Integrated Circuits Market Outlook:

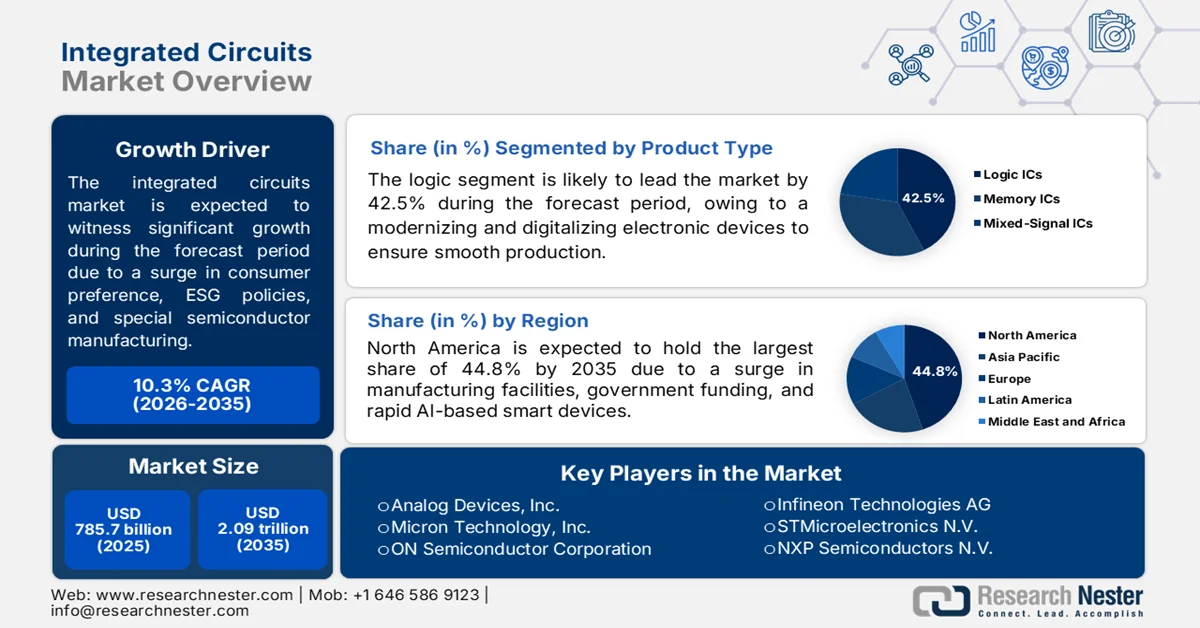

Integrated Circuits Market size was valued at USD 785.7 billion in 2025 and is poised to reach USD 2.09 trillion by the end of 2035, growing at an 10.3% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of integrated circuits is estimated at USD 866.6 billion.

The worldwide integrated circuits market is increasingly shaped by different cross-cutting factors, including evolving regulatory frameworks, a shift in consumer preferences towards subscription-based electronics and modular devices, the presence of Environmental, Social, and Governance (ESG) mandates, and the availability of specialized semiconductors. According to official statistics published by NLM in April 2023, the U.S. CHIPS and Science Act, which was passed by Congress in July 2022, solidified the semiconductor industry and set aside USD 280 billion to bolster competitiveness. Additionally, USD 52 billion was provided for a range of tax credits, research and development (R&D) fabrication, and subsidies for incentivizing the modernization, expansion, and construction of semiconductor equipment infrastructures, thus proliferating the market growth.

