Circuit Protection Market Outlook:

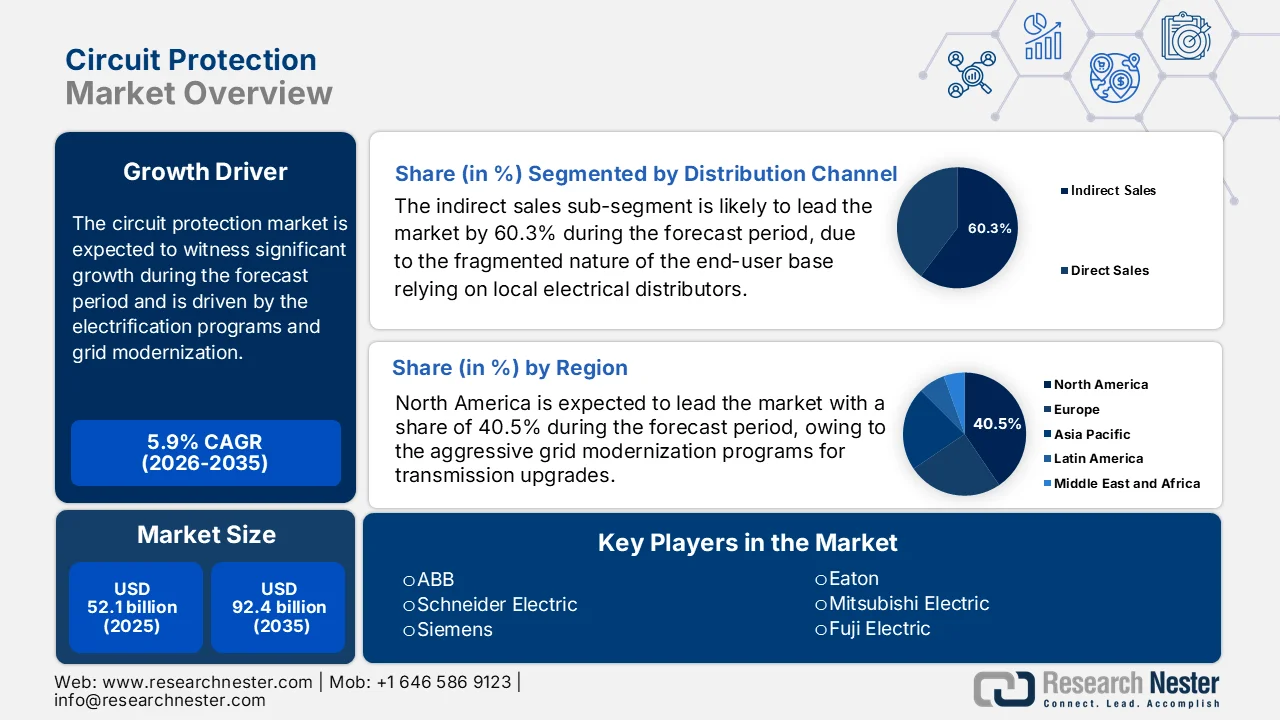

Circuit Protection Market size was valued at USD 52.1 billion in 2025 and is projected to reach USD 92.4 billion by the end of 2035, rising at a CAGR of 5.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of circuit protection is assessed at USD 55.2 billion.

Government infrastructure expansion, electrification programs, and grid modernization are increasing the demand for circuit protection components across transportation, industrial, and energy systems. According to the American Clean Power March 2025 data, the electricity demand in the U.S. is expected to grow by 35% to 50% by 2040 as electrification and digital infrastructure expand, requiring significant investment in power distribution equipment and digital infrastructure expand requiring significant investment in power distribution equipment and safety systems integrated with the protection components such as fuses, breakers, and relays. Moreover, the federal funding is surging for these deployments. The Alliance to Save Energy November 2021 report indicates that the U.S. Bipartisan Infrastructure Law allocates USD 65 billion for grid modernization and reliability, including investments in transmission expansion, resilience upgrades, and substation modernization, where circuit protection technologies are integral to equipment safety and operational continuity.

Additionally, the industrial electrification and renewable energy deployment are further reinforcing the demand for the circuit protection market. The March 2024 IRENA report indicates that the global renewable power capacity reached 3,870 GW in 2023, the highest annual increase recorded. Moreover, the renewable generation facilities require extensive protection systems across the inverters, transformers, switchgear, and grid interconnections to manage variable loads and prevent fault propagation. On the other hand, the grid disturbances and equipment failures remain a significant operational risk in high-capacity power systems, reinforcing the need for advanced protection mechanisms in substations, renewable plants, and distributed energy resources. These trends are expanding the procurement across utilities, industrial plants, and infrastructure projects where circuit protection components remain mandatory to maintain operational safety, protect capital equipment and comply with electrical safety standards across national power systems.

