Artificial Pancreas Device Systems Market Outlook:

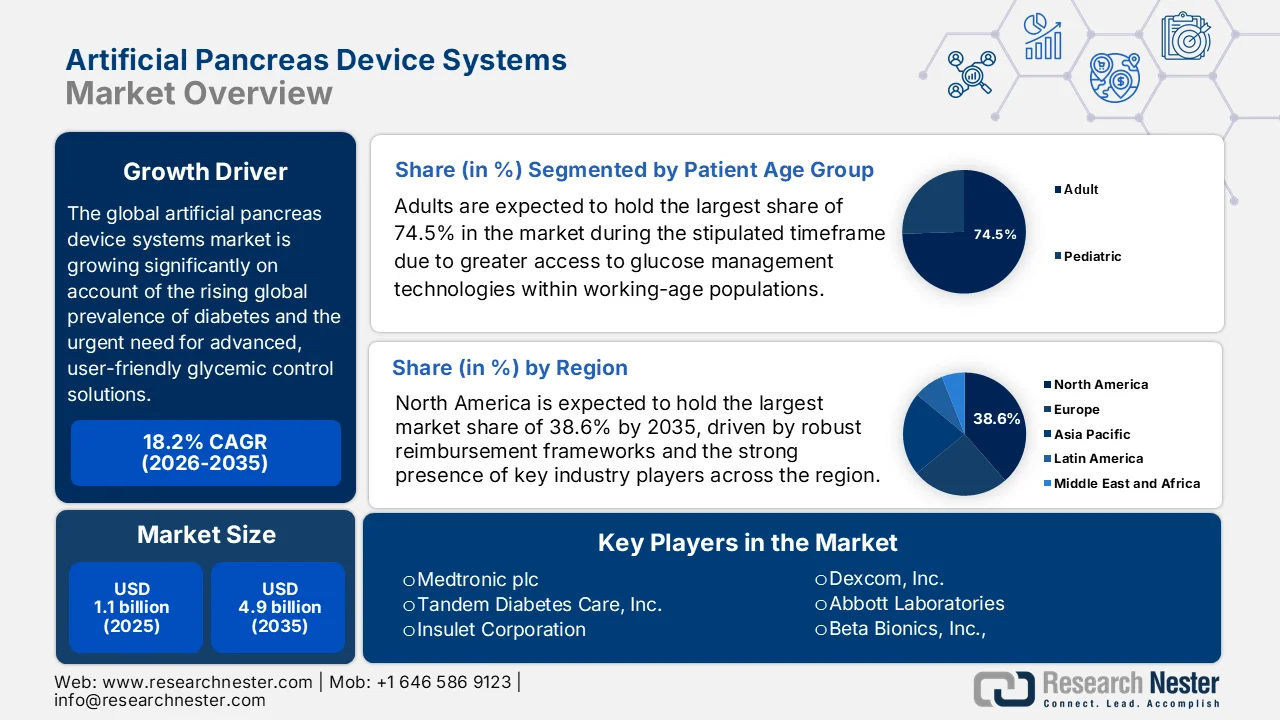

Artificial Pancreas Device Systems Market size was valued at USD 1.1 billion in 2025 and is forecasted to expand to USD 4.9 billion by 2035, progressing at a CAGR of 18.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of artificial pancreas device systems is estimated at USD 1.3 billion.

The artificial pancreas device systems market is poised for solid growth, effectively fueled by the rising global prevalence of diabetes and the urgent need for advanced, user-friendly glycemic control solutions. According to a World Health Organization article published in November 2024, the global diabetes patient pool expanded from 200 million in three decades ago to 830 million in 2022, wherein the prevalence reached 14% among adults aged 18 and above. Growth is disproportionately concentrated in low- and middle-income countries, where treatment access remains limited, with 59% of adults aged 30+ not receiving medication in 2022. More than 95% of cases are attributed to type 2 diabetes, while approximately 9 million individuals were living with type 1 diabetes as of the latest available estimates, thus denoting a huge necessity for an artificial pancreas device system.

