C-RAN Architecture Market Outlook:

C-RAN Architecture Market size was valued at USD 22.59 billion in 2025 and is likely to cross USD 84.48 billion by 2035, expanding at more than 14.1% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of C-RAN architecture is estimated at USD 25.46 billion.

The rapid growth of mobile data traffic requires a more efficient and cost-effective network architecture to support the growing demand for high-speed mobile data services. C-RAN technology enables mobile network operators to optimize network resources and provide a better quality of service to their customers. C-RAN architecture improves spectral efficiency by using centralized processing to optimize resource allocation and reduce interference. According to a study, the C-RAN architecture can improve spectral efficiency by up to 55% compared to the traditional RAN architecture.

The deployment of 5G technology requires new network architectures that can handle high-speed data transfer and low-latency requirements. C-RAN architecture offers a more efficient and flexible solution for the 5G network and is a major driver for the growth of the market. According to a report, the number of global 5G subscriptions is estimated to reach 580 million by the end of 2021 and 3.5 billion by the end of 2026. This significant increase in 5G subscriptions is expected to drive demand for C-RAN architectures. C-RAN architecture will provide better network performance, coverage, and capacity needed to support the growing number of 5G devices.

Key C-RAN Architecture Market Insights Summary:

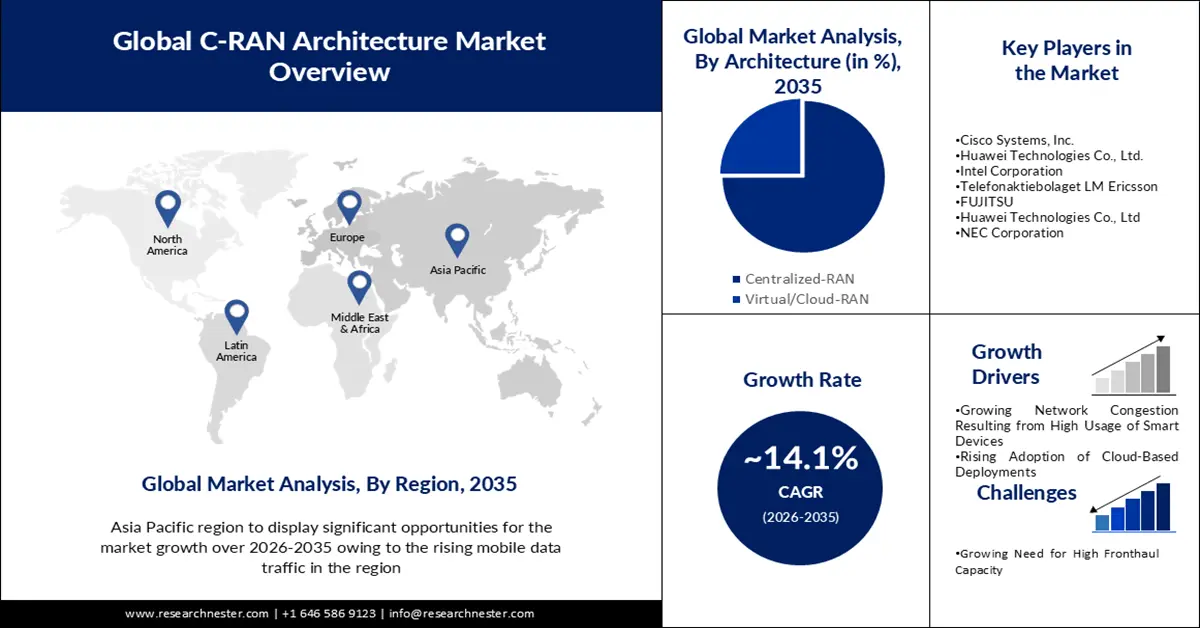

Regional Highlights:

- By 2035, Asia Pacific is projected to secure a 37% share of the c-ran architecture market, supported by rising mobile data traffic and expanding telecom investments owing to growing IoT and advanced analytics adoption.

