Construction Additives Market Outlook:

Construction Additives Market size was valued at over USD 28.8 billion in 2025 and is expected to reach USD 58.5 billion by the end of 2035, growing at a CAGR of 8.2% over 2026-2035. In 2026, the industry size of construction additives is evaluated at USD 31.1 billion.

The global construction additives market is significantly being reshaped by evolving industrial practices, technological advancements, a shift in regulatory landscapes, infrastructure expenditure, increased urbanization, and international trade realignments. According to official statistics published by the U.S. Bureau of Labor Statistics in March 2025, the aspect of construction employment reached an all-time high of 8.0 million, deliberately surpassing the previous peak employment level of 7.7 million. Besides, the industry is expected to grow by 4.7% between 2023 and 2033, rapidly than the projected 4.0% for the overall sectors. This particular growth resulted in the addition of nearly 380,100 new employment opportunities, thus bringing the expected employment growth in the industry to be almost 8.4 million by the end of 2033, thus boosting the market growth.

Construction Industry Employment and Expected Employment (2023-2033)

|

Construction Components |

Employment (in thousands 2023) |

Expected Employment (in thousands 2033) |

Employment Changes (in thousands 2023) |

Employment Percent Change (2023-2033) |

|

Power and communication line and related structures construction |

239.6 |

255.3 |

15.7 |

6.6 |

|

Electrical contractors and other wiring installation contractors |

1,067.4 |

1,137.9 |

70.5 |

6.6 |

|

Plumbing, heating, and air-conditioning contractors |

1,259.4 |

1,334.4 |

75.0 |

6.0 |

|

Nonresidential building construction |

884.2 |

936.4 |

52.2 |

5.9 |

|

Other building equipment contractors |

155.9 |

164.6 |

8.7 |

5.6 |

|

Other specialty trade contractors |

780.0 |

823.0 |

43.0 |

5.5 |

|

Poured concrete foundation and structure contractors |

255.8 |

267.9 |

12.1 |

4.7 |

|

Highway, street, and bridge construction |

369.8 |

386.3 |

16.5 |

4.5 |

Source: U.S. Bureau of Labor Statistics

Furthermore, the development of innovative low-carbon cement technologies, tactical partnerships for technological integration and market expansion, the growth of specialized additives for functional and aesthetic concrete, and accelerated innovation, owing to trade and tariffs protectionism, are certain trends that are responsible for bolstering the market globally. As stated in an article published by NLM in August 2023, it has been demonstrated that the worldwide cement production achieved a compound annual growth rate of an estimated 5.1% between 2022 and 2025. Besides, approximately 2% to 3% of the world’s annual energy utilization and 9% to 10% of industrial water are used by the concrete sector. In addition, the sector also effectively generates 8% to 9% of greenhouse gas emissions, or almost 10 billion metric tons yearly, thereby denoting an optimistic outlook for the market’s welfare.

Key Construction Additives Market Insights Summary:

Regional Highlights:

