Composites Market Outlook:

Composites Market size was valued at USD 112.9 billion in 2025 and is projected to reach USD 243.1 billion by the end of 2035, rising at a CAGR of 8.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of composites is estimated at USD 122.9 billion.

The global market is poised for immense growth based on factors such as expanding applications in aerospace, automotive, wind energy, marine, and construction industries. There has been a growing demand for lightweight, high-strength materials to improve fuel efficiency and performance, which continues to accelerate adoption. As per the data kept forward by the U.S. Department of Energy (DOE) in April 2023, the Institute for Advanced Composites Manufacturing Innovation (IACMI) funding was renewed by the DOE, which marks the first clean energy institute renewal under its Advanced Materials and Manufacturing Technologies Office. The first-year investment was USD 6 million, and a total of USD 70 million in DOE support, along with USD 180 million from partners. IACMI continues to drive R&D and commercialization in composites manufacturing.

Furthermore, the rising investments to reduce greenhouse gas emissions and building renewable energy infrastructure, particularly wind turbine blade manufacturing, stimulate consistent growth in the market. In July 2024, the U.S. Environmental Protection Agency (EPA) awarded a total amount of USD 6 million to the American Composites Manufacturers Association (ACMA) and the Institute for Advanced Composites Manufacturing Innovation , with the main goal ofreducing embodied greenhouse gas emissions in construction materials. The partnership will deploy a life cycle assessment–environmental product declaration generator, create new and updated Product Category Rules, and educate more than 200 manufacturers and customers on sustainable practices. Therefore, such initiatives combine industry investment with academic collaboration, positively impacting market expansion.

Key Composites Market Insights Summary:

Regional Highlights:

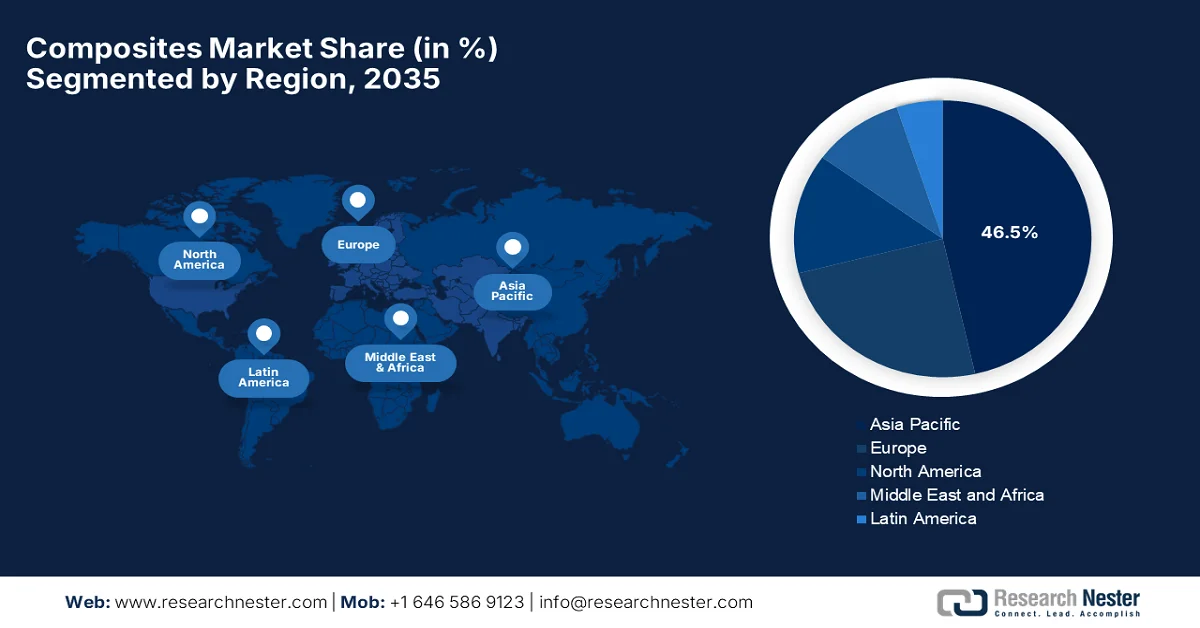

- Asia Pacific in the composites market is anticipated to secure the largest revenue share of 46.5% by 2035, propelled by robust industrialization and rising demand across construction, automotive, and renewable energy sectors.