Global Semiconductor Monthly and Yearly Sales Analysis (in Billion), 2026

|

Regions/Countries |

Monthly Sales |

Yearly Sales |

||||

|

Last Month |

Current Month (March) |

Change % |

Last Month |

Current Month (March) |

Change % |

|

|

America |

USD 29.8 |

USD 33.8 |

13.3 |

USD 18.4 |

USD 33.8 |

83.1 |

|

Europe |

USD 5.7 |

USD 6.2 |

8.4 |

USD 4.2 |

USD 6.2 |

46.5 |

|

Japan |

USD 3.7 |

USD 4.0 |

7.1 |

USD 3.7 |

USD 4.0 |

7.4 |

|

China |

USD 23.7 |

USD 26.7 |

12.7 |

USD 15.3 |

USD 26.7 |

74.8 |

|

Asia Pacific/Other |

USD 26.1 |

USD 28.7 |

9.8 |

USD 13.7 |

USD 28.7 |

108.5 |

|

Total |

USD 89.2 |

USD 99.5 |

11.5 |

USD 55.5 |

USD 99.5 |

79.2 |

Source: Semiconductors Organization

Furthermore, the integration of chiplet-based heterogeneous adoption, the shift toward in-memory computing architectures, and suitable design for recyclable and disassembly packaging are a few trends that are boosting the market globally. As stated in an article published by the Center for Strategic and International Studies (CSIS) Organization in August 2024, the Europe Commission generously allocated USD 4.9 billion from its initial budget to effectively implement suitable research elements of the CHIPS Act. Of this, USD 3.1 billion was redirected from Horizon Europe and an additional USD 1.6 billion from the Digital Europe Program. Besides, in terms of tax credits, the U.S. is projected to offer almost 25% for investments by the end of 2026. Therefore, based on these investments and suitable tax credits, there is a huge growth opportunity for the market.

Key Integrated Circuits Market Insights Summary:

Regional Highlights:

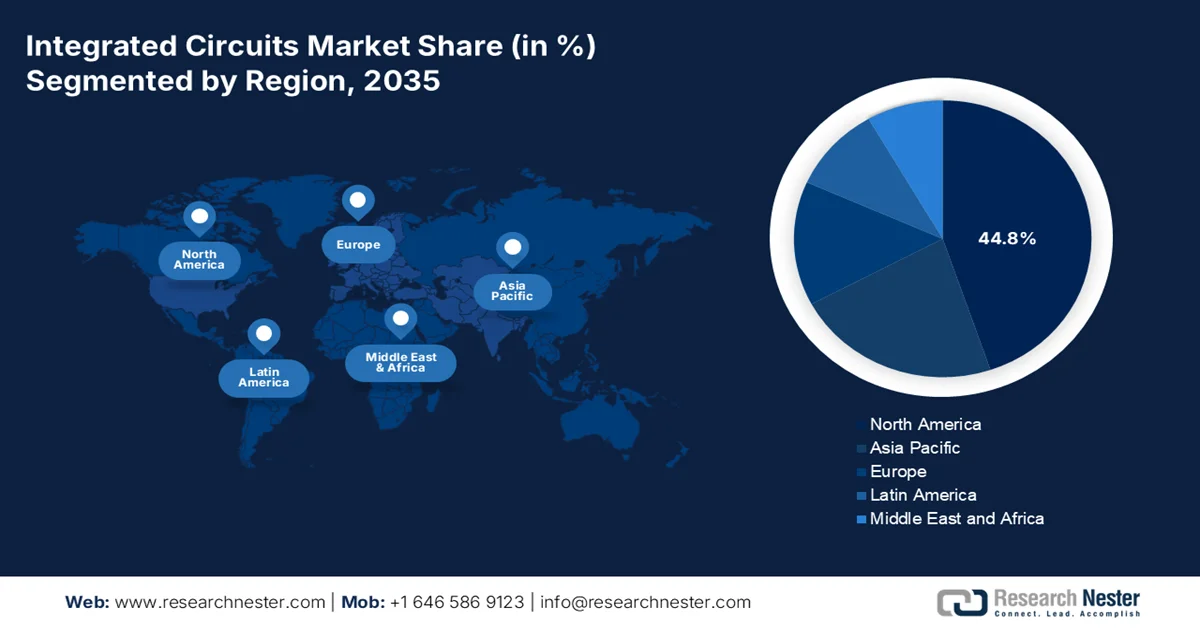

- The integrated circuits market in North America is projected to dominate with a 44.8% share by 2035, fostered by expanding AI-enabled smart devices, accelerating data center electricity consumption, and rising edge computing adoption