Furthermore, the artificial pancreas device systems market is witnessing growth due to proven efficacy and a structural shift towards automated and hybrid closed-loop systems that integrate continuous glucose monitoring with insulin delivery pumps to minimize hypoglycemia risks. In this context, the article published by the National Institute of Health (NIH) in March 2023 stated that a study evaluated 102 children aged 2 to 5 with type 1 diabetes, where 68 received an artificial pancreas system, and 34 remained on standard care. Besides, the article notes that children using the system improved time-in-range blood glucose levels from 55% at baseline to nearly 70% after 13 weeks, whereas the control group showed no significant change. This resulted in approximately three additional hours per day of optimal glucose control, with the most pronounced improvements observed during nighttime management. Therefore, improved clinical outcomes and safer glucose control in young patients are likely to increase adoption and payer support, thus driving market growth.

Key Artificial Pancreas Device Systems Market Insights Summary:

Regional Highlights:

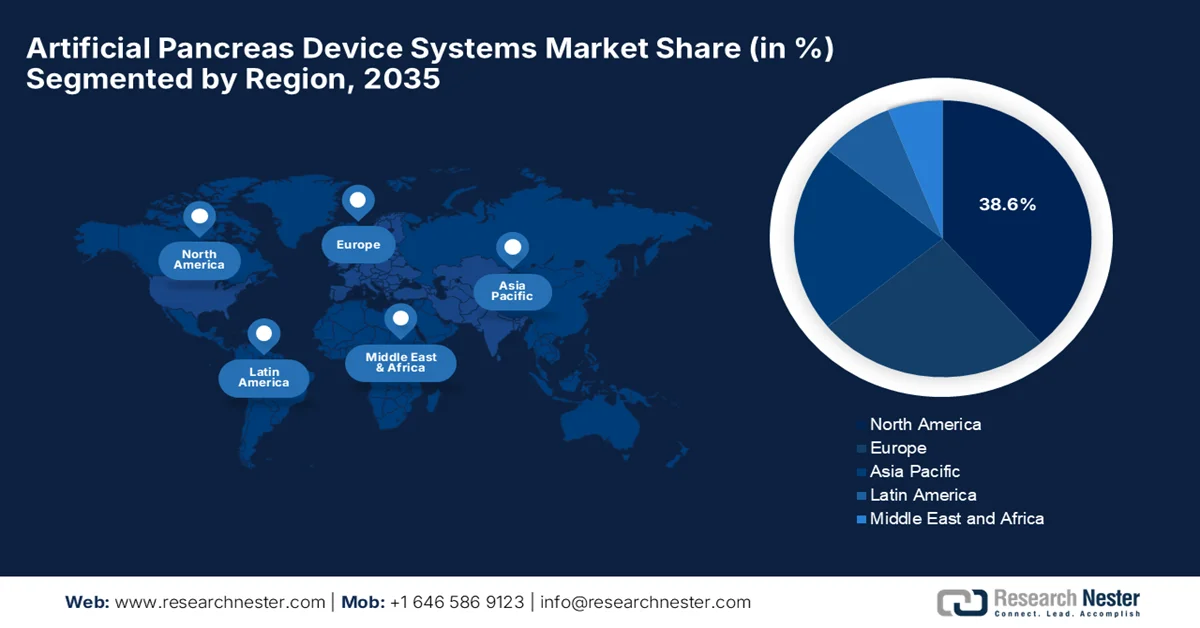

- By 2035, North America in the artificial pancreas device systems market is projected to command a leading 38.6% share, attributed to strong reimbursement systems, early adoption of closed-loop technologies, and the presence of leading players

- The Asia Pacific region is poised to register the fastest growth in the artificial pancreas device systems market during 2026–2035, impelled by growing health consciousness, substantial investments in healthcare infrastructure, and rising disposable income

Segment Insights:

