Automotive Carbon Fiber Composites Market Outlook:

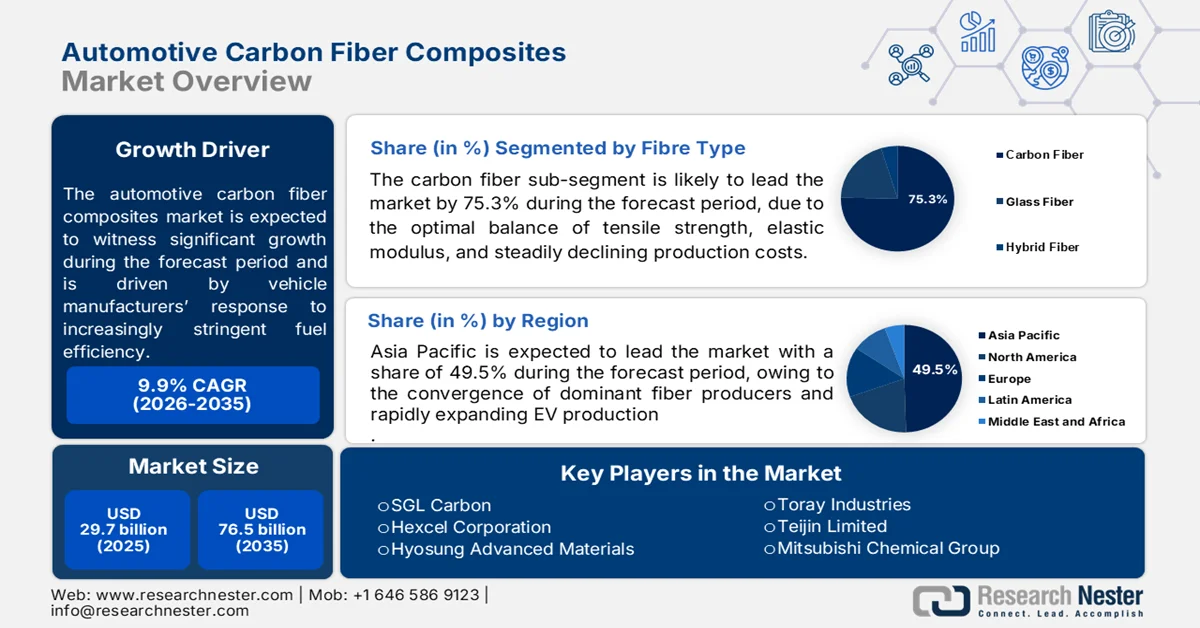

Automotive Carbon Fiber Composites Market size was valued at USD 29.7 billion in 2025 and is projected to cross USD 76.5 billion by the end of 2035, expanding at more than 9.9% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of automotive carbon fiber composites is estimated at USD 32.7 billion.

Automotive carbon fiber composites are gaining traction as vehicle manufacturers respond to increasingly stringent fuel-efficiency and emissions requirements established by government agencies across major automotive markets. In the U.S., the U.S. Department of Energy 2026 data has highlighted lightweight materials as a key pathway for reducing vehicle energy consumption, noting that a 10% reduction in vehicle weight can improve fuel economy by approximately 6%–8%, while a 25% weight reduction can deliver fuel-economy, depending on vehicle type and powertrain configuration. Carbon fiber composites are therefore being incorporated into structural, semi-structural, and exterior vehicle components to support compliance with regulatory objectives while maintaining vehicle performance and safety standards.

The transition toward electrified mobility is creating additional demand for automotive carbon fiber composites because vehicle mass directly affects battery efficiency and driving range. According to the U.S. Environmental Protection Agency (EPA) May 2026 data, transportation accounted for approximately 28% of total U.S. greenhouse gas emissions in recent reporting years, making vehicle efficiency improvements a major policy focus. Government agencies and public research organizations have emphasized lightweight materials as an important tool for extending electric vehicle range without proportionally increasing battery size. As automotive manufacturers increase production of battery-electric and hybrid vehicles while meeting regulatory efficiency targets, carbon fiber composites are expected to secure a larger role in vehicle design, supported by ongoing government-funded material research, manufacturing innovation programs, and transportation decarbonization policies.