- Europe is poised to register the fastest growth in the market during 2026-2035, catalyzed by rapid expansion in semiconductor and electronics production alongside increasing renewable energy and electric vehicle deployment

Segment Insights:

- The logic segment is anticipated to secure a 42.5% share of the integrated circuits market by 2035, fueled by the growing demand for high-speed, miniaturized, and cost-efficient electronics across smartphones, vehicles, and IoT devices

- The digital integrated circuits sub-segment is expected to capture the second-largest market share during the forecast period, accelerated by increasing investments in high-performance computing innovation and the expanding role of advanced digital technologies

Key Growth Trends:

- Proliferation of smart devices adoption

- Demand for current power management in airway-based devices

Major Challenges:

- Accelerating obsolescence and design complexity for smart devices

- Power density and thermal management in miniaturized enclosures

Key Players: Intel Corporation, Qualcomm Incorporated, Broadcom Inc., NVIDIA Corporation, Advanced Micro Devices, Inc., Texas Instruments Incorporated, Analog Devices, Inc., Micron Technology, Inc., ON Semiconductor Corporation, Microchip Technology Incorporated, Samsung Electronics Co., Ltd., SK Hynix Inc., Infineon Technologies AG, STMicroelectronics N.V., NXP Semiconductors N.V., Renesas Electronics Corporation, Sony Semiconductor Solutions Corporation, Toshiba Corporation.

Global Integrated Circuits Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 785.7 billion

- 2026 Market Size: USD 866.6 billion

- Projected Market Size: USD 2.09 trillion by 2035

- Growth Forecasts: 10.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.8% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Japan, South Korea, Germany

- Emerging Countries: India, Vietnam, Singapore, Taiwan, Netherlands

Last updated on : 15 May, 2026

Integrated Circuits Market - Growth Drivers and Challenges

Growth Drivers

- Proliferation of smart devices adoption: Modernized smart devices tend to integrate different sensor types, including microphones, barometers, ambient light sensors, magnetometers, gyroscopes, and accelerometers, which is positively impacting the market demand. For instance, as per the April 2022 World Economic Forum article, more than 130 million households are home to almost 1 smart speaker, and this is further predicted to increase to 335 million in the upcoming 5 years. Besides, the worldwide expenditure on Internet of Things (IoT) products effectively reached USD 1.1 trillion in 2023, which is also enhancing the market demand. Moreover, there are various smart devices that households are adopting, which denotes an optimistic outlook for the market growth.

Estimated Global Households Adopting Smart Devices, 2022 and 2027

|

Smart Device Type |

2022 |

2027 |

|

Smart Speaker |

131.4 |

335.3 |

|

Smart Security Camera |

77.5 |

180.7 |

|

Smart Big Appliances |

73.1 |

177.6 |

|

Smart Small Appliance |

72.2 |

172.1 |

|

Smart Smoke Detector |

48.4 |

116.2 |

|

Hub/Gateway |

39.3 |

55.2 |

Source: World Economic Forum

- Demand for current power management in airway-based devices: Battery-powdered devices frequently demand to remain in a low-power state, while increasing for detecting motion and wake words. As stated in an article published by the IATA Organization in June 2025, the airway industry’s gross domestic product (GDP) has remained above 3% since the past years. Besides, the worldwide growth in air cargo as of 2025 demonstrated sustainability to 0.7% year-over-year (YoY). Apart from these developments, conventional power management usually consumes continuous current in the case of a load-off situation, thereby making it suitable for positively boosting the market globally.

Challenges

- Accelerating obsolescence and design complexity for smart devices: The integrated circuits market for modern smart devices must support exponentially growing workloads, such as edge AI processing, high refresh rate displays, multi-protocol wireless connectivity, and advanced power management, all within shrinking physical footprints. This drives extreme design complexity, requiring heterogeneous integration, chiplets, and 3D stacking. However, the design cycle for a new application-specific IC (ASIC) or system-on-chip (SoC) now exceeds eighteen months, while consumer electronics' lifecycles shrink to under twelve months. Moreover, by the time an IC is mass-produced, the newest AI-based acceleration standards or memory interfaces might emerge.

