India |

95,140.67 |

3,958,450 |

Source: WITS

Key Control Valve Market Insights Summary:

Regional Highlights:

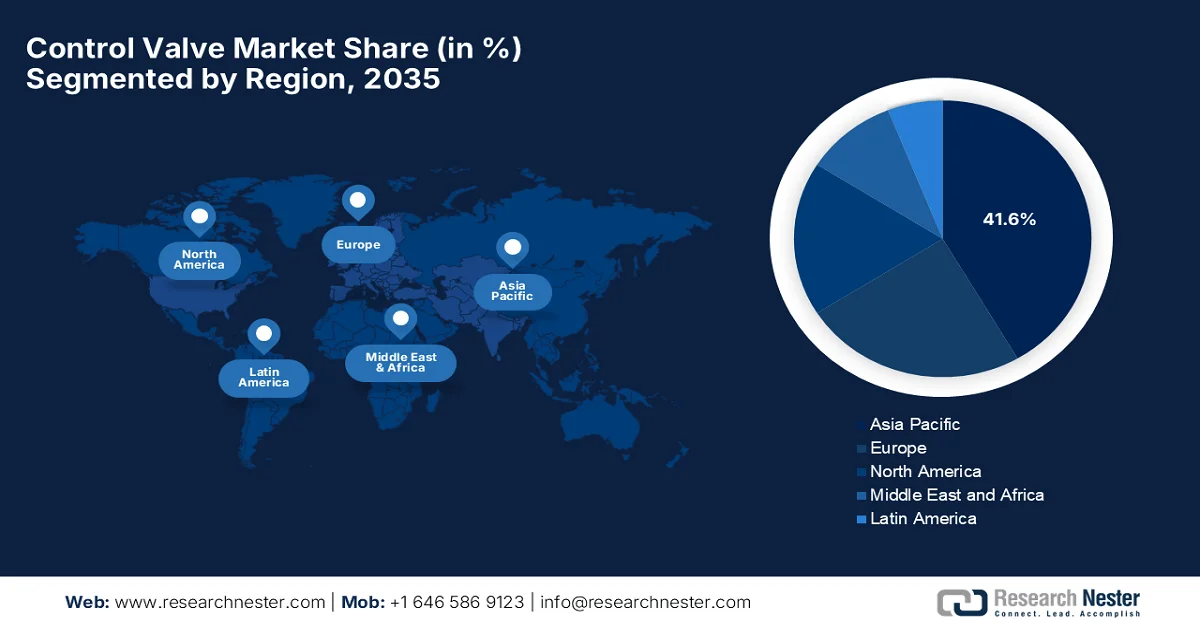

- Asia Pacific control valve market is projected to hold a dominant 41.6% share by 2035, fueled by rapid industrialization and expanding chemical, petrochemical, power, and infrastructure projects

- North America is anticipated to experience notable expansion in the forecast period, supported by strong investments across oil & gas, water treatment, and advanced manufacturing sectors

Segment Insights:

- Linear valve segment in the control valve market is expected to capture a leading 64.6% share by 2035, propelled by its precise flow regulation capabilities and stable performance across industrial applications

- Actuators segment is projected to witness considerable share growth by 2035, driven by rising industrial automation and increasing integration of digital control systems

Key Growth Trends:

- Increasing industrial automation & digitalization

- Expansion of process industries

Major Challenges:

- High initial costs and total cost of ownership

- Complex maintenance and operational challenges

Key Players: Emerson Electric Co. (U.S.), Flowserve Corporation (U.S.), Baker Hughes Company (U.S.), Curtiss-Wright Corporation (U.S.), Crane Company (U.S.), CIRCOR International Inc. (U.S.), IMI plc (UK), Rotork plc (UK), Spirax-Sarco Engineering plc (UK), KSB SE & Co. KGaA (Germany), Christian Bürkert GmbH & Co. KG (Germany), SAMSON AG (Germany), Metso Corporation (Finland), Alfa Laval AB (Sweden), KITZ Corporation (Japan), Trillium Flow Technologies (UK), Control Devices (U.S.), Sherwood Valve (U.S.), Woodward (U.S.), Valve Research & Manufacturing (U.S.), Azbil Corporation (Japan), Weir Group PLC (UK), Samyang Corporation (South Korea), L&T Valves Limited (India), Kossan Engineering (Malaysia).

