Atherectomy Devices Market Outlook:

Atherectomy Devices Market size was valued at USD 1.1 billion in 2025 and is projected to exceed USD 2.5 billion by the end of 2035, expanding at over 8.5% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of atherectomy devices is assessed at USD 1.2 billion.

The atherectomy devices market is supported by the growing clinical and economic burden of peripheral artery disease (PAD), coronary artery disease, diabetes, and age-related vascular conditions. According to the U.S. Centers for Disease Control and Prevention May 2024 data, approximately 6.5 million people aged 40 years and older in the U.S. are living with PAD, a condition associated with reduced blood flow to the limbs and a higher risk of cardiovascular complications. The NLM September 2024 study also reports that heart disease remains the leading cause of death in the U.S., accounting for more than 700,000 deaths annually. As healthcare systems continue to prioritize earlier diagnosis and treatment of vascular disease, hospitals and ambulatory care centers are increasing their use of minimally invasive endovascular procedures to reduce hospitalization time and improve patient outcomes.

Demand is also supported by the rising prevalence of diabetes, a major risk factor for lower-extremity arterial disease. The NLM 2024 study estimates that approximately 589 million adults worldwide were living with diabetes in 2024, creating a substantial patient pool vulnerable to vascular complications requiring interventional treatment. These disease trends continue to influence procurement decisions, capital equipment investments, and physician adoption across cardiovascular and peripheral vascular treatment settings. Across developed and emerging healthcare systems, increasing patient volumes, aging populations, rising diabetes prevalence, and sustained investments in cardiovascular care infrastructure are expected to maintain demand for atherectomy-related procedures and associated capital equipment over the long term.

Key Atherectomy Devices Market Insights Summary:

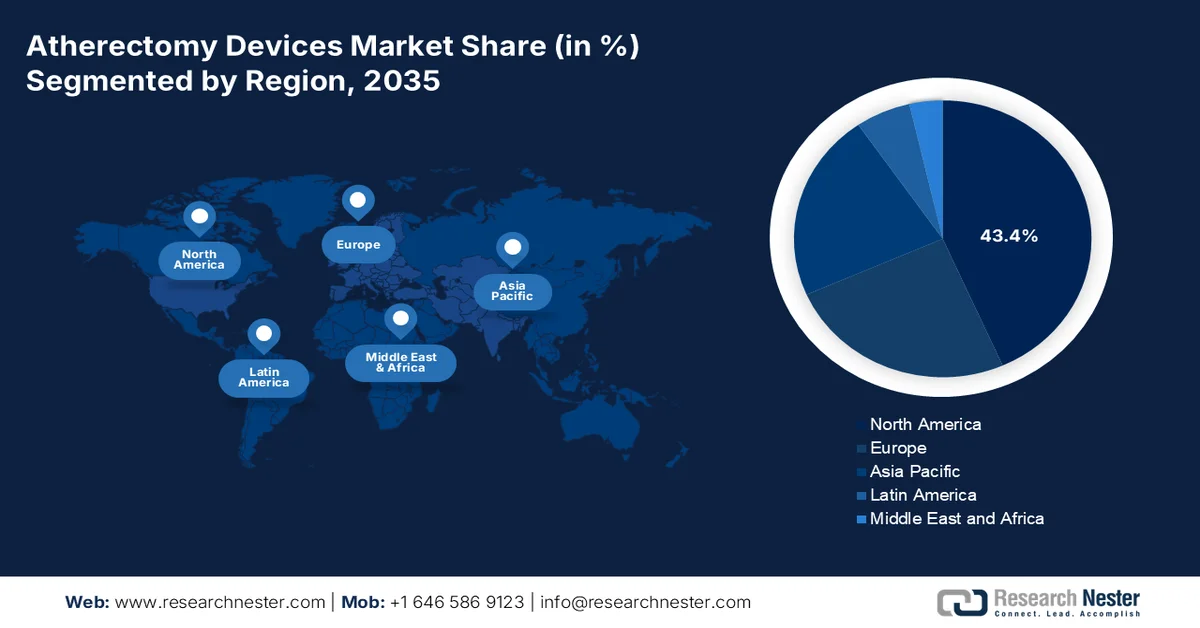

Regional Insights:

