Anticholinergic Drugs Market Outlook:

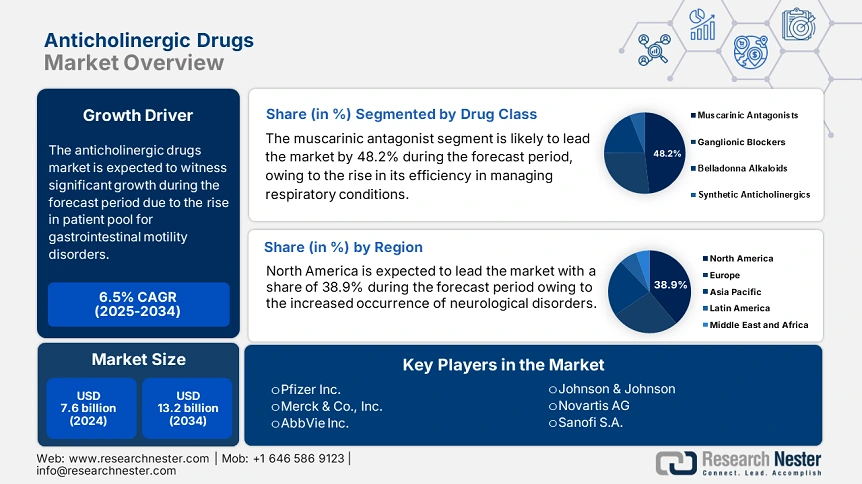

Anticholinergic Drugs Market size was valued at USD 7.6 billion in 2024 and is projected to reach USD 13.2 billion by the end of 2034, rising at a CAGR of 6.5% during the forecast period, i.e., 2025-2034. In 2025, the industry size of anticholinergic drugs is estimated at USD 8.1 billion.

The global patient pool requiring anticholinergic drugs for overactive bladder, gastrointestinal motility disorders, Parkinson’s disease, and COPD is rising rapidly. As per the U.S. Centers for Disease Control and Prevention report, nearly 25.6 million people in the U.S. are affected by urinary incontinence and are urging for antimuscarinic agents for continual treatment. The National Institute on Aging has stated that above 55.4 million people across the globe are affected by dementia, and these people are prescribed anticholinergics. Further, the other major indication is COPD, where 16.5 million people in the U.S. were affected in 2023 with ipratropium bromide and other drugs as the key components for therapeutics. The growing population in both developed and developing nations leads the market dominance.

On the supply chain side, the API synthesis, packaging, formulation, and distribution are key factors. The global manufacturing of API is from the U.S., India, and parts of Europe. The producer price index rose to 3.2% for pharmaceutical preparations in 2024, impacting the cost pressures in chemical synthesis and packaging. On the other hand, the consumer price index increased to 2.1% for prescription drugs. The U.S. International Trade Commission reports that exports of formed goods, especially to Latin America and Southeast Asia, rose by 7.5% in 2023 due to cost-effective U.S. formulations, and imports of anticholinergic-related APIs increased by 11.8% during that same period. Public-private partnerships and strategic stockpiling are the major supply chain resilience in the anticholinergic drugs market.

Anticholinergic Drugs Market - Growth Drivers and Challenges

Growth Drivers

-

Rising cases of chronic diseases: In Germany, the 2025 patient base requiring anticholinergic drug treatment is estimated at 8.6 million, up 17.3% from over the past ten years, primarily due to demographic aging and growing diagnostics. In the U.S., 16.4 million adults have been diagnosed with COPD according to the CDC, with ipratropium and tiotropium as standard-of-care therapies. The expanding patient volume is a key driver for drug volume demand and formulary growth in public and private payers. This anticholinergic drugs market demand has also surged from formulary additions, with Germany's statutory health insurers expanding coverage of anticholinergic drugs to address the demand.

-

Optimizing treatment pathways: As per the AHRQ report, pharmacoeconomic studies establish that generic anticholinergic agents’ lower long-term management costs by 19.4% as opposed to interventions for urinary and gastric conditions. This has led health systems to transition protocols to oral antimuscarinics at earlier stages of the disease, backed by training programs for primary care physicians. These cost savings are especially significant in Medicare and Medicaid programs, where preventive prescribing limits surgical procedures. Further, U.S. state Medicaid programs have updated their formularies in 2024 to favor generics such as oxybutynin and tolterodine as first-line treatments for overactive bladder and its attendant conditions.