Key Automotive Carbon Fiber Composites Market Insights Summary:

Regional Highlights:

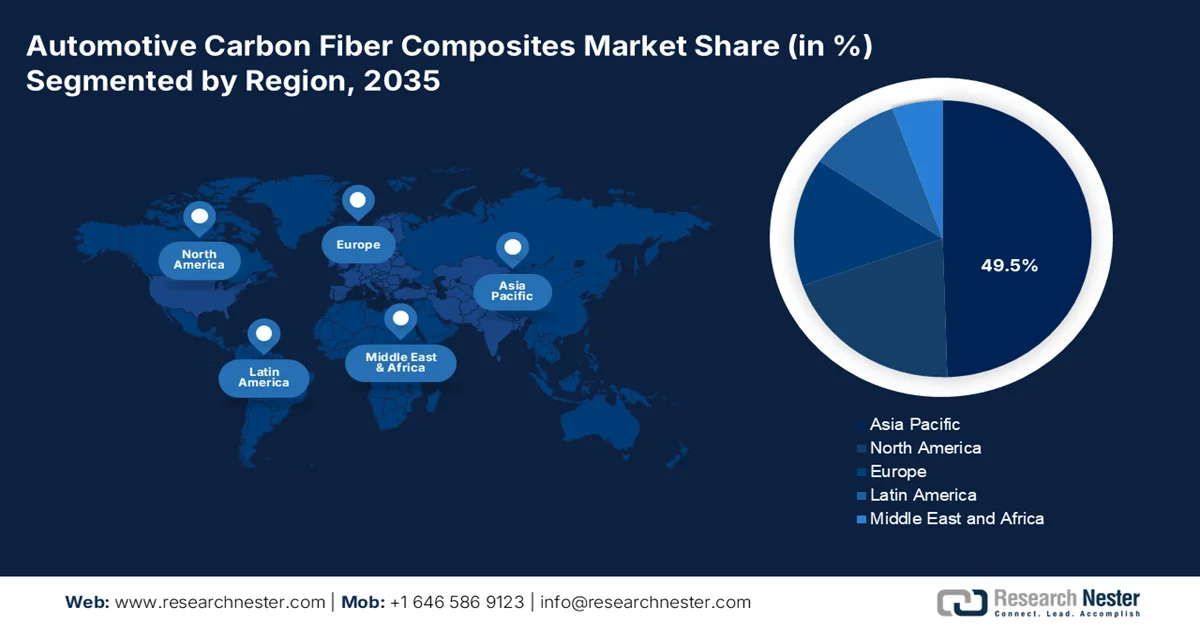

- The Asia Pacific automotive carbon fiber composites market is anticipated to command 49.5% of regional revenue by 2035, underpinned by the convergence of dominant fiber producers in Japan and South Korea, rapidly expanding EV production in China, and cost-competitive manufacturing bases in India and Southeast Asia

- North America is expected to witness the fastest expansion during 2026-2035, stimulated by the strong synergy between U.S. lightweighting regulations and Canadian clean-energy incentives fostering a collaborative cross-border supply chain

Segment Insights:

- In the automotive carbon fiber composites market, carbon fibers are forecast to secure a 75.3% share by 2035, supported by the optimal balance of tensile strength, elastic modulus, and steadily declining production costs

- Epoxy resins are projected to maintain the leading position throughout the forecast period, reinforced by their exceptional adhesion to carbon fiber, low cure shrinkage, and superior chemical resistance against automotive fluids

Key Growth Trends:

- Government-funded vehicle programs

- Expansion of electric vehicle incentive programs

Major Challenges:

- High raw material costs

- Lengthy qualification cycles

Key Players: Toray Industries (Japan), Teijin Limited (Japan), Mitsubishi Chemical Group (Japan), SGL Carbon (Germany), Hexcel Corporation (U.S.), Hyosung Advanced Materials (South Korea).

Global Automotive Carbon Fiber Composites Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 29.7 billion

- 2026 Market Size: USD 32.7 billion

- Projected Market Size: USD 76.5 billion by 2035

- Growth Forecasts: 9.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (49.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Canada, Mexico, Thailand, Vietnam

Last updated on : 24 June, 2026

Automotive Carbon Fiber Composites Market - Growth Drivers and Challenges

Growth Drivers

- Government-funded vehicle programs: Public investment in vehicle efficiency and lightweight transportation technologies remains a major demand driver for automotive carbon fiber composites. The IEA 2025 data continues to fund advanced manufacturing and lightweight materials programs through the Vehicle Technologies Office. In FY2025, approximately USD 425 million for Vehicle Technologies programs supporting advanced materials, electrification, and manufacturing innovation. These investments encourage the commercialization of lightweight structural materials across passenger and commercial vehicle segments. Carbon fiber composites are increasingly included in publicly funded mobility demonstrations and industrial partnerships aimed at lowering transportation energy consumption.