- Europe is anticipated to advance steadily through 2026–2035, capturing a substantial share as 5G rollouts and LTE upgrades expand, fueled by increasing cloud-based C-RAN deployments.

Segment Insights:

- The 5G segment in the c-ran architecture market, is poised to command the largest share by 2035, bolstered by surging traffic volumes and the need for energy-efficient architectures spurred by global 5G subscription growth.

- The centralized-RAN segment is projected to lead by 2035 as centralized baseband processing improves resource efficiency and minimizes power consumption, enabled by optimized fronthaul connectivity.

Key Growth Trends:

- Growing Network Congestion Resulting from High Usage of Smart Devices

- Rising Adoption of Cloud Based Deployments

Major Challenges:

- High Implementation Cost

- Network Latency

Key Players: Nokia Corporation, Cisco Systems, Inc., Huawei Technologies Co., Ltd., Intel Corporation, Telefonaktiebolaget LM Ericsson, FUJITSU, Huawei Technologies Co., Ltd, NEC Corporation, ZTE Corporation, Samsung Electronics Co Ltd.

Global C-RAN Architecture Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 22.59 billion

- 2026 Market Size: USD 25.46 billion

- Projected Market Size: USD 84.48 billion by 2035

- Growth Forecasts: 14.1%

Key Regional Dynamics:

- Largest Region: Asia Pacific (37% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Indonesia, Vietnam, Brazil, Mexico

Last updated on : 19 November, 2025

C-RAN Architecture Market - Growth Drivers and Challenges

Growth Drivers

- Growing Network Congestion Resulting from High Usage of Smart Devices - Using high-bandwidth applications such as video streaming, online gaming, and video conferencing also contributes to network congestion. Video streaming accounted for 60% of global mobile data traffic in 2020, according to a report. As the smart device usage increases it leads to more network congestion and internet traffic which further leads to problems such as dropped calls, low internet, buffering, and other concerns. C-RAN architecture can help to solve this issue by deploying small cells to the operators, this can be helpful in providing additional coverage and capacity in the high internet traffic areas. This can look into the problem of network congestion and can improve the network performance quickly.

- Rising Adoption of Cloud-Based Deployments – Growing implementation of cloud-based deployment is anticipated to drive the growth of the market in the forecast period. The emergence of 5G technology is also driving the adoption of cloud-based deployments in the market.

- Increasing Demand for High-Speed Mobile Data Services – According to a report, global mobile data traffic will grow by 49% in 2020 and is expected to grow by nearly 30% annually until 2025. This growth is primarily driven by the increased use of mobile video, social networking, and other high-bandwidth applications that require more efficient and cost-effective network architectures such as C-RAN.

- Rising Demand for Edge Computing - Edge computing is becoming increasingly important in the telecommunications industry as it allows data to be processed and analyzed closer to the source. This reduces latency and improves network performance. C-RAN architecture is able to support edge computing, thus becoming a key driver of market growth. As per a study, edge computing helps operators monitor network performance and security in real time, enabling them to detect and respond to threats faster.

Challenges

- High Implementation Cost - Deploying C-RAN architecture has a high initial cost as it requires significant investment in centralized processing and backhaul infrastructure. These costs can be a significant barrier to entry for small service providers and service providers operating in emerging markets.

- Network Latency

- Growing Need for High Fronthaul Capacity

C-RAN Architecture Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.1% |

|

Base Year Market Size (2025) |

USD 22.59 billion |

|

Forecast Year Market Size (2035) |

USD 84.48 billion |

|

Regional Scope |

|

C-RAN Architecture Market Segmentation:

Network Type Segment Analysis

The global C-RAN architecture market is segmented and analyzed for demand and supply by network type into 5G, 4G, and LTE. Out of these, the 5G segment is anticipated to account for the largest market share by the end of 2035. The massive increase in traffic and severe impact on the power consumption of current network architectures impose additional cost burdens on network operators. Therefore, carriers are looking for better alternative technologies and architectures to help reduce energy costs, improve coverage, agile network traffic management, and increase hourly throughput. According to a report, the number of global 5G subscriptions reached up to 580 million by the end of 2021 and is anticipated to reach 3.5 billion by the end of 2026.

