Application Specific Integrated Circuit Market Outlook:

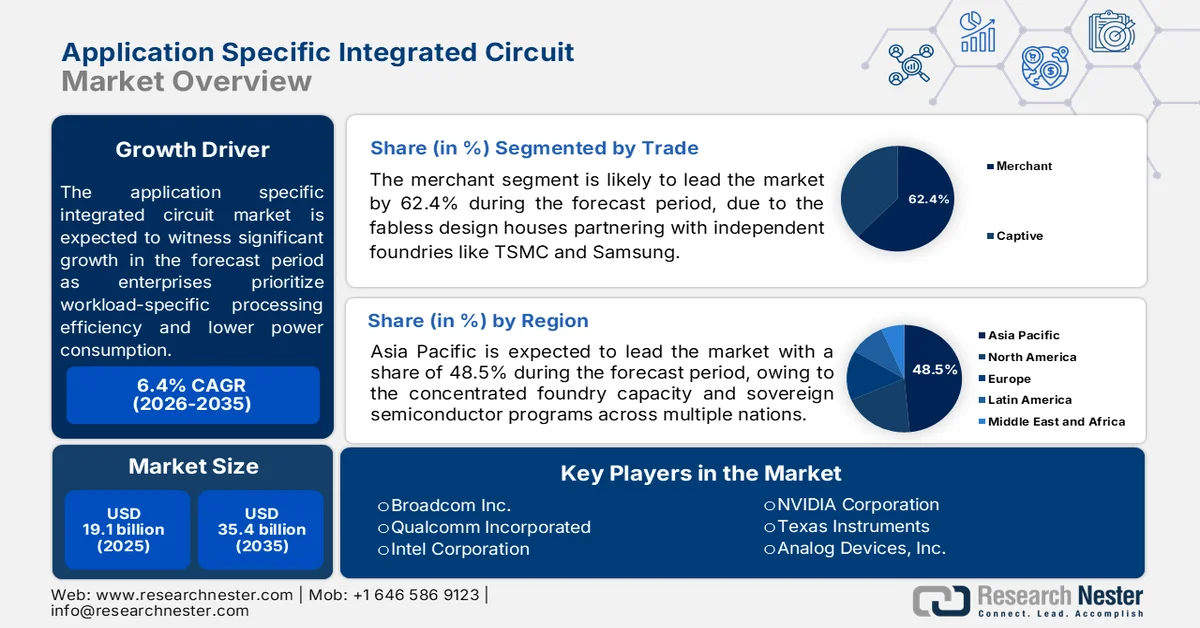

Application Specific Integrated Circuit Market size was valued at USD 19.1 billion in 2025 and is projected to reach USD 35.4 billion by 2035, rising at a CAGR of 6.4% during the forecast period 2026 to 2035. In 2026, the industry size of application specific integrated circuit is estimated at USD 20.2 billion.

The global application specific integrated circuit market demand is expanding across data centers, automotive electronics, telecommunications, and industrial automation as enterprises prioritize workload-specific processing efficiency and lower power consumption. The Semiconductor Industry Association (SIA) February 2025 data reported that global semiconductor sales reached USD 627.6 billion in 2024, representing a 19.1% YoY increase, supported largely by high-performance computing and AI infrastructure investments. The U.S. government continues to strengthen domestic semiconductor manufacturing via the CHIPS and Science Act. These investments are supporting wafer fabrication, advanced packaging, and ASIC-oriented design ecosystems within the U.S. On the other hand, the National Telecommunications and Information Administration (NTIA) and other federal agencies are accelerating broadband and 5G deployment programs, increasing demand for networking ASICs used in switches, routers, and telecom infrastructure.