- Expansion of electric vehicle incentive programs: Global EV support programs are creating strong demand for lightweight materials because vehicle mass directly affects energy efficiency and battery utilization. The International Energy Agency (IEA) 2025 reported that global electric vehicle sales surpassed 17 million units, representing more than one-fifth of global car sales. Governments continue to allocate substantial resources toward EV adoption. As automakers seek longer driving ranges without proportionately increasing battery sizes, carbon fiber composites are increasingly evaluated for body structures, battery enclosures, and reinforcement components. This trend is particularly visible in premium EV platforms and next-generation mobility programs supported by public funding.

Challenges

- High raw material costs: PAN-based precursor prices remain volatile, compressing margins for new entrants. Established players like Toray and SGL benefit from long-term supply contracts, whereas startups face spot-market premiums. Vertical integration into precursor manufacturing is capital-intensive, deterring smaller suppliers. Teijin mitigates this through strategic partnerships with petrochemical firms, securing acrylonitrile at stable rates, but this barrier persists for independent composite manufacturers.

- Lengthy qualification cycles: Automotive OEMs mandate years of validation testing for structural carbon fiber parts, including fatigue, crash, and environmental aging. New suppliers lack the financial runway to sustain zero-revenue qualification periods. Hexcel overcame this by co-developing parts with BMW during early prototype phases, sharing R&D costs. However, most entrants struggle to meet IATF 16949 and OEM-specific standards without prior Tier-1 relationships.

Automotive Carbon Fiber Composites Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.9% |

|

Base Year Market Size (2025) |

USD 29.7 billion |

|

Forecast Year Market Size (2035) |

USD 76.5 billion |

|

Regional Scope |

|

Automotive Carbon Fiber Composites Market Segmentation:

Fiber Type Segment Analysis

Under the fiber type segment, the carbon fibers are leading and is poised to hold the share value of 75.3% by the end of 2035. The segment is driven by the optimal balance of tensile strength, elastic modulus, and steadily declining production costs. According to the DOE June 2026 data, the carbon fiber reinforced composites has the capacity to reduce the weight of some components by 50% to 75% compared to steel versus aluminum. This dramatic lightweighting directly translates to extended EV range, improved acceleration, and lower brake/tire wear emissions key regulatory drivers under CAFE and Euro 7 standards. PAN fibers achieve this through their exceptional specific strength, enabling thinner gauges without sacrificing crashworthiness. This weight efficiency, combined with falling PAN precursor costs, ensures PAN-based fibers remain the structural backbone of the automotive carbon fiber composites market through 2035.

Resin Type Segment Analysis

The epoxy resins capture the largest share in the market driven by their exceptional adhesion to carbon fiber, low cure shrinkage, and superior chemical resistance against automotive fluids. Its thermoset nature provides superior creep resistance and dimensional stability under sustained mechanical loads, making it ideal for structural and semi-structural components. Furthermore, epoxy's ability to wet-out carbon fiber tows uniformly ensures optimal load transfer between fibers, maximizing the composite's strength-to-weight potential. Emerging rapid-cure epoxy systems are now compatible with high-volume production cycles, bridging the performance gap between aerospace-grade composites and automotive cost targets. This versatility ensures epoxy remains the preferred resin system for exterior panels, chassis structures, and battery enclosures in the market.

Application Segment Analysis

In the automotive carbon fiber composites market, structural assembly sub-segment is leading under the application segment. The segment is driven by validated lightweighting outcomes from recent academic research. NLM October 2025 study demonstrated that optimized battery pack enclosures achieved an 11.61% mass reduction while improving maximum deformation by 22.21% and increasing minimum natural frequency by 3.18%. More notably, a 48.86% weight loss using CFRP and aluminum hybrid designs, with first-order natural frequency rising to 32.03 Hz. These structural and dynamic improvements directly address the market's critical dual requirement—enhancing crash safety and thermal runaway protection while reducing pack mass to extend EV range.