- Power density and thermal management in miniaturized enclosures: As smart devices become thinner, lighter, and more feature-rich, the integrated circuits inside them face a critical physical roadblock, which is heat dissipation. Besides, high-performance application processors, 5G modems, and fast-charging power management ICs generate intense localized heat. In the case of foldable phones, smartwatches, and AR glasses, there is insufficient surface area for passive cooling, and active cooling fans are impossible due to size constraints. Likewise, excessive junction temperatures force ICs to throttle performance, reducing frame rates in gaming phones, delaying AI inference in voice assistants, or shutting down wireless charging circuits, thus hindering the integrated circuits market growth.

Integrated Circuits Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.3% |

|

Base Year Market Size (2025) |

USD 785.7 billion |

|

Forecast Year Market Size (2035) |

USD 2.09 trillion |

|

Regional Scope |

|

Integrated Circuits Market Segmentation:

Product Type Segment Analysis

Based on the product type, the logic segment is anticipated to account for the largest share of 42.5% in the integrated circuits market by the end of 2035. The segment’s upliftment is primarily attributed to its role as the foundational building blocks of modernized and digitalized electronics for enabling the cost-effective production, high-speed performance, and miniaturization of devices from smartphones to vehicles. According to official statistics published by the UN Trade and Development (UNCTAD) in July 2024, IoT devices are projected to surge 2.5 times from 2023 to 39 billion by the end of 2029. In this regard, the newest data across 43 countries deliberately represent almost 3 quarters of the worldwide GDP, demonstrating growth in business e-commerce sales by nearly 60% and reaching USD 27 trillion, thereby enhancing the segment’s demand.

Type of Circuit Segment Analysis

During the forecast period, the digital integrated circuits sub-segment, part of the type of circuit segment, is projected to garner the second-largest share in the market segment. The sub-segment’s growth is effectively driven by the foundation of modern technology that fuels miniaturization, speed, and efficiency from smartphones to supercomputers. As stated in an article published by the Department of Energy (DOE) in April 2026, the administrative organization offered USD 400,000 to small and medium-sized manufacturers, along with their non-profit, university, and national laboratory partners. In addition, the DOE also made over USD 10 million readily available for the high-performance computing innovation program, thus bolstering the sub-segment’s expansion.

Application Segment Analysis

The standard PCs sub-segment, which is part of the application segment, is expected to grab the third-largest share in the market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by the aspect of encompassing laptops, desktops, tablets, and workstations, designed for general-purpose computing across consumer, enterprise, and educational environments. This sub-segment remains a foundational pillar of the industry because these devices require a diverse and dense population of silicon chips to function. A single standard PC integrates multiple IC types, including central processing units, graphics processing units, memory controllers, power management ICs, wireless connectivity chips, audio codecs, and numerous interface controllers. Besides, the continuous supply of computers to and from different nations is also driving the sub-segment’s expansion.

2024 Computers Global Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

China |

185.0 billion |

- |

|

Taipei |

60.6 billion |

- |

|

Mexico |

56.7 billion |

- |

|

U.S. |

- |

140.0 billion |

|

Hong Kong |

- |

32.6 billion |

|

Germany |

- |

28.9 billion |

|

Global Trade Valuation |

504.0 billion |

|

|

Global Trade Share |

2.2% |

|

|

Product Complexity |

1.0 |

|

|

Export Growth |

24.7% |

|

Source: OEC

Our in-depth analysis of the integrated circuits includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Type of Circuit |

|

|

Application |

|

|

Technology |

|

|

Material Type |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Integrated Circuits Market - Regional Analysis

North America Market Insights

North America in the integrated circuits market is anticipated to grab the highest share of 44.8% by the end of 2035. The market’s uplift in the region is primarily attributed to a strong electronics ecosystem, innovative manufacturing research facilities, substantial government funding through legislation, the rapid adoption of AI-based smart devices, data center expansion, and the proliferation of edge computing. According to official statistics published by the DOE in December 2024, data centers consumed almost 4.4% of overall U.S. electricity in 2023 and are projected to consume 6.7% to 12% of domestic electricity by the end of 2028. In addition, the data center electricity utilization surged from 58 TWh to 176 TWh in 2023, and eventually expected to demonstrate an increase between 325 TWh and 580 TWh by 2028, thus driving the market growth in the region.