- The atherectomy devices market in North America is forecast to secure 43.4% of regional revenue by 2035, bolstered by high procedure volumes, supportive reimbursement structures, expanding outpatient coverage, and a robust ambulatory surgical center ecosystem

- Asia Pacific is expected to witness the fastest expansion during 2026–2035, catalyzed by rising diabetes prevalence, growing vascular screening initiatives, increasing adoption of advanced atherectomy technologies, and expanding access to minimally invasive vascular care

Segment Insights:

- By 2035, the directional atherectomy devices segment is anticipated to account for 38.8% of the atherectomy devices market, reinforced by its capability to reduce plaque volume, limit arterial trauma, and effectively treat lesions in anatomically challenging vessel segments

- The lower extremity PAD segment is projected to retain a leading position across 2026–2035, fueled by the high prevalence of lower-limb peripheral artery disease and the accelerating transition toward endovascular-first treatment approaches

Key Growth Trends:

- Growing diabetes burden

- Aging populations increasing vascular disease incidence

Major Challenges:

- Stringent regulatory approval processes

- High cost of clinical trials

Key Players: Boston Scientific, BD, Cardiovascular Systems Inc., Ra Medical Systems, Avinger Inc., Straub Medical AG, Rex Medical.

Global Atherectomy Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.1 billion

- 2026 Market Size: USD 1.2 billion

- Projected Market Size: USD 2.5 billion by 2035

- Growth Forecasts: 8.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (43.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, Germany, China, Canada

- Emerging Countries: India, Indonesia, Malaysia, South Korea, Australia

Last updated on : 15 June, 2026

Atherectomy Devices Market - Growth Drivers and Challenges

Growth Drivers

- Growing diabetes burden: Diabetes remains one of the strongest predictors of peripheral vascular disease and lower-limb ischemia, directly influencing atherectomy procedure demand. The CDC January 2026 data indicate that more than 40.1 million people have diabetes. Governments are allocating substantial budgets toward diabetes prevention, screening, and complication management programs because vascular complications significantly increase healthcare costs. Public health agencies increasingly emphasize preventing diabetic foot ulcers and amputations, which often require vascular intervention. As diabetic patients frequently develop calcified arterial lesions that are difficult to treat with conventional balloon angioplasty alone, healthcare providers are increasingly incorporating vessel-preparation technologies into treatment strategies. The expanding diabetic population therefore supports long-term growth in peripheral intervention procedures and associated atherectomy device utilization.

- Aging populations increasing vascular disease incidence: Population aging is a structural demand driver because vascular disease prevalence rises significantly among older adults. The World Health Organization October 2025 data estimates that by 2030, one in six people globally will be aged 60 years or older, while the population in this age group will reach approximately 1.4 billion. Older adults experience higher rates of atherosclerosis, calcified arterial lesions, coronary disease, and PAD, creating greater demand for minimally invasive vascular procedures. Governments are expanding healthcare budgets to address age-related chronic diseases and maintain quality of life among elderly populations. This trend supports increased utilization of atherectomy technologies in complex lesion management and contributes to higher procurement of vascular intervention equipment.

Challenges

- Stringent regulatory approval processes: Obtaining FDA or CE mark approval for atherectomy devices is time-consuming, requiring extensive clinical trials for safety and efficacy. The average time from submission to clearance is months, delaying market entry. Though the atherectomy devices market is expected to grow despite government pricing constraints and prolonged regulatory reviews.

- High cost of clinical trials: Randomized controlled trials comparing atherectomy to balloon angioplasty or stenting require large patient populations and long follow-up periods, often exceeding years. Costs routinely surpass million, a prohibitive barrier for small manufacturers. Though the atherectomy devices market shows a positive phase despite clinical trial expenses rising annually.