- Europe is projected to witness substantial growth by 2035, stimulated by stringent emission reduction regulations and increasing adoption of recyclable and bio-based composites across key manufacturing industries.

Segment Insights:

- The Glass fiber segment of the composites market is projected to account for a dominant 52.5% share by 2035, attributed to its cost-effectiveness and high-volume utilization across construction and wind energy applications.

- The Layup segment is expected to command a considerable share by 2035, fueled by its ease of use, design flexibility, and cost-efficient production processes.

Key Growth Trends:

- Stringent environmental and fuel‑efficiency regulations

- Growth in renewable energy

Major Challenges:

- Recycling and sustainability issues

- Complex manufacturing processes

Key Players: Hexcel Corporation (U.S.), Owens Corning (U.S.), Huntsman Corporation (U.S.), Toray Industries, Inc. (Japan), Teijin Limited (Japan), Mitsubishi Chemical Corporation (Japan), SGL Carbon SE (Germany), Solvay S.A. (Belgium), Gurit Holding AG (Switzerland), DSM (Netherlands), UPM-Kymmene Corporation (Finland), Nippon Sheet Glass Co., Ltd. (Japan), Hyosung Advanced Materials (South Korea), Kineco Kaman Composites India Pvt. Ltd. (India), Reliance Composites (India), Advanced Composite Corporation (Japan), Quickstep Holdings Limited (Australia), Petronas Chemicals Group Berhad (Malaysia), Exel Composites Oyj (Finland).

Global Composites Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 112.9 billion

- 2026 Market Size: USD 122.9 billion

- Projected Market Size: USD 243.1 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (46.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, South Korea, Brazil, Mexico, Italy

Last updated on : 23 February, 2026

Composites Market - Growth Drivers and Challenges

Growth Drivers

- Stringent environmental and fuel‑efficiency regulations: The regulations for automotive fuel economy and aircraft emissions are compelling manufacturers to adopt lightweight composite materials to meet strict fuel efficiency targets and lower carbon footprints. As stated by the U.S. Environmental Protection Agency, it has finalized greenhouse gas emissions standards for passenger cars and light trucks covering model years 2023 to 2026. These rules are the strongest ever for the light-duty sector and are expected to avoid more than 3 billion tons of emissions through 2050 by delivering around USD 190 billion in net benefits. In addition, they set the stage for future standards beyond 2027, supporting the transition toward zero-emission vehicles under the Clean Air Act, hence suitable for bolstering the composites market growth.

- Growth in renewable energy: Composites are highly essential in wind energy, especially in terms of turbine blades, which require materials that are strong, lightweight, and fatigue-resistant. Therefore, expansion in wind capacity worldwide efficiently boosts demand in the market. According to the official statistics published by the IRENA Renewable Capacity Statistics 2025 reports that by the end of 2024, renewables made up 46% of global installed power capacity, wherein 585 GW of new renewable capacity was added, including 113 GW from wind. It also underscores that this marked the largest annual increase to date, though deployment remains uneven across regions. This growth from wind energy denotes there is a huge growth potential for the market in the upcoming years.

- Expansion in aerospace & defense applications: Aerospace continues to be a major consumer of composites due to the need for more durable materials in aircraft structures, UAVs, and advanced defense systems. This particular trend deliberately supports the composites market growth in the upcoming years. In this context, in April 2023, the U.S. Navy’s 2023 SBIR stated that its topic N232-086 is looking to develop novel multifunctional and lightweight materials with a main goal to enhance the performance of small unmanned aerial vehicles (UAVs) by integrating functions such as sensors, circuitry, and structural components to reduce weight and improve mission capability. This particular program is focused on advanced materials and structural concepts that advance UAV design beyond conventional materials, with applications in Groups 1 to 3 UAVs, hence denoting a positive market outlook.