Besides, automotive electrification and industrial digitization are further strengthening the application specific integrated circuit market outlook. According to the International Energy Agency 2025 data, global electric vehicle sales exceeded 17 million units in 2024, accounting for more than 20% of worldwide car sales. The increasing electronic content per vehicle, including battery management systems, advanced driver-assistance systems, infotainment, and powertrain controls, is generating sustained demand for automotive-grade ASICs. ASIC adoption is also increasing in aerospace, defense, and healthcare systems where organizations require secure application-focused processing architectures with long product life cycles. Government-backed initiatives focused on semiconductor resilience, cybersecurity, and domestic supply chain localization are supporting additional investment in ASIC development and fabrication capacity, particularly in North America, Europe, and Asia-Pacific manufacturing hubs.

Global EV Car Sales, 2024

|

Region |

Sales (million) |

|

China BEV |

6.4 |

|

China PHEV |

4.9 |

|

Europe BEV |

2.2 |

|

Europe PHEV |

1.0 |

|

U.S. BEV |

1.2 |

|

U.S. PHEV |

0.3 |

|

Rest of World BEV |

1.0 |

|

Rest of World PHEV |

0.3 |

Source: IEA 2025

Key Application Specific Integrated Circuit Market Insights Summary:

Regional Highlights:

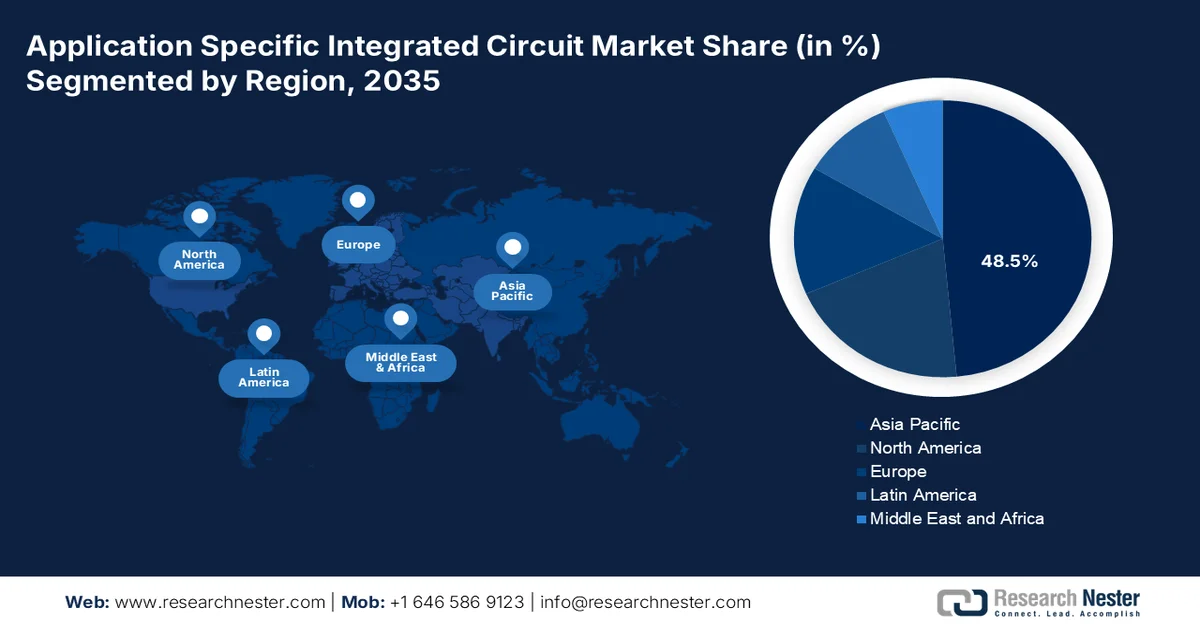

- Asia Pacific application specific integrated circuit market is anticipated to secure 48.5% revenue share by 2035, impelled by concentrated foundry capacity, expanding consumer electronics manufacturing, and sovereign semiconductor development programs

- North America is forecast to expand at a CAGR of 12.4% during 2026–2035, supported by rising demand for custom AI silicon from hyperscale data centers, defense agencies, and automotive manufacturers