Architecture Segment Analysis

The global market is segmented and analyzed for demand and supply by architecture into Centralized-RAN and Virtual/Cloud-RAN. Out of these, the centralized-RAN segment is estimated to account for the largest market share by the end of 2035. In a centralized RAN architecture, baseband processing is centralized at a central location (data center or central hub). Remote Radio Units (RRUs) are connected to the central site through a fronthaul network that carries digitized baseband signals between the central site and the RRUs. This architecture enables more efficient resource allocation and reduces power consumption.

Our in-depth analysis of the global market includes the following segments:

|

By Network Type |

|

|

By Architecture |

|

|

By Service |

|

|

By End User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

C-RAN Architecture Market - Regional Analysis

APAC Market Insights

The market in the Asia Pacific industry is expected to dominate majority revenue share of 37% by 2035. This can be attributed on the back of the rising mobile data traffic, growing investments in the telecom industry, and rapid increase in the adoption of technologies, such as IoT and advanced analytics, in the region. The internet traffic in the Asia Pacific was approximately 28 exabytes per month in 2017, which rose to about 75 exabytes per month by the end of the year 2020.

Europe Market Insights

Moreover, the market in Europe is also expected to witness robust growth during the forecast period. This can be attributed owing to the surge in the rollout of 5G networks, the rise in developments in LTE infrastructure, and the growing usage of video and music streaming applications in the region. In addition, improved 4G coverage across the European continent is also projected to boost this region’s market growth in the coming years. The market for C-RAN architecture in Europe is driven by the increasing adoption of cloud-based deployments. Cloud RAN deployments are expected to account for 40% of all his RAN deployments in Europe by 2025, according to the report. The deployment of 5G technology is also expected to boost the growth of the C-RAN architecture market in Europe. According to reports, Europe is expected to have an estimated 214 million 5G connections by 2025, making him one of the leading regions for 5G deployment. The European regulatory environment also favors the introduction of C-RAN architectures. For instance, the European Union has launched several initiatives to accelerate the adoption of cloud computing. It is hoped that this will drive the adoption of cloud-based C-RAN architecture.

North American Market Insights

The market in the North American region is estimated to account significant market share by the end of 2035. Market growth is driven by factors such as increasing demand for high-speed connectivity, increasing adoption of 5G technology, and the need for efficient network management. The deployment of 5G technology is expected to drive the growth of the market in North America. North America is expected to become one of the leading regions for 5G deployment, with an estimated 407 million 5G connections by 2025, according to reports. The North American regulatory environment favors the deployment of C-RAN architectures. For example, the US Federal Communications Commission (FCC) has launched several initiatives to accelerate the deployment of 5G networks. This is expected to drive the adoption of C-RAN architecture. Some of the key players operating in the North American C-RAN architecture market include Nokia, Ericsson, Huawei, ZTE, and Samsung. These companies are investing heavily in R&D to create advanced C-RAN solutions to meet the growing demand in the market. Therefore, the market for C-RAN architectures in North America is expected to grow steadily in the coming years, driven by the increasing adoption of 5G technology, favorable regulatory environment, and adoption of cloud-based deployments.

C-RAN Architecture Market Players:

- Nokia Corporation

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Intel Corporation

- Telefonaktiebolaget LM Ericsson

- FUJITSU

- Huawei Technologies Co., Ltd

- NEC Corporation

- ZTE Corporation

- Samsung Electronics Co Ltd.

Recent Developments

- Nokia Corporation commercialized the company’s next-generation Airscale Cloud RAN solution that helps operators to enable flexible end-to-end network slicing, generate revenue from 5G services, and meet IoT requirements.

- Fujitsu Network Communications is promoting Open Radio Access Network (Open RAN) technology with meta-connectivity worldwide. Under the deal, Fujitsu will provide 5G Massive MIMO (Multiple Input, Multiple Output) Radio Units (RU) to Evenstar.

- Report ID: 3422

- Published Date: Nov 19, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.