Global Control Valve Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 10.9 billion

- 2026 Market Size: USD 11.5 billion

- Projected Market Size: USD 17.6 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (41.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Saudi Arabia

Last updated on : 13 April, 2026

Control Valve Market - Growth Drivers and Challenges

Growth Drivers

- Increasing industrial automation & digitalization: The swift uptake of automation technologies in industries such as oil & gas, chemicals, and power generation is considered to be the primary driver for the control valve market. At the same time, integration with IIoT, smart sensors, and predictive maintenance systems is boosting the overall demand of this sector. As a result, this has led to remarkable imports from major nations. WITS stated that global trade in pressure-reducing valves in 2023 shows strong demand concentrated in industrialized as well as manufacturing-driven economies. The U.S. led the total imports at almost USD 573.2 million, which reflects the extensive usage across oil & gas, water systems, and industrial automation. China and Europe followed, which is driven by their manufacturing and infrastructure needs. Overall, the data highlights the prominence of these valves in energy, utilities, and industrial efficiency worldwide.

Top Global Importers of Pressure-Reducing Valves in 2023 by Trade Value and Volume

|

Country/Region |

Trade Value (USD ‘000) |

Quantity (Kg) |

|

U.S. |

573,226.79 |

25,758,300 |

|

China |

454,946.71 |

5,931,390 |

|

Europe |

292,090.96 |

7,394,310 |

|

Germany |

287,191.00 |

6,079,270 |

|

UK |

194,001.16 |

4,220,510 |

|

Canada |

147,188.09 |

2,484,850 |

|

Mexico |

129,193.15 |

2,840,320 |

|

Other Asia (nes) |

117,555.49 |

1,055,920 |

|

Brazil |

101,561.30 |

1,873,500 |

|

South Korea |

100,606.48 |

1,729,610 |

|

Japan |

96,103.94 |

2,221,870 |

Source: WITS

- Expansion of process industries: Growth in industries such as oil & gas, chemicals, pharmaceuticals, food & beverage contributes to the upliftment of the control valve market globally. These sectors actually require accurate fluid handling and process control, which in turn increases valve adoption. In this context, the U.S. Energy Information Administration reported that the U.S. leads in terms of global oil production, with 22%, and consumption, being 20% in 2023, which positions it as the dominant player in the energy industry. It also mentioned that major producers include Saudi Arabia and Russia, whereas countries such as Canada and China contribute remarkably to supply. On the consumption side, China and India are the major demand drivers due to rapid industrialization and population growth. It is observed that oil production is concentrated in resource-rich nations, denoting a lucrative growth opportunity for control valve market.

Top 10 Oil Producing Countries in 2023 by Output (Million Barrels per Day) and Global Market Share

|

Country |

Production (Million Barrels/Day) |

Share of World Total |

|

U.S. |

21.91 |

22% |

|

Saudi Arabia |

11.13 |

11% |

|

Russia |

10.75 |

11% |

|

Canada |

5.76 |

6% |

|

China |

5.26 |

5% |

|

Iraq |

4.42 |

4% |

|

Brazil |

4.28 |

4% |

|

UAE |

4.16 |

4% |

|

Iran |

3.99 |

4% |

|

Kuwait |

2.91 |

3% |

Source: U.S. EIA

- Rising energy & power demand: The aspect of increasing global energy consumption is driving investments in power plants, renewable energy systems, oil refining & gas processing. In this context, control valves are highly essential in ensuring operational efficiency and safety in these systems, thus allowing increased adoption in the control valve market. The International Energy Agency in March 2025 reported that globally, the energy demand rose by 2.2% in 2024, which is identified as nearly double the decade’s average of 1.3%, whereas the electricity consumption surged 4.3% or 1,100 TWh. Besides the renewables, which added a record 700 GW and, with nuclear, supplied 40% of total generation. In addition, natural gas demand climbed 115 bcm (2.7%), oil grew just 0.8%, and coal rose 1%, mainly due to heatwaves in China and India. Hence, all of these statistics reflect the presence of constant demand for control valves across major nations.