Key Circuit Protection Market Insights Summary:

Regional Highlights:

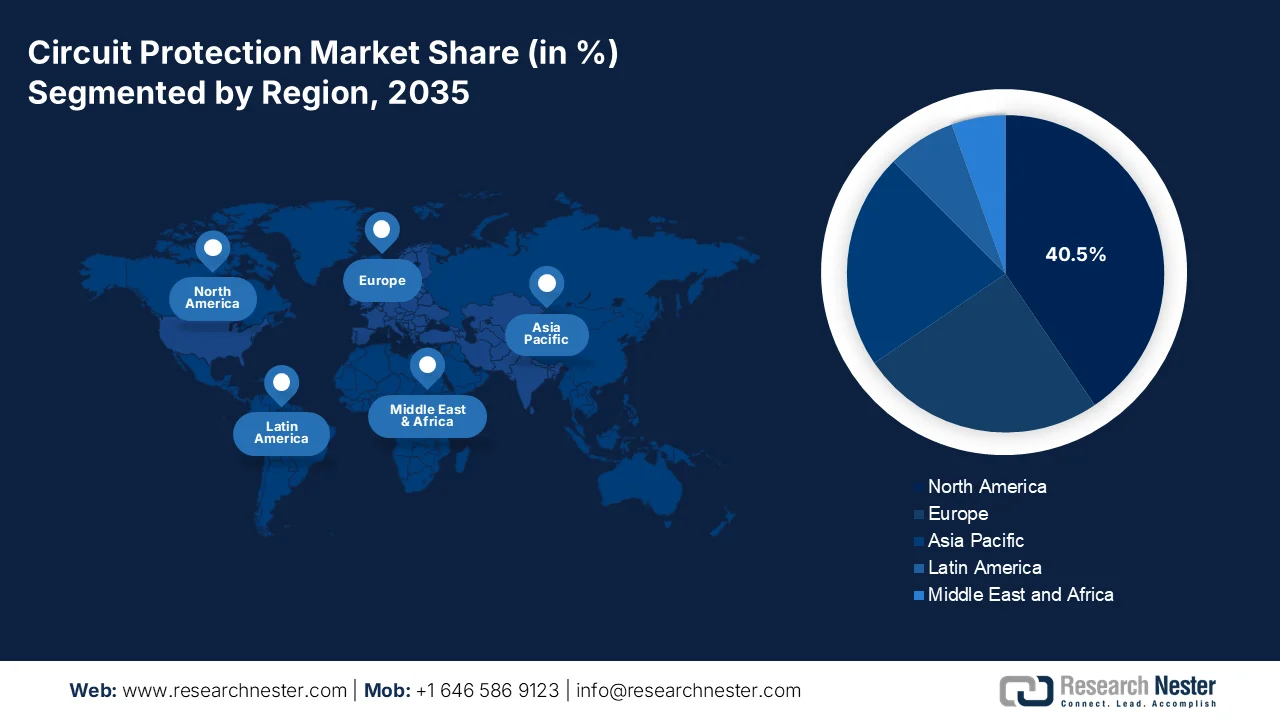

- North America in the circuit protection market is projected to hold a 40.5% share by 2035, attributed to extensive grid modernization initiatives, aging infrastructure replacement, and rising electrification needs

- Asia Pacific is expected to witness the fastest growth with a CAGR of 7.5% during 2026–2035, impelled by rapid industrialization, grid expansion, and strong electronics manufacturing demand

Segment Insights:

- The indirect sales segment in the circuit protection market is expected to command a 60.3% share by 2035, fueled by the fragmented end-user base relying on distributors for product availability and technical support

- The low voltage segment is anticipated to secure the leading share by 2035, propelled by its widespread deployment across residential, commercial, and industrial applications alongside rising demand for energy-efficient electrical systems

Key Growth Trends:

- Rising electricity demand from industrial electrification

- Rising EV charging infrastructure investment

Major Challenges:

- Tariff barriers and trade protectionism

- Reliability and failure risks

Key Players: ABB, Schneider Electric, Siemens, Eaton, Mitsubishi Electric, Fuji Electric, Panasonic Corporation, Littelfuse, TE Connectivity, Sensata Technologies, Bel Fuse Inc., Bourns Inc., E-T-A Elektrotechnische Apparate GmbH, OMRON Corporation, Legrand, Nexperia, LS Electric, Hager Group, Larsen & Toubro, Sécheron SA.