- By 2035, the adults segment in the artificial pancreas device systems market is projected to account for a dominant 74.5% share, propelled by higher prevalence of insulin-dependent diabetes and greater access to advanced glucose management technologies within working-age populations

- By 2035, the hybrid closed-loop platforms segment is anticipated to witness notable expansion, fueled by their ability to balance automation with clinician oversight, ensuring safer insulin delivery in complex glycemic conditions

Key Growth Trends:

- Need for improved glycemic control

- Technological advancements in diabetes management devices

Major Challenges:

- High cost and limited reimbursement

- Limited awareness and adoption in emerging markets

Key Players: Medtronic plc, Tandem Diabetes Care Inc., Insulet Corporation, Dexcom Inc., Abbott Laboratories, Beta Bionics Inc., Bigfoot Biomedical Inc., Johnson & Johnson, Technion - Israel Institute of Technology, Eli Lilly and Company, Senseonics Holdings Inc., Roche Diabetes Care, Diabeloop S.A., Ypsomed AG, Cellnovo Group, Inreda Diabetic B.V., Defymed SAS, Pancreum Inc., EoFlow Co. Ltd., Medtrum Technologies Inc., F. Hoffmann-La Roche Ltd.

Global Artificial Pancreas Device Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size:USD 1.1 billion

- 2026 Market Size: USD 1.3 billion

- Projected Market Size: USD 4.9 billion by 2035

- Growth Forecasts: 18.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, United Kingdom, Canada

- Emerging Countries: China, India, South Korea, Australia, Singapore

Last updated on : 23 April, 2026

Artificial Pancreas Device Systems Market - Growth Drivers and Challenges

Growth Drivers

- Need for improved glycemic control: The artificial pancreas device systems are being opted for due to their stronger capability to maintain stable blood glucose levels and reduce the risk of hypoglycemia and hyperglycemia. This aspect improves long-term health outcomes and reduces complications such as neuropathy, kidney disease, and cardiovascular issues. In September 2022, a clinical trial, which was funded by the NIH, found that the bionic pancreas remarkably improved blood glucose control in people with type 1 diabetes when compared to standard insulin delivery methods. In addition, the article notes that this device readily automates insulin dosing with minimal user input, thereby eliminating carb counting and frequent adjustments, and improving HbA1c and time-in-range. Hence, these results underscore its potential to ease daily management, reduce complications, and thus benefit the overall artificial pancreas device systems market.

- Technological advancements in diabetes management devices: The global artificial pancreas device systems market is witnessing advancements in terms of continuous glucose monitoring, insulin pump technology, and AI-based control algorithms, which are significantly driving market growth. In April 2023, Medtronic announced that the U.S. Food & Drug Administration (FDA) had approved the MiniMed 780G system, which is the first insulin pump with meal detection technology that delivers automatic corrections every five minutes. The system consists of a Guardian™ 4 sensor with no fingersticks, and it helps users manage mealtime challenges by adapting insulin delivery in real time. Therefore, such consistent innovations from the leading players denote a clear shift toward fully automated, AI-enabled diabetes management systems that enhance real-time glucose control and reduce patient intervention.

- Increasing demand for home-based and wearable solutions: There is a strong shift toward home-based and wearable medical devices that enable patients to manage chronic conditions outside clinical settings. Artificial pancreas systems support remote monitoring and automated insulin delivery, reducing the need for frequent hospital visits, thus driving surging adoption rates in the artificial pancreas device systems market. In November 2023, the article published by the Organization for Economic Co-operation and Development (OECD) stated that there is a rising diabetes prevalence, which is projected to reach 783 million by 2045, creating sustained and growing demand for long-term care. It emphasizes diabetes as a condition largely managed through home care and notes that most hospital admissions are avoidable with effective primary and home-based management. Overall, the study states that diabetes care as patient-centered system, increasingly dependent on home-based monitoring and continuous outpatient support.