Challenges

- High initial costs and total cost of ownership: This is the biggest burden for the control valve market since the advanced smart valves with digital controllers and actuators come with heavy initial expenses. Also, certain industries, i.e., oil & gas, power, and chemicals, mostly require customized, high-specification valves that are capable of operating under extreme temperatures and pressures, thereby remarkably increasing capital expenditure. Other than procurement, the aspects of installation, calibration, and integration into automation systems exacerbate the overall costs. Maintenance expenses, including periodic servicing, spare parts, and skilled labor, contribute significantly to the total cost of ownership. In this context, small and medium enterprises might find it challenging, causing delays in the adoption of advanced valve technologies.

- Complex maintenance and operational challenges: The control valves need to operate in harsh industrial scenarios that comprise high pressure, corrosive fluids, and extreme temperatures, which can lead to wear and tear over the long run. In this context, maintaining proper valve performance needs regular inspection, calibration, and replacement of components such as seals and actuators. Also, most of the industries are witnessing a shortfall of skilled technicians who are capable of handling advanced valve diagnostics and repairs. Unplanned downtime due to valve failure can disrupt entire production processes, resulting in significant financial losses for pioneers in the control valve market. In addition, improper maintenance practices can reduce valve lifespan and efficiency, which makes reliability a major burden for end users across process industries.

Control Valve Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 10.9 billion |

|

Forecast Year Market Size (2035) |

USD 17.6 billion |

|

Regional Scope |

|

Control Valve Market Segmentation:

Motion Type Segment Analysis

In the motion type segment, the linear valve is expected to attain the largest share of 64.6% in the control valve market during the forecast period. The subtype is extensively used for regulating flow, pressure, and level in pipelines, reactors, and processing vessels. They are widely preferred for their precise volumetric control, low leakage, and stable performance. For instance, in May 2022, John Crane introduced the G58IEP Fugitive Emission Control Packing, which is especially designed for API 624-certified valves across industries such as oil and gas, chemical processing, and power generation. It is built with high-purity flexible graphite, Inconel wire reinforcement, and a passive corrosion inhibitor. The packing ensures durability, chemical resistance, and reduced leakage. Hence, with such continued innovations, the linear valves segment will grow at a rapid pace in the years ahead.

Component Segment Analysis

By the conclusion of the forecast period, actuators, which are under the component segment, are anticipated to grow with a considerable share in the control valve market. The segment’s growth is largely driven by the growth of industry automation and digital control integration, requiring electric, pneumatic, and hydraulic actuation for remote operation and timely process adjustments. Besides, these actuators determine overall valve performance and compatibility with IIoT and smart systems. In January 2024, Emerson announced the launch of the Fisher Easy-Drive 200R electric actuator, which is especially designed for butterfly and ball valves in demanding industrial environments. It eliminates emissions from gas-operated actuators and offers easy one-button calibration, low energy usage, and reliable operation down to -40°C. Therefore, with such instances, the segment is expected to witness sustained growth as industries are looking for smart, energy-efficient, and digitally integrated actuation solutions.

Application Segment Analysis

In terms of application, the flow control is predicted to grow at a significant rate in the control valve market during the discussed timeframe. The expanding industrial automation, precision process optimization, and the critical role of control valves in regulating fluid volumes are the main factors driving this leadership. It regulates the fluid volumes in pipelines and reactors across sectors such as chemicals, oil & gas, and utilities. Industry-validated analysis states that these flow control leads this segment due to their high precision in volumetric control and minimal leakage characteristics. Also, the widespread adoption of automated and digitally enabled valves allows real-time flow adjustments, enhancing operational efficiency, safety, and process reliability. At the same time, heightened demand for accurate chemical dosing, efficient fluid transport, and optimized industrial processes efficiently drives this segment.