Global Circuit Protection Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 52.1 billion

- 2026 Market Size: USD 55.2 billion

- Projected Market Size: USD 92.4 billion by 2035

- Growth Forecasts: 5.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 17 March, 2026

Circuit Protection Market - Growth Drivers and Challenges

Growth Drivers

- Rising electricity demand from industrial electrification: Industrial electrification is driving the demand for the market in manufacturing plants, processing facilities, and heavy industries. Moreover, the electrified industrial systems rely on circuit protection to safeguard the motors, power converters, and automation equipment. According to the IEA 2024 data, the global electricity demand increased by 2.2% in 2023 and is expected to surge due to the electrification in manufacturing and digital infrastructure expansion. Industrial electrification initiatives supported by governments, including electrified steel, chemical processing, and battery manufacturing, require highly reliable circuit protection systems to prevent downtime and equipment damage. These developments are expanding procurement opportunities for circuit protection components across the industrial control panels, motor drives, and large-scale electrical distribution systems.

- Rising EV charging infrastructure investment: The rapid expansion of EV charging networks is creating a strong demand for the market as these technologies are mostly used in charging stations, power conversion equipment, and distribution panels. The high-power charging systems require robust electrical protection to prevent short circuits, overcurrent conditions, and voltage instability. Governments worldwide are allocating significant funding for EV infrastructure. According to the U.S. Department of Energy, February 2022 data, the U.S. National Electric Vehicle Infrastructure Program provides USD 5 billion to deploy EV charging stations, surging the installation of high-capacity charging systems that require integrated circuit protection devices. As EV adoption increases and fast-charging technologies expand, demand for advanced circuit protection components is expected to grow in transportation infrastructure.

- Increasing investment in power transmission: Large-scale investment in transmission and distribution infrastructure is expanding the installed base of electrical protection systems across the substation transformers and power distribution networks. The circuit protection components are vital for isolating the faults and preventing cascading failure in high-voltage systems. Moreover, the global investment in electricity networks is reflecting the growing need to strengthen the power infrastructure and integrate renewable energy sources. The governments are prioritizing the grid expansion to support the electrification and energy security. These investments are creating sustained demand for the circuit protection devices used in the utility-scale power infrastructure.

Challenges

- Tariff barriers and trade protectionism: Global trade tensions create significant cost disadvantages for the new players in the circuit protection market. The sharp escalation of U.S. tariffs and resulting trade tensions significantly affects the electrical and electronics sector, with key components such as semiconductors and rare earth metals facing heavy duties. Moreover, the growth reflects a modest reduction mainly due to the impact of tariffs. This directly affects the manufacturers via restricted access to surge protection components impacting electronics manufacturing and power grid reliability. Top companies are responding by shifting the assembly operations to tariff-exempt nations and redesigning products to reduce the reliance on restricted materials.

- Reliability and failure risks: Circuit breaker failures have serious potential to harm both people and equipment. The circuit breakers have been involved in numerous serious incidents in the petroleum industry, with underlying causes including the aging and residual life assessments, technical weakness in design, misdimensioning, and missing barriers in the event of failure. For new players, proving reliability is extremely difficult. Companies in the market must demonstrate that their products can withstand high-power environments where powerful electric arcs can occur when current paths are interrupted. Existing players use decades of field performance data, while the new players lack trust capital.

Circuit Protection Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.9% |

|

Base Year Market Size (2025) |

USD 52.1 billion |

|

Forecast Year Market Size (2035) |

USD 92.4 billion |

|

Regional Scope |

|

Circuit Protection Market Segmentation:

Distribution Channel Segment Analysis

The indirect sales are dominating and are projected to hold the largest revenue share of 60.3% by the end of 2035 in the circuit protection market. This dominance is driven by the fragmented nature of the end-user base, where small to medium enterprises and residential contractors rely on the local electrical distributors for immediate availability of components such as circuit breakers and fuses. These intermediaries provide a critical value via inventory management technical support and the consolidation of products from multiple manufacturers into a single order. According to the FRED March 2026 data, the total sales of electronic shopping and mail order houses for the period December 2025 reached USD 156,581, underscoring the growing reliance on the indirect digital channels for component procurement.