Challenges

- High cost and limited reimbursement: One of the biggest barriers hindering adoption in the artificial pancreas device systems market is the upfront and ongoing costs, including insulin pumps, continuous glucose monitors, sensors, and software subscriptions. In most of the regions, reimbursement policies are considered to be inconsistent or limited, especially in terms of emerging nations. Even in the case of developed regions, coverage criteria can cause restricted access to only specific patient groups, such as type 1 diabetes patients. This financial burden reduces accessibility and slows market penetration. Therefore, manufacturers in this sector need to continuously demonstrate cost-effectiveness through clinical outcomes and real-world data to convince insurers and governments to expand reimbursement frameworks and improve affordability.

- Limited awareness and adoption in emerging markets: The awareness regarding artificial pancreas systems is identified to be low in most of the developing regions, wherein diabetes management still depends heavily on traditional methods such as manual insulin injections. Also, the lack of trained healthcare professionals, limited patient education, and inadequate healthcare infrastructure hinder adoption in the artificial pancreas device systems market. At the same time, cultural factors and resistance to wearable medical devices play a role. In countries such as India, a large diabetic population exists, but penetration of advanced automated insulin delivery systems is still minimal. In this context, companies need to make heavy investments in education campaigns, physician training, and localized strategies to increase acceptance and expand their presence in high-growth but underserved markets.

Artificial Pancreas Device Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.2% |

|

Base Year Market Size (2025) |

USD 1.1 billion |

|

Forecast Year Market Size (2035) |

USD 4.9 billion |

|

Regional Scope |

|

Artificial Pancreas Device Systems Market Segmentation:

Patient Age Group Segment Analysis

In the patient age group segment, adults are expected to hold the largest share of 74.5% in the artificial pancreas device systems market during the stipulated timeframe. The segment’s dominance is largely propelled by higher prevalence of insulin-dependent diabetes and greater access to advanced glucose management technologies within working-age populations. As per the article published by NIH in March 2025 U.S. national data on adults with diabetes in a span of a decade show mixed quality-of-care outcomes: in adults, A1C control (<8.0%) improved from 71.1% to 75.6%, while blood pressure control (<140/90 mmHg) rose from 65.7% to 71.5%, indicating gradual but plateauing improvements in risk factor management. Besides, in adults, diabetes-related hospitalizations are a major concern, wherein hypoglycemia occurs in 0.08 to 0.57 cases per 100 people, highlighting the urgent need for efficacious solutions such as artificial pancreas devices.

Device Type Segment Analysis

In terms of the device type segment, the hybrid closed-loop platforms are anticipated to grow at a considerable rate in the artificial pancreas device systems market by the end of 2035. The growth of the segment is largely driven by their ability to balance automation with clinician oversight, ensuring safer insulin delivery in complex glycemic conditions. In May 2023, the U.S. FDA cleared the iLet Bionic Pancreas system, which combines the iLet ACE Pump, iLet dosing decision software, and a compatible iCGM to automate insulin delivery for people aged six and older with type 1 diabetes. The system’s adaptive algorithm eliminates manual pump adjustments and simplifies mealtime dosing with a meal announcement feature by using only body weight for initialization. Therefore, such a supportive regulatory environment expands access to next-generation AID technology and eases the daily burden of diabetes management.

Component Segment Analysis

By the conclusion of 2035, the insulin pumps segment is predicted to hold a significant share in the artificial pancreas device systems market over the forecasted years. Their established role as the primary insulin delivery hardware integrated into automated diabetes systems is the main factor behind the subtype’s leadership. Growth is supported by miniaturization of pump devices, improved patch-based designs, and enhanced connectivity with digital health platforms, thereby enabling real-time dosing adjustments. In May 2024, the Medtronic MiniMed 780G automated insulin delivery system was recognized by Fast Company in its World Changing Ideas Awards for advancing diabetes care through automated insulin adjustment and meal detection technology. The company notes that this system continuously corrects glucose levels every five minutes, reducing manual intervention and helping improve long-term glycemic stability in real-world diabetes management, thus denoting a positive outlook for the segment’s growth and exposure.