Atherectomy Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.5% |

|

Base Year Market Size (2025) |

USD 1.1 billion |

|

Forecast Year Market Size (2035) |

USD 2.5 billion |

|

Regional Scope |

|

Atherectomy Devices Market Segmentation:

Type Segment Analysis

Under the type segment, the directional atherectomy devices are leading and is poised to hold the share value of 38.8% by the end of 2035. Directional atherectomy offers theoretical advantages over other endovascular techniques, including plaque volume reduction, decreased arterial barotrauma, and the ability to treat arterial segments at sites of tension and flexion, such as the superficial femoral artery. According to the NLM October 2024 study, in the U.S. market, six classified devices exist, including excisional, ablative, aspirational, rotational, and directional atherectomy. However, in some regions, the only available option is directional atherectomy with the TurboHawk™ device (Medtronic/Covidien, Plymouth, Minnesota, USA). Clinical trials evaluating device performance remain scarce, with a clear predominance of claudicant patients (75%) and femoropopliteal disease (80%). Combined results show an average primary patency rate at one year of 63.5% , highlighting both the clinical utility and the need for further long-term randomized evidence to solidify directional atherectomy's role in peripheral artery disease treatment.

Application Segment Analysis

Lower extremity PAD is the dominant application for the atherectomy devices market, accounting for nearly half of all procedures due to the high prevalence of femoropopliteal and infrapopliteal calcifications in diabetic and elderly patients. Atherectomy offers a minimally invasive alternative to surgical bypass, preserving future access sites and enabling same-day discharge. The NLM June 2023 study indicates that approximately 8.5 million adults in the U.S. have peripheral artery disease, with the majority affecting the lower extremities. The shift toward endovascular first-line therapy, combined with favorable reimbursement for critical limb ischemia, continues to fuel adoption. Technological advances in orbital, directional, and laser atherectomy systems now allow treatment of long, tortuous segments.

End user Segment Analysis

Ambulatory surgical centers are emerging as the leading end-user sub-segment in the atherectomy devices market due to their operational efficiency and patient-centric care models. Unlike traditional hospital settings, ASCs offer shorter waiting times, reduced infection risks, and same-day discharge for peripheral atherectomy procedures. The shift toward value-based healthcare has accelerated the migration of minimally invasive vascular interventions from inpatient facilities to ASCs. Device manufacturers are responding with portable, single-use atherectomy systems designed specifically for outpatient environments. As physicians gain confidence in performing complex plaque modification outside hospitals, ASCs are becoming the preferred setting for treating lower extremity peripheral artery disease, particularly in non-emergent, elective cases.

Our in-depth analysis of the atherectomy devices market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Modality |

|

|

Application |

|

|

End user |

|

|

Technology Integration |

|

|

Lesion Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Atherectomy Devices Market - Regional Analysis

North America Market Insights

North America is dominating the atherectomy devices market and is expected to hold the regional revenue share of 43.4% by the end of 2035. The region is characterized by high procedure volumes, established reimbursement frameworks, and a well-developed ambulatory surgical center (ASC) infrastructure. The U.S. dominates regional activity, driven by the Centers for Medicare & Medicaid Services expanding outpatient coverage for peripheral atherectomy. Canada operates under a distinct public health model, where provincial tenders and centralized procurement limit device variety but ensure cost predictability. Key market characteristics include a strong preference for disposable, single-use catheters, increasing adoption of imaging-guided atherectomy systems, and physician training programs focused on reducing complication rates. The region continues to serve as a primary launch market for next-generation rotational and orbital atherectomy platforms.