Our in-depth analysis of the control valve market includes the following segments:

|

Segment |

Subsegments |

|

Motion Type |

|

|

Component |

|

|

Application |

|

|

Material Type |

|

|

End use Industry |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Control Valve Market - Regional Analysis

APAC Market Insights

The Asia Pacific control valve market is projected to dominate the entire global dynamics with a total share of 41.6% over the forecasted years. The region’s dominance is effectively propelled by rapid industrialization, the expansion of chemical, petrochemical, power, and urban infrastructure projects. Adoption of automation, IIoT-enabled valves, and smart control systems is rising, making this region a key growth engine for the global control valve market. In this context, IEA stated that the Asia Pacific is central to shaping the global energy future. In 2023, coal dominated the energy mix at 49.3%, followed by oil at 23.2% and natural gas at 11.1%, whereas renewables accounted for 3.8% of supply and 23.8% of power generation. It also mentioned that China leads the clean energy growth, whereas India is set for the fastest demand increase, and Southeast Asia is rapidly expanding. Countries such as Japan and Korea are charting secure decarbonization pathways, hence positively impacting regional control valve market growth.

The strong industrial expansion across chemicals, pharmaceuticals, water treatment, and electric vehicle manufacturing sectors is responsible for uplifting the control valve market in China. Continued investments in infrastructure development, renewable energy projects, and industrial modernization efficiently accelerate market demand. Based on the government data published in September 2025, the country aimed for a target of 5% annual growth in the added value of its petrochemical and chemical industries for 2025-2026. The plan was issued by the Ministry of Industry and Information Technology and other agencies, emphasizing boosting innovation, improving economic returns, and cutting pollution and carbon emissions. It mentioned that ten priority measures were focused on expanding high-end supply, advancing critical products such as electronic chemicals and polyolefins, and fostering modern chemical parks, thus suitable for bolstering the country’s market.

The modernization of process industries and a remarkable push toward industrial automation are deliberately supporting the upliftment of the control valve market in India. The main demand drivers for the country’s market are expanding infrastructure projects, such as smart city initiatives and water management schemes, along with growing, refining, and power generation sectors. As stated by Press Information Bureau (PIB) in February 2026, the Union Budget FY 2026-27 announced the development of three chemical parks in India, generously allocating around USD 72 million with the main goal to strengthen domestic chemical manufacturing. Besides, these parks are designed as cluster-based, plug-and-play hubs with shared infrastructure to improve efficiency, reduce costs, and enhance industrial integration. Also, these initiatives build on existing models such as plastic parks, bulk drug parks, and PCPIRs, thereby promoting demand for control valves.

North America Market Insights

The North America control valve market is witnessing noteworthy growth due to the safety regulations. The region’s demand is extensively supported by heavy investment in oil & gas, water treatment, and advanced manufacturing sectors. Leading OEMs and aftermarket service providers in the U.S. and Canada are expanding digital integration and automation in control valve offerings, with a main goal to capture growth in both new installations and retrofit projects. In March 2026, the U.S. Department of Energy reported that it will release 172 million barrels of oil from the Strategic Petroleum Reserve as part of a coordinated IEA effort totaling 400 million barrels. It also stated that these reserves will be replenished with 200 million barrels within a year, exceeding the release by 20% at no taxpayer cost. Hence, such an oil ecosystem in the country indicates a huge opportunity for control valves.

The increasing industrial automation, the adoption of Industry 4.0, and the need for enhanced process efficiency across different sectors are supporting the expansion of the control valve market in the U.S. Simultaneously, the increasing investments in infrastructure projects, including transport management, are also contributing to sustained market demand in the country. In June 2024, the U.S. Department of Transportation stated that Pete Buttigieg announced almost USD 1.8 billion in RAISE grants under the Bipartisan Infrastructure Law as part of the Joe Biden administration’s nationwide infrastructure investment push. The funding supports 148 projects across all 50 states, 4 territories, and Washington, D.C., focusing on safety, transit access, climate resilience, and economic development. In addition, the projects range from road restoration and rail safety upgrades to electric transit, pedestrian networks, and port modernization, thus prompting a huge demand for control valves.