Our in-depth analysis of the artificial pancreas device systems market includes the following segments:

|

Segment |

Subsegments |

|

Patient Age Group |

|

|

Device Type |

|

|

Component |

|

|

End user |

|

|

Technology |

|

|

Treatment Type |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Artificial Pancreas Device Systems Market - Regional Analysis

North America Market Insights

By the end of 2035, the North America artificial pancreas device systems market is anticipated to lead with the largest share of 38.6%. The region’s dominance in this field is majorly fueled by strong reimbursement systems, early adoption of closed-loop technologies, and the presence of leading players. Over the forecasted years, growth will remain robust due to continuous innovation and high patient awareness. As per the official press release by Breakthrough T1D in January 2022, the U.S. FDA authorized the Insulet Omnipod 5, which is the first tubeless, wearable artificial pancreas system for people aged six and older, integrating directly with the Dexcom G6 CGM. Besides, clinical trials showed significant improvements: adults gained 2.2 extra hours in range daily with HbA1c dropping from 7.16% to 6.78%, whereas children gained 3.7 hours in range with HbA1c reduced from 7.67% to 6.99%. This is deliberately supported by breakthrough T1D’s long-term research investment, hence suitable for bolstering the region’s artificial pancreas device systems market growth.

The integration of AI-driven, personalized algorithms, a shift towards user-friendly, wearable, and connected patch pumps, is propelling the artificial pancreas device systems market in the U.S. The country’s market also benefits from a large and technologically savvy user base, along with supportive U.S. FDA approval pathways that aim to minimize the need for manual meal announcements. In January 2022, the American Diabetes Association and the Patient Advocate Foundation launched a new co-pay relief fund to provide financial assistance for people living with diabetes. This particular program helps eligible patients cover co-pays, deductibles, co-insurance, and even insurance premiums, easing the burden of high out-of-pocket costs. The report highlighted that diabetes accounts for USD 1 of every USD 4 spent on U.S. healthcare, and annual expenses average USD 9,600 more than for those without the condition, whereas the fund offers critical support.

The artificial pancreas device systems market in Canada is growing exponentially, owing to the expanding reimbursement policies and a growing preference for home-based, less-invasive technologies. The sector is witnessing intense innovation, wherein major players are introducing advanced hybrid closed-loop systems, leading to a significant shift from manual, semi-automated insulin delivery to fully automated regulation. In November 2024, Health Canada approved the mylife YpsoPump insulin pump and CamAPS FX hybrid closed-loop algorithm. Together with the Dexcom G6 CGM, these technologies form the mylife Loop, which is an automated insulin delivery system especially designed to simplify therapy and improve glucose control for residents of Canada who are living with type 1 diabetes. Hence, with such regulatory support, the country will witness strong growth in the next decade.

APAC Market Insights

The Asia Pacific artificial pancreas device systems market is expected to grow at the fastest rate from 2026 to 2035. The region’s pace of progress in this field is effectively driven by growing health consciousness, substantial investments in healthcare infrastructure, and rising disposable income. The artificial pancreas device systems market is also bolstered by supportive government initiatives, which improve diabetes management, increase awareness of long-term diabetes complications, and technological collaborations aimed at launching user-friendly devices. Based on the government data from Australia in July 2022, the government has invested almost USD 273.1 million over four years to enable all 130,000 people with type 1 diabetes access to subsidized continuous glucose monitoring devices under the National Diabetes Services Scheme in Australia. It mentioned that adults over 21 can now access CGMs at a co-payment of USD 32.50 per month instead of paying up to USD 5,000 annually. The plan expands the insulin pump program, adding 35 fully subsidized pumps annually for disadvantaged young adults aged 18 to 21.

