Central Lab Market Outlook:

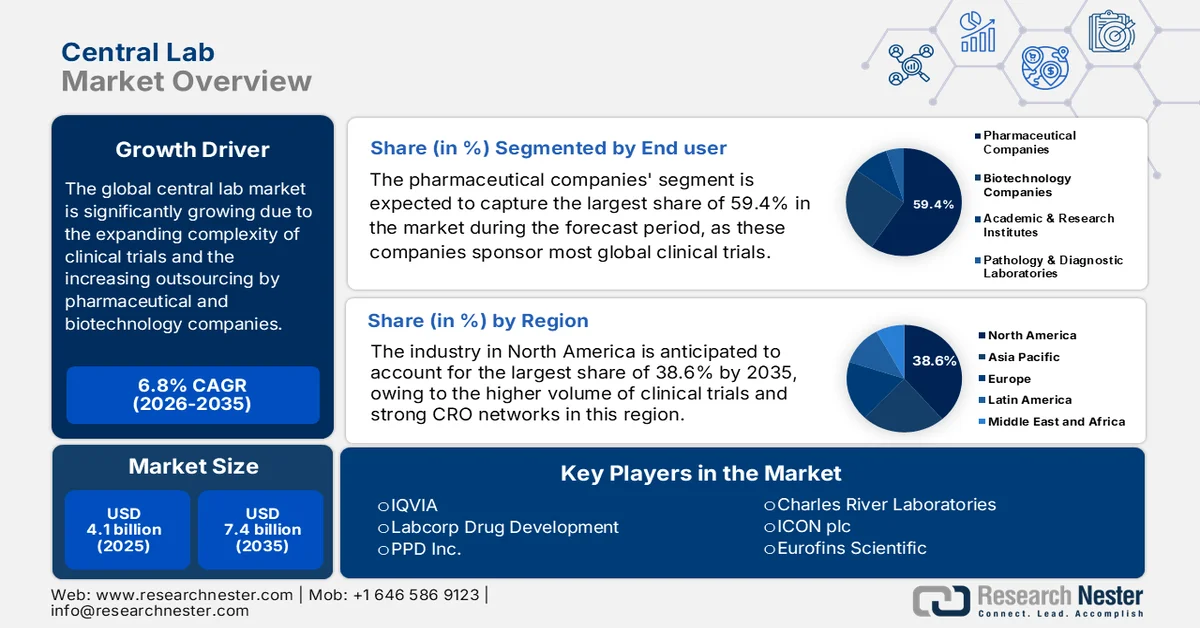

Central Lab Market was valued at USD 4.1 billion in 2025 and is anticipated to reach a value of USD 7.4 billion by 2035, expanding at a CAGR of 6.8% throughout the forecast period from 2026 to 2035. In 2026, the industry size of central lab is assessed at USD 4.3 billion.

The central lab market is positioned for sustained growth, which is largely fueled by the expanding complexity of clinical trials, particularly in oncology and rare disease research. The increasing outsourcing by pharmaceutical and biotechnology companies, which are seeking standardized, high-quality data across multi-site studies, also propels market growth. According to the article published by the World Health Organization (WHO) in November 2025, the global clinical trial registrations peaked in 2021 across most regions. In 2024, the Western Pacific region reported 27,172 trials, which is almost 25 times higher when compared to Africa’s 1,049, wherein China and Japan are the leading countries in the region. High-income countries dominate trial registrations, whereas lower-middle-income countries are showing rapid growth. Multicountry trials are counted once per country, highlighting broad geographic participation and ongoing expansion of global clinical research, denoting a huge growth potential for the central lab market in the years ahead.