Retail Sales: Electronic Shopping and Mail-Order Houses

|

Year (December) |

Units (USD millions) |

|

2018 |

62,603 |

|

2019 |

79,342 |

|

2020 |

101,597 |

|

2021 |

108,286 |

|

2022 |

115,096 |

|

2023 |

129,134 |

|

2024 |

146,567 |

|

2025 |

156,581 |

Source: FRED March 2026

Voltage Rating Segment Analysis

In the voltage rating segment, the low voltage segment is anticipated to capture the dominant share in the market. this sub segment’s leadership is sustained by its pervasive application across the commercial buildings, residential complexes, and industrial control panels where the standard electrical distribution occurs. The proliferation of data centers, smart home devices, and 5G infrastructure requires reliable protection for sensitive electronics operating at these voltage levels. Moreover, the global push for energy efficiency in building management systems necessitates the installation of new low-voltage switchgear and control gear. According to the EIA September 2025 data, the total residential energy consumption in Q4 was 336 billion kilowatt hours of electricity, which is managed and protected by the low voltage circuit protection devices, highlighting the vast installed base driving replacement and upgrades demand.

Technology Segment Analysis

Within the technology segment, the solid-state/digital sub-segment is poised to lead the segment in the market. The traditional electromechanical breakers, solid-state devices utilize semiconductor-based switches to interrupt the current in microseconds, offering a superior arc-less performance and enhanced durability for the high cycling applications such as the renewable energy systems and EV charging stations. The digital aspect, incorporating the IoT connectivity, allows remote monitoring and predictive analytics by reducing downtime in critical facilities. This technological shift is vital for the modern grid modernization efforts. Moreover, integrating advanced power electronics, including the solid-state protection, reduces the power conversion losses in solar plus storage systems, providing a compelling efficiency driver for the rapid adoption of this technology.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Voltage Rating |

|

|

Component Type |

|

|

End user |

|

|

Application |

|

|

Distribution Channel |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Circuit Protection Market - Regional Analysis

North America Market Insights

North America is a dominant player is poised to hold the regional share value of 40.5% by the end of 2035 in the circuit protection market. The region benefits from aggressive grid modernization programs for transmission upgrades requiring protective equipment. On the other hand, the Canada’s smart renewables and electrification pathways program funds utility investments in digital switchgear and protection systems. Aging infrastructure drives the replacement demand as 70% of the U.S. transmission lines exceed 25 years based on the U.S. Department of Energy's October 2023 data. Electrification of transportation and buildings create a new protection requirement targeting EV charges requiring DC fuses and breakers. Further, the industrial decarbonization incentives fund motor control center upgrades with integrated protection. Regulatory mandates for arc-fault and ground-fault protection in commercial construction sustain baseline demand across both countries.

The rising electricity consumption, renewable energy deployment, and ongoing product innovation in electrical safety systems are shaping the market in the U.S. According to the U.S. Energy Information Administration, April 2025 data, total U.S. electricity consumption reached approximately 4.10 trillion kWh in 2024, reflecting expanding demand that requires reliable circuit protection equipment across distribution networks and power electronics. Moreover, the EIA reported that renewable sources accounted for about 22% of total U.S. electricity generation in 2023, increasing installations of solar, wind, and energy storage systems that depend on circuit breakers to safeguard electrical infrastructure. On the other hand, the recent development, such as the launch of the ReliaHome Flex modular energy management system and ReliaHome ELITE circuit breakers in March 2026 by ABB, is expanding advanced circuit protection solutions designed to support electrified residential infrastructure and modern power distribution systems. These data show an optimistic growth in the market.

Key Developments in the Circuit Protection Market

|

Date |

Company/Organization |

Development |

|

March 2026 |

ABB |

Launched ReliaHome Flex energy management system and ReliaHome ELITE circuit breakers for residential electrification in Canada. |

|

October 2025 |

CNC Electric |

Introduced YCB3 Series circuit protection devices for residential, commercial, and light industrial applications. |

|

August 2025 |

Oak Ridge National Laboratory (ORNL) |

Developed medium-voltage DC circuit breakers to improve grid capacity and reduce electricity system costs. |

|

July 2023 |

Siemens |

Released additional versions of Sentron 3WA Air Circuit Breakers for industrial power distribution systems. |