Our in-depth analysis of the automotive carbon fiber composites includes the following segments:

|

Segment |

Subsegments |

|

Fiber Type |

|

|

Resin Type |

|

|

Application |

|

|

Vehicle Type |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Automotive Carbon Fiber Composites Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the automotive carbon fiber composites market and is projected to hold the regional revenue share of 49.5% by the end of 2035. The region is driven by the convergence of dominant fiber producers in Japan and South Korea, rapidly expanding EV production in China, and cost-competitive manufacturing bases in India and Southeast Asia. The region benefits from vertically integrated supply chains, with precursor chemicals, carbonization lines, and component molding often co-located within national borders. Market dynamics are shaped by aggressive government EV mandates, particularly in China and India, alongside Japan's focus on lightweighting for fuel efficiency. Thermoplastic composites are gaining traction alongside traditional thermosets, enabled by regional expertise in injection molding.

The vehicle electrification, domestic manufacturing, and advanced mobility programs expand is driving the market in India. Lightweight materials are increasingly important for improving vehicle efficiency and supporting the country’s transition toward cleaner transportation. According to the Teriin September 2025 data, India recorded more than 1.95 million electric vehicle registrations, reflecting strong growth in EV adoption and creating demand for lightweight vehicle components. In addition, the PIB August 2025 data depicted that the government approved ₹10,900 crore under the PM E-DRIVE scheme to accelerate electric mobility deployment and supporting infrastructure. These government-backed initiatives are encouraging automakers and component manufacturers to evaluate advanced composite materials, including carbon fiber-based solutions, for future vehicle platforms and efficiency-focused designs.

New-energy vehicle (NEV) deployment and advanced manufacturing upgrades is driving the automotive carbon fiber composites market in China. Lightweight materials are increasingly being incorporated into vehicle development to improve efficiency and support electrification targets. According to the People’s Republic of China January 2025 data, the country produced 12.89 million new-energy vehicles in 2024, representing a year-on-year increase of approximately 35.5%, highlighting the growing scale of vehicle manufacturing that can benefit from advanced composite materials. Additionally, the Ministry of Finance support vehicle trade-in and equipment renewal programs, stimulating demand for newer and more efficient vehicles. These initiatives are encouraging automakers to invest in lightweight material solutions, including carbon fiber composites, for future mobility platforms.

North America Market Insights

The North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the market. The region is driven by the strong synergy between U.S. lightweighting regulations and Canadian clean-energy incentives, fostering a collaborative cross-border supply chain. The region benefits from established automotive hubs in Michigan, Ontario, and Ohio, enabling close OEM-supplier co-development of structural components. Market dynamics are driven by the shift from luxury/exotic applications to high-volume electric pickup trucks and SUVs, demanding rapid-cure manufacturing processes and large-tow fiber adoption. Recycling and circularity are emerging as competitive differentiators, with both nations investing in pyrolysis and solvolysis pilot facilities.

The federal investments in vehicle electrification, domestic manufacturing, and transportation modernization is shaping the automotive carbon fiber composites market in the U.S. Demand is increasing as automakers seek lightweight materials to improve vehicle efficiency, extend electric driving range, and support next-generation vehicle platforms. A key catalyst is the DOE February 2022 data, which provides USD 5 billion to support nationwide EV charging deployment, accelerating production of electric vehicles that increasingly utilize lightweight composite components. In addition, the U.S. Drive Electric 2022-2023 data reported that battery-electric vehicles accounted for 9.8% of new light-duty vehicle sales, up from earlier years, reinforcing the need for weight-reduction strategies. These developments are encouraging OEMs and suppliers to expand investments in advanced composite materials, including carbon fiber-based structural and exterior applications.

The expanding as government policies encourage zero-emission vehicle (ZEV) adoption and advanced manufacturing investments is driving the market in Canada. Lightweight composite materials are increasingly being evaluated by automakers to improve vehicle efficiency and support electrified transportation goals. According to the Government of Canada September 2025 data, zero-emission vehicles represented 15.4% of all new light-duty vehicle registrations, reflecting continued growth in the EV fleet and increasing demand for lightweight vehicle structures. Additionally, C.D.Howe April 2025, the federal government committed up to CAD 2.4 billion to support the electric vehicle supply chain through the Strategic Innovation Fund, strengthening domestic automotive manufacturing capabilities. These initiatives are encouraging greater use of advanced composites in vehicle design, production, and next-generation mobility platforms across Canada.

Europe Market Insights

The Europe automotive carbon fiber composites market is defined by stringent CO₂ emission regulations, a strong premium automotive heritage, and aggressive circular economy mandates that drive innovation in recyclable thermoset and thermoplastic systems. The region benefits from deep collaboration between German OEMs (BMW, Mercedes, VW) and specialized composite suppliers like SGL Carbon, fostering co-development of lightweight body-in-white and battery protection structures. Market dynamics are shaped by the EU's End-of-Life Vehicle (ELV) directive, pushing manufacturers toward bio-based precursors and pyrolysis recovery solutions. Southern Europe contributes through motorsports expertise, while Nordic countries focus on sustainable manufacturing using renewable energy.