Segment Insights:

- The merchant segment in the application specific integrated circuit market is projected to account for 62.4% share by 2035, driven by fabless semiconductor companies collaborating with independent foundries including TSMC and Samsung

- The 64-bit architecture segment is expected to maintain its dominance through 2035, owing to increasing deployment in AI inference, encryption, aerospace systems, and high-precision industrial automation workloads

Key Growth Trends:

- Energy efficiency mandates for data centers

- Government-led electronics manufacturing expansion

Major Challenges:

- Massive non-recurring engineering costs

- Extreme technological complexity

Key Players: Broadcom Inc. (U.S.), Qualcomm Incorporated (U.S.), Intel Corporation (U.S.), NVIDIA Corporation (U.S.), Texas Instruments (U.S.), Analog Devices, Inc. (U.S.), Marvell Technology Group (U.S.), Microchip Technology Inc. (U.S.), ON Semiconductor (U.S.), NXP Semiconductors (Netherlands), Infineon Technologies (Germany), STMicroelectronics (Italy), Renesas Electronics Corporation (Japan), Sony Semiconductor Solutions (Japan), Samsung Electronics (South Korea), SK Hynix Inc. (South Korea), Accenture (Ireland), Tata Consultancy Services (India), Ericsson (Swedan), Cyient (India).

Global Application Specific Integrated Circuit Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 19.1 billion

- 2026 Market Size: USD 20.2 billion

- Projected Market Size: USD 35.4 billion by 2035

- Growth Forecasts: 6.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (48.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Taiwan, South Korea, Japan

- Emerging Countries: India, Canada, Germany, Singapore, Israel

Last updated on : 14 May, 2026

Application Specific Integrated Circuit Market - Growth Drivers and Challenges

Growth Drivers

- Energy efficiency mandates for data centers: Government regulations limiting data center power consumption are creating demand for application specific integrated circuit markets that deliver higher performance per watt than GPUs. The European Commission’s January 2026 Data Energy Efficiency Directive requires data centers above 500 kilowatts to report the energy intensity metrics and implement best available techniques defined to include workload-specific accelerators where technically feasible. The U.S. Department of Energy's Better Buildings Challenge has participating data center operators committed to reducing power usage effectiveness; ASIC deployments for fixed AI inference tasks provide a compliance pathway. Singapore's Infocomm Media Development Authority mandates that new data centers achieve power usage effectiveness.

- Government-led electronics manufacturing expansion: According to the PIB December 2025 data, India’s Electronics Components Manufacturing Scheme (ECMS), launched in 2025, is strengthening demand conditions for the application-specific integrated circuits market by expanding the domestic electronics manufacturing ecosystem. The scheme promotes local production of printed circuit boards, camera modules, and electromechanical components that are widely integrated with ASIC-enabled systems across telecom, automotive, industrial automation, and consumer electronics applications. The Ministry of Electronics and Information Technology (MeitY) estimated investment proposals of USD 7.1 billion under the program; however, actual proposals reached nearly USD 13.9 billion, reflecting stronger-than-expected industry participation and accelerating semiconductor ecosystem localization in India.

- Expansion of 5G and broadband infrastructure: Telecommunications infrastructure deployment is creating sustained demand for networking and signal-processing ASICs. Governments worldwide are increasing funding for broadband expansion, 5G rollout, and digital connectivity programs to support economic digitization. ASICs are critical components in base stations, routers, switches, optical networking systems, and edge computing equipment due to their ability to process high data volumes efficiently. The FCC and NTIA continue distributing broadband infrastructure funding under national connectivity programs. Meanwhile, the European Union’s Digital Decade strategy is accelerating regional telecom modernization initiatives. Moreover, the rising mobile data traffic and edge-computing adoption are expected to increase telecom equipment procurement globally.