The large cardiovascular patient population, expanding procedural capacity, and strong federal healthcare coverage is shaping the atherectomy devices market in the U.S. According to the KFF June 2026 data, more than 68 million people were enrolled in Medicare in 2024, supporting sustained demand for vascular interventions among older adults who are at higher risk of peripheral and coronary artery disease. In addition, the U.S. Centers for Disease Control and Prevention October 2024 reports that approximately 805,000 people experience a heart attack each year in the United States, highlighting the ongoing burden of atherosclerotic disease that often requires catheter-based treatment. Continued investments in outpatient cardiovascular care, hospital catheterization laboratories, and Medicare-supported vascular procedures are expected to support demand for atherectomy systems across the country.

The rising cardiovascular care demand, an aging population, and continued public healthcare investment in diagnostic and interventional services is driving the atherectomy devices market in Canada. According to Statistics Canada June 2025 data, individuals aged 65 years and older accounted for approximately 19.3% of Canada’s population in 2024, increasing the prevalence of atherosclerotic and peripheral vascular diseases that often require endovascular treatment. Additionally, the Insurance Portal December 2024 data reported that total health spending in Canada was projected to reach USD 370 billion in 2024, equivalent to about USD 9,054 per person, reflecting sustained investment in healthcare infrastructure and specialized cardiovascular services. These trends are encouraging hospitals and cardiac centers to expand minimally invasive vascular treatment capabilities, supporting demand for advanced plaque-modification technologies and related interventional devices across Canada.

APAC Market Insights

The Asia Pacific is projected to emerge as the rapidly during the assessed period, 2026 to 2035 in the atherectomy devices market. The region is highly heterogeneous, with mature markets like Japan and Australia exhibiting advanced adoption of rotational and laser systems, while emerging economies such as India, Indonesia, and Malaysia present volume-driven opportunities constrained by price sensitivity. Japan leads the region due to its high prevalence of severe coronary calcification and fast-track regulatory pathways. China and India are witnessing gradual uptake, driven by expanding diabetes populations and government-funded vascular screening programs. However, fragmented distribution networks, import tariffs, and limited physician training in complex atherectomy techniques remain barriers. Local manufacturing partnerships and portable, low-cost device designs are gaining traction. Australia and South Korea demonstrate steady growth through ambulatory care shifts and value-based reimbursement models.

The increasing burden of cardiovascular diseases, expanding access to interventional cardiology services, and government-supported healthcare investments is driving the atherectomy devices market in India. According to the NLM December 2024 study, more than 410 million Ayushman Bharat Health Accounts had been created, strengthening digital healthcare access and facilitating earlier diagnosis and treatment of chronic vascular conditions. In addition, the PIB August 2025 data reported that over 1.76 lakh Ayushman Arogya Mandirs were operational by 2025, significantly expanding primary healthcare coverage across urban and rural regions. These developments are improving patient referral pathways and access to specialized cardiovascular care, encouraging greater adoption of minimally invasive vascular interventions and supporting demand for atherectomy devices in India's growing healthcare sector.

The increasing adoption of advanced plaque-modification techniques in complex coronary interventions is driving the atherectomy devices market in China. The Frontiers October 2025 study of 75 CTO-PCI patients demonstrated that rotational atherectomy achieved a 90% procedural success rate, while excimer laser coronary atherectomy achieved 84% success, highlighting strong clinical acceptance of both technologies in challenging lesions. The study also found that rotational atherectomy was used in 76% of moderate-to-severe calcified lesions, whereas laser atherectomy was preferred for in-stent restenosis CTO cases and longer lesions. With comparable midterm safety outcomes and growing expertise in complex PCI procedures, Chinese hospitals are increasingly integrating specialized atherectomy technologies into cardiovascular treatment pathways, supporting atherectomy devices market expansion.

Europe Market Insights

The divergent national health systems, varying reimbursement policies, and a steady shift from inpatient to outpatient vascular procedures is driving the atherectomy devices market in Europe. Germany, France, and the UK lead regional adoption, driven by DRG reforms favoring ambulatory care and national amputation reduction initiatives. Southern and Eastern European countries exhibit slower uptake due to budget constraints and limited access to advanced rotational or laser systems. The market is characterized by strong preference for directional and laser atherectomy platforms, particularly for femoropopliteal disease. Physician training requirements, device cost sensitivity, and tenders through public procurement frameworks influence supplier strategies. The Nordics emphasize real-world evidence generation, while Russia and Eastern Europe rely on imported devices with limited local service support.