Challenges

- Recycling and sustainability issues: This factor hampers the growth of the market, especially in terms of end-of-life disposal. The thermoset composites cannot be easily remelted or reshaped, making recycling extremely complex and expensive. The environmental regulations are tightening across different nations, which results in pressure on manufacturers to develop circular economy solutions. On the other hand, landfilling composite waste is being restricted in both emerging and established economies. Besides, the wind turbine blades and aerospace components represent large-scale disposal concerns due to their size and material complexity. Furthermore, the absence of established recycling infrastructure also complicates waste management, causing a hindrance to market expansion.

- Complex manufacturing processes: The process of manufacturing composite materials is considered to be complex and often time-consuming with autoclave curing, resin transfer molding, and filament winding. These processes necessitate specialized equipment, controlled environments, and skilled work personnel, thereby increasing operational costs. When compared to metal fabrication, composite production cycles are longer, which reduces output efficiency for high-volume industries. Also, the aspect of quality control is more challenging, as defects like voids or delamination may not be visible externally, making adoption critical in the composites market. In addition, maintaining consistent material properties across batches can be difficult. Therefore, these manufacturing complexities limit scalability and hinder faster market penetration.

Composites Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 112.9 billion |

|

Forecast Year Market Size (2035) |

USD 243.1 billion |

|

Regional Scope |

|

Composites Market Segmentation:

Fiber Type Segment Analysis

Glass fiber is anticipated to emerge as the strongest subsegment with the largest share of 52.5% in the market by 2035. The dominance of the subtype is attributable to its cost-effectiveness and high-volume use in construction and wind energy. In September 2025, Indus Towers announced that it had partnered with IIT Madras to pioneer research on glass fiber reinforced polymer structural sections, with a collective goal to develop lightweight, corrosion-resistant, and high-performance alternatives to conventional steel for telecom infrastructure. This particular initiative is a part of Indus Towers’ CSR program, Pragati, which focuses on mechanical performance, durability, and lifecycle sustainability. Therefore, such industry-academia collaborations are setting new benchmarks for structural design, contributing to a wider segment scope.

Manufacturing Process Segment Analysis

By the conclusion of the forecast period, the layup is expected to lead with a considerable share in the manufacturing process segment. The growth of the subtype is mainly propelled by the ease of use, design versatility, and cost-efficient production processes. On the other hand, techniques such as hand layup and spray layup are commonly utilized to manufacture large or complex composite structures, making them highly suitable for marine, construction, and transportation applications that have moderate production volumes. In addition, the low tooling costs, customization potential, and capability to produce thick, high-strength components readily enhance their appeal for small and mid-sized manufacturers. Furthermore, their wide-ranging applicability ensures continued strong revenue contribution for the composites market over the discussed timeframe.

Application Segment Analysis

The automotive & transportation, which is a part of the application segment, is predicted to grow at a significant rate in the market during the stipulated timeframe. The stringent emission regulations and the growing demand for lightweight vehicle components are the key factors behind this leadership. Composites are utilized in exterior panels, chassis parts, and interior structures to reduce vehicle weight, whereas the rising electric vehicle production has also boosted demand for improved composites to enhance battery efficiency and driving range. As per the official statistics published by IEA, global electric vehicle sales were at a surge, exceeding 17 million units in 2024 and are projected to surpass 20 million in 2025, which is an indication that more than 25% of global car sales. It also mentioned that China is dominating this sector, wherein EVs account for almost half of all car sales in 2024 and are projected to reach 60% in 2025. Strong growth is also observed in emerging economies, with EV sales outside China expected to reach 1 million units in 2025.