U.S. RAISE Infrastructure Grants Breakdown (2024): Funding for Major Transportation and Community Projects Nationwide

|

Project |

Location |

Funding |

Key Focus |

|

Alaska Highway Permafrost Restoration |

Fairbanks, Alaska |

USD 25.0 million |

Road repair, climate resilience |

|

Electrify Downeast Acadia |

Maine (multiple counties) |

USD 23.53 million |

Electric buses, clean transit |

|

Joe Louis Greenway & Iron Belle Trail |

Detroit, Michigan |

USD 20.70 million |

Shared-use paths, safety |

|

Holloway Street Transit Access |

Durham, North Carolina |

USD 12.04 million |

Intersection upgrades, pedestrian safety |

|

Santa Ana Boulevard Grade Separation |

Santa Ana, California |

USD 25.0 million |

Rail crossing, multimodal transport |

|

Lake Wales Complete Streets |

Lake Wales, Florida |

USD 22.93 million |

Road diets, bike/ped infrastructure |

|

Reconnect Toledo Riverwalk |

Toledo, Ohio |

USD 19.11 million |

Multi-use trail, climate resilience |

|

Allegheny Riverfront Connectivity |

Sharpsburg, Pennsylvania |

USD 24.94 million |

Bridge, transit access, trails |

|

Wharf D Reconstruction |

Puerto Nuevo, Puerto Rico |

USD 21.22 million |

Port safety, emissions reduction |

Source: The U.S. Department of Transportation

A strong emphasis on digitalizing industrial processes, especially the energy and manufacturing sectors are propelling the control valve market in Canada. Major end user sectors in the country, such as oil and gas, petrochemicals, water treatment, and pulp and paper, are driving this demand by prioritizing modernization and upgrading aging infrastructure. Based on the government data published in April, 2026, Canada launched the Build Communities Strong Fund, with a total USD 51 billion initiative in a span of 10 years to expand critical infrastructure nationwide. The fund will be matched by USD 17 billion from provinces and additional municipal and private investments, thereby boosting GDP by almost USD 95 billion. As part of the first projects, USD 28 million was allocated to expand wastewater, stormwater, and water systems in Northeast St. Albert, Alberta, unlocking 800 acres of future residential development, propelling continued control valve demand.

Europe Market Insights

The control valve market in Europe has acquired a prominent position in the global dynamics propelled by its focus on industrial automation, stringent environmental regulations, and the necessary modernization of aging infrastructure. The region’s market is witnessing remarkable technological advancements in terms of smart actuators, digital positioning, and digital twin technology, which are readily facilitating improved operational safety and reduced downtime. In February 2024, Siemens Smart Infrastructure showcased its exclusive building technologies at MCE 2024 by mainly focusing on sustainable heating, cooling, and ventilation solutions. Besides, a highlight was the MVL702 magnetic expansion valve, which boosts heating capacity by up to 21% and delivers energy savings of up to 14% for heat pumps and chillers. Hence, with constant innovations, the region’s market is expected to witness unprecedented growth in the next decade.

The booming manufacturing base and a strong pivot toward Industry 4.0 automation are the main boosting factors for the control valve market in Germany. At the same time, the rising investments in renewable energy infrastructure, such as hydrogen production and district heating systems, are creating new growth opportunities for specialized valve applications. In this context, in April 2023, the country’s Federal Ministry announced nearly USD 1.1 billion in funding for Salzgitter AG’s SALCOS project. In addition to more than USD 2.2 billion in total investment, the initiative will build hydrogen-ready steel plants, including a direct reduction facility, electric arc furnace, and 100 MW electrolyser. Therefore, these technologies are expected to cut 46 million tons of carbon emissions by 2041, thus suitable for bolstering the control valve industry in the country in the years ahead.

The UK control valve market has gained immense exposure, highly driven by the need for precision control across industrial sectors. At the same time, modernization programs within water infrastructure and district heating networks are encouraging the adoption of more responsive and reliable flow-control equipment capable of supporting variable operating conditions. Based on the government data published in February 2026, the UK Health and Safety Executive published a tender for an 80 mm vacuum-insulated control valve, which is designed for liquid hydrogen service at cryogenic temperatures. This valve must consist of pneumatic actuation, an ATEX Zone 1 position indicator, and ANSI class 300 flanged connections. It also mentioned the contract value of about USD 25,000, excluding VAT, or USD 30,000 including VAT. Hence, with such government procurements, the country’s control valve market will proliferate at a noteworthy pace.