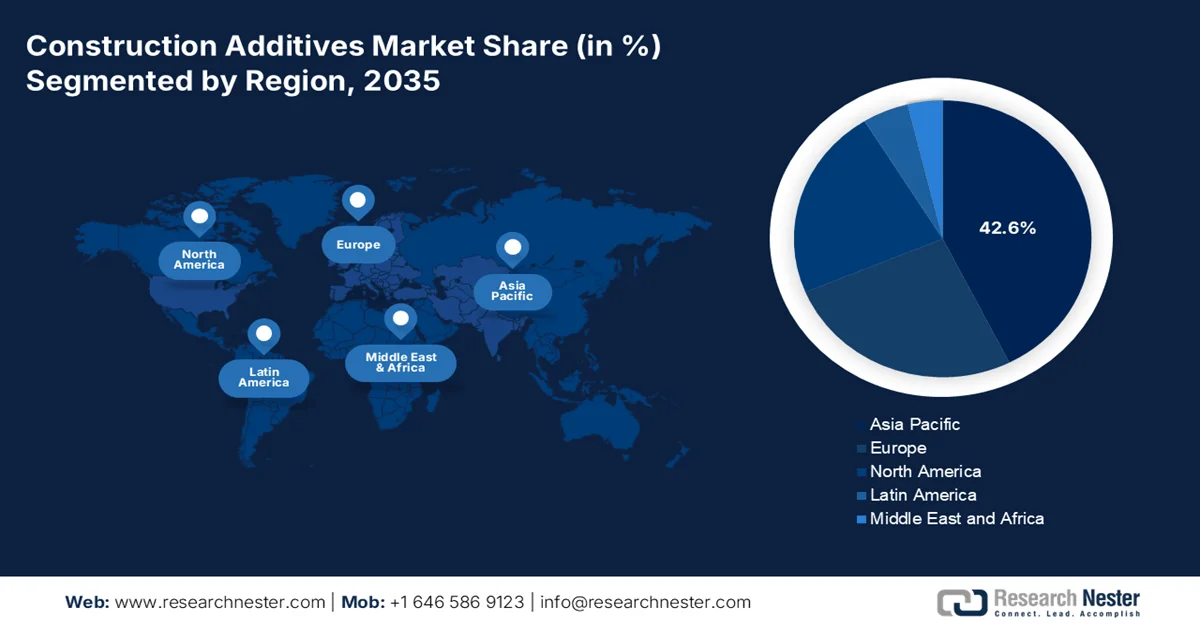

- Asia Pacific in the construction additives market is projected to hold a leading 42.6% share by 2035, attributed to unprecedented infrastructure growth, rapid urbanization, and increasing energy efficiency implementation

- North America is anticipated to be the fastest-growing region over the 2026–2035 period, impelled by expanding construction chemicals usage, rising repair and rehabilitation activities, and strategic investments in clean technological manufacturing

Segment Insights:

- The liquid-applied membranes segment in the construction additives market is projected to account for a dominant 60.7% share by 2035, propelled by its superior performance characteristics and application versatility

- The steel fibers sub-segment is expected to secure the second-highest share during the 2026–2035 period, driven by its importance for enhancing the toughness, strength, and durability of concrete along with improving structural integrity and controlling cracking

Key Growth Trends:

- Increase in green-building solutions

- Massive infrastructure pipelines

Major Challenges:

- Infrastructure and logistics constraints in emerging economies

- Competition from substitutes and traditional construction methods

Key Players: BASF SE, Sika AG, Dow Inc., MAPEI S.p.A., Saint-Gobain S.A., RPM International Inc., GCP Applied Technologies Inc., Fosroc International, W.R. Grace & Co., Evonik Industries AG, Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema S.A.

Global Construction Additives Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 28.8 billion

- 2026 Market Size: USD 31.1 billion

- Projected Market Size: USD 58.5 billion by 2035

- Growth Forecasts: 8.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (42.6% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, India, Germany, Japan

- Emerging Countries: Brazil, Indonesia, Vietnam, Mexico, Saudi Arabia

Last updated on : 23 March, 2026

Construction Additives Market - Growth Drivers and Challenges

Growth Drivers

- Increase in green-building solutions: Green building certifications and energy-performance directives are major drivers for the market globally. According to official statistics published by the World Economic Forum in June 2024, China and Beyond collaborated with Boston Consulting Group and successfully identified 11 strategic transition levers across the overall value chain of buildings. These particular levers, in combination, have the capability to unlock more than 80% of the industry’s abatement potential and provide accessibility to a USD 1.8 trillion industry opportunity. Besides, buildings are significantly responsible for 37% of worldwide carbon dioxide emissions, while rapid urbanization across emerging economies is increasing, thus uplifting the market expansion.