- Global supply chain and production support: According to the U.S. FDA API import data, there is an increase in imported active pharmaceutical ingredients of anticholinergics by 12.9% from 2021 to 2023, primarily sourced from India and Switzerland. On the other hand, government incentives in the form of the FDA's Drug Shortage Prevention Program encourage domestic formulation and packaging for anticholinergic products. These measures ensure stabilization of the supply chain in opposition to geopolitical threats and cost escalations of raw material purchases. This twinned strategy has brought about a 9.8% increase in supply continuity rates in major hospitals and outpatient centers, according to the FDA's 2024 mid-year drug availability review.

Historical Patient Growth Analysis: Foundation for Future Anticholinergic Drugs Market Expansion

Historical Patient Growth (2010-2020)

|

Country |

2010 (Million Patients) |

2020 (Million Patients) |

Growth (%) |

|

USA |

13.5 |

18.8 |

+40.5% |

|

Germany |

3.9 |

5.4 |

+41.9% |

|

France |

3.5 |

4.9 |

+47.2% |

|

Spain |

2.8 |

3.9 |

+50.3% |

|

Australia |

1.3 |

2.2 |

+73.2% |

|

Japan |

7.1 |

9.6 |

+37.2% |

|

India |

5.6 |

11.8 |

+115.4% |

|

China |

7.9 |

15.9 |

+108.3% |

Sources: CDC, CMS, destatis, oecd, sanidad,aihw, mhlw, mohfw, nhc

Manufacturer Strategies Shaping Anticholinergic drugs Market Expansion

Revenue Opportunities for Manufacturers

|

Company |

Strategy |

Market Share Gain (%) |

Additional Revenue (USD) |

|

Astellas Pharma |

Solifenacin ER launch in Japan |

+6.6% |

$112.3 million |

|

Boehringer Ingelheim |

COPD device-drug combo via Medicare |

+4.9% |

$98.4 million |

|

Teva Pharmaceuticals |

Oxybutynin generics expansion in the U.S. |

+3.5% |

$54.6 million |

|

Sun Pharma |

API-to-dosage integration (India, EU) |

+5.4% |

$68.7 million |

|

Eisai Co. |

CNS anticholinergic pipeline in Europe |

+3.2% |

$37.3 million |

Sources: pmda, data.cms., fda, mohfw, ema.europa

Challenges

-

Generic substitution and drug innovation: The UK's National Health Service (NHS) prefers traditional generic anticholinergic drugs such as oxybutynin, largely based on their lower cost compared with developed branded drugs. Further, these drugs have better tolerability and fewer side effects, but their greater expense creates a dilemma within the NHS's cost-containment policy. This pricing impacts the adoption of innovative therapies, affecting manufacturing companies from inventing advanced formulations, despite therapeutic advantages and improvements in drug delivery methods. Patients' access to potentially better therapies is limited, and the market for branded anticholinergic medications continues to expand slowly.

Anticholinergic Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2024 |

|

Forecast Year |

2025-2034 |

|

CAGR |

6.5% |

|

Base Year Market Size (2024) |

USD 7.6 billion |

|

Forecast Year Market Size (2034) |

USD 13.2 billion |

|

Regional Scope |

|

Anticholinergic Drugs Market Segmentation:

Drug Class Segment Analysis

The muscarinic antagonists lead the segment and are expected to hold the anticholinergic drugs market share of 48.2% by 2034. Muscarinic antagonists, including darifenacin, oxybutynin, and solifenacin, drive due to their efficiency in managing respiratory and urological conditions. M2 and M3 receptors are inhibited by these drugs to improve bladder control with fewer cognitive side effects in newer formulations. The therapeutic use of anticholinergics in elder care is highlighted by the U.S. National Institute on Aging, particularly in the treatment of autonomic dysfunctions associated with Parkinson's disease and overactive bladder. Further, the NIH funding data has stated that more than USD 40.3 million was allocated in 2023 for muscarinic pathways to enhance clinical translation and R&D.