Key Control Valve Market Players:

- Emerson Electric Co. (U.S.)

- Flowserve Corporation (U.S.)

- Baker Hughes Company (U.S.)

- Curtiss-Wright Corporation (U.S.)

- Crane Company (U.S.)

- CIRCOR International Inc. (U.S.)

- IMI plc (UK)

- Rotork plc (UK)

- Spirax-Sarco Engineering plc (UK)

- KSB SE & Co. KGaA (Germany)

- Christian Bürkert GmbH & Co. KG (Germany)

- SAMSON AG (Germany)

- Metso Corporation (Finland)

- Alfa Laval AB (Sweden)

- KITZ Corporation (Japan)

- Trillium Flow Technologies (UK)

- Control Devices (U.S.)

- Sherwood Valve (U.S.)

- Woodward (U.S.)

- Valve Research & Manufacturing (U.S.)

- Azbil Corporation (Japan)

- Weir Group PLC (UK)

- Samyang Corporation (South Korea)

- L&T Valves Limited (India)

- Kossan Engineering (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Emerson Electric Co. is widely regarded as a global leader in control valve market propelled by its strong presence in process automation. The company’s strength lies in its integrated ecosystem combining valves, actuators, and digital control systems such as DeltaV, which allows it to maintain a leading position in this sector.

- Flowserve Corporation is a major player that is best known for its portfolio of control valves, pumps, and seals. Besides, the firm differentiates itself through engineering expertise in severe-service applications, particularly in terms of oil & gas, power generation, and chemical processing.

- IMI plc is a key player based in Europe, and the company specializes in highly engineered flow control solutions through its IMI Critical Engineering division. The company is mainly focused on high-specification, mission-critical valves used in energy, nuclear, and petrochemical industries.

- Metso Corporation was formerly known as Metso Outotec and is considered to be a leading provider of flow control solutions with a strong focus on process industries such as mining, pulp & paper, and energy. The firm emphasizes digital valve controllers, intelligent valve monitoring, and lifecycle services, allowing customers to focus primarily on optimizing process efficiency.

- KITZ Corporation is one of the leading valve manufacturers, best known for its wide range of industrial valves, including control valves. Also, the company has built a strong reputation for high-quality manufacturing, cost competitiveness, and extensive distribution networks, particularly in the Asia Pacific markets.

Below is the list of some prominent players operating in the global control valve market:

Emerson Electric Co., Flowserve Corporation, Baker Hughes Company, Curtiss-Wright Corporation, Crane Company, CIRCOR International Inc., and IMI plc are dominating the overall control valve market globally. Competition in this field is effectively driven by technological innovation, especially in smart valves, digital automation, and IIoT integration. At the same time, leading pioneers in this sector are proactively participating in R&D, launching advanced products, and expanding manufacturing footprints globally. Strategic initiatives include mergers and acquisitions, partnerships, and capacity expansion with the main goal of strengthening supply chains and regional presence. In March 2026, Woodward announced the acquisition of Valve Research & Manufacturing, which is a Florida-based aerospace valve maker, to add solenoid, check, and relief valve technologies to its portfolio. The acquisition will strengthen Woodward’s aerospace controls capabilities and maintain VRM’s operations and customer relationships.

Corporate Landscape of the Control Valve Market:

Recent Developments

- In February 2026, Flowserve announced a total of USD 490 million acquisition of Trillium Flow Technologies’ Valves Division, to solidify its portfolio in nuclear and traditional power markets. The deal expands Flowserve’s installed base and enhances its aftermarket service potential.

- In January 2026, Control Devices announced the acquisition of Sherwood Valve to expand its flow control solutions across industrial, specialty, high-purity, and medical gas applications. The acquisition strengthens Control Devices’ position in the compressed gas industry.

- In October 2025, Azbil Corporation introduced its 6000 Series control valves, conforming to IEC 60534 standards and optimized with CFD analysis for superior performance. The valves deliver improved Cv values, excellent shutoff capability, making them a key element in Azbil’s CV total solution for advanced automation.

- Report ID: 5740

- Published Date: Apr 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Control Valve Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.