- Massive infrastructure pipelines: The presence of government-funded and sustained city-building programs across regions, such as the Asia Pacific, is the ultimate engine of bulk admixtures consumption, which is positively impacting the market. As stated in an article published by OECD in 2026, the gap between present levels of infrastructure investment and the level demanded to achieve the Sustainable Development Goals is projected to grow by more than USD 18 trillion by the end of 2040. This particular infrastructure investment caters to a severe pathway towards an inclusive and fair shift to net-zero, while expanding resilience to the climate change impact that tends to address biodiversity pollution and loss. Therefore, based on all these factors, the market is gaining increased exposure.

- Growing emphasis on construction durability: Private developers and governments are readily prioritizing the long-lastingness of assets for reducing maintenance expenses, which is positively uplifting the market. As stated in an article published by Next Sustainability in 2024, in terms of durability, concrete consumes an estimated 70% of Portland cement, while the remaining 305 is utilized for other cement-based materials, including grout and mortar. Besides, over 4 billion tons of Portland cement are currently produced every year globally, along with an annual increase of almost 23% predicted by the end of 2050. This is highly driven by rapid urbanization and a surge in population, thus making it suitable for fueling the market’s upliftment.

Challenges

- Infrastructure and logistics constraints in emerging economies: While emerging nations, particularly in the Asia Pacific and Africa, represent the fastest-growing regions for construction additives, they also present formidable infrastructure and logistics challenges that constrain the construction additives market expansion. The transportation of chemical additives requires specialized handling, temperature-controlled environments, and strict adherence to safety protocols that are often lacking in developing regions. Poor road conditions, unreliable power supplies, and inadequate port facilities create supply chain bottlenecks that can delay deliveries by weeks or months, disrupting construction schedules and damaging manufacturers' reputations.

- Competition from substitutes and traditional construction methods: The market faces persistent competition from traditional construction methods and alternative materials that threaten to capture market share in specific applications. In many developing regions, conventional construction techniques relying on plain concrete, lime-based mortars, or locally sourced materials remain deeply entrenched due to lower upfront costs, familiarity among local workers, and resistance to change within conservative construction industries. Contractors and builders, particularly those serving the residential sector, may view chemical additives as unnecessary expenses rather than long-term investments in durability and performance.

Construction Additives Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.2% |

|

Base Year Market Size (2025) |

USD 28.8 billion |

|

Forecast Year Market Size (2035) |

USD 58.5 billion |

|

Regional Scope |

|

Construction Additives Market Segmentation:

Waterproofing Chemicals Segment Analysis

The liquid-applied membranes segment in the construction additives market is anticipated to garner the highest share of 60.7% by the end of 2035. The segment’s upliftment is highly propelled by its superior performance characteristics and application versatility. These advanced systems, applied as a liquid coating that cures to form a seamless, fully bonded protective layer, have revolutionized waterproofing practices across roofing, underground construction, walls, and wet areas. The technology's dominance stems from its fundamental advantage over traditional sheet membranes. Besides, the elimination of seams and joints creates a monolithic barrier with no potential weak points where water infiltration typically occurs.

Fibers Segment Analysis

The steel fibers sub-segment, which is part of the fibers segment, is projected to account for the second-highest share in the market during the forecast period. The sub-segment’s growth is highly driven by its importance for enhancing the toughness of concrete, strength, and durability, along with effectively improving structural integrity and controlling cracking. According to official statistics published by NLM in April 2022, at present, nearly 300,000,000 metric tons of fibers are utilized for reinforcing concrete. Based on this, steel fiber is the most utilized fiber, accounting for almost 50% of the overall ton utilization, which is followed by 20% of polypropylene, 5% of glass, and 25% of other fiber types. Besides, almost 600,000 tons of tires are effectively disposed to landfill in Europe every year, thereby denoting a positive upliftment of the sub-segment for offering an alternative fiber material.

