Automotive Robotics Market Outlook:

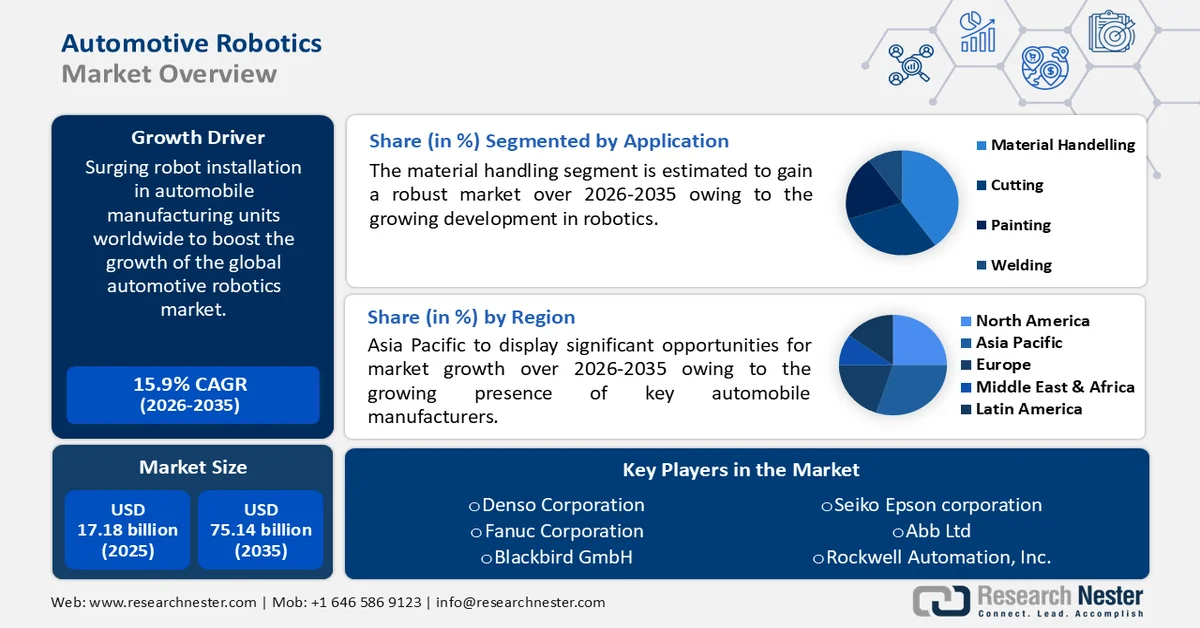

Automotive Robotics Market size was valued at USD 17.18 billion in 2025 and is set to exceed USD 75.14 billion by 2035, expanding at over 15.9% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of automotive robotics is estimated at USD 19.64 billion.

The expansion of the market can be ascribed to the rising adoption of robots in car making. According to data published by the International Federation of Robotics, in March 2023, 1 million robots worked in the car industry globally. Robots are used for various tasks such as arc welding, painting, internal logistics, material handling, and spot welding among others. The automotive sector is the number one adopter of industrial robots, reaching up to 33% of all installations in the U.S. in the last year. In 2023, Volvo Cars took the lead in enhancing its workplace environment and retaining talent. The company has acquired more than 1,300 robots from ABB to assemble its next generation of electric vehicles.

Key Automotive Robotics Market Insights Summary:

Regional Highlights:

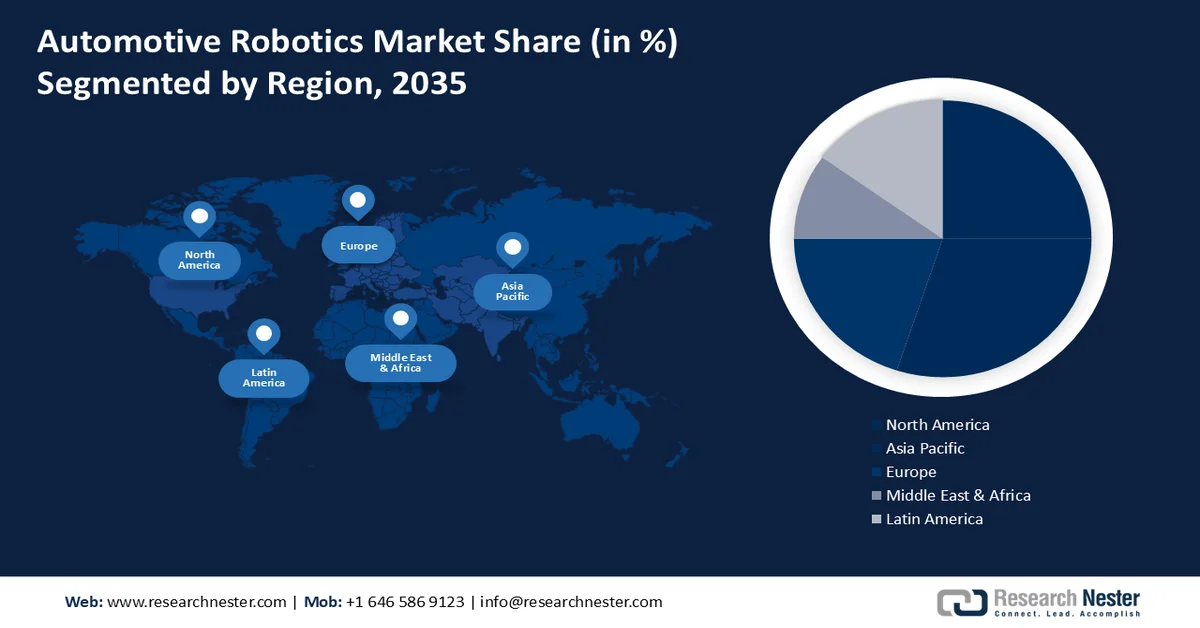

- The Asia Pacific is anticipated to command the largest revenue share by 2035 in the automotive robotics market, impelled by the rising automation industry and advancements in artificial intelligence.

- North America is projected to experience substantial expansion in the automotive robotics market through 2026-2035, attributable to the presence of leading market players and strong demand for robots to enhance operational productivity.

Segment Insights:

- The material handling segment of the automotive robotics market is projected to account for the largest revenue share by 2035, propelled by rising attempts from industrialists to reduce workplace accidents and labor costs.

- The robotic arm segment is anticipated to witness rapid growth during 2026-2035, driven by increasing automation in the automotive sector and growing investments in AI-driven robotic arms for enhanced production efficiency and quality control.

Key Growth Trends:

- Rising efforts for efficacy

- Increasing demand for cars

Major Challenges:

- High initial investment and lack of expertise

Key Players: Seven Corners Inc., Berkshire Hathaway Specialty Insurance, TravelSafe Insurance, Assicurazioni Generali S.p.A., Trip Mate, Inc., AXA, Chubb Group Holdings Inc., Insure & Go Insurance Services Limited, Zurich Insurance Group Ltd, American International Group, Inc.

Global Automotive Robotics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 17.18 billion

- 2026 Market Size: USD 19.64 billion

- Projected Market Size: USD 75.14 billion by 2035

- Growth Forecasts: 15.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific

- Fastest Growing Region: North America

- Dominating Countries: Japan, Germany, China, United States, South Korea

- Emerging Countries: Brazil, Mexico, Argentina, Chile, Colombia

Last updated on : 25 February, 2026

Automotive Robotics Market - Growth Drivers and Challenges

Growth Drivers

-

Rising efforts for efficacy: Robots can not only lessen the probability of human errors but also raise operational efficiency. Major market players such as BMW and Mercedez Benz are incorporating humanoids to enhance work efficiency and reduce accidents. Chemical exposure, fire hazards, slip-and-fall accidents, heat stress, and hearing loss are some of the most common accidents faced by workers. The introduction of robots in the automotive industry prevents these risks to a great extent. According to the Bureau of Labor Statistics, in 2020, there were 9,940 cases of automotive service technicians found with illness and non-fatal injury.