The increased adoption of advanced glycemic management technologies is effectively fueling the artificial pancreas device systems market in China. This market is heavily driven by international leaders, domestic manufacturers who are increasingly innovating, focusing on wearable patch pumps and, notably, the development and adoption of open-source automated insulin delivery systems. As per an article published by NIH in July 2025, a single-center study in China found that a do-it-yourself artificial pancreas system remarkably improved blood glucose control in children with type 1 diabetes. It stated that among 41 participants who were aged 3 to 18, time in range rose from 72.4% to 80.8%, fasting glucose dropped from 8.2 to 6.7 mmol/L, and HbA1c decreased from 6.6% to 6.3%. Importantly, no cases of diabetic ketoacidosis, severe hypoglycemia, or other adverse events occurred, thereby confirming DIYAPS as a safe and effective option for pediatric diabetes management.

The urgent need to manage the massive, growing burden of diabetes is prompting a profitable business environment for pioneers in the artificial pancreas device systems market in India. The fundamental growth drivers propelling the country’s market are rapid urbanization, increasing awareness of advanced diabetes technology among healthcare providers, and the push for home-based connected care models. In August 2025, Abbott announced the launch of FreeStyle Libre® 2 Plus in the country to offer continuous glucose readings every minute with optional real-time alarms sent directly to smartphones. This innovation provides a crucial tool for proactive management and prevention of complications, whereas the clinical studies show Libre technology reduces hypoglycemia episodes by up to 43%, lowers HbA1c by 0.9% to 1.5%, and cuts hospital visits by 66%, thus denoting a lucrative opportunity for the artificial pancreas device systems market to grow.

Europe Market Insights

Well-established healthcare infrastructures, along with supportive government policies for diabetes management and increasing reimbursement coverage, are certain factors that are responsibly uplifting the artificial pancreas device systems market expansion in Europe. The competitive landscape is fueled by intense research and development, wherein the leading regional players are mostly focused on AI-driven algorithms and wearable, user-friendly devices to enhance precision in glucose regulation. In this context, the region funded the FORGETDIABETES project with a total budget of USD 4.2 million that ran from five years until 2025 and was coordinated by the University of Padova has developed a fully implantable bionic pancreas that delivers insulin through the intraperitoneal route, mimicking natural physiology more closely than subcutaneous pumps. This particular system integrates a glucose sensor, adaptive algorithm, and pump with an internal reservoir refilled weekly through oral insulin capsules, thereby reducing the burden of injections.

The heightened demand for innovative, user-friendly technologies, including patch pumps and advanced sensor-augmented systems, is driving the overall artificial pancreas device systems market in Germany. A significant trend towards personalized diabetes management, strong reimbursement support for digital health tools, is strengthening the adoption of these connected care models. Expanding integration of AI-driven insulin dosing algorithms is improving real-time glucose responsiveness and treatment precision in the country’s market. Increasing clinical adoption of interoperable closed-loop systems is enabling smoother data exchange between pumps, sensors, and mobile apps. Rising collaboration between medtech firms and research hospitals is accelerating next-generation device validation and deployment, thus denoting a positive market outlook.

There is a huge opportunity for the artificial pancreas device systems market in the UK to grow in the next decade, owing to increasing patient awareness of technologies that offer improved quality of life and reduced hypoglycemia. A key driver is the active support from the NHS and the implementation of NICE technology appraisal guidelines recommending the rollout of these devices to eligible patients. The industry is seeing intense research and development, which is focused on creating more interoperable and accurate devices. In June 2025, the article published by Open Access Government reported that the NHS in England has rolled out hybrid closed-loop systems, ie, an artificial pancreas, to around 20,000 children and young people with type 1 diabetes. It also mentioned that uptake rose sharply after NICE’s 2023 recommendation, with usage increasing from 36% to 62% in just one year. These systems combine an insulin pump, glucose sensor, and algorithm managed through a smartphone, transforming daily care.

Key Artificial Pancreas Device Systems Market Players:

- Medtronic plc (Ireland)

- Tandem Diabetes Care, Inc. (U.S.)

- Insulet Corporation (U.S.)

- Dexcom, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Beta Bionics, Inc. (U.S.)

- Bigfoot Biomedical, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Technion - Israel Institute of Technology (Israel)

- Eli Lilly and Company (U.S.)