Global Clinical Trial Registrations by Country in 2025: WHO Official Statistics

|

Country |

Number of Clinical Trials |

|

U.S. |

197,090 |

|

China |

162,704 |

|

India |

94,141 |

|

Japan |

67,462 |

|

Germany |

59,320 |

|

UK |

52,227 |

|

France |

50,768 |

|

Netherlands |

45,471 |

|

Iran (Islamic Republic of) |

42,951 |

|

Canada |

38,166 |

|

Spain |

37,438 |

|

Italy |

37,190 |

|

Australia |

35,499 |

|

Republic of Korea |

29,765 |

|

Brazil |

22,832 |

|

Belgium |

22,740 |

|

Türkiye |

21,679 |

|

Poland |

17,957 |

|

Denmark |

17,689 |

Source: WHO

Furthermore, the rising demand for advanced diagnostic testing globally stimulates consistent growth of the central lab market. Increasing reliance on composite reagents, automated analyzers, and quality-controlled laboratory services efficiently drives market expansion across multiple regions. In this context, the World Integrated Trade Solution reported that in 2023, the U.S. exported composite diagnostic or laboratory reagents to several international markets, in which Argentina led imports at a total of USD 57.3 million. Other significant importers included the Philippines, which is USD 17.1 million, 155,861 kg; Trinidad and Tobago, USD 9.9 million, 105,411 kg; and Lebanon imports were valued at USD 9 million, 58,118 kg. Smaller volumes were exported to countries such as Barbados, Ghana, Aruba, and Suriname, reflecting diverse global demand for laboratory reagents, hence indicating a positive outlook for the global central lab industry.

U.S. Exports of Composite Diagnostic and Laboratory Reagents by Country in 2023

|

Country |

Trade Value (USD 1000) |

Quantity (Kg) |

|

Ghana |

2,360.34 |

90,764 |

|

Aruba |

1,811.22 |

29,919 |

|

Suriname |

1,752.53 |

26,323 |

|

Occupied Palestinian Territory |

1,741.58 |

10,546 |

|

Central African Republic |

1,595.43 |

4,952 |

|

Grenada |

1,385.09 |

12,593 |

|

French Polynesia |

1,288.87 |

7,168 |

|

Angola |

1,244.84 |

22,521 |

|

Cayman Islands |

1,002.12 |

5,885 |

|

Georgia |

739.01 |

4,365 |

|

Antigua and Barbuda |

710.08 |

10,543 |

|

Tajikistan |

691.53 |

2,881 |

Source: WITS

Key Central Lab Market Insights Summary:

Regional Highlights:

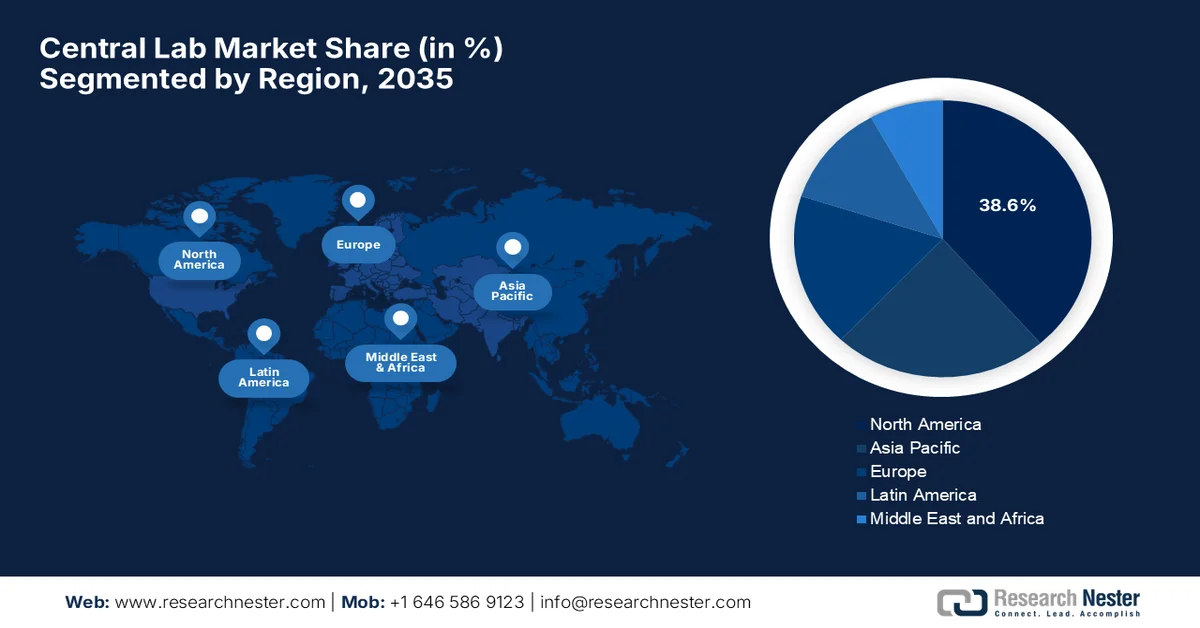

- North America central lab market is projected to command a 38.6% share by 2035, bolstered by high clinical trial volume and strong CRO networks.

- Asia Pacific is expected to witness the fastest growth during 2026–2035, fueled by massive genetically diverse patient populations and increasing outsourcing by biopharmaceutical firms.

Segment Insights:

- Pharmaceutical companies segment in the central lab market is estimated to hold a dominant 59.4% share by 2035, propelled by rising outsourcing of complex laboratory functions for global clinical trials.

- Biomarker services segment is forecasted to secure a considerable share by 2035, impelled by growing adoption of precision medicine and surrogate endpoints in clinical trials.

Key Growth Trends:

- Rising pharmaceutical & biotech R&D investment

- Growing complexity of clinical trials

Major Challenges:

- Increasing competition and pricing pressure

- Managing large-scale global clinical trials

Key Players: IQVIA (U.S.), Labcorp Drug Development (U.S.), PPD Inc. (U.S.), Charles River Laboratories (U.S.), ICON plc (Ireland), Eurofins Scientific (Luxembourg), SGS SA (Switzerland), Intertek Group plc (UK), Unilabs (Switzerland), Cerba HealthCare (France), SRL Inc. (Japan), LSI Medience Corporation (Japan), Fujirebio (Japan), Sonic Healthcare (Australia), Healius Limited (Australia), Seegene Inc. (South Korea), Green Cross Laboratories (South Korea), Metropolis Healthcare Limited (India), Dr. Lal PathLabs (India), LabConnect (U.S.), Labor Dr. Wisplinghoff (U.S.), ARUP Laboratories (U.S.), Gribbles Pathology (Malaysia).

Global Central Lab Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.1 billion

- 2026 Market Size: USD 4.3 billion

- Projected Market Size: USD 7.4 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, China, Japan, United Kingdom

- Emerging Countries: India, South Korea, Singapore, Australia, Spain

Last updated on : 20 March, 2026

Central Lab Market - Growth Drivers and Challenges

Growth Drivers

- Rising pharmaceutical & biotech R&D investment: The growth in R&D spending by pharmaceutical and biotechnology companies directly fuels demand for central lab services, as more testing is needed to support drug development. The article published by the National Institute of Health (NIH) in November 2023 states that the pharmaceutical R&D in low- and middle-income countries is growing, which is driven by both public and private investments. LMICs such as Bangladesh and Colombia are building innovation capacity through local generic production, government policies, and targeted funding, with partnerships and philanthropic support playing key roles. Clinical trial activity, including early-phase trials, is increasing, benefiting the overall central lab market. Hence, this reflects the rising pharmaceutical innovation in the Global South, but continued policy support and coordination are highly essential to unveil R&D’s full potential.

- Growing complexity of clinical trials: Trials mostly involve advanced endpoints such as biomarker analysis, pharmacogenomics, precision medicine, and cell and gene therapies, all requiring specialized laboratory knowledge. On the other hand, personalized medicine approaches and rare-disease studies increase complexity, driving outsourcing. In June 2025, Novartis started the DFT383 Phase I/II trial, which is an open-label, multi-center study assessing the safety, tolerability, and efficacy of a cellular gene therapy in pediatric participants aged 2 to 5 years with nephropathic cystinosis. The study includes two cohorts running in parallel across multiple U.S. sites. Cohort 1 participants are followed for up to 32 months in the core phase and up to 13 years in the long-term extension, whereas the other cohort is followed for 24 months. The trial involves complex endpoints, including genetic analyses, benefiting the overall central lab market.