-

Increasing demand for cars: According to the European Automobile Manufacturers Association in 2024, the global car production reached 76 million units. In the coming years, the number is projected to increase at an exponential rate. Robots have faster operating times resulting in to higher level of productivity. Additionally, robots increase productivity because of their prolonged hours of operation without any chance of fatigue.

Challenges

-

High initial investment and lack of expertise: The price of cobots/humanoids/robots is exorbitant and needs a large beforehand investment. Also, there is a lack of control engineers resulting in scarce expertise. After the deployment of robots in the car manufacturing units, their maintenance cost is quite high. Automotive robots require compulsive preventive maintenance to avoid any chance of failure.

Automotive Robotics Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.9% |

|

Base Year Market Size (2025) |

USD 17.18 billion |

|

Forecast Year Market Size (2035) |

USD 75.14 billion |

|

Regional Scope |

|

Automotive Robotics Market Segmentation:

Application Segment Analysis

The material handling segment in automotive robotics market is anticipated to garner the largest revenue by the end of 2035. The growth of the segment can be attributed to the rising attempt from industrialists to reduce the chance of accidents and labor costs. For instance, KUKA AG offers a wide range of palletizing robots for material handling with payloads from 40 to 1300 kilograms. Also, these robots reach up to 3,601 millimeters. These provide short cycle times and increased throughput amalgamated with low space requirements.

Component Segment Analysis

The robotic arm segment is expected to register rapid growth during the forecast period owing to increasing automation in the automotive sector, high usage of robotic arms in electric vehicles and self-driving cars to enhance production and efficiency, and growing investments in AI-driven robotic arms for better quality control and improved decision-making.

Our in-depth analysis of the global automotive robotics market includes the following segments:

|

Type |

|

|

Component |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Robotics Market - Regional Analysis

Asia Pacific Market Insights

The automotive robotics market in Asia Pacific is projected to hold the largest revenue share by the end of 2035 driven by the rising automation industry and advancements in artificial intelligence. According to the International Federation of Robotics in 2023, Aisa had a robot density of 182 units per 10,000 persons deployed in manufacturing. Japan and China are amongst the top 10 automated countries globally. In fact, in 2023, Japan took 3rd place surpassing Japan and Germany, possessing a robot density of 470 per 10,000 employees.

In India, with the rising vehicle demand, and government initiatives such as production-linked incentives (PLI) for automotive sectors, market is expected to fuel market growth during the forecast period. In addition, the integration of AI, ML, and IoT in robotics to enhance efficiency, production, and precision is expected to boost market growth going ahead.

North America Market Insights

North America is also witnessing burgeoning market expansion during an assessed period. The market expansion can be ascribed to the presence of leading market players. There is a huge demand for automotive robots to enhance the productivity of operations. According to The Association for Manufacturing Technology, in the U.S. top category for using industrial robots was automotive in 2021. The data further says that in the same year, there were 9,782 robots installed in the country’s auto industry.

Key Automotive Robotics Market Players:

- Kawasaki Heavy Industries, Ltd.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Seiko Epson Corporation

- Rockwell Automation, Inc.

- ABB Ltd, Switzerland

- Denso Corporation

- Comau S.p.A.

- Fanuc Corporation

- Yaskawa Electric Corporation

- Blackbird GmbH

- Nachi Fujikoshi Corp.

The competitive landscape of the market is rapidly evolving as established key players, automotive giants, and new entrants are investing in advanced technologies. Key players in the market are focused on developing new technologies and products catering to the stringent regulatory norms and consumer demand. These key players are adopting several strategies such as mergers and acquisitions, joint ventures, partnerships, and novel product launches to enhance their product base and strengthen their market position. Here are some key players operating in the global market:

Recent Developments

- In December 2024, ABB Robotics announced the launch of a new autonomous mobile robotics training and showroom facility in Madrid, Spain. This initiative was launched to cater to the growing demand for skilled professionals in the expanding AMR market.

- In March 2022, Fanuc America Corporation announced the release of the CRX-5iA, CRX-20iA/L, and CRX-25iA collaborative robots. These new machines are part of the popuslar CRX series that also includes the CRX-10iA and CRX-10iA/L collaborative robots.

- Report ID: 324

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.