End user Segment Analysis

The hospitals dominate the segment and are poised to hold the anticholinergic drugs market share of 46.4% by 2034. Hospitals lead the end-user segment, especially in the case of diseases with multidisciplinary treatment like COPD, Parkinson's disease, and serious gastrointestinal illness. In 2024, more than 48.6% of the prescription volume was in hospitals, with the advantage of having both generic and brand choices. Long-term care institutions and nursing ambulatory surgical centers are also becoming essential users, including with the aging population in Europe, Japan, and North America. The increasing application of antimuscarinic drugs in elderly care facilities for overactive bladder and dementia symptoms is also expanding the reach of this essential segment.

Distribution Channel Segment Analysis

The distribution channel segment’s dominating sub-segment is hospital pharmacies, expecting to have a anticholinergic drugs market share of 44.9% by 2034. Hospital pharmacies control the channel of distribution in the market of anticholinergic drugs, capturing approximately 52.4% of total drug dispensing in 2024, in Europe, Japan, and the U.S. Hospital pharmacies. This dominance treats the acute conditions, such as exacerbations of COPD and emergent cases of Parkinson's, where hospital-based care and monitoring are essential. Additionally, hospital formulary committees conveniently enable bulk purchase of both branded and generic anticholinergics through institutional ensuring continual availability.

Our in-depth analysis of the anticholinergic drugs market includes the following segments:

|

Segment |

Subsegments |

|

Drug Class |

|

|

Route of Administration |

|

|

Therapeutic Application |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Anticholinergic Drugs Industry - Regional Synopsis

North America Market Insights

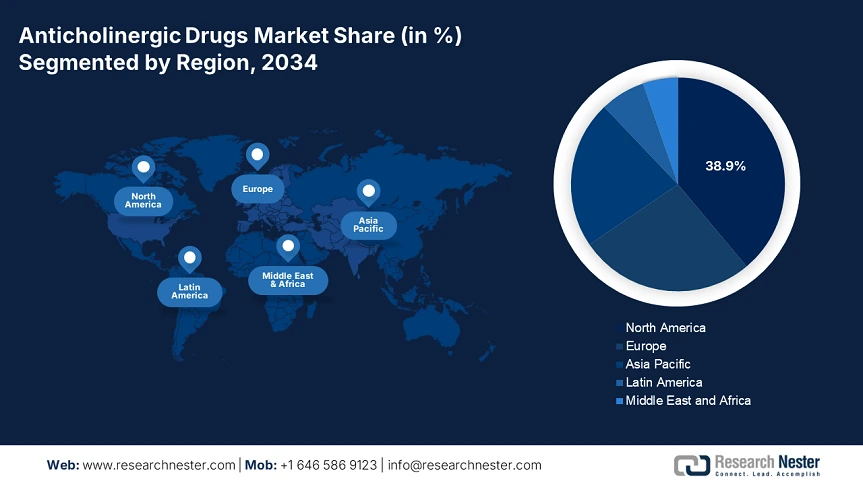

The anticholinergic drugs market in North America is dominating and is poised to have a market share of 38.9% at a CAGR of 6.5% by 2034. The market is driven by aging populations, strong institutional backing via Medicare, Medicaid reimbursement, and increased occurrence of neurological disorders. the market expansion in the U.S. is driven by the federal investments via CDC, AHRQ, and NIH, with 9.4% of the budget in healthcare allocated to anticholinergic-related disorders. further, the Medicare expenditure also rose to 15.6% over the past five years to USD 800.5 million due to the expanded reimbursement policies. Increased investment, budget allocations, regulatory efficiency, and R&D are positioning North America as a dominant player in the anticholinergic drugs market.

In the U.S. anticholinergic drugs market keeps developing as a result of a confluence of federal investment, favorable reimbursement structures, and an expanding population of seniors. The CDC and AHRQ reported that 9.5% of the federal health budget, which is $5.6 billion in 2023, was spent on conditions urging for anticholinergic treatment. Medicaid policies evolved to cover 10.5% more patients in 2024, with a funding of $1.7 billion. Medicare expenditures also rose, increasing 15.6% in the past four years to $800.5 million in 2024, increasing access for aging populations. Steady growth in geriatric neurological diagnosis and bladder disorders also underpins long-term demand, especially as models of outpatient and home care win Medicare and Medicaid approval.