- Demand for advanced diagnostics & biomarker testing: Central labs provide high-value services such as genetic testing, next-generation sequencing, and complex immunoassays that are essential for modern diagnostics and targeted therapies. The rise in chronic conditions such as cancer, cardiovascular diseases, and diabetes, and the focus on monitoring biomarkers, accelerate demand in the central lab market. In February 2025, the WHO revealed that Cancer is responsible for nearly 10 million deaths in a year, which is about one in six deaths. The most common cancers by incidence were breast cancer with 2.26 million cases, lung cancer with 2.21 million cases, colon and rectum cancer with 1.93 million cases, and prostate cancer with 1.41 million cases. The report also states that each year, around 400,000 children are diagnosed with cancer, underscoring the critical need for central labs to enable accurate diagnostics and support personalized treatment approaches.

Challenges

- Increasing competition and pricing pressure: The central lab market has become extremely competitive due to the presence of global contract research organizations, diagnostic laboratories, and regional service providers. As more companies enter the market, pricing pressure has intensified, particularly for routine testing services. Pharmaceutical and biotechnology companies are also looking for cost-effective solutions by focusing on maintaining high-quality standards. Therefore, such a scenario compels central labs to balance the competitive pricing with operational efficiency and service quality. In this context, companies need to differentiate themselves through advanced testing capabilities, global laboratory networks, and value-added services such as data analytics and biomarker knowledge in order to be competitive in the evolving central lab market.

- Managing large-scale global clinical trials: The central laboratories play a highly crucial role in terms of supporting large-scale multinational clinical trials, which involve numerous study sites and a large number of participants. In this context, the aspects of coordinating sample collection, testing, data reporting, and communication across multiple regions are considered to be operationally complex. On the other hand, the time zone differences, varying site capabilities, and regulatory differences can create logistical as well as administrative challenges in the central lab market. In addition, ensuring timely reporting of laboratory results is highly essential for maintaining trial timelines and regulatory submissions. Therefore, laboratories need to develop efficient project management systems and strong collaboration with clinical trial sponsors to effectively manage the complexity of global trials.

Central Lab Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 4.1 billion |

|

Forecast Year Market Size (2035) |

USD 7.4 billion |

|

Regional Scope |

|

Central Lab Market Segmentation:

End user Segment Analysis

The pharmaceutical companies end user segment is expected to dominate with the largest share of 59.4% in the central lab market during the forecast period. These companies sponsor most global clinical trials and rely on central laboratories for standardized testing, regulatory compliance, and data management across multiple trial sites. In June 2024, Labcorp announced the launch of Global Trial Connect, which is a suite of digital and data-driven central laboratory solutions especially designed to accelerate clinical trials and improve investigator site workflows. It also provides 24/7 study management support, helping sponsors speed up trial startup, patient recruitment, and data collection. Hence, such constant developments efficiently solidify the trend of outsourcing complex laboratory functions to maintain efficiency, data quality, and compliance across global clinical trials.

Service Type Segment Analysis

The biomarker services are anticipated to grow with a considerable share in the central lab market over the forecasted years. The subtype plays a pivotal role in identifying disease pathways, analyzing drug responses, and supporting precision medicine development. Biomarker testing helps researchers monitor treatment efficacy and stratify patient populations during clinical trials. In December 2025, the U.S. Food & Drug Administration (FDA) qualified hip bone mineral density change as the first-ever surrogate endpoint for osteoporosis clinical trials, thereby replacing fracture occurrence as the primary measure. This was achieved through the FNIH Biomarkers Consortium’s SABRE study, which will significantly reduce trial costs and timelines by using routine DEXA scans instead of long-term fracture monitoring. Hence, the decision marks a major advance in osteoporosis drug development, the growing importance of biomarker services in supporting precision medicine, and accelerating drug development.