Challenges

- Massive non-recurring engineering costs: Entering the application specific integrated circuit market requires upfront investment reaching hundreds of millions of dollars before a single chip is sold. A single advanced node design cycle costs million in NRE fees alone, covering design tools, mask sets, and validation; for comparison, FPGA-based design can start with certain numbers. This creates a huge barrier for startups and smaller firms. Though the market is set to expand, ASIC design projects span months from concept to tape-out, during which no revenue is generated, forcing companies to maintain substantial cash reserves.

- Extreme technological complexity: As the industry migrates to 2nm and 3nm process nodes, design complexity has exploded exponentially. Engineers must now master 3D Chiplet architectures, heterogeneous integration via SoIC, and complex packaging such as CoWoS. A single 2nm design potentially requires multiple tape-outs for compute dies, I/O dies, SRAM, and HBM bottom dies using different process technologies. This multi-die approach demands expertise across thermal management, signal integrity, and power delivery that few organizations possess.

Application Specific Integrated Circuit Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.4% |

|

Base Year Market Size (2025) |

USD 19.1 billion |

|

Forecast Year Market Size (2035) |

USD 35.4 billion |

|

Regional Scope |

|

Application Specific Integrated Circuit Market Segmentation:

Trade Segment Analysis

Under the trade segment, the merchant is dominating the application specific integrated circuit market and is poised to hold a share value of 62.4% by 2035. The segment is driven by fabless design houses partnering with independent foundries like TSMC and Samsung. Unlike captive ASICs manufactured in‑house for a single company, merchant ASICs benefit from shared R&D costs, multi‑customer mask sets, and access to leading‑edge process nodes. The sheer scale of merchant IC commerce is evident from global trade data: according to the OEC 2024 data, HS4 code 8542 (Electronic Integrated Circuits) recorded USD 928 billion in world trade during 2024, ranking as the 3rd most traded product category out of 1,222. This figure includes all integrated circuits; merchant ASICs, particularly AI accelerators, and automotive custom silicon, form a rapidly growing subset.

Bit Architecture Segment Analysis

The 64‑bit architecture is the leading sub‑segment within bit architecture in the application specific integrated circuit market. 64‑bit ASICs provide a larger addressable memory space (over 4 GB) and higher precision for data‑intensive workloads, including AI inference, encryption, and network packet processing. According to the PIB December 2025 data, India’s first homegrown 1.0 GHz 64‑bit dual‑core microprocessor, DHRUV64, directly reinforces why 64‑bit architecture is the leading sub‑segment in the application specific integrated circuit market. Developed under the Digital India RISC‑V (DIR‑V) programme, DHRUV64 targets secure computing IoT gateways and aerospace applications that demand memory addressing beyond 4 GB and high-precision data processing exactly where 64‑bit ASICs excel. While DHRUV64 is a general-purpose microprocessor, its 64‑bit core logic is directly reusable in semi‑custom ASICs for defense and industrial automation.

Type Segment Analysis

Within the type segment, semi‑custom is fueling the application specific integrated circuit market. Standard cell ASICs use pre‑characterized logic blocks (e.g., NAND, flip‑flops) placed and routed to meet specific application needs, offering a balance between full‑custom performance (high efficiency) and programmable logic (shorter design time). They are the backbone of AI accelerators, 5G baseband processors, and automotive domain controllers. A report from the Department of Energy (.gov) states that standard cell semi‑custom ASICs reduced total energy consumption compared to FPGAs for the same neural network inference tasks while requiring a certain percentage of the development time of full‑custom chips. This efficiency‑to‑time trade‑off ensures semi‑custom ASICs remain the preferred choice for volume products through 2035.