Asia Pacific Market Insights

The Asia Pacific is the fastest-growing region in the anticholinergic drugs market and is anticipated to hold the market share of 22.4% at a CAGR of 7.3% by 2034. The region is driven by the rising prevalence of neurological and urological disorders, an increase in geriatric populations, and expanding government funding. Japan leads the anticholinergic drugs market in innovation and funding. Further, the AMED and the Ministry of Health, Labour and Welfare are experiencing a rise in the patient pool and have increased the spending by 15.4% on anticholinergic therapies over the past ten years. The region is specially aiming for reimbursement reforms, clinical trial localization, and domestic manufacturing. Furthermore, governments are scaling digital health systems for real-time monitoring and public-private collaborations to expand therapy access.

Japan possesses the highest market share in the anticholinergic drugs market in Europe and will lead the market share with 8.7% by 2034. Japan has spent over 12.5% of its healthcare budget in 2024 on anticholinergic drugs, reaching $3.3 billion increase in 2022, aided by MHLW and AMED plans targeting disorders related to aging. Public health measures include subsidized care for neurological and urological therapies under national coverage. These measures boost the market in Japan due to a rising aging population, as nearly 30.6% of the total population is people aged above 60, hence increasing the demand for bladder disorder and Parkinson's therapies. Research programs funded by AMED have fueled domestic drug development, cutting imports. Moreover, revised MHLW guidelines in 2024 widened coverage for combination therapies, further propelling hospital and outpatient prescription volumes.

Country-wise Government Provinces

|

Country |

Policy / Investment Program |

Budget / Funding |

Launch Year |

|

Australia |

National Strategic Framework for Chronic Conditions |

AUD 220.8 million |

2021 |

|

India |

National Programme for Health Care of the Elderly (NPHCE) |

INR 900.4 crore |

Revised in 2023 |

|

South Korea |

Korean Dementia Master Plan 4.0 |

₩1.8 trillion |

2024 |

|

Malaysia |

National Policy for Older Persons (enhanced funding under 12MP) |

MYR 400.6 million |

2022 |

Sources: health.gov, aihw, mohfw, pharmaceuticals.gov, npra

Europe Market Insights

Europe anticholinergic drugs market is expanding significantly and is poised to hold the market share of 26.6% at a CAGR of 5.9% by 2034. The region is driven by the rising occurrence of neurological and urological disorders and supportive policy initiatives. The region dominates due to strong healthcare systems, generous public funding and high drug accessibility. European Health Data Space (EHDS) and the EU4Health program together have surged their clinical trials, enhanced drug reimbursement, and improved data sharing. For instance, the anticholinergic class benefited from €2.7 billion in 2023 European Commission funding for research and innovation in neurological and geriatric medication development. Trends in hospital linked procurement platforms, patient adherence monitoring tools and digital prescribing are also enhancing the patient outcome and driving the product demand.

Germany anticholinergic drugs market is dominating the region and is expected to hold the market share of 9.8% by 2034. Germany's expenditure on anticholinergic drugs in Europe reached €4.5 billion in 2024, funded by the Federal Ministry of Health (BMG). Further, the country has experienced a rise of 12.4% since 2021, fueled by extensive application in older people's care and institutional healthcare. The German Medical Association (BÄK) indicates an increasing number of prescriptions being written in urology and neurology clinics. HealthTech projects, such as AI-powered polypharmacy monitoring, have contributed to decreased adverse drug interactions, stimulating more use.