Modality Segment Analysis

In the modality segment, the small molecule drug is expected to grow with a considerable revenue share in the central lab market by the conclusion of 2035. The growth of the segment is largely propelled by the continued prevalence of small-molecule therapeutics in treating a wide range of chronic and acute diseases, such as cardiovascular, metabolic, and infectious conditions. Besides the aspect of the established manufacturing and regulatory frameworks for small molecules also facilitates frequent clinical studies, efficiently driving demand for centralized laboratory services. In this context, the U.S. FDA approved 50 novel drugs in 2024, many of which were small-molecule therapies used to treat conditions such as cancer, thyroid, and other rare genetic disorders. The presence of extensive regulatory support highlights the importance of small-molecule drugs in clinical trials, which require central lab support for standardized testing as well as biomarker monitoring.

FDA 2024 Novel Drug Approvals: Officially Reported Therapies, Small-Molecule Drugs

|

Drug Name |

Active Ingredient |

Approved Use |

|

Ensacove |

Ensartinib |

Non-small cell lung cancer |

|

Itovebi |

Inavolisib |

Locally advanced/metastatic breast cancer |

|

Yorvipath |

Palopegteriparatide |

Hypoparathyroidism |

|

Sofdra |

Sofpironium |

Primary axillary hyperhidrosis |

|

Tryvio |

Aprocitentan |

Hypertension |

Source: U.S. FDA

Our in-depth analysis of the global central lab market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Service Type |

|

|

Modality |

|

|

Therapeutic Area |

|

|

Clinical Trial Phase |

|

|

Test Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Central Lab Market - Regional Analysis

North America Market Insights

North America central lab market is anticipated to garner the largest revenue share of 38.6% by the end of 2035. The region’s market is largely propelled by high clinical trial volume and strong CRO networks. Besides, there has been a surge in demand due to the expanding access to affordable, high-quality care through new insurance options. As of March 13, 2026, the U.S. accounted for almost 164,713 of the 576,032 studies registered on ClinicalTrials.gov, which is 29% of all studies. Interventional studies account for the majority. The region leads in terms of clinical research infrastructure, which is supported by robust regulatory frameworks. In May 2025, Labcorp announced the expansion of its precision oncology portfolio with new NGS panels for hematologic malignancies, which include a Rapid AML Panel, and enhanced pan-solid tumor testing, including HRD profiling. Overall, with this growing volume of clinical trials and strategic company activities, the region is poised to witness extensive demand for central labs in the years ahead.

Capabilities in advanced diagnostic testing are the primary factor responsible for uplifting the overall central lab market in the U.S. Growth in the country is also propelled by the increasing prevalence of chronic and infectious diseases, which are necessitating specialized services such as biomarker analysis, genetic testing, and complex specimen management. In February 2026, the Centers for Disease Control and Prevention stated that its Antimicrobial Resistance Laboratory Network (AR Lab Network) spans all of the 50 states, cities, and territories, which includes seven regional labs and the National TB Molecular Surveillance Center. It tracks and responds to resistant pathogens such as Candida auris, carbapenem-resistant Enterobacterales, and drug-resistant Mycobacterium tuberculosis. The report stated that since its launch, the network has conducted more than 1.5 million tests, including 664,000 whole genome sequences, enabling rapid detection and outbreak control, hence positively impacting central lab market growth.

The central lab market in Canada is growing due to a highly supportive environment for biopharmaceutical research. Market growth is also supported by a robust healthcare infrastructure, a favorable regulatory framework, and attractive research and development tax credits that draw the interest of international sponsors. In March 2024, the country’s government announced a total of USD 63.2 million investment to build new laboratory facilities under the Regulatory and Security Science Main (RSS Main) Project. The facility is located at the Canada’s Food Inspection Agency’s Ottawa Laboratory, which will focus on protecting human, plant, and animal health, food safety, emergency preparedness, and border security. This particular program is a part of the USD 1.05 billion Laboratories Canada strategy, and it will provide federal scientists with modern, sustainable, and collaborative research infrastructure to advance national science priorities.