Global Electric Vehicle Sales and Market Share Trends 2024-2025

|

Metric |

2024 |

2025 (Projected) |

Notes |

|

Global EV sales |

17 million |

>20 million |

>25% of total car sales |

|

EV share in China |

50% |

60% |

1 in 10 cars on Chinese roads is electric (2024) |

|

EV sales in emerging economies (excluding China) |

0.6 million |

1 million |

Asia & Latin America are key growth regions |

|

Electric truck sales (global) |

+80% growth |

- |

China accounts for >80% of sales. |

Source: IEA

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Manufacturing Process |

|

|

Application |

|

|

Resin Type |

|

|

Matrix Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Composites Market - Regional Analysis

APAC Market Insights

The Asia Pacific composites market is expected to register its dominance, capturing the largest revenue share of 46.5% during the discussed timeframe. The region’s leadership is mainly propelled by strong industrialization, construction, automotive, and renewable energy demand. The region is one of the leading producers and consumers of composites, encouraging more investments from domestic and foreign firms. In April 2024, UBE Corporation announced that it had launched new composite products incorporating recycled carbon fiber to reduce greenhouse gas emissions and environmental impact. These products combine recycled carbon fiber with various nylons, enhancing functionality for applications in automotive and sports sectors while lowering energy use and production emissions, hence attracting more players to establish their footprint in this field.

The mass market automotive use, growing wind energy programs, and extensive infrastructure projects that use composite materials are the main driving factors for the composites market in China. Also, the country is identified as a leader in the region, largely attributable to its construction and transportation sectors. According to the reports published by USCC in November 2025, the country's progress in new materials under Made in China 2025 is mixed, and it leads in terms of production scale, especially in composites such as carbon fiber. Despite challenges in measuring market impact due to the breadth of new materials, the country is the world’s largest producer of mid-range carbon fiber, owing to the demand for wind turbine blades and industrial applications. Government support through manufacturing innovation centers, preferential policies, and strategic investments has enabled rapid capacity growth.

China Carbon Fiber and New Materials Production Statistics (2019 to 2028); Global Share, Capacity, and Growth Trends

|

Metric |

Value / Year |

Notes |

|

Global share of mid-range carbon fiber production |

43% |

As of November 2024 |

|

Annual carbon fiber production capacity |

120,000 tons |

2023, up from 20,000 tons in 2019 |

|

Domestic share of Chinese carbon fiber |

>60% |

2023, up from 12.5% in 2015 |

|

Xinjiang carbon fiber facility projected capacity |

50,000 tons |

By 2028 |

|

Graphene powder production goal achieved |

10,000 tons |

Target for 2025 met in 2021 |

Source: USCC

The renewable energy installations, especially wind turbine blades, coupled with growing automotive composites demand, are propelling the upliftment of the market in India. Simultaneously, government backing for infrastructure development incorporates composite materials for modern construction techniques, leading to a progressive demand in this field. From 2023 to 2026, the Department of Science and Technology, India, is funding research at the National Institute of Technology Jamshedpur for the development of self-healing composite materials with a total budget of USD 11,500. This particular project looks into carbon fiber laminates, microcapsules with rejuvenators, graphene or HMMM hybrid shells, and supramolecular elastomers to repair microcracks and enhance structural longevity with the main aim to improve reliability in remote and critical applications. Hence, such an R&D ecosystem & strong imports denote that there is a lucrative growth opportunity for the market in the country.

India Glass Fiber (Including Glass Wool) and Article (HS 701990) Imports by Country 2023: Officially -Reported Trade Data & Top Suppliers