The vehicle electrification, industrial modernization, and low-emission mobility is driving the automotive carbon fiber composites market in Germany. Lightweight materials are increasingly important for improving energy efficiency and extending electric vehicle range, particularly among premium vehicle manufacturers. According to the European Commission January 2025 data, 380,609 battery-electric passenger cars were newly registered in 2024, demonstrating continued demand for advanced vehicle technologies. In addition, the Federal Ministry for Economic Affairs and Energy (BMWK) launched the Climate and Transformation Fund (KTF), supporting decarbonization, clean mobility, and industrial innovation initiatives. These developments are encouraging OEMs and suppliers to expand the use of high-performance composite materials, including carbon fiber composites, across structural, exterior, and lightweight vehicle applications.

The market in the UK is advancing as manufacturers focus on lightweight vehicle design, electrification, and domestic innovation in advanced materials. Demand is supported by government-backed programs that promote zero-emission mobility and industrial competitiveness. According to the Transport and Environment July 2025 data, there were 1.4 million licensed battery-electric cars on UK roads, reflecting the growing importance of lightweight materials for vehicle efficiency and range optimization. Additionally, the Advanced Propulsion Centre UK (APC) announced billion joint government-industry commitment to support automotive transformation and net-zero vehicle technologies. These initiatives are encouraging OEMs and suppliers to increase investment in carbon fiber composite solutions for structural, exterior, and performance-focused vehicle applications across the UK automotive sector.

Key Automotive Carbon Fiber Composites Market Players:

- Toray Industries (Japan)

- Teijin Limited (Japan)

- Mitsubishi Chemical Group (Japan)

- SGL Carbon (Germany)

- Hexcel Corporation (U.S.)

- Hyosung Advanced Materials (South Korea)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Toray Industries commands a dominant share in the market through its vertically integrated value chain, from PAN-based precursor fibers to finished structural parts.

- Teijin Limited leverages its Tenax® brand and thermoplastic-based composites to differentiate itself in the market, focusing on lightweight solutions for electric vehicle structural doors and seat frames.

- Mitsubishi Chemical Group (MCG) positions itself as a full-solution provider in the automotive carbon fiber composites market, offering both PAN-based and pitch-based fibers alongside proprietary Kyron™ prepregs for crash-sensitive automotive structures.

- SGL Carbon stands as Europe’s largest independent player in the market, renowned for its BMW i-series and 7-series carbon core bodies produced via its joint venture in Moses Lake, USA.

- Hexcel Corporation is a U.S. powerhouse in the market, leveraging its aerospace-grade heritage to deliver high-performance HexPly® prepregs and dry fabrics for supercar and hypercar applications (e.g., Ferrari, McLaren).

Here is a list of key players operating in the global market:

The global automotive carbon fiber composites market remains highly concentrated, with Toray, Teijin, Mitsubishi, and SGL leading in capacity and OEM supply contracts. Intense competition centers on cost reduction through large-tow fibers, automated layup, and rapid-cure resins. Key strategic initiatives include joint ventures with automakers, vertical integration into recycling, and capacity expansions in the U.S. and Europe to counter logistics costs. Asian players leverage low-cost PAN precursors, while Western firms emphasize lightweighting for EVs. Sustainability is emerging as a differentiator, with several players investing in bio-based or pyrolytic-recovered fibers.

Corporate Landscape of the Market:

Recent Developments

- In March 2026, Teijin Carbon announced that it has expanded the Tenax Next™ product line with sustainable and new industrial material solutions. Tenax Next™ products are next-generation carbon fiber materials based on circular feedstocks, which deliver an audited 36% CO₂ reduction.

- In October 2025, Hyundai Motor Group and Toray Industries, Inc. (Toray Group) signed a Strategic Joint Development Agreement to collaborate on advanced materials and components innovation, aiming to set new standards in future mobility.

- In March 2024, the Mitsubishi Chemical Group announced that it has developed a carbon fiber prepreg material using plant-derived resin. They are expanding BiOpreg portfolio and are adding the BiOpreg #400 series that contains glass fiber prepreg as well as carbon fiber prepreg.

- Report ID: 8626

- Published Date: Jun 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.