Adhesives & Sealants Segment Analysis

By the end of the stipulated timeline, the polyurethane-based sub-segment, part of the adhesives and sealants segment in the market, is expected to hold the third-highest share. The sub-segment’s development is highly propelled by boosting structural integrity, durability, and energy efficiency. As per an article published by the MDPI in May 2025, the polyurethane industry is significantly categorized into 39% of flexible foams, which is followed by 26% of rigid foams, 13% of coatings, 12% of elastomers, 7% of adhesives, and 3% of others. Moreover, the worldwide polyurethane industry size was worth USD 78.1 billion as of 2023, and is further predicted to expand at a yearly growth rate of 3.9% by the end of 2030. The yearly production and utilization of polyurethane is increasing globally, owing to outstanding characteristics, which is fueling its demand.

Our in-depth analysis of the construction additives market includes the following segments:

|

Segment |

Subsegments |

|

Waterproofing Chemicals |

|

|

Fibers |

|

|

Adhesives & Sealants |

|

|

Mineral Additives |

|

|

Chemical Additives |

|

|

Repair & Rehabilitation |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Construction Additives Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the construction additives market is anticipated to garner the largest share of 42.6% by the end of 2035. The market’s upliftment in the region is highly attributed to unprecedented infrastructure growth, government-funded manufacturing strategies, rapid urbanization, escalation in construction activities, and energy efficiency implementation. According to official statistics published by Energy Economics in October 2024, there has been a demonstration that implementing energy policies in the region significantly correlates with an average surge in energy efficiency by 0.158%. However, the regional impact relies on policies displayed as strategies, regulations, or laws. Besides, the overall region’s average energy efficiency is 0.34, with a continuous upward trend. Moreover, improving aggregate energy reforms has led to substantial energy savings, averaging 0.15 quadrillion, which is positively impacting the market growth.

The construction additives market in China is growing significantly, owing to the unparalleled upscaling of construction and manufacturing activities, being the largest producer of construction chemicals, and wide-ranging industrialization across different end use sectors, such as automotive, packaging, and electronics. As per an article published by NLM in March 2024, there has been an increase in the number of registered chemicals to 204 million, and it is further continuing to grow at a suitable rate of more than 10 million every year. For instance, the country has readily emerged as one of the largest producers of chlorinated paraffins and polyfluoroalkyl, accounting for an estimated 37% and 40% of the worldwide cumulative production and utilization, respectively. Therefore, with this upliftment in the chemical industry, the market in the country is gradually expanding.

The aspects of infrastructure investment, policy support, demographic expansion, urbanization, industrialization, green construction activities, and infrastructure development are certain factors that are responsible for bolstering the market in India. As stated in an article published by the India Investment Grid in October 2025, the construction industry in the country contributes nearly 8% of the domestic GDP, and significantly boasts a valuation of roughly USD 126 billion. This pivotal sector is effectively attributed to strong investments in infrastructure, which has propelled the domestic construction equipment industry to an outstanding yearly growth rate of 30%. Besides, the 2023 Union Budget accounts for establishing the Urban Infrastructure Development Fund (UIDF), with a yearly infusion of USD 1.2 billion, thus bolstering the market development.

North America Market Insights

North America in the construction additives market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the wide-ranging construction chemicals, expansion in repair and rehabilitation by utilizing innovative chemical additives, and strategic investments in clean technological manufacturing. According to official statistics published by the U.S. Department of the Treasury in June 2023, the real manufacturing construction expenditure in the U.S. by type amounted for USD 84 billion as of 2022, which further reached USD 166 billion in 2023 between January and April. Additionally, this particular rise in spending commenced after the passing of the CHIPS Act and other policies readily contributing to construction spending, thereby making it suitable for developing the market in the overall region.