Source: ABB, CNC Electric, ORNL, Siemens

The rising electricity demand, clean energy deployment, and government investments in power infrastructure and electrification are driving the market in Canada. According to the Canada Energy Regulator's May 2023 data, electricity accounted for 17% of Canada’s total final energy consumption in 2023, indicating the increasing electrification across residential buildings, commercial facilities, and industrial operations that require reliable electrical protection systems within the power distribution networks. Moreover, the Government of Canada's August 2023 data reports that about 84% of the country’s electricity generation came from non-emitting sources in 2023, which require protection devices to safeguard generators, substations, and grid interconnections. On the other hand, the OSPE 2026 data depicts that the Canada Infrastructure Bank announced plans to invest USD 2.5 billion in clean power generation, transmission, and energy storage over the next three years, forming part of a broader USD 5 billion clean power investment strategy aimed at strengthening the national electricity network. These developments are increasing the deployment of circuit protection systems across various sectors throughout Canada, indicating positive growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to register a CAGR of 7.5%. The region is driven by rapid industrialization, grid expansion, and electronics manufacturing growth. The demand is sustained by the continuous build-out of industrial automation in factories across China and Southeast Asia, which requires extensive control panels and motor-dense urban environments drive the construction of high-rise residential and commercial buildings, each requiring thousands of voltage circuit breakers and residential current devices to meet the national electrical codes. Moreover, the Southeast Asian manufacturing expansion drives the panel building demand. As per the 2025 Invest Malaysia data, Malaysia’s electrical and electronics sector accounts for 6.8% of GDP, requiring UL and IEC certified branch circuit protection for factory automation. Regional grid interconnection projects under the ASEAN Power Grid require standardized protection schemes across member states.

The circuit protection market in China is expanding rapidly due to the grid expansion and significant government investment in renewable energy and power infrastructure. According to the National U.S. ARAB Chamber of Commerce, October 2024 data, the country’s electricity consumption reached approximately 9.22 trillion kWh in 2023, reflecting strong demand from industrial production, digital infrastructure, and urban development, all of which require reliable circuit protection systems within power distribution networks and electrical equipment. On the other hand, the IEA 2024 data indicates that China is expected to install 3,207 GW by 2030 requiring circuit breakers, protective relays, and surge protection devices. Further, China continues to expand and modernize its power grid to support clean energy integration and regional electricity demand, therefore making the nation suitable for market growth.

The increasing electrification growth in residential and commercial construction and continuous product innovation are driving the market in India. ABB India, in January 2021, launched the Formula DIN-Rail range of circuit breakers, including Miniature Circuit Breakers, Residual Current Circuit Breakers, and isolators developed under the Make in India program for residential and commercial buildings, targeting the country’s electrical retail segment, which is estimated to be worth around USD 250 million. On the other hand, technological innovation is strengthening the circuit protection landscape. In April 2023, Havells India entered a commercial agreement with Swedish technology startup Blixt Tech AB to introduce solid-state circuit breakers in the India, enabling faster fault protection and supporting advanced electrical infrastructure. These advancements are boosting the market growth in the overall country.

Europe Market Insights

The circuit protection market in Europe is expanding rapidly and is driven by the aggressive grid modernization and renewable energy integration mandates. The European Commission's February 2026 report shows that the REPowerEU plan, supported by USD 327 billion in funding, accelerates the deployment of digital switchgear and protection systems across the member states to accommodate variable renewable generation. Aging infrastructure replacement creates a sustained demand. The European Commission's August 2025 data indicates that 40% of the EU distribution networks are over 40 years old, requiring circuit breaker upgrades. Moreover, building renovation waves under the Energy Performance of Buildings Directive mandate modern electrical panels with arc-fault protection in retrofitted commercial structures. Grid codes requiring faster fault clearing for the interconnection of offshore wind farms drive protective relay replacements across the North Sea coastal states.

The market in Germany is supported by the country’s large industrial base, rapid renewable energy expansion, and government-backed investments in power infrastructure modernization. According to Umwelt Bundesamt December 2025 data, renewable energy accounted for 54.1% of Germany’s gross electricity consumption in 2024, reflecting substantial growth in solar and wind installations that require circuit breakers. Industrial electricity demand also contributes to market growth. As per the Clean Energy Wire, February 2025 data shows that the country’s manufacturing sector consumed more than 201 terawatt-hours of electricity in recent years, highlighting the need for advanced circuit protection within automated production systems and industrial power distribution networks. These data show that the country is gaining increased exposure.