|

Partner Country |

Trade Value (1000 USD) |

Quantity (Kg) |

|

China |

54,604.31 |

24,927,700 |

|

U.S. |

13,400.09 |

507,905 |

|

Germany |

6,195.21 |

445,943 |

|

Sweden |

2,041.29 |

341,987 |

|

Italy |

1,706.06 |

77,382 |

|

UK |

1,573.01 |

58,142 |

|

Spain |

1,512.29 |

203,588 |

|

Korea, Rep. |

1,489.00 |

217,591 |

|

Mexico |

1,199.61 |

128,063 |

Source: WITS

Europe Market Insights

The Europe composites market is considered to be one of the most influential and mature landscapes, mainly driven by the presence of manufacturing hubs and emission reduction regulations. The automotive OEMs in the region are incorporating composites into structural components, whereas emphasis on recyclable and bio-based composites supports sustainability objectives. The European Circular Composites Alliance, which was introduced in 2025 by the European Composites Industry Association in Belgium, aims to establish a circular economy for composites across the region. This platform efficiently facilitates knowledge sharing, collaboration, and collective action to promote sustainable value chains, set targets for recycled composite use, and develop circular design standards. In addition, the industry stakeholders across sectors such as aerospace, construction, and policy can join ECCA and participate in its specialized working groups to improve circularity in composites.

Germany composites market is augmenting its leadership in Europe, effectively fueled by its engineering sectors and R&D capabilities. Advances in terms of industrial automation improve production efficiency, and sustainability and recycling considerations shape material choices. In July 2025, the Fraunhofer Institute for Applied Polymer Research (IAP), in collaboration with Brandenburg University of Technology Cottbus-Senftenberg, announced that it is developing next-generation sustainable carbon fibers based on cellulose by combining high mechanical, electrical, and thermal performance with eco-friendly production. This project is supported by the country’s Federal Ministry for Economic Affairs and Energy, and is part of the Carbon Lab Factory Lausitz, aiming to scale pilot production and create a full value chain from raw materials to technical components, hence suitable for bolstering the market’s growth and exposure.

The shift toward a net-zero economy is driving growth in the UK market. The sector is modernizing from manual methods to automated, high-rate production with digital integration to boost efficiency. The country’s market is strongly backed by research centers and organizations, whereas the supply chain is adopting circular economy practices, including recyclable resins and carbon fiber reclamation. In June 2025, NCC confirmed the location of its open-access Carbon Fibre Development Facility at Cygnet Texkimp’s site in Northwich, Cheshire West, which is supported by the UK government’s industrial strategy and funded by the Department for Science, Innovation and Technology (DSIT). The facility will house two digitally-enabled development lines, enabling carbon fiber innovation, supporting advanced materials, defence, aerospace, and energy sectors, and training the next generation of chemists and engineers, hence suitable for standard market growth.

North America Market Insights

The North America composites market is growing exponentially on account of huge adoption in aerospace, defense, and automotive sectors. The region benefits from well-established production capacity, R&D in multifunctional materials, and strong federal support for innovation in improved composites processes. In this regard, the U.S. Department of Defense, in November 2023, reported that it allocated a total amount of USD 3.7 million to Qarbon Aerospace through the industrial base analysis and sustainment program to design and manufacture advanced lightweight thermoplastic composite structures for defense aviation applications. The project is highly focused on components requiring icing protection, improving efficiency, durability, and repairability when compared to conventional systems. Therefore, this award strengthens domestic manufacturing capabilities and solidifies U.S. leadership in terms of composite technologies.

Aircraft modernization programs are the main factor increasing the demand for carbon fibers, thereby prompting a highly profitable business ecosystem for the U.S. composites market. On the other hand, improvements in manufacturing technologies enhance production efficiency, whereas substantial R&D investment continues to support innovation and the development of new materials. For instance, Mitsubishi Chemical Corporation in December 2025, notified that it has plans to expand its high-performance carbon fiber production at facilities in the U.S. and Japan with a collective goal meet growing demand from sports, aerospace, and hypercar sectors. The phased capacity enhancement, which is from 2025 to 2027, aims to approximately double current production, leveraging existing plants in Tokai, Japan, and Sacramento in the U.S., hence supporting industry growth and value creation in advanced composites.

The automotive and aerospace hubs, particularly around Ontario and Quebec, with a greater focus on creating lightweight structural materials drives growth in composites market in Canada. Progress in terms of renewable energy installations, particularly in wind power, supports demand for large composite structures such as turbine blades. In December 2023, the country’s government allocated the Composites Knowledge Network an amount of CAD 1 million (USD 740,000) under the strategic science fund to support the translation of advanced composites research into the country’s industry. This funding enables CKN to help small and medium-sized enterprises expand knowledge transfer initiatives such as the Knowledge in Practice Centre and AIM webinars and foster innovation in sectors such as aerospace, automotive, construction, health, and renewable energy.