The construction additive market in the U.S. is gaining increased traction, owing to the combination of federal infrastructure investment, technological innovation, and climate resilience requirements in construction methodologies, along with a strong rebound in housing starts. As per an article published by The Associated General Contractors (AGC) of America in 2026, construction is regarded as one of the major contributors to the country’s economy. In addition, the country comprises over 919,000 construction establishments, particularly in the first quarter of 2023. Moreover, the overall construction industry also employs 8.0 million employees and develops almost USD 2.1 trillion worth of structures annually. Therefore, with such developments in the overall industry, there is a huge growth opportunity and expansion of the market in the country.

The aspects of provincial and federal infrastructure programs, robust policies towards sustainable construction materials, extreme climate adaptation requirements, as well as the government’s commitment to infrastructure renewal and public projects, are factors that are boosting the market in Canada. Based on the September 2025 Natural Resources Canada article, the country comprised 504 major projects in September 2024. These particular projects have been under construction for more than 10 years in terms of mining, forest, and energy industries, accounting for a combined potential capital valuation of USD 632.6 billion. Therefore, this demonstrates an increase from 2023 in both 493 projects as well as a surge in the capital value by more than 10.9%, amounting to USD 570.5 billion, thus driving the market growth.

Energy Project Trends Analysis in Canada (2021-2024)

|

Components |

2021 |

2022 |

2023 |

2024 |

|

Overall Energy Projects |

305 (USD 450 billion) |

320 (USD 427 billion) |

343 (USD 472.3 billion) |

340 (USD 510.0 billion) |

|

Oil and Gas-based |

106 (USD 339 billion) |

96 (USD 294 billion) |

87 (USD 318.6 billion) |

67 (USD 296.2 billion) |

|

Electricity Generation and Transmission |

176 (USD 102 billion) |

179 (USD 106 billion) |

182 (USD 97.4 billion) |

188 (118.9 billion) |

|

Other |

23 (USD 8.9 billion) |

45 (USD 26.6 billion) |

74 (USD 56.2 billion) |

85 (USD 94.9 billion) |

Source: Natural Resources Canada

Europe Market Insights

Europe in the construction additives market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by strict sustainability mandates, technological advancements, aging infrastructure renewal, modernized construction across infrastructure, commercial, and residential segments, and suitable regulatory frameworks for product development. According to official statistics published by the Europe Commission in July 2025, the construction industry in the region has been subjected to structural transformation, fueled by digital and twin green transitions, accounting for a yearly growth rate of 2.1%. This particular growth is effectively underpinned by public-based investments that are focused on resilient infrastructure, cost-effective housing, and energy-efficient renovation, thus proliferating the market expansion.

The construction additives market in Germany is gaining increased exposure, owing to the existence of its unparalleled manufacturing ecosystem, the export strength for adhesive glue, proactive support for chemical industry innovation through sustainable manufacturing, and industrial decarbonization funding. As stated in a data report published by the OEC in 2024, the export of glues and adhesives in the country amounted to USD 125 million, while the import valuation was worth USD 79.1 million. Besides, as per an article published by the Clean Energy Wire in March 2024, the 12 largest chemical producers in the country cause almost 23 million tons of carbon emissions as of 2022, which is approximately 3% of the nation’s overall yearly greenhouse gas output, thereby demanding sustainability approaches for the market growth.

The regional funding aspect, infrastructure modernization, catch-up upliftment in construction practices, and substantial fund allocation for making advancements in transport networks, optimizing building energy efficiency, and upgrading public infrastructure are factors that are proliferating the construction additives market in Romania. Based on government estimates published by the ITA in July 2025, the country’s rail network comprises an estimated 10,600 kilometers, of which nearly 4,000 kilometers are electrified, and meanwhile, just 20% of the network is double-tracked. Besides, average speeds on a few major routes remain below 60 kilometers per hour, owing to outdated signaling and deferred maintenance. Besides, more than USD 8 billion in the overall region and national investments have been earmarked with USD 3 billion in March 2025, thus driving the market growth.

Key Construction Additives Market Players:

- BASF SE (Germany)

- Sika AG (Switzerland)

- Dow Inc. (U.S.)