The government investment in power infrastructure modernization and rising electricity demand is fueling the market in the UK. According to the Veriforce CHAS February 2024 data, renewable energy sources generated 47% of the UK’s electricity in 2023, reflecting rapid growth that requires circuit breakers to safeguard the grid connections and generation equipment. Moreover, the electricity demand across infrastructure and buildings continues to drive the need for reliable protection technologies. The July 2025 Government of the UK data reported that total electricity supplied in the UK was around 285 terawatt-hours in 2023, supporting large-scale deployment of power distribution equipment in commercial facilities, industries, and public infrastructure. Further the Ofgem approved a GBP 20 billion investment program to upgrade and expand electricity transmission networks. Therefore, fueling the market expansion.

Key Circuit Protection Market Players:

- ABB (Switzerland)

- Schneider Electric (France)

- Siemens (Germany)

- Eaton (Ireland)

- Mitsubishi Electric (Japan)

- Fuji Electric (Japan)

- Panasonic Corporation (Japan)

- Littelfuse (U.S.)

- TE Connectivity (Switzerland)

- Sensata Technologies (U.S.)

- Bel Fuse Inc. (U.S.)

- Bourns, Inc. (U.S.)

- E-T-A Elektrotechnische Apparate GmbH (Germany)

- OMRON Corporation (Japan)

- Legrand (France)

- Nexperia (Netherlands)

- LS Electric (South Korea)

- Hager Group (Germany)

- Larsen & Toubro (India)

- Sécheron SA (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- ABB is a dominant player in the market, offering a comprehensive range of solutions from miniature circuit breakers to advanced high-voltage switchgear. The company uses its deep expertise in the electrification and industrial automation to provide protection devices that enhance the safety and reliability across utilities, buildings, and transportation. In 2024, the company made a revenue of USD 1.47 billion as per the annual report.

- Schneider Electric is a pivotal innovator in the circuit protection market, renowned for its industry-leading brands such as Merlin Gerin and Square D. The company views circuit protection as a critical component of its broader mission to digitize energy management and automation. Schneider’s strategy involves embedding advanced protection functions within the connected products, which form the backbone of modern resilient electrical distribution networks.

- Siemens stands as a technological leader in the global market, driving innovation via its SENTRON and SIVACON portfolios. The company integrates its protection devices into comprehensive solutions for power distribution ensuing the safety of infrastructure, manufacturing plants, and data centers. Siemens is at the forefront of merging the physical and digital worlds within the circuit protection market using its extensive industrial IoT expertise.

- Eaton is a key player in the circuit protection market, offering a wide array of fuses, circuit breakers, and surge protection devices. The company strategically emphasizes the integration of the electrical and industrial systems to solve critical power management challenges. In the evolving market, the company actively develops solutions for next-gen applications, mainly in EV charging infrastructure and data center power redundancy.

- Mitsubishi Electric is a key contributor to the circuit protection market, combining its expertise in factory automation with high-reliability electronic components. The company’s offerings include advanced no-fuse breakers, earth leakage circuit breakers, and molded case circuit breakers designed for the rigorous demands of industrial machinery and building infrastructure. According to the 2024 annual report, the company has made a revenue of USD 4.27 billion.

Here is a list of key players operating in the global market:

The global circuit protection market is highly competitive and consolidated, dominated by a large multinational corporation alongside specialized regional players. The key strategic initiatives among the market leaders focus on technological innovation, mainly in miniaturization and energy efficiency, for applications in renewable energy, electric vehicles, and industrial automation. Companies are actively pursuing mergers and acquisitions to expand their product portfolios and geographic reach. For example, in February 2025, Sécheron acquired LoPro high-voltage circuit breaker technology from TE Connectivity. Furthermore, there is a significant push to develop smart circuit protection devices that provide connectivity and diagnostic capabilities for IoT ecosystems. To reduce the supply chain risks and cater to local demand, the major players are also investing in expanding their manufacturing footprints across Asia and North America.

Corporate Landscape of the Circuit Protection Market:

Recent Developments

- In March 2026, Siemens Smart Infrastructure has announced the expansion of the functionalities of its semiconductor-based SENTRON Electronic Circuit Protection Device (ECPD) and introducing the SIRIUS 3RW5 -Z R11 refurbished soft starter, its first product designed according to circular economy principles.

- In March 2026, Sensata Technologies announced the launch of its FaultBreak contactor, which is a next generation high voltage switching and protection solution engineered to improve fault clearing performance, enhance safety, and simplify electric vehicle power systems.

- In August 2025, Schneider Electric, the leader in the digital transformation of energy management and automation, announces the launch of FeederSeT, which is a new product range bringing advanced digital connectivity to circuit protection solutions.

- Report ID: 8442

- Published Date: Mar 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.