Our in-depth analysis of the application specific integrated circuit market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Trade |

|

|

Application |

|

|

End user Industry |

|

|

Bit Architecture |

|

|

Process Node |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Application Specific Integrated Circuit Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the application specific integrated circuit market and is expected to hold the regional revenue share of 48.5% by the end of 2035. The market is driven by concentrated foundry capacity, consumer electronics volume, and sovereign semiconductor programs across multiple nations. Taiwan and South Korea lead in advanced node ASIC fabrication, housing the world’s largest dedicated foundries serving global fabless clients. Japan contributes via mixed-signal ASICs for robotics, medical imaging, and automotive systems supported by domestic manufacturing equipment suppliers. China prioritizes indigenous ASIC design for surveillance, telecommunications infrastructure, and electric vehicle powertrain controllers under self-sufficiency initiatives. The region serves both captive ASIC production for domestic conglomerates and merchant supply for international customers. Consumer electronics drives high-volume, cost-sensitive ASICs for smart home devices and wearables.

The increasing investments in indigenous semiconductor development, aerospace electronics and defense modernization programs are driving the application specific integrated circuit market in India. According to the ISRO July 2023, the Indian Space Research Organization and Space Applications Centre have advanced the use of ASICs in space-borne, Synthetic Aperture Radar systems used in RISAT-1A/1B satellite missions. The OBC-2.3 ASIC developed for transmit/receive controller applications in radar payloads was designed using the 0.18-micron CMOS process at Semiconductor Laboratory (SCL), Chandigarh, reflecting India’s growing domestic semiconductor manufacturing capabilities. This transition from dependence on foreign semiconductor foundries toward indigenous ASIC fabrication supports national supply chain resilience and strategic electronics development. Rising investments in satellite communication, remote sensing, phased array radar systems, and defense electronics are expected to further strengthen ASIC demand across India’s aerospace and high-technology sectors.

Japan application specific integrated circuit market reached USD 1.3 billion in 2025 and is expected to reach USD 2.2 billion by the end of 2035, and is expected to expand at a CAGR of 5.4% during the assessed period. In 2026, the market is expected to be valued at 1.4 billion. The nation is driven by the rapid expansion of the country’s semiconductor and electronic components industry. According to the JEITA January 2024 data, the production value of electronic components and devices reached USD 3.62 billion in January 2024, representing a 105.4% year-over-year increase. Integrated circuits, which form the technological foundation for ASIC development and manufacturing, accounted for USD 1.22 billion, increasing 123.4% compared to the previous year, while discrete semiconductors reached USD 483 million. The strong growth in the semiconductor production reflects increasing demand from automotive electronics, industrial automation, telecommunications infrastructure, and 5G network deployment.

Production by Japan's Electronics Industry, 2024

|

Category |

Amount |

% |

|

Consumer electronics devices |

30,034 |

128.2 |

|

Industrial electronic equipment |

258,304 |

99.1 |

|

Communication equipment |

59,046 |

94.0 |

|

Computers and information terminals |

89,309 |

110.8 |

|

Electronic application equipment |

59,655 |

85.1 |

|

Electrical measuring instruments |

42,545 |

106.0 |

|

electronic office equipment |

7,749 |

111.5 |

|

Electronic components and devices |

561,794 |

105.4 |

|

Electronic components |

239,596 |

98.8 |

|

electronic equipment |

322,198 |

111.0 |

|

Total Electronics |

850,132 |

104.1 |

Source: JEITA January 2024

North America Market Insights

The North America is projected to emerge as the fastest-growing region in the application specific integrated circuit market and is poised to expand at a CAGR of 12.4% during the assessment period, 2026 to 2035. The market is shaped by the concentrated demand from hyperscale data center operators, defense agencies, and automotive manufacturers. The U.S. leads in ASIC design activity due to its concentration of fabless semiconductor firms and cloud service providers developing custom silicon for AI inference workloads. Canada contributes via specialized design services and automotive ASIC engineering using its proximity to Detroit-based vehicle manufacturers. Government programs focus on rebuilding domestic leading-edge manufacturing capacity and reducing reliance. The region prioritizes energy-efficient ASICs for fixed-function tasks, responding to the power consumption constraints in data centers and regulatory pressures on carbon intensity.