The Germany atherectomy devices market benefits from the country’s strong healthcare infrastructure and leading position in the European medical technology industry. Germany represents approximately 26.5% of the European medical device market, generating around USD 44 billion in annual medical device revenue, according to ITA August 2025 data. The healthcare sector contributes roughly 12.8% of Germany’s GDP, with an economic footprint of approximately USD 838 billion, supporting continuous investment in advanced cardiovascular treatment technologies. Additionally, ongoing healthcare reforms, hospital modernization initiatives, and growing demand for minimally invasive vascular procedures are encouraging hospitals and cardiac centers to adopt specialized plaque-modification devices, supporting continued market growth.

The growing need to treat complex calcified coronary lesions through advanced interventional cardiology procedures is shaping the atherectomy devices market in the UK. According to NLM October 2024 study, approximately 20% of coronary lesions treated with PCI in Europe are severely calcified, creating a substantial demand for plaque-modification technologies. The same study reported that rotational atherectomy was used in 3.1% of PCI procedures in the UK as of 2015, representing the highest adoption rate among European countries, where utilization ranged from 0.8% to 3.1%. Increasing clinical expertise, expanding treatment of complex coronary artery disease, and continued use of specialized rotational atherectomy systems in catheterization laboratories are supporting market growth across the United Kingdom.

Key Atherectomy devices Market Players:

- Boston Scientific (U.S.)

- BD (U.S.)

- Cardiovascular Systems Inc. (U.S.)

- Ra Medical Systems (U.S.)

- Avinger Inc. (U.S.)

- Straub Medical AG (Switzerland)

- Rex Medical (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- The atherectomy devices market is highly consolidated, led by North America firms due to advanced R&D and high procedural volumes. Key players focus on strategic initiatives such as product innovation, geographic expansion into Asia-Pacific, and regulatory approvals. Mergers and acquisitions are common to enhance portfolio diversification and distribution networks. For example, in March 2024 Zylox-Tonbridge announced a new strategic partnership with Avinger. Europe and Japan companies compete through precision engineering and cost-effective solutions, while emerging players from India and South Korea target niche segments. Intense rivalry drives technological integration, including image-guided devices and disposable catheters for peripheral and coronary applications.

- Boston Scientific competes aggressively in the atherectomy devices market with its Rotablator™ rotational atherectomy system, a gold standard for coronary calcium modification. Strategic initiatives include developing next-generation low-profile catheters, expanding into peripheral atherectomy, and combining atherectomy with lithotripsy technologies.

- BD operates in the atherectomy devices market primarily through its peripheral intervention division, offering rotational and aspiration-based atherectomy solutions. The company’s strategy emphasizes single-use, disposable catheters designed for ambulatory and office-based labs. In 2025, the company has made a revenue of USD 21.8 billion.

Here is a list of key players operating in the global atherectomy devices market:

Corporate Landscape of the Market:

Recent Developments

- In May 2026, Johnson & Johnson announced the launch of its Shockwave C2 Aero Coronary IVL Catheter which is designed for enhanced lesion crossing, improved deliverability, and new repositioning capabilities for the treatment of calcified coronary artery disease (CAD).

- In November 2024, Royal Philips announced the enrollment of the first patient in the U.S. THOR IDE clinical trial based on an innovative combined laser atherectomy and intravascular lithotripsy catheter developed by Philips, which integrates two critical PAD treatments into a single device.

- In January 2024, AngioDynamics, Inc. announced that the U.S. Food and Drug Administration (FDA) had granted clearance for Auryon XL Catheter, a 225-cm radial access catheter, for use with the Auryon Atherectomy System in the treatment of Peripheral Arterial Disease (PAD).

- Report ID: 8102

- Published Date: Jun 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.