APAC Market Insights

The Asia Pacific central lab market is expected to register the fastest growth from 2026 to 2035. The region’s leadership is effectively attributable to its massive, genetically diverse patient populations. This expansion is heavily supported by healthcare infrastructure and a strategic shift by global biopharmaceutical firms toward cost-effective outsourcing models. As per the article published by WHO in November 2024, the Global Laboratory Leadership Programme (GLLP), which was developed by WHO and partners, is strengthening laboratory leadership across the Asia Pacific to improve outbreak detection and response. It also mentions a recent workshop that brought leaders from 12 countries together to build core competencies, foster collaboration, and promote a One Health approach linking human, animal, and environmental health. By enhancing managerial and technical skills, the program equips laboratory leaders to respond more effectively to public health threats, making it suitable for bolstering the regional market growth.

A significant surge in terms of domestic biopharmaceutical innovation and continued facility expansions boost the overall central lab market in China. The supportive government policies and regulatory reforms by the National Medical Products Administration (NMPA) that have harmonized local standards with international requirements are making the country even more attractive for global multi-center trials. For instance, in July 2023, Labcorp announced the expansion in China with a new kit production facility in Suzhou, along with an upgraded immunology and immunotoxicology lab in Shanghai. The company stated that the Suzhou site reduces overseas shipping costs and lead times while meeting global quality standards, and the Shanghai expansion adds advanced capabilities such as flow cytometry, PCR assays, and cell and gene therapy support. Hence, these investments strengthen the country’s prominence in advancing drug development and patient care.

The central lab market in India is efficiently evolving into a global hub for clinical research, which is driven by the vast and treatment-naive patient population. The country’s market also benefits from a highly favorable cost-to-quality ratio and a network of accredited facilities that comply with international standards such as those set by the National Accreditation Board for Testing and Calibration Laboratories (NABL). In December 2025, the Ministry of Health & Family Welfare reports disclosed that 1,81,873 Ayushman Arogya Mandirs were functional across India, as of November 2025, which were delivering primary healthcare services under PM-ABHIM. It stated that 744 Integrated Public Health Laboratories have been approved nationwide to enable real-time disease surveillance and outbreak preparedness through the integrated health information platform, thus making it suitable for standard central lab market growth.

Europe Market Insights

Europe central lab market is solidifying its position in the global landscape on account of a high degree of integration between clinical research organizations and pharmaceutical developers. The region’s growth is efficiently fueled by its focus on early disease detection and its role as a leading hub for multi-country clinical trials. In January 2026, the European Centre for Disease Prevention and Control reported that three new EU reference laboratories for food- and waterborne diseases became operational to strengthen Europe’s outbreak detection and response. It will cover bacteria, helminths, and viruses, and support national labs with specialized testing, harmonized methods, and proficiency programs. Their role is to ensure reliable, comparable data across the regional countries, improving surveillance and preparedness against cross-border health threats, hence suitable for the market’s expansion and exposure.

A highly sophisticated diagnostic infrastructure and a strong emphasis on quality assurance are responsible for uplifting the central lab market in Germany. As a primary hub for biopharmaceutical research and development, the market benefits from a dense network of world-class academic institutions and private laboratories that drive innovation in complex testing areas like molecular diagnostics and oncology. According to the NIH April 2025 article, laboratory medicine is a foundation of evidence-based healthcare in the country, with almost 1,200 specialists in laboratory medicine and 840 in microbiology. It also underscored that laboratory physicians are the second most consulted non-curative specialty after general practitioners. About 108,000 people work in medical laboratories, accounting for 1.8% of the healthcare workforce, with annual diagnostic costs being 2.6% of total healthcare spending.

The UK central lab market is growing based on factors such as a well-established life sciences ecosystem and a proactive regulatory environment. The market is currently being revitalized by technological innovation and the rapid adoption of AI-based analytics, digital pathology, and automated sample management systems to handle increasingly complex biomarker and genetic testing. Based on the government data in December 2024, UKHSA launched the Diagnostic Accelerator, which is a specialist team designed to speed up the development and rollout of diagnostic tests for emerging infectious disease threats. The initiative readily enhances pandemic preparedness by improving the rapid availability of tests such as PCR, molecular point-of-care, and lateral flow devices. The government also noted that such initiatives build partnerships with industry, academia, and NGOs to target pathogens with the greatest epidemic potential.