Key Composites Market Players:

- Hexcel Corporation (U.S.)

- Owens Corning (U.S.)

- Huntsman Corporation (U.S.)

- Toray Industries, Inc. (Japan)

- Teijin Limited (Japan)

- Mitsubishi Chemical Corporation (Japan)

- SGL Carbon SE (Germany)

- Solvay S.A. (Belgium)

- Gurit Holding AG (Switzerland)

- DSM (Netherlands)

- UPM-Kymmene Corporation (Finland)

- Nippon Sheet Glass Co., Ltd. (Japan)

- Hyosung Advanced Materials (South Korea)

- Kineco Kaman Composites India Pvt. Ltd. (India)

- Reliance Composites (India)

- Advanced Composite Corporation (Japan)

- Quickstep Holdings Limited (Australia)

- Petronas Chemicals Group Berhad (Malaysia)

- Exel Composites Oyj (Finland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Hexcel Corporation is one of the leading suppliers of advanced composites, especially in terms of carbon fiber and honeycomb materials, serving aerospace, defense, and industrial sectors. The company benefits from its integration with major aerospace OEMs and its continuous investment in lightweight, high-performance materials.

- Toray Industries, Inc. is yet another prominent player in this field and is one of the largest global producers of carbon fiber and thermoplastic composites. The company benefits from a strong presence in aerospace, automotive, and energy sectors. In addition, Toray is focused on R&D, international expansion, and partnerships to accelerate the adoption of composites across industries.

- Solvay S.A. is based in Europe, which is specializing in high-performance thermoset and thermoplastic composites. The firm has a strong footprint in aerospace, automotive, and renewable energy applications. Tactical collaborations with aerospace OEMs and automotive manufacturers solidify its position in lightweight materials.

- Owens Corning is a central player in this field, which is serving the construction, automotive, and industrial sectors. The company has its strength in cost-effective, durable materials that support infrastructure and energy efficiency posiitioning it as a leading player in the composites industry.

- Teijin Limited is based in Japan, and it has expertise in carbon fiber, aramid fibers, and thermoplastic composites. It has a strong presence in aerospace, automotive, and industrial applications. The company is mainly focused on innovation in lightweight, high-strength materials and acquisitions, with a main goal to expand its international footprint.

Below is the list of some prominent players operating in the global market:

The composites market is witnessing an intense competition among established global leaders and emerging regional players. Companies such as Hexcel, Toray, and Solvay are dominating in terms of aerospace and automotive applications through their continued innovations in carbon fiber and thermoplastic composites. Acquisitions, joint ventures, and collaborations with startups are the major strategies opted for by the pioneers in this field to strengthen their market positions. For instance, in February 2026, Karman Space & Defense reported that it had completed the acquisition of Seemann Composites and MSC by forming its new Maritime Defense Systems end market to expand capabilities from deep sea to deep space. This particular deal strengthens Karman’s exposure to high-priority U.S. Navy programs, and along with the acquisitions, Karman increased its incremental term loan to USD 772 million at a reduced interest rate hence suitable for standard market growth.

Corporate Landscape of the Composites Market:

Recent Developments

- In January 2026, Cambium reported that it had secured USD 100 million in Series B funding, which was led by 8VC, and participation from investors Lockheed Martin Ventures and MVP Ventures, to accelerate advanced materials discovery and manufacturing in the U.S. and Europe.

- In December 2025, Toray Advanced Composites announced that its Toray Cetex TC1225 low-melt PAEK has achieved NCAMP qualifications, which allows it to expand its availability in semi-preg and reinforced thermoplastic laminate formats.

- In November 2024, Daikin Industries reported that it had invested in Advanced Composite Corporation, which specializes in aluminum-based metal matrix composites, to accelerate innovation in HVAC&R compressor parts.

- Report ID: 4570

- Published Date: Feb 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.