The large scale federal investments supporting semiconductor manufacturing and advanced chip research are driving the application-specific integrated circuit (ASIC) market in the U.S. According to the NIST December 2025 data under the CHIPS and Science Act of 2022, the U.S. Department of Commerce received USD 50 billion to strengthen domestic semiconductor capabilities. The CHIPS Research and Development Office allocated USD 11 billion toward semiconductor R&D initiatives, while the CHIPS Program Office dedicated USD 39 billion for the incentives supporting manufacturing facilities and equipment investments across the U.S. These initiatives are stimulating ASIC development for AI infrastructure, automotive electronics, defense systems, and high-performance computing applications while reducing dependence on overseas semiconductor supply chains and improving long-term domestic production capacity.

Rising federal investments in semiconductor research, AI computing infrastructure, and advanced manufacturing programs are driving the application specific integrated circuit market in Canada. According to the Government of Canada's March 2025 data, USD 240 million is allocated via the Strategic Innovation Fund to strengthen domestic semiconductor and photonics development capabilities. The National Research Council Canada also continues supporting semiconductor R&D through its Advanced Electronics and Photonics Research Centre, which collaborates with industrial manufacturers developing specialized chip technologies. Additionally, the Prime Minister of Canada's April 2024 data states that USD 2 billion is invested in AI and computing initiatives, including data center and high-performance computing infrastructure programs that support ASIC deployment in AI workloads. The expansion of electric vehicle supply chains and telecommunications modernization projects is further increasing the demand for custom semiconductor solutions across Canadian industries.

Europe Market Insights

The application specific integrated circuit market in Europe is shaped by automotive safety regulations, industrial automation requirements, and sovereign semiconductor initiatives. Germany leads in automotive ASIC development for advanced driver assistance systems and battery management controllers, driven by the region's concentrated vehicle manufacturing base. France and Italy contribute via industrial ASICs for factory automation and energy grid monitoring equipment. The UK focuses on mixed-signal ASICs for aerospace and medical diagnostics, leveraging its legacy in analog design. Government programs target open-source RISC-V architectures to reduce dependence on non-European instruction set licenses, fostering customized silicon for public sector applications. Automotive electrification continues driving fixed-function accelerator demand.

Strong semiconductor manufacturing base, high industrial electronics demand, and substantial research investments are shaping the application specific integrated circuit market in Germany. According to the BFMR October 2025 data, Germany accounts for nearly 30% of the European Union’s wafer manufacturing capacity, making it the largest microelectronics hub in Europe and a key contributor to ASIC supply chains across automotive, industrial automation, and high-performance computing applications. Moreover, the microelectronics sector contributes approximately 4% directly and 15% indirectly to Germany’s gross domestic product, reflecting the sector’s strategic economic importance. On the other hand, Germany’s electrical and digital industry invests more than USD 22.7 billion annually in research and development, supporting innovation in sensors, power semiconductors, IoT security devices, and advanced semiconductor manufacturing equipment under the broader framework of the European Chips Act.

Government support for semiconductor design R&D infrastructure and supply-chain resilience initiatives is driving the application-specific integrated circuit (ASIC) market in the UK. According to the UK Government's May 2023 data under the UK Semiconductor Strategy, the government committed up to USD 266 million and up to USD 1.33 billion over the next decade to strengthen semiconductor innovation, prototyping and manufacturing capabilities. The UK is home to more than 110 semiconductor design companies, including Arm and Graphcore, supporting ASIC development for AI, automotive, telecom, and defense applications. Government-backed initiatives such as the UK Semiconductor Infrastructure Initiative and semiconductor incubator programs are improving access to chip design tools, prototyping facilities, and advanced research infrastructure.

Key Application Specific Integrated Circuit Market Players:

- Broadcom Inc. (U.S.)

- Qualcomm Incorporated (U.S.)

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Texas Instruments (U.S.)

- Analog Devices, Inc. (U.S.)