The integrated circuits market in the U.S. is growing significantly, owing to federal strategies, private investments for domestic fabrications, an increase in the need for innovative process control, a surge in the utilization of industrial zones, AI-driven laptops, and smart home controllers, along with secured supply chain dynamics, and aerospace and defense expenditure. As stated in an article published by the Pew Research Center Organization in January 2026, 9 in 10 adults in the country utilized the internet regularly, including 41%of them having an online presence. The aspect of regular internet use has emerged as a suitable norm for the domestic adult population, and almost 4 in 10 constantly remain online on their respective smart devices. Moreover, the population earning USD 100,000 have readily adopted the online lifestyle on their electronic devices, thereby enhancing the market demand in the country.

U.S. Adult Population Having Smartphone, 2015-2025

|

Year |

Population % |

|

2015 |

69 |

|

2016 |

77 |

|

2017 |

- |

|

2018 |

77 |

|

2019 |

81 |

|

2020 |

- |

|

2021 |

85 |

|

2022 |

- |

|

2023 |

90 |

|

2024 |

91 |

|

2025 |

91 |

Source: Pew Research Center Organization

The tactical focus on silicon photonics for telecommunication facilities and quantum computing, the presence of suitable funding programs, an increase in the utilization of communication devices, growth in the electric vehicle supply chain, and the need for automotive-grade power management are certain factors that are positively impacting the market in Canada. Based on government estimates published by the ITA in April 2026, information and communication technology plays a huge role in all these factors, with the industry highly dependent on imports, totaling USD 38.6 billion and worth USD 12 billion of exports. Besides, the U.S. is the country’s top partner in trading facilities, with USD 7.9 billion in exports. Additionally, Ontario imports are also valued at USD 4.8 billion, followed by USD 767.5 billion from Quebec, USD 395.9 million from British Columbia, and USD 251.8 million from Manitoba, thereby proliferating the market exposure.

Information and Communication Technology Trade Data Analysis in Canada, 2022-2025

|

Components (USD Million) |

2022 |

2023 |

2024 |

2025 |

|

Total Exports |

2,816 |

3,206 |

3,110 |

3,250 |

|

Total Imports |

4,647 |

4,894 |

4,734 |

4,850 |

|

Imports from the U.S. |

1,772 |

1,911 |

1,781 |

1,850 |

|

Trade Surplus/Deficit |

-1,831 |

-1,688 |

-1,624 |

-1,600 |

Source: ITA

Europe Market Insights

Europe in the integrated circuits market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by significant import dependency, rapid growth in the semiconductors and electronics industries, technological innovation in the telecommunication and automotive sectors, and an increase in renewable energy technologies, along with electric vehicles. According to an official data report published by the Electronics Organization in June 2024, the regional production of electronic systems across 8 industries is predicted to expand by 52.5% by the end of 2035. Besides, the region is focused on successfully achieving an additional 16.8% growth for the upcoming 12 years, with the intention of maintaining its 2023 global share of 16.7% in electronics systems, thereby making it suitable for fueling the market growth.