Key Central Lab Market Players:

- IQVIA (U.S.)

- Labcorp Drug Development (U.S.)

- PPD Inc. (U.S.)

- Charles River Laboratories (U.S.)

- ICON plc (Ireland)

- Eurofins Scientific (Luxembourg)

- SGS SA (Switzerland)

- Intertek Group plc (UK)

- Unilabs (Switzerland)

- Cerba HealthCare (France)

- SRL Inc. (Japan)

- LSI Medience Corporation (Japan)

- Fujirebio (Japan)

- Sonic Healthcare (Australia)

- Healius Limited (Australia)

- Seegene Inc. (South Korea)

- Green Cross Laboratories (South Korea)

- Metropolis Healthcare Limited (India)

- Dr. Lal PathLabs (India)

- LabConnect (U.S.)

- Labor Dr. Wisplinghoff (U.S.)

- ARUP Laboratories (U.S.)

- Gribbles Pathology (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- IQVIA is one of the leading players in the central lab market, which is offering integrated clinical research and laboratory services to pharmaceutical and biotechnology companies. The company benefits from its global laboratory network and improved analytics capabilities, which support highly complex clinical trials.

- Labcorp Drug Development is one of the most prominent central lab providers in the global landscape. Besides, the firm provides laboratory testing services for clinical trials, i.e., for biomarker testing, genomics, and companion diagnostics. LabCorp efficiently supports multinational trials with standardized processes and rapid turnaround times.

- PPD Inc., which operates as part of Thermo Fisher Scientific, provides laboratory testing, bioanalytical services, and biomarker analysis for clinical trials across multiple therapeutic areas. In addition, the firm has a strong international network of laboratories, which allows efficient handling of clinical samples and complex testing requirements.

- Eurofins Scientific is a major laboratory testing provider that has a huge network of laboratories across the globe. The company offers specialized testing services, which include central lab support for clinical trials, biomarker analysis, and bioanalytical testing.

- ICON plc is yet another prominent player in this field, which supports pharmaceutical, biotechnology, and medical device firms in terms of their laboratory testing, biomarker services, and sample management. ICON has strengthened its market position through acquisitions and strategic partnerships, enabling it to expand its service offerings and global reach.

Below is the list of some prominent players operating in the global central lab market:

The central lab market is characterized by the presence of CROs, diagnostic laboratories, as well as testing service providers. Major players such as IQVIA, Labcorp Drug Development, and ICON plc dominate the market through extensive global laboratory networks and integrated clinical trial services. Pioneers in this field are making extensive investments in terms of automation, molecular technologies, and digital data platforms with a prime focus on improving efficiency and accuracy. Mergers and acquisitions, partnerships with pharmaceutical companies, and expansion into emerging markets are adopted by the players to strengthen service portfolios and enhance the overall geographic reach. In December 2024, Eurofins Central Laboratory announced the acquisition of Clinical Trial Pathology Services' assets from DCL Pathology LLC. This particular move strengthens Eurofins’ portfolio, particularly in terms of oncology and vaccine development, enhancing support for pharma, biotech, and CRO clients worldwide.

Corporate Landscape of the Central Lab Market:

Recent Developments

- In March 2026, LabConnect inaugurated a new central laboratory facility in Wuxi, China, thereby expanding its global network to support multi-regional clinical trials. The site is developed with Teddy Laboratory, which integrates advanced logistics, biorepository services, and unified data oversight to meet international standards.

- In February 2026, ARUP Laboratories announced the launch of Innovation Central Laboratory in Salt Lake City to accelerate diagnostic innovation in collaboration with biotechnology, pharmaceutical, and other industrial partners.

- In May 2024, LabConnect and Labor Dr. Wisplinghoff announced a strategic alliance to deliver high-quality, central laboratory services in Europe to support global clinical trials.

- Report ID: 4233

- Published Date: Mar 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Central Lab Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.