- Marvell Technology Group (U.S.)

- Microchip Technology Inc. (U.S.)

- ON Semiconductor (U.S.)

- NXP Semiconductors (Netherlands)

- Infineon Technologies (Germany)

- STMicroelectronics (Italy)

- Renesas Electronics Corporation (Japan)

- Sony Semiconductor Solutions (Japan)

- Samsung Electronics (South Korea)

- SK Hynix Inc. (South Korea)

- Accenture (Ireland)

- Tata Consultancy Services (India)

- Ericsson (Swedan)

- Cyient (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Broadcom Inc. is a dominant player in the application specific integrated circuit market, mainly for data center networking and broadband communications. The company designs high-performance ASICs that enable hyperscalers to scale AI workloads and switch fabric architectures. By offering custom silicon solutions customized to specific customer requirements, the company has reduced latency and power consumption in massive-scale computing environments.

- Qualcomm Incorporated uses the application specific integrated circuit market to power its leadership in mobile communications and edge AI. The company’s Snapdragon platform integrates custom ASICs for signal processing, modern functions, and multimedia acceleration, enabling advanced smartphone capabilities. Beyond handsets, Qualcomm develops automotive ASICs for driver assistance systems and cellular vehicle-to-everything communication.

- Intel Corporation has re-engineered its portfolio around the application specific integrated circuit market, focusing on custom silicon for AI high-performance computing and programmable logic. Through its ASIC and FPGA divisions, Intel offers customized accelerators for workloads such as genomic sequencing, financial trading, and video transcoding.

- NVIDIA Corporation has expanded beyond graphics processing units into the application specific integrated circuit market by developing custom silicon for autonomous machines, healthcare instruments, and data center acceleration. While known for GPUs, NVIDIA designs ASICs for specific functions such as video encoding/decoding, deep learning interference, and robotic control. In 2025, the company made revenue of USD 130.5 billion.

- Texas Instruments excels in the application specific integrated circuit market via its focus on mixed-signal and embedded processing solutions for industrial, automotive, and healthcare applications. The company offers semi-custom ASIC design services that integrate analog front ends, microcontrollers, and power management on a single die. In 2025, the company made a revenue of USD 2,697 billion.

Here is a list of key players operating in the global application specific integrated circuit market:

The application specific integrated circuit market is highly fragmented and is dominated by a few large players from the U.S. and Asia, with intense competition driven by the demand for AI, IoT, and 5G. U.S firms lead in high-end design and fabless innovation, while South Korea and Japan excel in memory-integrated and consumer ASICs. Europe companies focus on automotive and industrial sectors. The key strategic initiatives include vertical integration partnerships with foundries such as TSMC and investments in chiplet-based architectures to reduce the time to application specific integrated circuit market. For example, in July 2024, Accenture acquired Cientra, a silicon design and engineering services company, offering custom silicon solutions for global clients. The terms of the acquisition were not disclosed. Additionally, players are expanding into edge AI and custom data center solutions to counter the dominance of standard GPUs and FPGAs.

Corporate Landscape of the Application Specific Integrated Circuit Market:

Recent Developments

- In September 2025, Tata Consultancy Services (TCS), a global leader in IT services, consulting, and business solutions, announced the launch of its Chiplet-based System Engineering Services, designed to help semiconductor companies push the boundaries of traditional chip design.

- In June 2025, Ericsson is expanding its Research and Development (R&D) team in Bengaluru, India to enhance its capabilities in Application-Specific Integrated Circuit (ASIC) development. This strategic move underscores Ericsson's commitment to enable India to be at the forefront of future communication technology.

- In April 2025, Cyient, a leading global engineering and technology solutions company, announced the launch of its fully owned semiconductor subsidiary, Cyient Semiconductors. This strategic move strengthens the company’s commitment to innovation and excellence across the global semiconductor landscape.

- Report ID: 5533

- Published Date: May 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.