2024 Electronics and Electrical Machinery Export/Import Analysis in Europe

|

Countries |

Export (USD) |

Import (USD) |

|

Germany |

159 billion |

197 billion |

|

Netherlands |

47 billion |

78.5 billion |

|

France |

44.7 billion |

69.5 billion |

|

Italy |

43.1 billion |

48.1 billion |

|

Czechia |

42.9 billion |

50.1 billion |

|

Poland |

41.9 billion |

49.7 billion |

|

Hungary |

37 billion |

30.7 billion |

|

UK |

26.4 billion |

66.3 billion |

|

Spain |

22.7 billion |

43.3 billion |

|

Ireland |

20.8 billion |

14.2 billion |

Source: OEC

The integrated circuits market in Germany is gaining increased traction, owing to a surge in the demand for electronic components across the consumer, industrial, and automotive industries, a massive transformation to electric vehicles and autonomous driving, administrative programs supporting semiconductor research and development, and the strong research facility for innovative semiconductor materials. As stated in an article published by the EV TCP Organization in 2024, almost 2.8 million electric vehicles were readily registered in the country. Additionally, nearly 1.8 million were battery-electric vehicles, while 1 million were categorized as plug-in hybrids. Besides, in the first half of 2024, the share for newly registered battery-electric vehicles lowered to 13%, down from 16% as of 2023. Despite the drop in share, there is an ongoing registration of electric vehicles, based on which there is a huge demand for the market in the country.

The upsurge in electronic chip consumption, the presence of the manufacturing facility for consumer electronics, favorable policies implementation by the government, strategic location providing access to the overall region and the North Africa economy, and the rapid digital economy are a few trends that are responsible for driving the integrated circuits market in Spain. As per an article published by the ITA in September 2024, fiber-to-the-premises coverage stands at 95.2% and 92.3% for 5G. Besides, the country has allocated an estimated 26% of NextGeneration funds to digital matters, which caters to fortifying the digitalized infrastructure and creating advanced technologies. Moreover, the nation achieved 2.3% of GDP in foreign direct investment over the past 5 years, in comparison to only 1% from OECD countries, thus denoting an optimistic outlook for the market expansion.

APAC Market Insights

The Asia Pacific in the market is projected to witness a considerable expansion by the end of the stipulated timeline. The market’s growth in the region is effectively driven by generous government spending, suitable budget provision for advanced materials, and the development of the semiconductor supply chain. According to a data report published by the Semiconductor Industry Association in May 2025, Korea accounted for 21.1% share of semiconductor shipments, while China catered to 4.5% and Japan with 8.2%. Besides, the presence of U.S.-based semiconductor organizations in the region constituted a 51.1%, in comparison to 48.9% of other organizations for the USD 152.3 billion semiconductor industry. Meanwhile, 50.7% U.S.-specific companies have their presence in China, and 49.3% of other organizations for the USD 185.1 billion industry, thus enhancing the market exposure.

The integrated circuits market in China is gaining increased exposure, owing to the presence of the largest consumer electronics manufacturing base, increased growth in the electric vehicle sector, the existence of government organizations for prioritizing semiconductor self-sufficiency, and the mobile device penetration. As stated in an article published by the State Council Information Office in November 2025, the value-added industrial output of the majority of companies in the country surged by 10.9% YoY, demonstrating a 4.7 percentage points higher than the total industrial sector. Based on this growth, the mobile phone production experienced rapid expansion, successfully reaching 1.1 billion units. Additionally, the smartphone output constituted 881 million units, which reflected a YoY upsurge by 1%, thus enhancing the market growth and expansion.

The aspects of suitable government support policies, increased focus on private and public partnerships, generous investment opportunities, the supply chain dynamics, the adoption of innovative design technologies, and strengthening mass production capabilities are a few factors that are fueling the integrated circuits market in Japan. Besides, the industrial growth in the country catered to USD 45.1 billion by the end of 2025, which is further projected to be worth USD 48.7 billion by 2026 and USD 98.2 billion, with an 8.1% growth rate by 2035. Based on government estimates published by the ITA in November 2025, the AI-based semiconductor chips industry in the country is steadily extending and reached more than USD 51 billion by the end of 2025. Moreover, there has been the provision of 0.7% of domestic GDP or USD 25.7 billion as funding for the semiconductor industry for 3 years, thereby creating a positive outlook for the market growth.