- Senseonics Holdings, Inc. (U.S.)

- Roche Diabetes Care (Switzerland)

- Diabeloop S.A. (France)

- Ypsomed AG (Switzerland)

- Cellnovo Group (UK)

- Inreda Diabetic B.V. (Netherlands)

- Defymed SAS (France)

- Pancreum, Inc. (U.S.)

- EoFlow Co., Ltd. (South Korea)

- Medtrum Technologies Inc. (China)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic plc is the most influential player in this market, positioned by its MiniMed insulin pump portfolio and advanced hybrid closed-loop systems such as the MiniMed 780G. The company is highly focused on interoperability by integrating its devices with third-party CGMs such as Abbott’s sensors.

- Tandem Diabetes Care, Inc. maintains a strong position in this sector through its t: slim X2 insulin pump, which is powered by the Control-IQ algorithm. The firm is best known for its software-driven approach, enabling remote updates and continuous improvement of insulin delivery performance.

- Insulet Corporation is identified as a major force in the artificial pancreas device systems market with its Omnipod tubeless, patch-based insulin delivery system. The company is highly focused on expanding fully disposable and wearable artificial pancreas solutions, which are positioning it as a predominant leader in the artificial pancreas device systems industry.

- Dexcom, Inc. plays a critical enabling role in the artificial pancreas ecosystem as a leading continuous glucose monitoring provider. The firm’s G6 and G7 sensors are widely integrated into automated insulin delivery systems from multiple pump manufacturers, thus making Dexcom a foundational technology partner in the APDS market.

- Abbott Laboratories is another major CGM-driven player that is reshaping the artificial pancreas device systems market industry through its FreeStyle Libre portfolio. The company has expanded from flash glucose monitoring to real-time CGM integration, enabling broader use in automated insulin delivery systems.

Below is the list of some prominent players operating in the global artificial pancreas device systems market:

The artificial pancreas device systems market is an extremely consolidated landscape, which is being dominated by Medtronic, Tandem Diabetes Care, Insulet, Dexcom, and Abbott, which control most commercialized automated insulin delivery ecosystems. These firms are highly focused on integrated CGM-pump-algorithm platforms and frequent software upgrades to strengthen user lock-in. Strategic partnerships are reshaping interoperability standards, whereas emerging players such as Beta Bionics, Diabeloop, and EoFlow are driving continued innovation in fully closed-loop and patch-based systems. Companies across different nations are making heavy investments in AI-based glucose prediction, regulatory fast-track pathways, and clinical evidence to expand reimbursement coverage and accelerate global adoption. In July 2025, Tandem Diabetes Care entered into a partnership with Abbott with a main goal to integrate its insulin delivery systems with Abbott’s upcoming dual glucose-ketone sensor, aiming to help patients detect early ketone rises and prevent diabetic ketoacidosis.

Corporate Landscape of the Artificial Pancreas Device Systems Market:

Recent Developments

- In February 2026, researchers from the Technion - Israel Institute of Technology and major U.S. institutions developed an implantable living pancreas that can sense glucose levels and produce insulin autonomously, potentially eliminating the need for external insulin injections.

- In February 2025, Tandem Diabetes Care announced the U.S. FDA clearance of its Control-IQ+ automated insulin delivery technology for adults with type 2 diabetes, expanding the use of its t: slim X2 pump system beyond type 1 diabetes.

- In July 2024, Tandem Diabetes Care and Dexcom announced that the t: slim X2 insulin pump integrated with Dexcom G7 CGM has received Health Canada authorization, making it the first automated insulin delivery system in Canada compatible with both Dexcom G7 and G6 sensors.

- In April 2024, the National Health Service began a world-first ever rollout of artificial pancreas devices for people with type 1 diabetes, using hybrid closed-loop technology to automatically monitor glucose and deliver insulin. This particular system reduces the need for injections, prevents dangerous highs and lows, and promises better outcomes.

- Report ID: 8527

- Published Date: Apr 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.