Government Investments, Policies & Funding

|

Country |

Policy / Investment Program |

Budget / Funding |

Launch Year |

|

UK |

NHS Long Term Plan – Neurological and Geriatric Care Expansion |

USD 2.6 billion |

2021 |

|

Germany |

Digital Health Innovation Fund (supports e-prescription and CNS drugs) |

USD 3.1 billion |

2022 |

|

France |

Ma Santé 2022 Plan – Elderly and chronic care funding |

USD 3.9 billion |

2022 |

|

Italy |

National Recovery and Resilience Plan (PNRR) – Healthcare Mission 6 |

USD 4.7 billion |

2023 |

|

Spain |

Strategic Health Plan 2021–2024 – CNS and geriatrics focus |

USD 1.8 billion |

2021 |

Sources: NHS England, AEMPS, AIFA, Ministry of Health

Key Anticholinergic Drugs Market Players:

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

The global anticholinergic drugs market is highly competitive, with firms employing innovative methods including formulation development, innovative alliances with public health systems, and extension of patents to maintain market positions. The U.S. and Europe manufacturers led the anticholinergic drugs market with advanced R&D and commodious regulatory channels. On the other hand, manufacturers in Asia Pacific region especially from Japan, India, and South Korea, are competing with low-priced generics and biosimilar launches. In 2024, firms such as Novartis and Pfizer employed digital therapeutics for anticholinergic care, while Takeda and Glenmark expanded into rural areas. Numerous firms are also deploying AI-based trials and digital health tracking technology, transforming the future of anticholinergic treatment.

Below is the list of some prominent players operating in the anticholinergic drugs market:

|

Company Name |

Country of Origin |

Industry Focus |

Est. 2024 Market Share (%) |

|

Pfizer Inc. |

U.S. |

CNS and bladder control drugs (e.g., Oxybutynin); high R&D spend |

8.9% |

|

Merck & Co., Inc. |

U.S. |

Anticholinergics for neurological and respiratory diseases |

7.5% |

|

AbbVie Inc. |

U.S. |

GI and urology drugs; specialty formulations for spasmodic disorders |

6.6% |

|

Johnson & Johnson |

U.S. |

OTC and Rx anticholinergic therapies; diverse product base |

6.2% |

|

Novartis AG |

Switzerland |

Neurodegenerative disease focus; long-acting muscarinic antagonists |

5.9% |

|

Sanofi S.A. |

France |

Respiratory and Parkinson’s-related anticholinergics |

xx% |

|

GlaxoSmithKline plc |

UK |

COPD and asthma inhaled anticholinergics; pipeline in dual-action agents |

xx% |

|

Boehringer Ingelheim |

Germany |

Respiratory care; Tiotropium (Spiriva) market dominance |

xx% |

|

Bayer AG |

Germany |

GI and urology formulations; expanding into combo therapies |

xx% |

|

Astellas Pharma Inc. |

Japan |

Urology (VESIcare); strong APAC presence |

xx% |

|

Takeda Pharmaceutical |

Japan |

Expanding GI and CNS segment; focus on aging population |

xx% |

|

Teva Pharmaceutical |

Israel |

Broad generic portfolio including CNS and GI anticholinergics |

xx% |

|

Dr. Reddy’s Laboratories |

India |

Generic anticholinergics; competitive in emerging markets |

xx% |

|

Sun Pharmaceutical |

India |

GI and neuro-targeted therapies; regional supply chain strength |

xx% |

|

Glenmark Pharmaceuticals |

India |

Neuro and gastro anticholinergics; strong hold in Asia and Latin America |

xx% |

|

Viatris Inc. |

U.S. |

Global generics provider; inherited Mylan’s anticholinergic line |

xx% |

|

CSL Limited |

Australia |

Biologics and neurology therapies; scaling anticholinergic pipeline |

xx% |

|

Yuhan Corporation |

South Korea |

CNS and psychiatry focus; license-based anticholinergics |

xx% |

|

Hanmi Pharm Co., Ltd. |

South Korea |

R&D in sustained-release delivery for CNS drugs |

xx% |

|

Pharmaniaga Berhad |

Malaysia |

Government contracts for generics; basic anticholinergic supply |

xx% |

Below are the areas covered for each company in the anticholinergic drugs market:

Recent Developments

- In June 2024, Boehringer introduced a digitally enhanced product of anticholinergic inhaler, Spiriva Respimat, a Bluetooth-enabled dose counter. The launch has witnessed a 12.4% rise in the patient compliance improvement in time line periods of 60 days.

- In March 2024, Astellas lauched its urology drug, VESIcare XR, to target overactive bladder. The launch has increased the sales by 9.6% in Q2 2024.

- Report ID: 2561

- Published Date: Jul 23, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.