- MAPEI S.p.A. (Italy)

- Saint-Gobain S.A. (France)

- RPM International Inc. (U.S.)

- GCP Applied Technologies Inc. (U.S.)

- Fosroc International (UAE) [Operations in Malaysia, India]

- W.R. Grace & Co. (U.S.)

- Evonik Industries AG (Germany)

- Henkel AG & Co. KGaA (Germany)

- H.B. Fuller Company (U.S.)

- Arkema S.A. (France)

- Sanyo Chemical Industries, Ltd. (Japan)

- Kao Corporation (Japan)

- Sobute New Materials Co., Ltd. (India)

- Pidilite Industries (India)

- Euclid Chemical Company (U.S.)

- Mapei Construction Products India Pvt. Ltd. (India)

- Fosroc Malaysia Sdn Bhd (Malaysia)

- CEMEX (Mexico)

- Saint-Gobain Group (France)

- Clariant (Switzerland)

- Sika (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF SE is a dominant force in the market, leveraging its extensive portfolio of high-performance chemical solutions to enhance concrete durability and workability globally. The company's strategic focus on sustainability drives the development of innovative, low-carbon admixtures that help reduce the environmental footprint of modern infrastructure projects.

- Sika AG stands as a global market leader, renowned for its comprehensive range of concrete admixtures, sealants, and waterproofing systems that address complex construction challenges. Through continuous investment in local manufacturing and technical expertise, the company ensures tailored solutions that meet diverse regional construction standards and climatic demands.

- Dow Inc. contributes significantly to the construction sector through its advanced material science expertise, producing high-quality polymer-based additives that improve the performance and longevity of building materials. The company's commitment to innovation focuses on developing sustainable solutions that enable energy efficiency and durability in residential and commercial construction applications.

- MAPEI S.p.A. has established itself as a premier provider of construction additives, offering an extensive line of chemical products for concrete, adhesives, and protective coatings used worldwide. The company's dedication to research and development results in cutting-edge formulations that address the evolving needs of architects, contractors, and engineers across diverse construction projects.

- Saint-Gobain S.A. delivers comprehensive construction solutions through its expertise in high-performance materials, including advanced additives that enhance the sustainability and functionality of building systems. The company's holistic approach integrates additive technologies into broader construction solutions, promoting resource efficiency and improved living comfort in buildings across global markets.

Here is a list of key players operating in the global market:

The global construction additives market is characterized by a consolidated competitive landscape dominated by large multinational specialty chemical corporations with extensive R&D capabilities and global distribution networks. Europe-based and North America-specific players, particularly Swiss-based Sika AG and German-based BASF SE, maintain leadership positions through continuous product innovation and strategic acquisitions to expand their geographic footprint and product portfolios. Key players are increasingly focusing on sustainability-driven strategies, developing low-carbon and bio-based additives to tighten environmental regulations. Besides, in January 2023, CEMEX unveiled the line of bio-based admixtures solutions, which has the ability to diminish carbon footprint by 70%, thereby effectively proliferating the construction additives industry.

Corporate Landscape of the Construction Additives Market:

Recent Developments

- In July 2025, Saint-Gobain Group acquired the complete business assets of Interstar Materials Inc. to effectively strengthen its extension in the construction chemical industry of North America.

- In December 2024, Clariant expanded its Cangzhou production facility for manufacturing multifunctional additive Nylostab S-EED, which is the latest production line by completely acquiring Hebei Province of China, in association with its localized partner, Beijing Tiangang Auxiliary Co., Ltd.

- In May 2023, Sika significantly acquired the MBCC business for generating USD 2.6 billion in net sales as of 2022, leading to yearly synergies projected to range between USD 201 million and USD 227 million by the end of 2026, which is suitable for driving sustainable transformation for the construction industry.

- Report ID: 8457

- Published Date: Mar 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.