Japan’s Semiconductor Industry Size Analysis, 2022-2025

|

Year |

Industry Size (USD Billion) |

YoY Growth |

Exchange Rate |

|

2022 |

48.1 |

10.2% |

131.4 |

|

140.4 |

150.5 |

-2.9% |

140.4 |

|

2024 |

47.4 |

1.4% |

150.5 |

|

2025 |

51.8 |

9.4% |

148.9 |

Source: ITA

Key Integrated Circuits Market Players:

- Intel Corporation (U.S.)

- Qualcomm Incorporated (U.S.)

- Broadcom Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Analog Devices, Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- ON Semiconductor Corporation (U.S.)

- Microchip Technology Incorporated (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- SK Hynix Inc. (South Korea)

- Infineon Technologies AG (Germany)

- STMicroelectronics N.V. (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Renesas Electronics Corporation (Japan)

- Sony Semiconductor Solutions Corporation (Japan)

- Toshiba Corporation (Japan)

- MediaTek Inc. (Taiwan)

- Semiconductor Manufacturing International Corporation (China)

- ASE Technology Holding Co., Ltd. (Taiwan)

- Motorola Solutions (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Intel Corporation maintains a foundational presence in the integrated circuits market through its legacy in microprocessors for personal computers and laptops. The company is strategically transitioning from a traditional integrated device manufacturer to a major foundry player, aiming to produce logic ICs for other smart device brands.

- Qualcomm Incorporated dominates the wireless connectivity and mobile application processor space within the integrated circuits market, powering a vast majority of premium and mid-tier smartphones globally. The company integrates 5G modems directly into its system-on-chip solutions, enabling thinner, more power-efficient smart devices.

- Broadcom Inc. holds a critical position in the market by supplying a wide portfolio of mixed-signal, RF, and switching ICs used in wireless communication devices and data center infrastructure. Its chips are essential components inside smartphones, Wi-Fi routers, and smart home hubs, enabling high-speed data transfer and power management.

- NVIDIA Corporation has transformed the Integrated Circuits landscape by elevating the graphics processing unit from a rendering engine to the core compute platform for artificial intelligence. Its integrated circuits are now central to AI-accelerated laptops, autonomous smart devices, and edge computing nodes that require real-time neural network inference.

- Advanced Micro Devices, Inc. competes vigorously in the market with its portfolio of high-performance central processing units and graphics processing units for personal computers and gaming consoles. The company's chiplet-based design approach allows it to deliver scalable computing solutions across thin-and-light laptops, desktop workstations, and handheld gaming devices.

Here is a list of key players operating in the global market:

The global integrated circuits market remains intensely competitive, dominated by a mix of U.S.-based design leaders and Asia-specific manufacturing giants. The landscape is bifurcated between integrated device manufacturers (IDMs), such as Intel and Samsung, controlling both design and production, and Fabless companies, including NVIDIA and Qualcomm, outsourcing manufacturing to foundries such as TSMC. Moreover, to navigate geopolitical tensions and evolving AI demands, key players are pursuing distinct strategies. A major trend is vertical integration and capacity expansion, with Intel aggressively expanding its foundry services to compete with TSMC and Samsung. Besides, in May 2025, NVIDIA launched the NVLink Fusion program, permitting consumers and partners to utilize non-NVIDIA CLPUs and GPUs, while being in tandem with its products, thus boosting the integrated circuits industry growth.

Corporate Landscape of the Market:

Recent Developments

- In October 2025, ASE Technology Holding Co., Ltd. and Analog Devices proclaimed tactical joint efforts in Malaysia by effectively signing the binding memorandum of understanding (MoU) for enhancing the manufacturing diversity and global supply chain resilience.

- In May 2025, Motorola Solutions entered into a definitive agreement and acquired Silvus Technologies, Inc. for USD 4.4 billion in up-front consideration, and aimed to increase the security, safety, and defense utilization cases for autonomous systems and secure high bandwidth communications.

- Report ID: 8568

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.